Part 1: Deep dive on Arista Networks ($ANET)

In order to read this entire deep dive on Arista Networks ($ANET) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (up +105.2% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up 105.2% YTD) and my trading portfolio (up +72.9% YTD) throughout the day including lots of charts, market opinions, macro analysis, earnings analysis, and much more.

Here are my other newsletters…

Company: Arista Networks

Ticker: (ANET)

Website: Arista.com

IPO date: June 2014

IPO price: $13.81 (split-adjusted, 4-for-1 stock split in 2021)

Current stock price: $206.84

Outstanding shares: 311.1 million

52 week high: $216.29 on November 6, 2023

52 week low: $107.57 on January 24, 2023

ATH: $216.29 on November 6, 2023

Market cap: $64.3 billion

Net cash/debt: $4.4 billion

Enterprise value: $59.9 billion

Headquarters: Santa Clara, California, United States

Number of employees: 3,600+

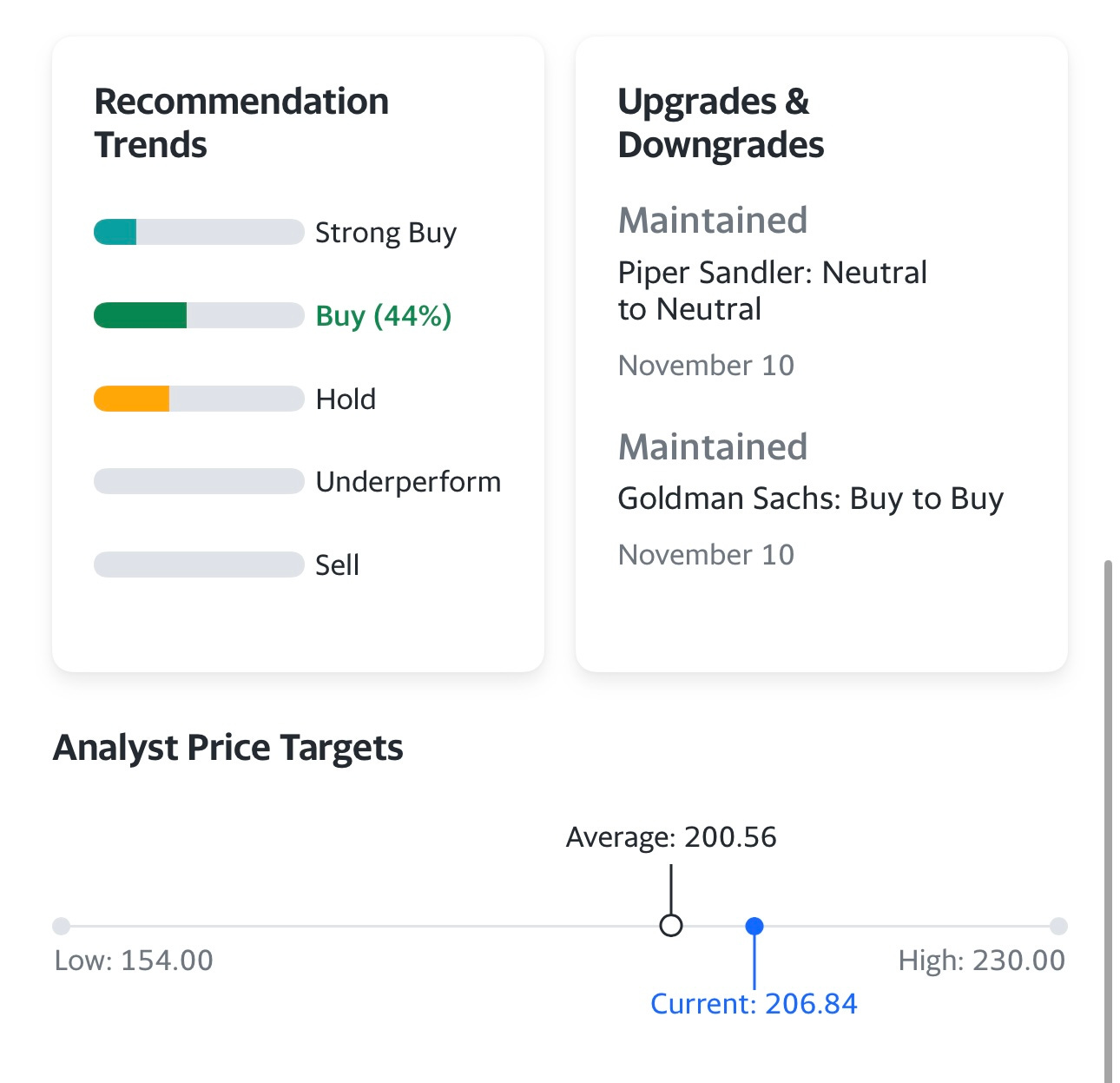

Average price target from analysts: $206.84

Investor Relations: https://investors.arista.com

Q3 2023 Earnings Report [click here]

Investor Presentation October 2023 [click here]

Needham Networking, & Communications Conference [click here]

UBS Global Tech Conference [click here]

Wells Fargo TMT Summit [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 2]

Below the paywall is the Arista Networks ($ANET) deep dive along with links to my investment portfolio (up +105.2% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here]

My investment models [click here]

My daily webcasts [click here]

Introduction

I do not currently have a position in ANET but I did earlier last week. Right now ANET does look like one of the market leaders (as you can see from the stock chart below) however there was a mini dip on Friday after the company provided rough future growth forecasts at an investor conference that were slightly below what some analysts might have been expecting. I got stopped out in both my portfolios when ANET sliced through the 10d ema, TBH I was probably a little aggressive with my stop loss on ANET but I’m trying to protect my year-to-date gains and not willing to take any big losses before year end.

ANET is a high-quality large cap tech company like PANW, CRWD, NOW, CRM and others however many of these stocks including ANET are selling at rich P/E multiples when you look out over the next few years. ANET is coming off a couple years of very strong growth and more companies migrate to the cloud including their two largest clients which are MSFT and META (they make up ~40% of ANET revenues) but analysts expect growth to slow down over the next few years (into the mid teens) but the problem with that for shareholders is that ANET already has amazing margins (so they won’t get much better) and the stock already trades at 21.1x 2024 EV/EBITDA and 28.7x 2024 earnings, neither of which is overly expensive but I definitely wouldn’t call the stock cheap and expect any significant multiple expansion which means ANET is likely to trade inline with the broad markets or even underperform if that P/E multiple starts to contract into the mid-teens which is more inline with revenue & earnings growth expectations over the next few years.

If megacap tech is grinding higher I think ANET will do just fine but if we run into a recession and macro because a headwind I won’t think I’d want to own a stock trading at almost 30x NTM EPS with growth rates in 2024 likely to be half of that number (ie ~15%).

ANET is already up 70% YTD but revenues are only expected to be up 33.5% in 2023 which means the stock has already seen some big multiple expansion this year therefore we likely need to see some consolidation on the charts.

If we do get a year end rally in the markets I would expect ANET to participate but I do think there are better places to put your money. I’m not always going to be bullish on every deep dive that I do however it’s important that we keep learning about more companies and trying to uncover new opportunities. After doing this ANET deep dive I now understand the company much better and I hope you will too.

In part 2 of the deep dive I’ll go through the valuation and investment models in more detail but here’s a sneak peak at my estimates for the next 4+ years which shows why I’m not super bullish on the company… the growth estimates just don’t leave enough upside to get me excited.

Company Background

Arista Networks was founded in 2004 by industry luminaries Andy Bechtolsheim (still with the company, serves as a Chief Development Officer and owns approximately 15% of the company worth ~$9.7 billion), Ken Duda (serves as a Chief Technology Officer and Senior Vice President, Software Engineering), and David Cheriton (left the company in 2014 and sold all of his shares since then).

Andy Bechtolsheim previously co-founded Sun Microsystems in 1982, where he was the Chief System Architect responsible for next-generation server, storage, and network architectures. Together with David Cheriton, Bechtolsheim also co-founded Granite Systems in 1995, the company that developed Gigabit Ethernet products.

Granite Systems was later acquired by Cisco, and Bechtolsheim, Cheriton, and Ken Duda (Granite Systems' first employee) ended up at Cisco, where they worked for the next seven years.

The three left Cisco in 2004 to found Arastra (later renamed to Arista). For about four years, they have been working on their own network operating system – software that controls and coordinates network resources and services, enabling computers and devices to communicate and share resources with each other in a network environment. Examples of network operating systems include Microsoft Windows Server, Linux-based systems like Ubuntu Server, and Novell NetWare.

Arista's network, EOS, was launched in 2008, and it became the first fully programmable and highly modular Linux-based network operating system, running as a single binary software image across the Arista switching family of products. EOS was architected for resiliency and programmability and had a unique multi-process state-sharing architecture, different from the architectures of other network operating systems.

This architecture also provided low latency, which was critical for financial institutions that started to use EOS for their high-frequency trading applications. Soon, big data customers across various industries began using EOS, too. The early commercial success of EOS had brought the need for someone more experienced to run and grow the company while founders could focus on developing EOS further.

That same year, Jayshree Ullal joined Arista. Ullal was the ideal candidate for this role, previously serving as a Senior Vice President at Cisco, where she was responsible for a $10 billion business in data center, switching, and services. She has led the company ever since, growing Arista literally from zero to a multibillion-dollar business while being recognized as an “Entrepreneur of the Year” by E&Y’s in 2015, “World’s Best CEOs” by Barron’s in 2018, one of Fortune’s “Top 20 Business persons” in 2019, and one of the most respectful leaders in the networking industry. She still holds approximately 3.35% of the company, worth around $2.2 billion.

Under Ullal's reign, Arista started working with early cloud companies, a pivotal moment in the company's history. Arista was not only at the dawn of the cloud revolution but also its enabler. So, in 2010, Arista introduced a 7500 Spine switch with increased performance and port density.

It forever revolutionized networks from a legacy three-tiered architecture to a flatter two-tiered spine-leaf approach, delivering unprecedented cloud scale with reliable wire speed performance while providing cost savings to customers. From that point, Arista became profitable and cash flow positive and has stayed such ever since.

The business was indeed proliferating. By the time Arista went public in June 2014, it had sold 2 million switch ports, resulting in over $360 million in revenues in 2013 (an increase of 87% YoY) and $117.2 million in the first quarter of 2014 (an increase of 91% YoY). The stock started to trade at $43 per share (~$13.81 split-adjusted), well above its expected price range of $36-$40. Arista raised $226 million, valuing the company at about $2.75 billion (Arista is a $66 billion company today).

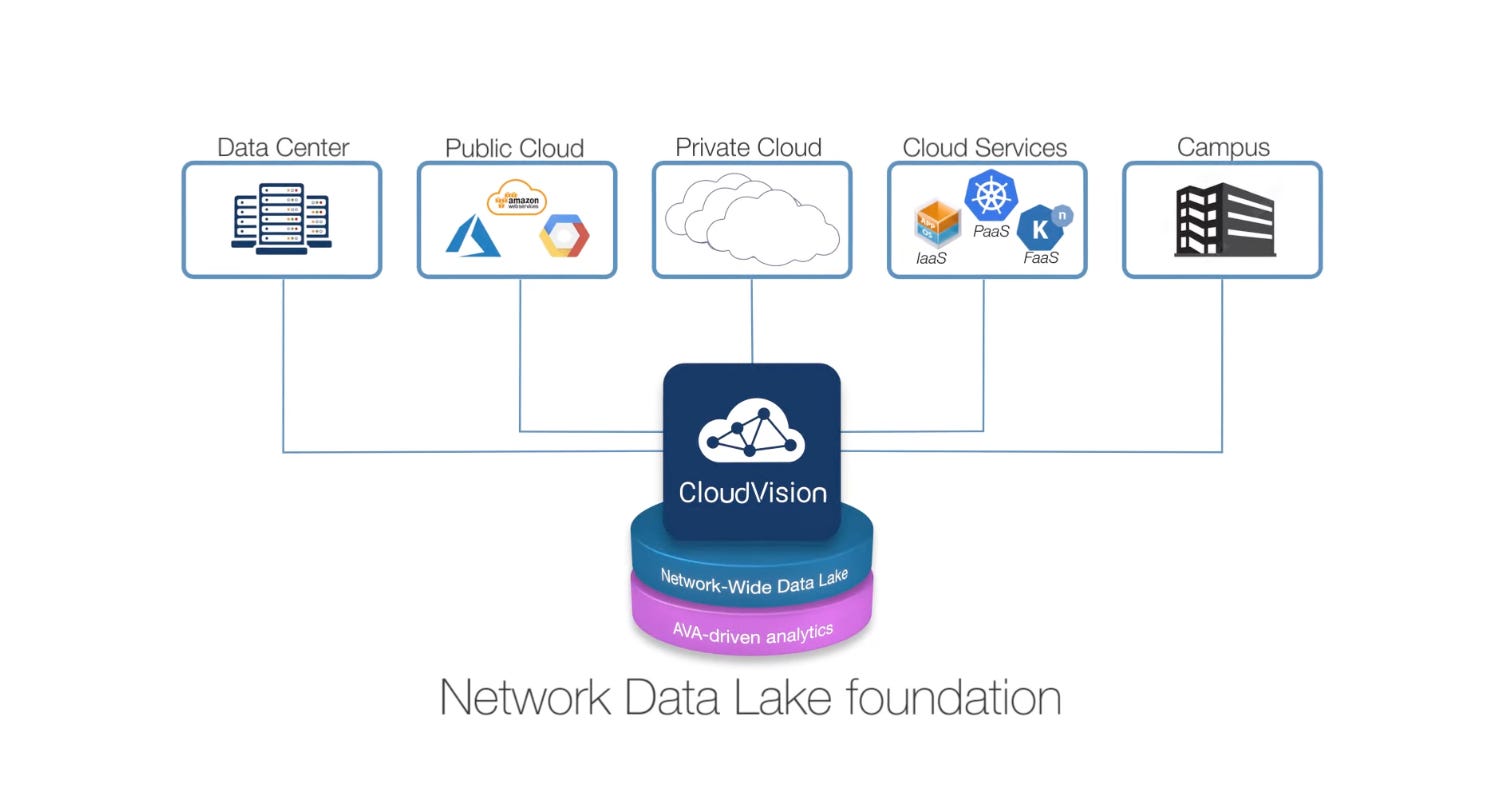

The second significant event in the company's history happened in 2015 with the introduction of CloudVision, a workload orchestration and automation solution that leverages EOS to deliver turnkey automation and configuration capabilities across data center, wired and wireless workspaces, multi-cloud, and WAN routing use cases – greatly reducing network operational costs. CloudVision allowed Arista to expand from the data center to the multi-cloud to the cognitive campus – three distinct markets in which the company operates today.

In the years following the launch of CloudVision, Arista has continued to grow and innovate within the networking industry. A lot of innovation came from numerous acquisitions the company made starting in 2018. That year, Arista finally reached a settlement with Cisco, the battle which lasted for four years and cost the company $400 million. As part of the settlement, Cisco dropped all infringement claims while Arista's antitrust claims against Cisco were also dismissed, and the two companies agreed to stand down for five years.

The next few years were challenging for Arista, with revenue declining in 2020 due to COVID-19 and 2021 being a year of transformation. The big breakthrough came in 2022, when the company's revenue skyrocketed to $4.38 billion, growing almost 50% YoY as a result of record sales of its switching and routing products, highlighting strong demand from its customers.

Arista has a prestigious set of customers, including Fortune 500 global companies. In total, the company serves over 9,000 customers, including large internet companies, service providers, financial services organizations, government agencies, media and entertainment companies, telecommunication service providers, and other cloud service providers. However, almost 40% of its total revenue comes from just two customers: Microsoft and Meta. Both of these customers have been growing their purchases from Arista in the last several years while actively building out its AI and metaverse empires.

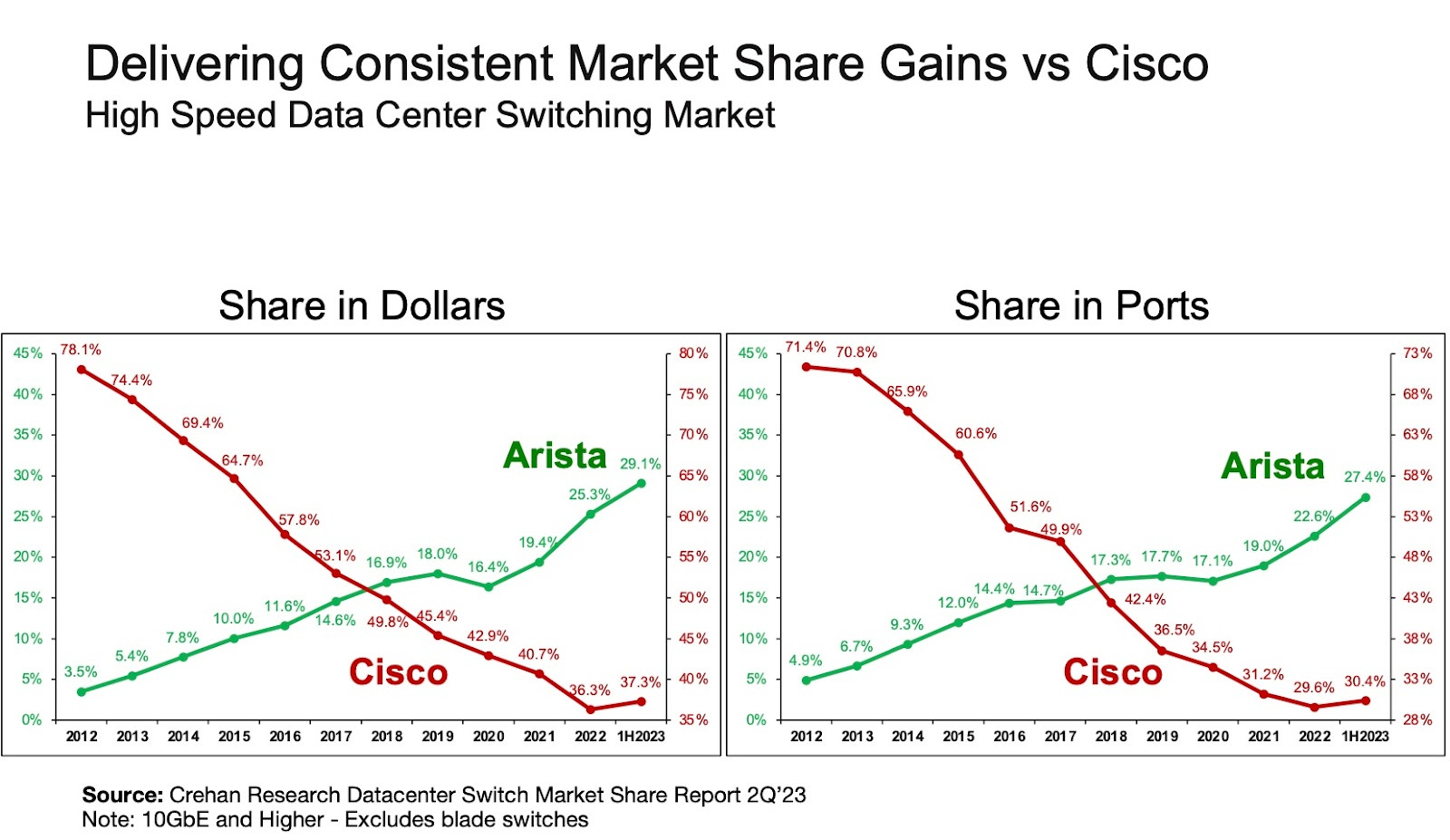

As a result, Arista achieved the second-largest market share in data center Ethernet switch ports and revenue after Cisco. But Arista is rapidly eating Cisco's share while the overall opportunity is growing. And as Ethernet is slowly replacing InfiniBand as a primary AI networking, Arista is best positioned to win in the AI data center buildout and emerge as the leader in this rapidly growing, already ~$25 billion AI networking market.

Opportunity

Arista Networks operates in the business of internet infrastructure. The majority of the backbone of the Internet runs on Arista's products, including both its proprietary hardware (switches) and software (EOS, CloudVision) needed to operate the hardware.

The company's primary market is the high-speed data center switching market for 10 Gigabit Ethernet and above. After adding routing capabilities to some of its switches, Arista began addressing the Data Center Interconnect (DCI) market, cloud-grade routing, next-generation network edge, and wide area networking routing market. The company also operates in the enterprise campus market for 1 Gigabit Ethernet switching and above and in the cloud-managed wireless networking market.

Arista primarily sells switches – devices that connect multiple other devices on a computer network by using packet switching to receive, process, and forward data to the destination device. A switch only sends the necessary data to the device that needs it, which makes networks more efficient.

Trends

Digital transformation / move to the cloud

Digital transformation has fundamentally changed the way IT infrastructure is built and how applications are delivered. With the move to the cloud, applications are now distributed across thousands of servers, which are interconnected by high-speed networking switches.

These switches play a critical role as they form a pool of resources that allows applications to be rapidly deployed and cost-effectively updated. Cloud computing made it possible for these applications to be accessed by internet-connected devices, including personal computers, tablets, Internet of Things (IoT) devices, and smartphones.

Today, nearly all consumer applications are delivered through the cloud. This shift from traditional legacy network architectures to client-to-cloud networking was initially pioneered by today's internet leaders – Amazon, Google, Microsoft, and Meta. To meet the growing demand for their services, these companies began building large-scale cloud data centers before making them available to thousands of other companies.

Among these companies are large enterprises that have traditionally been slower to adapt to innovation. However, enterprises are now rapidly moving to the cloud as cloud services become more accessible and cost-effective than traditional applications, providing scale unmatched prior.

Services in the cloud generate a magnitude higher bandwidth than typical legacy data center networks. Networks in such cloud environments (cloud networks) must be architected and built in a new way: they must provide high capacity, availability, and performance. They should also be programmable for third-party integration to manage networks, automate tasks, and orchestrate services.

As organizations of all sizes are moving their workloads to the cloud, spending on cloud and next-generation data centers will only grow in the coming years, while traditional legacy IT spending will see a decline over time.

Transition to 400G

The term "400G" in networking refers to the next generation of network speeds that support data transfer rates of 400 gigabits per second (Gbps). This represents a significant leap from the previous standard of 100G, quadrupling the potential bandwidth.

The demand for 400G has surged due to the remarkable increase in data traffic, primarily driven by the proliferation of Internet of Things (IoT) devices, cloud computing, and video streaming. As the number of devices connected to the Internet continues to rise and the need for faster Internet speeds increases, the infrastructure that handles this data must continuously evolve to keep up with the demand.

The primary advantage of 400G technology is its ability to handle more data simultaneously, which is critical for supporting bandwidth-intensive applications, such as 4K video streaming, virtual reality, and advanced cloud-based services.

400G networks also make more efficient use of the available infrastructure, vital for reducing operational costs and energy consumption. At the same time, 400G enables scalability, as it requires fewer cables and less hardware to deliver higher throughput, making it easier to expand network capacity as demand increases.

For applications that require real-time responses, such as online gaming, stock trading, and certain types of scientific research, 400G can help reduce latency.

Higher bandwidth networks like 400G are considered the foundational technology for next-generation networking standards like 5G, and while 800G networks are already seen on the horizon (currently used by the largest players in the data center industry for their own purposes), 400G will remain the primary standard for years to come, and the transition to it will only accelerate.

Integration of AI into networks (AI networking)

AI networking refers to the integration of artificial intelligence (AI) into network management and operations. As modern networks become more complex (comprising countless devices) and see higher demands (different traffic types), they require more automation, predictive analytics, and self-optimizing capabilities beyond what humans can do.

AI can analyze large amounts of network data to detect anomalies, optimize traffic flows, predict outages, and respond to real-time changes. This improves the performance, security, and reliability of the network.

As AI and distributed applications continue to expand, they present new challenges for scaling and performance in networks. AI workloads are typically data and compute-intensive, involving large sparse matrix computations that are distributed across hundreds or thousands of processors (CPU, GPU, TPU, etc.). These computations are highly intensive and require a high-bandwidth, scalable, and lossless network to service them. Thus, a network with these characteristics is essential for supporting such workloads.

The need for these intelligent and adaptive networks will only grow in the coming years. AI will completely reshape how networks are managed and operated.

The evolution of campus networks

A campus network refers to a computer network that connects local area networks (LANs) within a specific geographical area, like an office building, university campus, or government facility. Such a network is supported by equipment such as switches and routers, as well as communication media like optical fiber or copper cabling.

Campus networks have undergone significant evolution to adapt to changing technology and growing demands for connectivity and data transfer. Traditional wired and wireless campus networks now need to accommodate an increasing number of IoT devices and remote work locations, allowing users to be connected from anywhere.

Managing the increasingly complex campus networks has become a major challenge for administrators. To tackle the problem, they have adopted various platforms, operating systems, proprietary features, and network management tools. However, the explosive growth of IoT and the need for remote workloads have worsened the situation, leading to prohibitively high operational costs.

Campus networks are now increasingly moving towards more intelligent, automated, and flexible networks that can adapt to changing needs and incorporate cutting-edge technologies such as Wi-Fi 6, 5G, and even AI-driven network management to ensure that they remain at the forefront of technological innovation.

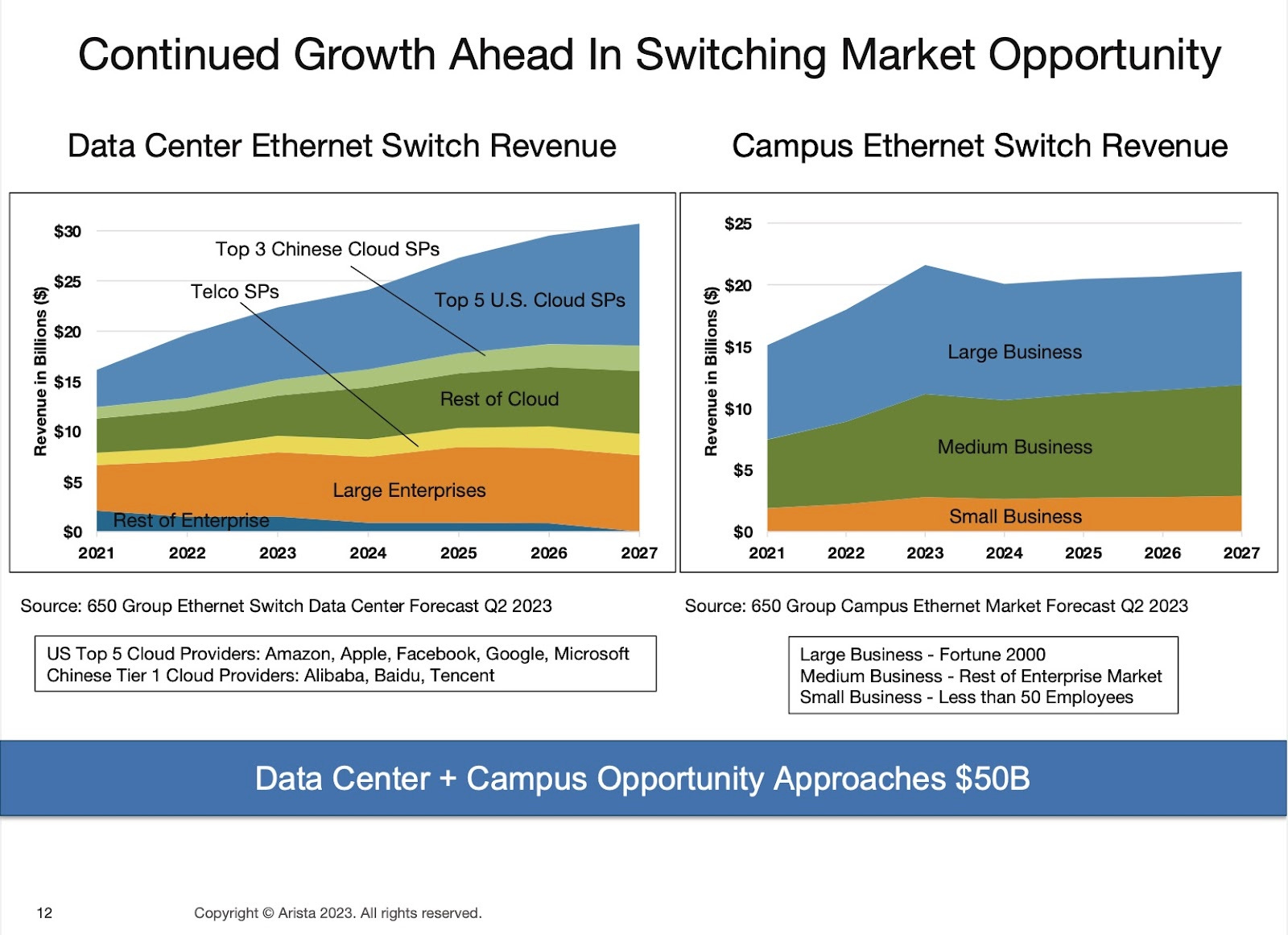

Total Addressable Market (TAM)

Arista's primary market, the high-speed data center switching market (both data center and campus), is estimated to be approximately $45 billion today. This is a large and fast-growing opportunity that could exceed $50 billion by 2027.

Arista is on its way to delivering $5.85 billion in revenue in 2023, which represents ~13% of the current market opportunity.

Growth Drivers

After navigating through the COVID-19 year and the year after, Arista had a fantastic financial year in 2022, delivering almost 50% YoY growth and 55% growth compared to the pre-COVID year. In 2023, the consensus among analysts is $5.85 billion in revenue, representing a solid 33% YoY increase.

Management remains optimistic about double-digit growth in 2024 and 2025, though it will be significantly less, somewhere in the low teens.

Despite "muted" times for the cloud ahead due to a highly robust infrastructure buildout over the last few years, Arista still has strong catalysts for growth during and beyond this period.

The company will likely use the coming years to transform into what management calls Arista 2.0, which is largely centered around AI networking.

AI networking

The next phase for Arista is really building a platform for all of what the company has already done for the cloud and Web 3.0, but now bringing that to AI clusters in the back end of the network.

For 25 years, the back end of the network was primarily InfiniBand, a high-performance, low-latency networking technology used mainly in supercomputing and enterprise data centers. It's a communications standard for interconnecting servers, storage systems, and other data center hardware to facilitate fast data transfer and scalability.

Today, InfiniBand is the most commonly used technology (primarily because of its low latency) bundled with Nvidia's GPUs when building AI-driven data centers. However, Ethernet will eventually win over InfiniBand as the technological difference between the two is rapidly shrinking.

Historically, Ethernet has always lagged. When InfiniBand was doing 40G, Ethernet was doing just 10G. When InfiniBand went to DDR, EDR, MDR, and HDR rates and was always doubling, Ethernet was always behind. But that changed dramatically in the past year. Today, Ethernet can do 100G, 200G, 400G, and 800G (InfiniBand won't be able to do 800G for another several years at minimum). There is even a path to 1.6 terabytes. This makes Ethernet a natural standard-based ecosystem with a wide level of capability and troubleshooting techniques. Furthermore, Ethernet is by far more popular globally, with over 600 million ports shipped every year. Ethernet will be the primary choice for AI-driven data centers going forward.

Another reason Arista will be a big winner in the ~$25 billion AI networking market is its agnostic approach: the company works with any GPU vendor, whether Nvidia, Broadcom, or Intel.

AI presents a long-term tailwind for the entire networking space and specifically for Arista, given its high-end Ethernet share.

Enterprise switching market

The enterprise switching market is a segment of the network hardware industry that focuses on selling switches for enterprise networks. These switches are crucial components that connect devices within a local area network (LAN) in businesses, organizations, and institutions.

This market includes a range of products, from basic unmanaged switches to sophisticated managed and multi-layer switches that offer advanced features such as security, traffic management, and network monitoring.

The need for reliable, efficient, and secure networking within corporate environments drives the demand in this market, and Arista will continue to gain a share of the enterprise switching market going forward. Its share in 2022 was just 10%, but analysts expect it to grow to 27% by the end of 2027.

The big catalyst for the growth in this market is the growth of the data center Ethernet switch segment. This segment alone is a $20 billion opportunity, which is anticipated to grow to $30 billion by the end of 2027.

So, Arista will not only increase its share of the enterprise switching market but will also see the market growing in size and overall opportunity.

Expand with current customers

Arista sells its products and services to over 9,000 customers across the globe. Every single one of these customers represents an opportunity to sell more products, especially in the new product cycle.

While the next several years are expected to be largely "muted" due to high spending on Internet infrastructure in previous years, some customers will continue expanding their networks regardless and will require more products from Arista.

This is especially true with Arista's two main customers, Microsoft and Meta, which currently represent almost 40% of its total revenue. Both companies will spend big on servers, AI, and AI hardware in the coming years. Microsoft continues to build data centers for OpenAI, while Meta is working on several large projects, including its own AI and metaverse. Meta alone is expected to spend between $30 billion and $35 billion in 2024 on capital expenditures (the large part will be spent on servers) after spending almost $30 billion in 2023.

Selling more products to Microsoft and Meta is the company's near-term catalyst.

Expansion into new markets

Arista is diversifying its product line by expanding into new segments like campus switching and WiFi networking markets, aiming to tap into new revenue streams.

The company is also entering new markets, like the healthcare sector, with its Network-as-a-Service offering. This innovative approach integrates Arista's flagship EOS, CloudVision, and Arista CUE platforms to bolster healthcare network infrastructures.

Such expansions broaden Arista's market reach and present additional growth opportunities.

Growing partner ecosystem

Partnership relationships are key to new customer growth for every company. Arista sells a lot of its products through partnerships with its channel partners (including distributors, value-added resellers, systems integrators, and original equipment manufacturer (OEM) partners) and in conjunction with various technology partners, among which are AWS, Google Cloud, Azure, VMware, Splunk, Zscaler, SentinelOne, ServiceNow, and many others.

To engage partners who provide value-added services and extend their reach into the marketplace, Arista created a partner program, the Arista Partner Program. Authorized training partners perform technical training of Arista's channel partners and end customers. These partners commonly receive an order from an end customer before placing an order with Arista. Arista ships the order directly to the end user and pays a commission to the partner.

Business Model

Arista's business model is centered around providing high-end, scalable networking solutions primarily for data centers, cloud computing environments, and large-scale internet companies like Meta. Arista focuses not on the 'compute' part but the networking systems that enable high-speed communication between computing resources.

The company generates revenue primarily from sales of specialized, high-performance networking hardware (Product revenue) like switching and routing products, incorporating its EOS software and related network applications to offer flexibility and customization.

Arista also generates revenue from post-contract support (PCS) and renewals (Service revenue), which end customers typically purchase with the products on a recurring basis.

Product revenue represents the majority of total revenue (86%). However, the share of service revenue has been steadily growing, and the company is looking to significantly increase the recurring revenue in the coming years, partially by pushing more Software-as-a-Service offerings.

Arista geographically sells all around the globe, but the majority of customers come from North America (80%), followed by Europe, the Middle East and Africa (~11%), and Asia-Pacific (~9%).

Gross Margin

For a primarily hardware company, Arista has a pretty solid gross margin of ~62% (GAAP), in line with its main competitor, Cisco.

There is a slight gross margin expansion expected in the coming years, but no more than 100-200 bps.

Financial Snapshot

Based on Q3 2023

Revenue

Actual:

2022 – $618 million (+25.5% YoY)

Q3 2023 – $1.50 billion (+28.3% YoY)

Nine months of 2023 – $4.31 billion (+39.1% YoY)

Guidance:

Q4 2023 – $1.5 billion to $1.55 billion (+25% YoY)

Estimates:

2023 – $5.84 billion (+33.5% YoY)

2024 – $6.52 billion (+11.6% YoY)

Operating Expenses

2022 – 26.2% of total revenue

Q3 2023 – 22.5% of total revenue

Nine months of 2023 – 23.4% of total revenue

Although operating expenses have increased in absolute dollars, their percentage of total revenue has consistently decreased from 42% in 2016 to 33% in 2020 to 26.2% in 2022.

The company achieved a record operating margin of almost 40% (GAAP) and 42% (non-GAAP).

Stock-based compensation (SBC)

2022 – 5.27% of total revenue and 0.36% of the market cap

Nine months of 2023 – 4.99% of total revenue and 0.33% of the market cap

The company is on its way to exceeding SBC in 2023 compared to 2022.

Since going public, Arista has increased its shares outstanding by just 22.3%, while its stock price has appreciated more than 1,400%.

Profitability

Arista has been profitable on a GAAP basis since 2010. In 2022, the company generated $1.35 billion in net income and is on the verge of delivering $1.9 billion in 2023, a 41.9% increase compared to the year prior.

Analysts expect a significant slowdown in net income growth starting in 2024, forecasting the growth in the low teens. The company is still expected to deliver almost $3 billion in positive earnings by the end of 2023.

Balance Sheet

As of Q3 2023, Arista had $4.45 billion in cash, cash equivalents, and marketable securities, compared to $3.74 billion a quarter prior. The company has just $67 million in debt.

Management plans to maintain a healthy balance sheet and invest back into the business to compete aggressively with the company's primary competitor, Cisco.

The company has a share repurchasing program in place to offset dilution and return cash to shareholders (if the price is below a reasonable range estimate of intrinsic value).

Arista does not currently pay dividends, but it is on the management's map.

Cash Flow

Arista turned free cash flow (FCF) positive in the same year as it became profitable.

After a deceleration in 2022, when the company generated $448 million in FCF compared to almost $1 billion in 2021, it is expected to deliver $1.7 billion in FCF in 2023, an increase of over 170% compared to 2022.

Analysts expect steady growth from there, growing another 40% in 2024 before slowing down to low mid-teens in the years after. In 2027, Arista is expected to generate over $3 billion in FCF.

Competitive Advantages

Arista Networks operates in a highly competitive market with rapidly evolving technologies and frequent product introductions (fast product cycles). It faces intense competition from established companies like Cisco, Extreme Networks, Dell/EMC, Hewlett Packard Enterprise, and Juniper Networks.

Cisco has been Arista's primary competitor in the switches and routers business – 70% of Cisco's revenue still comes from this business. However, Arista has been slowly eating Cisco's share for many years, and there is still a lot to gain.

Arista has a much superior product for the Hyperscalers, so the Cloud Titans primarily choose Arista's products. Arista now has superior products for the Enterprises, both cloud and campus. So, Arista is not only eating Cisco's share (which offers growth opportunities on its own for at least the next five years) but also a share of new networks, especially AI-based.

The secret of winning is in its unique technology, especially the extensible operating system (EOS), which runs a single image across all devices and gives Arista a competitive edge by simplifying network operations and enhancing performance. EOS and best-in-class merchant-switching silicon with superior performance, delivery, and power efficiency are integrated to create next-gen switching systems unmatched by its rivals.

EOS software provides another competitor advantage to Arista: its highly modular structure allows the company to rapidly deliver new features and applications while preserving the structural integrity and quality of its network operating system. This enables Arista to provide new features and capabilities more quickly than any other legacy switch/router provider can. It is critical in the rapidly evolving cloud and next-generation data center and campus networking market.

Arista's leadership and quality have been recognized by various industry experts.

In this industry, management plays a vital role. While Cisco's leadership has been lousy in recent years, Arista's management has been firing on all cylinders. Its team consists of networking veterans with extensive data center and campus networking expertise. Arista's President and Chief Executive Officer, Jayshree Ullal, has over 30 years of networking expertise and is recognized as one of the most influential people in the industry. Andy Bechtolsheim, Arista's Founder and Chief Development Officer, was previously a founder and chief system architect at Sun Microsystems.

These people have established deep and close working relationships with many of its largest customers. This provides Arista with valuable insights into their needs and future requirements, helping to be the first to develop and introduce new products and continuously build its leadership position.

Risks

The next several years will be "muted" for the networking industry due to elevated spending on the infrastructure in the previous several years and upcoming recession;

A significant drop in revenue growth starting in 2024, with estimates in the low teens;

A significant customer concentration risk with two customers, Microsoft and Meta, accounting for approximately 40% of the total revenue;

Risk related to the networking industry heading to 800G cycle (from 400G), which will require significant capital investment from Arista;

Dependence on just one product segment – switches;

To build a mission-critical AI network, Ethernet technology must significantly evolve from its current state, which would take several years;

Arista does not manufacture its products and works with third-party manufacturers, having less control over the price and entire process.

Additional Sources

Management – https://www.arista.com/en/company/management-team

Board of Directors – https://www.arista.com/en/company/management-team/board-of-directors

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/1596532/000119312523126846/d411423ddef14a.htm#toc411423_52 (page 65)

Have a great week!!!

~Jonah

You can follow me on Twitter at @JonahLupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.