Part 2: Deep dive on Arista Networks ($ANET)

In order to read this entire deep dive on Arista Networks ($ANET) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (up +109.9% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up 109.9% YTD) and my trading portfolio (up +79.9% YTD) throughout the day including lots of charts, market opinions, macro analysis, earnings analysis, and much more.

Here are my other newsletters…

Company: Arista Networks

Ticker: (ANET)

Website: Arista.com

IPO date: June 2014

IPO price: $13.81 (split-adjusted, 4-for-1 stock split in 2021)

Current stock price: $206.84

Outstanding shares: 311.1 million

52 week high: $216.29 on November 6, 2023

52 week low: $107.57 on January 24, 2023

ATH: $216.29 on November 6, 2023

Market cap: $64.3 billion

Net cash/debt: $4.4 billion

Enterprise value: $59.9 billion

Headquarters: Santa Clara, California, United States

Number of employees: 3,600+

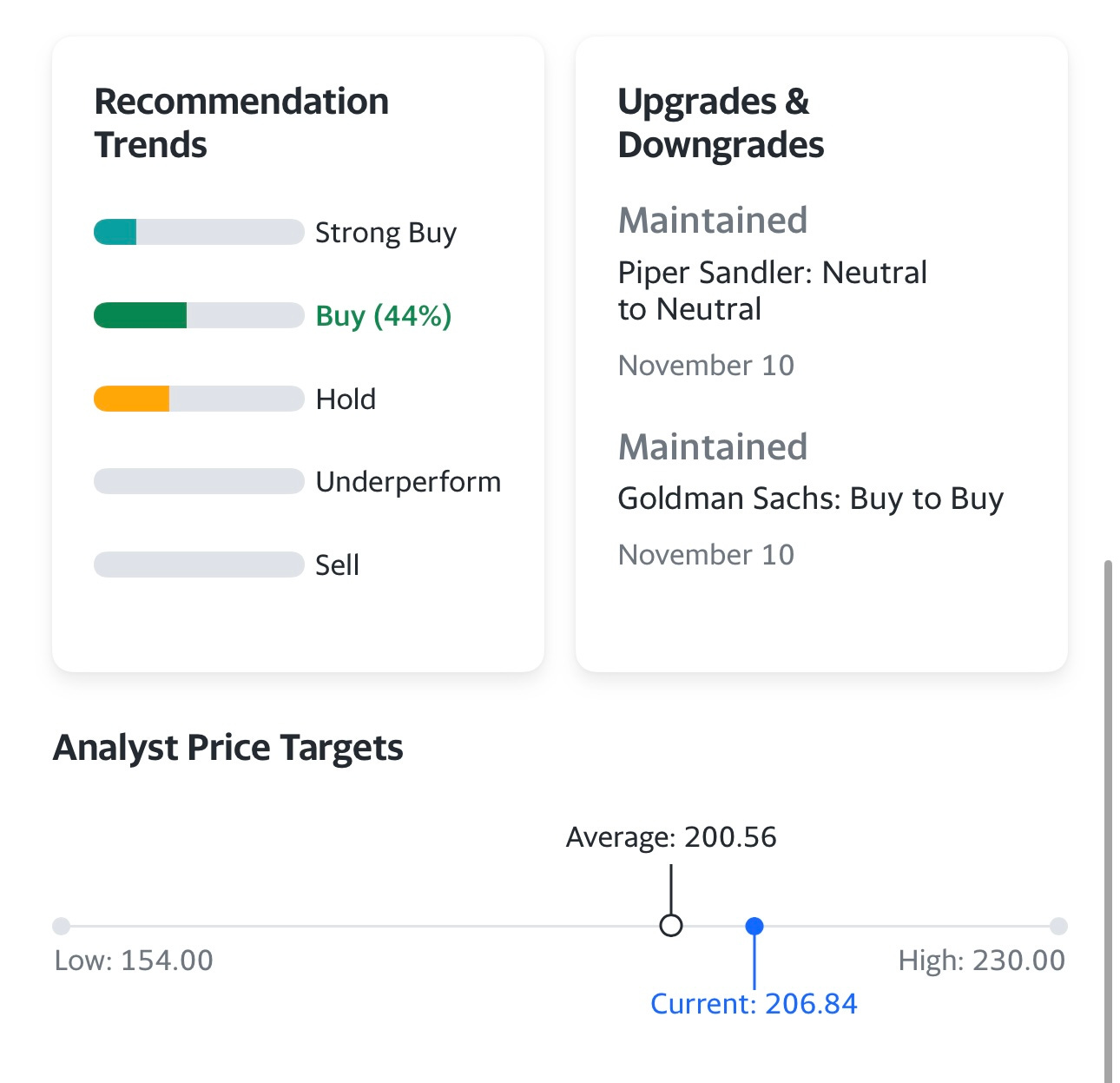

Average price target: $200.56 (Yahoo Finance) and $207.19 (StockTargetAdvisor)

Investor Relations: https://investors.arista.com

Q3 2023 Earnings Report [click here]

Investor Presentation October 2023 [click here]

Needham Networking, & Communications Conference [click here]

UBS Global Tech Conference [click here]

Wells Fargo TMT Summit [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 2]

In case you missed it, here is part 1 of the ANET deep dive…

Part 1: Deep dive on Arista Networks ($ANET)

In order to read this entire deep dive on Arista Networks ($ANET) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (up +105.2% YTD), my investment models and my daily webcasts.

Below the paywall is the Arista Networks ($ANET) deep dive along with links to my investment portfolio (up +109.9% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here]

My investment models [click here]

My daily webcasts [click here]

Valuation

ANET appears to be one of the market leaders and it’s certainly a high-quality company in the right sector but this is definitely not a cheap stock and my concern would be multiple compression over the next few years as growth slows down from the 30-50% range into the 10-15% range and it’s unlikely that margins can expand much further and certainly not enough to makeup for the slowdown in growth.

Using the current $59.9 billion enterprise value and the estimates below, ANET is trading

10.2x 2023 EV/SALES and 9.1x 2024 EV/SALES

23.3x 2023 EV/EBITDA and 21.1x 2024 EV/EBITDA

28.9x 2023 EV/NET INCOME and 25.9x 2024 EV/NET INCOME

I think these 2024 multiples would be fine if ANET was expected to growth revenues and earnings much faster next year, perhaps 2x faster because revenue growth and earnings growth in the low teens makes it hard to justify paying 25x 2024 earnings. I’m not saying ANET is super overvalued or the stock will crash but it’s hard to imagine the stock being a big outperformer over the next 12-18 months unless they blowout these estimates. ANET is already up 450% from the March 2020 lows so it’s hard to imagine we see anymore multiple expansion unless the future projections get much better and based on the company’s recent investor day I don’t think that is likely. Personally I think paying more than 1.5x NTM PEG ratio for a stock is asking for trouble so that’s why I’d be staying away from ANET as an investment but I’m certainly willing to trade it which I’ve been doing every week for the past couple months.

Investment Model

Here are my estimates which are just slightly ahead of the consensus estimates from analysts. As you can see if they only get to ~$9 billion of revenues in 2027 with 35.5% net income margins it means net income is only growing at 11.5% which means a 20 P/E would probably be on the high side and even with that you’re still not seeing much upside from here. This is a good example of a great company but not a great stock because the gains over the past few years have been massive which means the gains over the next few years are likely to be disappointing (that’s my opinion at this time).

In order for ANET to double over the next few years they’d probably have to do $11+ billion in 2027 with 35-40% net income margins in which case the P/E multiple might be closer to 25-30x and then you’re lookin at a $350-400 stock in 2027 but that would be very unexpected if it happens. I’m surprised the analysts are as bullish as they are on ANET given their low teens revenue growth projections. If you’re looking for tech/cloud/infrastructure, I think there are better opportunities elsewhere.

Analysts

Overall the analysts remain bullish with lots of buy ratings which is slightly confusing because the average price target in the low $200s (below the current price) however if you look at the last 15 price targets the average is closer to $220 but that’s still barely above the current price. Over the next few weeks I suspect some analysts will either keep a buy rating and raise their price target OR keep the price target and drop the rating from buy to hold citing the current valuation/multiple with slowing growth.

Here’s what the analysts are saying:

November 10th: Needham raised the firm's price target on Arista Networks to $235 from $215 and keeps a Buy rating on the shares. The analyst is citing the company's Analyst Day commentary, stating that the firm is a "buyer on weakness" as Arista offered 10%-12% growth in 2023 and 15% through 2027. Needham further contends that investors should look at the content of the Arista technology, the positioning for AI, the Network as a Service and the ability to drive into Enterprise and Campus.

November 10th: Barclays raised the firm's price target on Arista Networks to $230 from $226 and keeps an Overweight rating on the shares following the analyst day. The company announced more detailed 2024 guidance, in-line with consensus models, the analyst tells investors in a research note. The firm says that while some may be disappointed by the 20% long-term annual growth dropping to mid-teens, this is off a higher base and likely conservative. It remains positive on the shares.

October 31st: Needham raised the firm's price target on Arista Networks (ANET) to $215 from $210 and keeps a Buy rating on the shares. The company reported "another classic Arista quarter" with revenue growth ahead of target and also raised its outlook, the analyst tells investors in a research note. Arista's margins are now significantly above Cisco's (CSCO) 35% even as Arista takes significant share, the firm added.

October 31st: Evercore ISI raised the firm's price target on Arista Networks to $210 from $200 and keeps an Outperform rating on the shares following what the firm calls "another solid beat and raise" in the September-end quarter. The analyst, who thinks "a faster growing but better diversified" Arista "should end-up with a higher valuation going forward," sticks with the stock as its Top Pick.'

October 31st: KeyBanc raised the firm's price target on Arista Networks to $232 from $217 and keeps an Overweight rating on the shares post the beat/raise Q3 report. The firm sees Arista new Cloud and AI Titans segment guide as bullish.

October 31st: JMP Securities analyst Erik Suppiger raised the firm's price target on Arista Networks to $215 from $200 and keeps an Outperform rating on the shares. Arista reported Q3 results that beat consensus estimates and guided for FY23 growth of greater than 33%, up from previous guidance for greater than 30%, the analyst tells investors in a research note. Supply chain constraints are expected to normalize in 2024, the firm adds.

October 31st: Barclays raised the firm's price target on Arista Networks to $226 from $200 and keeps an Overweight rating on the shares. The company had another strong beat in Q3 and raised the full year guide, the analyst tells investors in a research note. The firm expects low double-digit growth in 2024 with acceleration in 2025 as artificial intelligence becomes more meaningful.

October 31st: Morgan Stanley analyst Meta Marshall upgraded Arista Networks to Overweight from Equal Weight with a price target of $220, up from $185. The analyst views Arista as the best way to play artificial intelligence networking's eventual move to ethernet. The company's Q3 results point to continued strength in cloud, despite investor caution, the analyst tells investors in a research note. The firm says getting past the CFO transition and conclusion of AI trials are catalysts for the shares.

October 16th: Evercore ISI is adding Arista Networks (ANET) to the firm's "Tactical Outperform" list ahead of the company reporting results. Arista "should continue their track record of beating guidance and it's possible we see one more increase to the full year guide," says the analyst, who adds that hyperscale capex commentary will remain favorable across key Arista customers. The firm remains "positively biased here" as it thinks customer EPS calls from Meta (META) and Microsoft (MSFT) could be positive for Arista and maintain an Outperform rating and $200 price target on Arista shares.

September 13th: BofA analyst Tal Liani raised the firm's price target on Arista Networks (ANET) to $225 from $190 and keeps a Buy rating on the shares after the firm virtually hosted 15 sessions at its Global AI Conference. Following the event, the firm raised its price targets for both Cisco (CSCO) and Arista based on its belief in the abilities of both companies to drive long-term AI growth and support the demand for AI-related bandwidth.

Technicals

As I mentioned above, ANET is not only up 450% from the March 2020 lows but also up 1,450% from the IPO in June 2014. It’s not surprising that ANET’s stock price has done very well because they did $584M of revenues in 2014 and now 10 years later they are expected to do $6.5+ billion in 2024 which is an 11.2x revenue increase however net income has gone from $105M in 2014 to an expected $2.312 billion in 2024 which is a 23.1x increase.

Just looking at this daily chart below you can see why I called ANET one of the market leaders. There was a selloff in October but the stock has recovered nicely and now back above all the moving averages. If you’re an investor I think you need to be very cautious about owning ANET for the reasons I mentioned above. If you’re a trader then I think ANET still looks attractive on pullbacks to the 10d ema.

Conclusion

My concerns with ANET are directly related to valuation and the risk of buying a stock at ~26x 2023 EPS estimates with EPS growth expected to be less than half of that which means ANET is trading with a 2024 PEG ratio above 2.0 which is something that doesn’t interest me. There are simply too many high-quality growth stocks trading PEG ratios below 1.5x and some that are even below 1.0x with better growth potential and better margin expansion potential.

I do these deep dives so we can not just uncover great investment opportunities but also analyze some of the current leaders to determine whether we should consider them or not. There are literally trillions of dollars in large mutual funds and hedge funds that are too big to own small/mid caps so they are forced to pay big premiums to own the best large caps which is one reason why stocks like ANET can trade at 26x 2024 EPS estimates and the analysts support it.

As I’ve probably mentioned before, my goal is to own ~20 stocks that I think can double over the next 3-4 years and ANET doesn’t fit the bill, I’d rather keep adding to stocks like CELH, SMCI, UBER, TMDX, LNTH, ONON, NU, MELI, DKNG, PLTR, etc — you should be following my investment portfolio at https://docs.google.com/spreadsheets/d/1oqNvhyZH76EWdQPM7faTjqCthvskiNPNCOIEG295raE/edit#gid=0

Additional Sources

Management – https://www.arista.com/en/company/management-team

Board of Directors – https://www.arista.com/en/company/management-team/board-of-directors

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/1596532/000119312523126846/d411423ddef14a.htm#toc411423_52 (page 65)