Part 1: Deep dive on VTEX ($VTEX)

In order to read this deep dive on VTEX ($VTEX) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support.

Paid subscribers receive ~3 deep dives per month (~8,000 words) and ~3 mini deep dives per month (~2,000 words) plus access to my current investment portfolio (up +135.2% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up +135.2% YTD) and my trading portfolio (up +98.8% YTD) including morning newsletter, daily activity updates, stock charts, market opinions, macro analysis, earnings analysis, analyst upgrades/downgrades, webcasts and much more.

Company: VTEX

Ticker: (VTEX)

Website: https://vtex.com/us-en/

IPO date: July 21, 2021

IPO price: $19.00

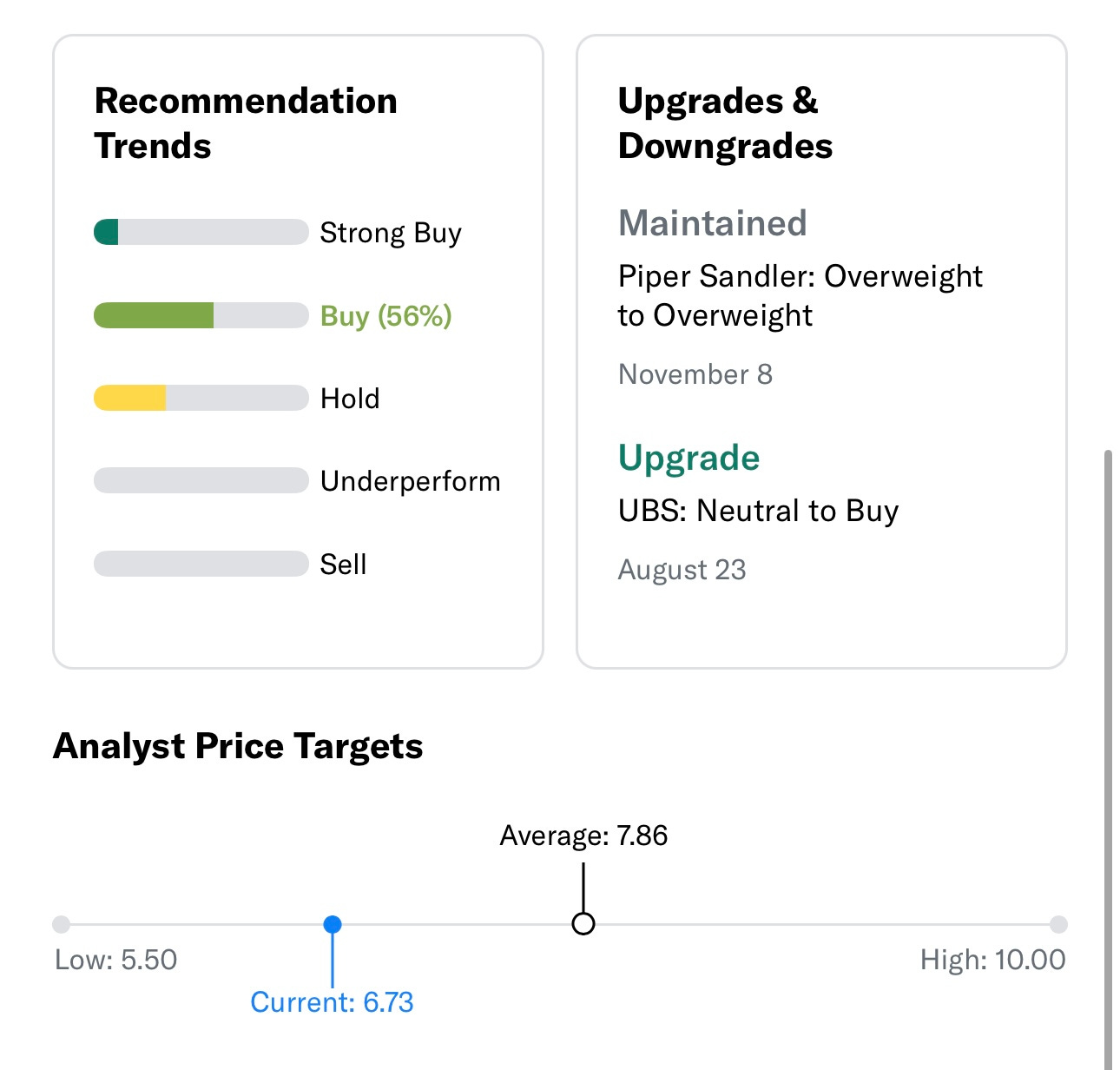

Current stock price: $6.73

Outstanding shares: 187.82 million

52 week high: $7.15 on November 20, 2023

52 week low: $3.18 on December 22, 2022

ATH: $33.36 on August 10, 2021

Market cap: $1.26 billion

Net cash/debt: $209 million

Enterprise value: $1.05 billion

Headquarters: London, United Kingdom

Number of employees: 1,270+

Average price target from analysts: $7.86 (only a few analysts cover VTEX)

Investor Relations:

https://www.investors.vtex.com/

Q3 2023 Earnings Report: https://s28.q4cdn.com/761427389/files/doc_financials/2023/q3/_VTEX-3Q23-Earnings-Press-Release-pptx.pdf

Business Overview (November 2023): https://s28.q4cdn.com/761427389/files/doc_financials/2023/q3/VTEX-3Q23-Earnings-Presentation.pdf

Investor Day (July 2023): https://s28.q4cdn.com/761427389/files/doc_presentations/07/VTEX-Investor-Day-2023.pdf

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1]

Many investors and Wall Street strategists believe that 2024 will be a very strong year for small/mid caps and I agree.

Over the past 28 years the Russell 2000 (aka IWM) has only had 4 double digit negative years (2002, 2008, 2018, 2022) however the combined returns of the 2 years following those negative double years is 51.5% and with $IWM currently up 17.5% YTD that means next year IWM could be setting up for a monster year. FWIW, the average of the 5 best years since 1995 is 31.5% and I think it’s possible if inflation continues coming down and the FOMC starts cutting rates while the economy and labor markets remain strong.

Several weeks ago I ran a stock screener looking for companies with market caps between $1 billion and $10 billion that are expected to grow revenues by 20% or more in 2023, 2024 and 2025 while being EBITDA positive in 2023, 2024 and 2025. There were ~32 results (not including China & Russia companies) however several of these companies are in the process of being acquired (including IMGN, ESMT, OLK) so the ones left that met my criteria were:

ACMR

AMPS

ATAT

BE

BROS

CYBR

DLO

DUOL

DV

FLYW

FOUR

FROG

FRPT

GLBE

GSHD

HIMS

INSP

MARA

MNDY

NOVA

ONON

OWL

RELY

SHLS

SPT

SWAV

SYM

TOST

VTEX

Out of all the names on this list the company I was the least familiar with was VTEX so that’s why I decided to do this deep dive… to figure out if this was a company I should be paying attention to and how much potential upside the stock might have over the next few years.

Introduction

I do not currently have a position in VTEX and I never have.

As I mentioned above, VTEX is not a company that I was familiar with until recently and I’m glad I did this deep dive because I learned alot about the company. There’s alot to like about VTEX but of course there’s plenty of risks and red flags which is typically true for any small cap company ($1.2 billion market cap).

Even though VTEX is technically based in the UK, they do most of their business outside of the UK with a heavy concentration in LATAM and for the record if you want LATAM exposure I’d recommend MELI and NU (I own both) but they’re much larger companies so keep that in mind.

I’m always on the lookout for undiscovered and undervalued small/mid caps because I want to find them before the big funds do because that’s how we can make huge returns like I did with CELH, TMDX, ASPN, and many others over the past few years.

VTEX is like a really small Shopify (SHOP) although this is not a true apples-to-apples comparison. Perhaps, VTEX is a blend between SHOP and BigCommerce (BIGC) but most people aren’t familiar with BIGC so that’s why I’m going to use SHOP as an example for this next part.

SHOP is now a $100 billion company but they actually came public in 2015 at a $1.2 billion market cap [click here].

Let’s be clear, I’m certainly not saying that VTEX is the next SHOP but simply reminding everyone that VTEX should not be ignored just because it’s on the smaller side, sometimes that’s where the best opportunities can be found.

I’m a big SHOP fan, I’ve been a customer multiple times and they have an amazing product offering. I’ve also been a shareholder several times over the past few years but let’s be honest, the stock is not cheap. SHOP currently trades at 72x NTM EV/EBITDA which is very expensive for a company that is only expected to grow revenues next year by 19.2% however the company is finally doing a good job of expanding margins so analysts are expecting 74% EBITDA growth in 2024 so you can sort of justify that current EV/EBITDA multiple on SHOP however analysts are only expecting 13% annual EBITDA growth from 2024 through 2027 so that EBITDA multiple could get compressed quite drastically towards the end of next year.

In terms of VTEX, the stock currently trades at 40x NTM EV/EBITDA with 22.2% revenue growth expected for next year along with 316% EBITDA growth because analysts are expecting EBITDA margins to expand from 3% in 2023 to 13% in 2024 which creates quite the setup for growth across all financial metrics. Keep in mind that only a few analysts cover VTEX whereas 40+ analysts cover SHOP, but with that said, the analysts that do cover VTEX are looking for 47% annual EBITDA growth from 2024 through 2027 (compared to 13% for SHOP) which means that the current EBITDA multiple for VTEX is more likely to hold up and not go through some serious compression over the next few years but that’s only if VTEX can hit the current consensus estimates. Analysts think VTEX can expand margins from 3% in 2023 to 24% in 2027 which might be possible because they currently have 68% gross margins (going to 75% in 2027) vs SHOP which has currently has 50% gross margins (going to 52% in 2027).

If we look at current year (2023) through 2027 for both VTEX and SHOP….

VTEX trading at 40x NTM EBITDA with 90% EBITDA growth through 2027

SHOP trading at 72x NTM EBITDA with 26% EBITDA growth through 2027

Once again, I’m not saying that VTEX is a better company (because that would be crazy) but it’s very possible VTEX outperforms SHOP over the next 3-5 years because they might end up with better growth rates, more margin expansion, and higher EPS growth which matters even more since VTEX is trading at a 50% discount (in terms of EBITDA multiple).

I’ll cover both of these more in part 2 but here are the current estimates for VTEX and my investment model using those estimates (although I was more conservative with net income margins)…

I also like that VTEX is still founder led and together they own almost ~30% of the company which means they definitely have a vested interest in the long-term success of VTEX and doing what is best for shareholders.

The success of VTEX is quite simple… they need to continue adding more enterprise customers, they need to increase GMV (currently at $4 billion), they need to continue growing revenues by 20-25% per year, they need to increase net income margins by 3-5% per year… if they do all of these things for the next ~4 years then the stock could triple during that time frame — btw, 215% return over the next ~4 years would be a 33% CAGR.

I wish SHOP was cheaper because I love the long-term upside of the ecommerce industry but it’s just too hard for me to pay 72x NTM EBITDA for SHOP whereas VTEX looks more compelling at current prices/multiples not to mention if 2024 is a big year for small/mid caps then VTEX could be primed and ready to go.

Just keep in mind that companies like VTEX are littered with risks such as smaller/weaker balance sheets (although VTEX does have 16% of their market cap in cash), operational challenges outside of the US in less stable geopolitical climates and of course the risks of dealing with larger competitors however not only does VTEX have strong fundamentals (35% YoY GMV growth and 31% YoY revenue growth in Q3) but they could always be an acquisition target. Personally I think 2024 has the potential to be a record year for M&A deals across the globe and I would not be shocked if a company like VTEX got scooped up by SHOP or maybe GLBE wants to move beyond cross-border logistics or DLO wants to move beyond payments. Of course private equity could always be a buyer, just like they bought ROVR (+30% buyout premium) which was one of my deep dives from November.

I’m far from an expert on VTEX, I still have alot to learn but I’m definitely intrigued by the company, the industry, their business model, their expansion strategy, the founder-led team with big equity stakes and of course the compelling valuation and multiples — however since I’m a big fundamentals and valuation investor, I’ll need to keep a close eye on growth and margins because that’s what will lead to stock price appreciation which is all I really care about. SHOP might be a bigger, better company but VTEX might be the better stock and that’s what I need to figure out.

It’s possible I end up starting a small position in VTEX soon (~1.5% position) but I’d probably use a stop loss in case we finally get that market pullback in early 2024. The spots that look the most interesting to me (to start a position) would be a close above the VWAP from recent high, or wait for breakout through 7.15, or wait for pullback to the 50d ema/sma in the 6.40 range (no guarantee that pullback happens).

If you’re interested in VTEX then I’d recommend reading some of the customer case studies because they’re all very different and help demonstrate that VTEX is more than just a basic ecommerce platform for brands to launch new products…. https://vtex.com/us-en/customer-stories/

Company Background

VTEX was founded in Brazil back in 2000 by two engineers, Geraldo Thomaz and Mariano Gomide. Both founders are still with the company, acting as co-CEOs, with Thomaz leading the Research & Development teams and Gomide in charge of VTEX's Sales and Marketing teams, overseeing the UK and Asia markets. The duo remains the largest individual shareholders, holding 11% (worth ~$140 million) and 17% (worth ~$216 million), respectively.

Fresh from the university, Thomaz and Gomide embarked on the opportunity to develop software for the textile industry. The name VTEX actually means Vitrine Têxtil. The initial idea was to create an ecommerce solution to enable a digital transformation for the textile industry.

After almost five years of building, iterating, and launching product trials and pilots, the founders decided to move away from the textile industry and pivot to something less niche. They had a much bigger ambition: to enable a digital transformation for brands and retailers, regardless of the niche, without the need for significant investments and have flexibility and customization for their enterprise complexities.

But for the next few years, VTEX was building online stores (from existing solutions) for different small brands and retailers in Brazil. The big breakthrough for Thomaz and Gomide came in 2007 when they won an opportunity to build an ecommerce platform for Walmart, the world’s largest retailer, which was expanding to Brazil at that time. Walmart chose VTEX for one primary reason: speed to market, which only a small company like VTEX could offer. The ecommerce platform for Walmart was eventually built by VTEX within eight months.

The solution for Walmart laid the foundation for VTEX's own platform. In 2010, the company launched its SaaS Commerce Platform, focusing on blue-chip enterprises (big brands and retailers) that want to go direct-to-consumer and explore new digital sales channels.

What differentiated VTEX from any other platform on the market was its approach to building technology that not only enables commerce but also solves the problem of increasing assortment and delivering faster to consumers. This approach helped to win many new customers in Brazil, and by 2012, VTEX had become the absolute leader in the Brazilian market, a market that is not only the largest in Latin America but also faces enormous complexities, from laws and regulations to infrastructure and logistics. The VTEX team was able to figure out the ways to overcome countless challenges its customers faced domestically. It remains the company's competitive advantage up to now.

After conquering Brazil, it was time to expand to other countries in the region, and in the next two years, VTEX entered Argentina, Chile, Peru, Colombia, and Mexico. By 2019, VTEX had become the leading ecommerce platform in almost all countries in LatAm and built a reputation as a go-to platform for any global enterprise that wants to scale its operations into this region.

And VTEX has become more than just an online store solution for its customers. Today’s consumers expect fast delivery and being able to find everything they need in one place. They want to have a smooth experience across digital and physical channels. This created a high bar for brands and retailers since brick-and-mortar and online were traditionally separated. VTEX is helping to bridge this gap and become the backbone for connected commerce.

Having established itself as the market leader in the LatAm region and despite a huge untapped potential there on its own, it was clear that the next big chapter for the company is international expansion, specifically to the US and Europe. The company acquired its first clients from these regions just before the pandemic hit. The expansion plans have stalled a bit, but the pandemic has accelerated digital transformation all around the globe by several years, pushing VTEX's IPO forward.

The company had a highly successful IPO, pricing its shares at $19, above the expected price range of between $15 and $17. The stock surged 32% in its debut, closing at $22.18 per share, giving the e-commerce software platform a valuation of $4.7 billion. The company raised approximately $361 million in the public offering.

However, since the IPO, the stock has been down more than 70% (at some point, it was close to 90%). There are several reasons for that, starting from the high valuation at which VTEX went public and ending with the company being still unprofitable after 21 years since inception, though coming so close to profitability in 2020 (just short of $900k from breakeven).

The company continues its journey to profitability and cash generation, and in Q3 2023, it achieved its breakeven target from a non-GAAP operating income and free cash flow basis, one quarter before management's expectation. Analysts covering the company estimate it will turn profitable in 2024 with an expected revenue CAGR above 25%, margins in the high teens until 2025, and >30% FCF expansion.

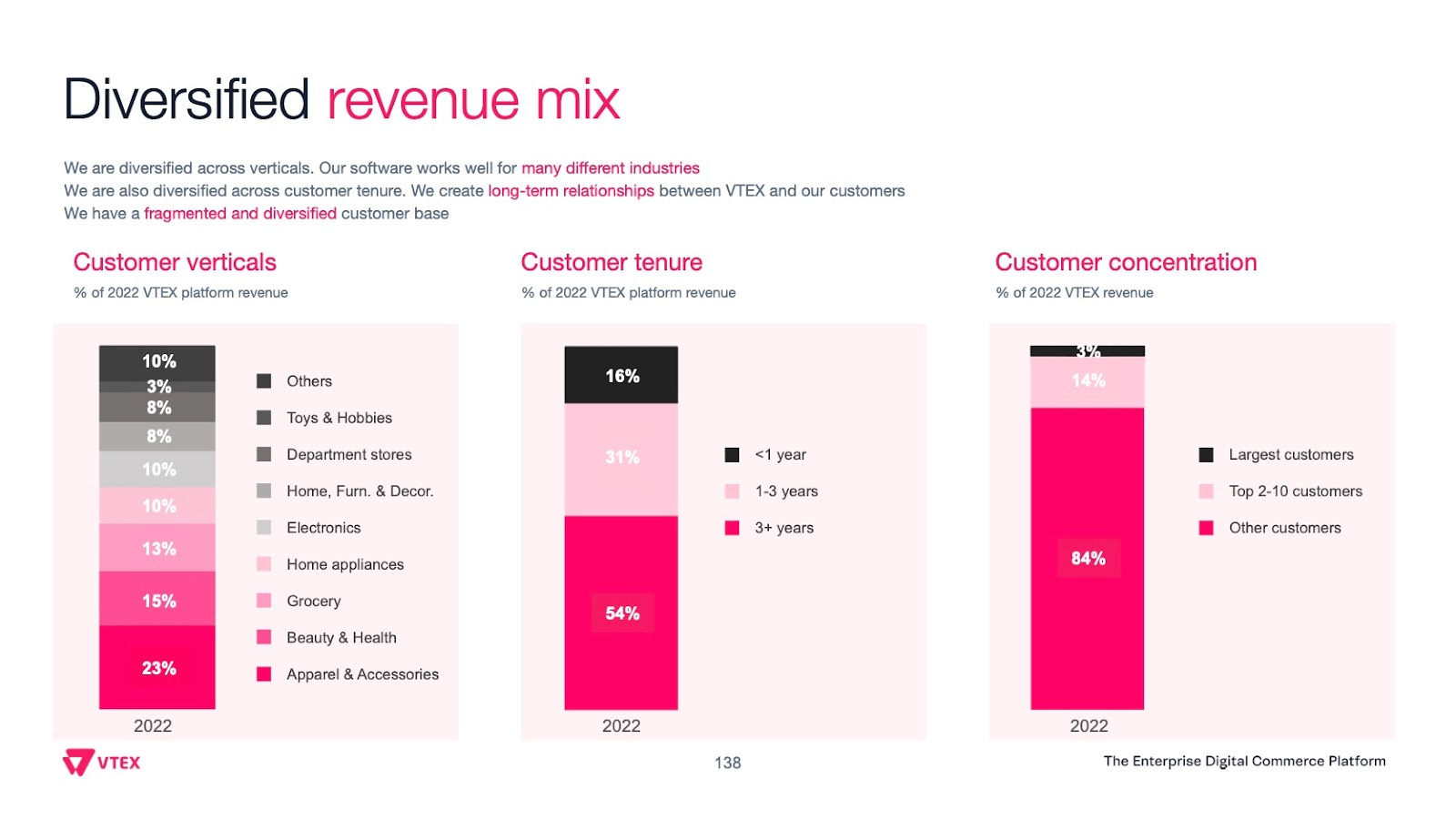

VTEX's focus on enterprises, which account for over 85% of its revenue, while subscription revenues account for ~94% of total revenues. Here are some of the customers that VTEX has added since going public: Asics, Beauty Counter, Hearst, Mazda, Pandora, Under Armor, Walmart, Xiaomi, and Yamaha.

One particular case, the Casino Group (Casino Guichard-Perrachon), a French mass-market retail group with more than 11,500 stores across France and Latin America, stands out. It is the best testimonial for VTEX's capability-rich technology when a European company moves to a non-European solution at this large scale.

Another strong testimonial for VTEX is how existing customers are expanding to new countries over time, and the best example of such a customer is Motorola. Motorola began working with VTEX in 2017 in Brazil and Mexico. In six years, Motorola expanded its online store into 19 countries (including Europe, Canada, and the US) while significantly growing GMV (gross merchandise value).

And VTEX is just scratching the surface with its current GMV, providing continuous revenue growth for the company. It can grow GMV by adding new logos and expanding with existing customers (2,400+ customers in 38 countries). As of Q3 2023, over 3,400 unique stores generated GMV for VTEX. More to come in the coming years.

Opportunity

VTEX operates as a provider of a technology platform in the e-commerce industry. Its platform natively combines commerce, order management, and marketplace functionality, allowing enterprises to sell a wide assortment of products across various channels, including direct-to-consumer, marketplace, ship-from-store, endless aisle, drop-ship, conversational commerce, and live shopping.

VTEX has witnessed substantial evolution and growth in recent years, driven by several key trends, including the rising adoption of digital commerce solutions (as part of digital transformation), the demand for integrated and comprehensive digital platforms, and the proliferation of online retail and marketplace models.

Additionally, the shift towards omnichannel retail, the need for advanced inventory and order management in e-commerce, the increasing relevance of personalized customer experiences, and the integration of AI and data analytics for enhanced decision-making have further propelled VTEX's growth.

The following trends underscore the constantly evolving landscape of e-commerce and the growing importance of sophisticated, scalable platforms like VTEX, designed to help enterprises navigate the complexities of e-commerce and take advantage of new opportunities as they arise.

The growth of international commerce in LatAm

LatAm's e-commerce has grown enormously in recent years, driven by increased internet penetration, growing smartphone usage, and a young, digitally-savvy population with a rising middle class. With this extensive growth, the LatAm market has become increasingly attractive to international brands and retailers wanting to establish regional operations to capture this massive new target audience.

A significant number of international brands have entered the market in the past five to ten years. However, this is just a tiny number of potential new entrants, and more companies, from large enterprises to much smaller retailers, are expected to start their operations in the region in the near future.

Furthermore, many of those brands that already operate do this in one or two concrete markets, predominantly in Brazil and Mexico, providing a tremendous opportunity for further expansion to other countries in the region.

There will be an influx of new companies and those that are already present in some markets in the coming years but want to expand, and the majority of those companies will need a solution that will know how to overcome all the complexities (like integrating with local logistics providers, payment gateways, and other essential services) of operating across the entire LatAm while being flexible, easy to implement, and rich in features.

Shift to omnichannel

The growth of omnichannel retailing has been at the forefront for some years. This is a shift towards a seamless integration of both online and offline channels, driven by increased expectations of modern consumers to have a seamless shopping experience, whether online, in a physical store, or using a mobile app.

A typical customer experience today may look like the following: first, research a product online, then try it in-store, and finally, make a purchase via a mobile app.

These expectations have driven retailers to adopt omnichannel strategies, which require synchronization of inventory, pricing, and customer data across various channels. Yet, not all current solutions retailers use have been designed to support omnichannel strategies, providing an inconsistent and ununified customer experience.

Today, seamless integration is critical: online stores must be synched with physical retail operations, mobile apps, social media platforms, and marketplaces. Omnichannel retailing also demands advanced inventory management tools, helping retailers keep track of inventory levels across all channels.

Furthermore, the modern full-stack commerce platform must offer robust data analytics capabilities, enabling retailers to collect and analyze data from various channels, leading to a more personalized shopping experience and making better business decisions.

And finally, such a platform must be scalable and work globally, allowing retailers to quickly adapt their omnichannel strategies in every market of operation. This scalability is crucial when retailers are deciding which vendor to choose.

So, adopting omnichannel strategies is not an option anymore; it is mandatory for any modern retailer to stay competitive. This will only increase the demand for platforms that can support such integration, and not many can provide the level of integration that VTEX offers.

Total Addressable Market

So, VTEX is the gateway to the fastest-growing ecommerce market in the world. Indeed, between 2019 and 2022, LatAm has seen the highest CAGR (37%) among all other regions, yet it still represents a small fraction of the total retail sales in Latin America: the ecommerce market in LatAm was estimated to be around $168 billion in 2022, representing only about 12% of all retail sales.

So, VTEX, with its expected GMV of around $15 billion in 2023, is addressing a massive market with tremendous room for further penetration as more sales shift online. Insider Intelligence estimates the Latin American ecommerce market will grow to $257 billion by 2026.

With expanding globally, VTEX significantly increases its total addressable opportunity. According to Insider Intelligence, global GMV was estimated to be approximately $5.7 trillion in 2022 and is expected to grow to around $8.1 trillion by 2026. As VTEX continues its global expansion, the company will be able to capture more of this GMV over time, and the growth in GMV is literally unlimited.

VTEX's total addressable market will increase significantly going forward as more consumers continue to shift online and retailers adapt to evolving consumer preferences, including omnichannel.

Growth Drivers

VTEX has seen solid growth in the past two years, growing its revenue at around 26% CAGR. Analysts estimate the revenue growth to continue at the same rate in 2023 and remain such throughout 2025 at a minimum.

At the same time, the company is expected to turn adjusted EBITDA positive in 2023 and significantly accelerate its growth going forward.

The growth is foreseen to come from different avenues, more specifically from new customer additions, GMV growth with existing customers, geographic expansion, upselling and cross-selling through innovation and platform expansion, and finally through ecosystem development.

In no particular order, the primary growth drivers are the following.

Growth within existing customers

The company reports the number of customers and online stores they operate only at the end of the financial year. As of FY 2022, over 3,400 online stores of 2,400+ customers run on the VTEX platform, about 55% of which were from Brazil, 35% from the rest of LatAm, and 10% from the rest of the world. The latter number has increased 2x in the past three years.

Not only is the number of customers increasing, but the GMV of these customers is also growing, resulting in increasing revenue for VTEX. Average revenue by customer for the top 100 customers grew at 27% CAGR from 2017 to 2022 and 24% CAGR for the top 25 customers. During the same period, the number of customers with revenue over $250,000 per year grew from just 18 in 2017 to 94 in 2022.

Furthermore, the top 100 customers keep opening new stores both in the same countries and expanding into new countries. In 2017, there were 2.2 stores on average per customer. In 2022, this number was already 5.9 stores per customer.

But GMV growth is not the only growth driver within existing customers. VTEX charges a fixed subscription fee in addition to a transaction-based fee (based on GMV), and this fixed subscription fee is higher for those customers who generate higher GMV and depends on the number of products that customers adopt. So, the company can grow its revenue by building more products (portfolio expansion) and continuously enhancing its platform.

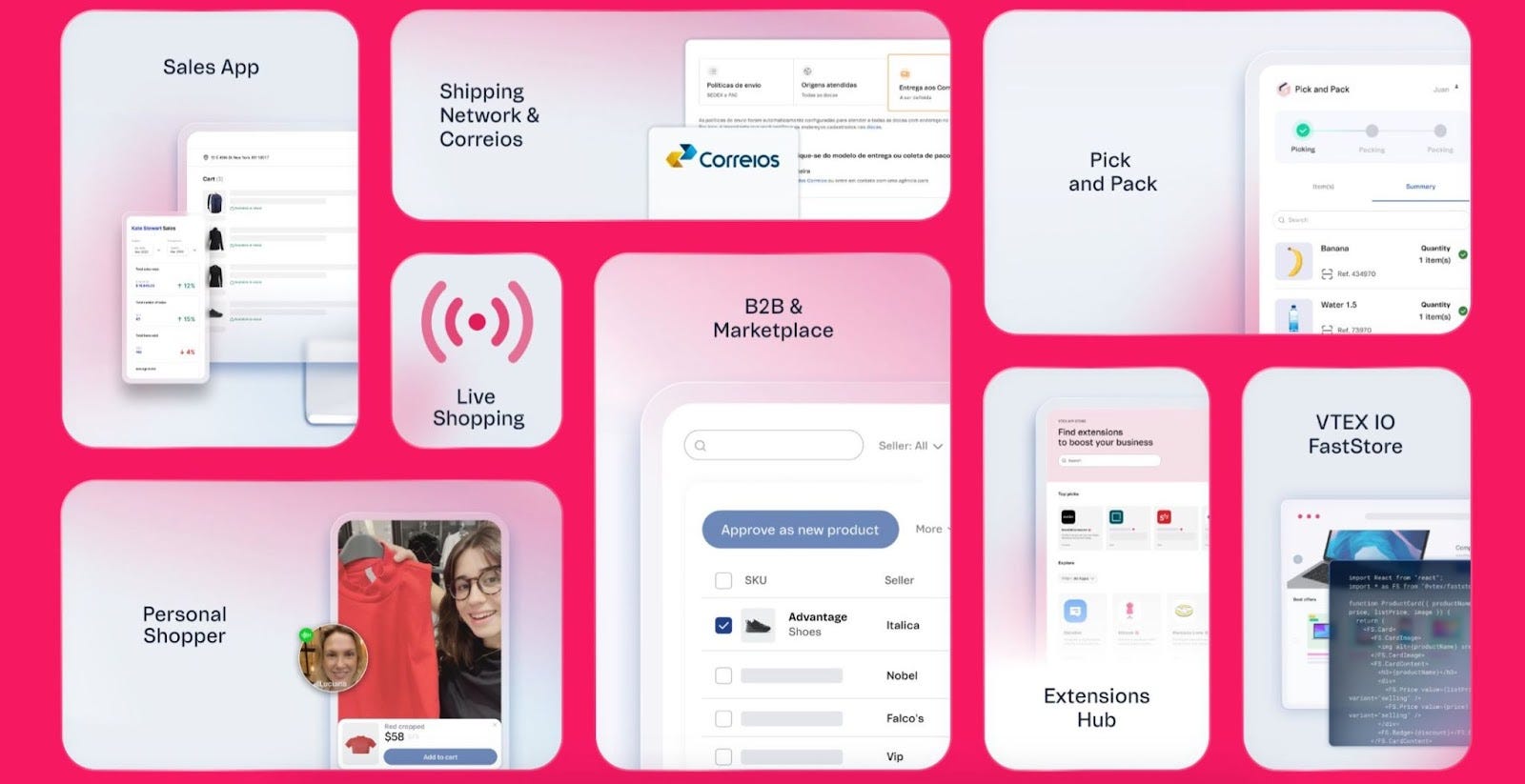

VTEX continuously introduces new products that have both strategic rationale and financial impact. For example, the VTEX Sales App allows for better digitization of physical stores while potentially increasing volume. Or VTEX Shipping Network enables asset-light fulfillment optimization that could potentially lead to a slight take-rate increase.

So, portfolio expansion helps to upsell and cross-sell existing customers to grow GMV. And management has identified three major opportunities to expand its portfolio: first – enable fulfillment efficiencies for customers. A large number of VTEX customers are retailers with extensive networks of physical stores. For example, Track&Field, the largest sports brand in Brazil with 331 stores in 145 cities, had 81% of orders in 2022 delivered from brick-and-mortar stores. VTEX helps such customers transform their physical stores into distribution centers through the Pick and Pack product, an asset-light fulfillment for physical stores.

Next is enabling new sales channels. VTEX wants to become an e-commerce engine for any front-end, whether it is online, mobile apps, messaging apps, or live streams. In Q3 2023, the company achieved significant success with its VTEX Live Shopping product, introduced earlier this year. One of its customers, PatBo, hosted a Live Shopping event during New York Fashion Week, becoming the first and only Brazilian brand to do so. PatBo saw a remarkable 300% sales increase, a 125% boost in orders, and a 79% rise in average order value.

Finally, VTEX allows customers to expand their business model, offering DTC, B2B, and B2E. One of its flagship customers, Electrolux, a Swedish multinational home appliance manufacturer, has 18 storefronts and 34 third-party marketplaces supporting all of these business models.

Growth with existing customers could also come from expanding to other markets, like in Motorola's example, which started using VTEX in 2017 to expand to LatAm. Just two years later, Motorola switched to VTEX in all major markets, including the US and the United Kingdom, before fully migrating to VTEX in 19 countries of its current operations.

Another example of growth within existing customers could come from the expansion of several brands within one group. The largest retail group in LatAm, Cencosud, began using VTEX in 2015 in Peru and Colombia with just one of its many brands. Today, VTEX is used by 11 brands operating in five countries.

These kinds of expansions are happening on a constant basis. Just a few of such in the recent quarter: Calvin Klein added a new store in Ecuador and is now operating in nine countries in Latin America, or Whirlpool who added its Kitchenaid brand in Austria, Denmark, Finland, France, the UK, and Italy, and is now operating in Latin America, EMEA, and APAC.

Growth within existing customers in all of its forms will remain the primary growth driver for VTEX in the foreseeable future.

Adding new customers

The second biggest opportunity for VTEX lies in growing its customer base. Although the global macroeconomic environment continues to impose challenges on retailers and ecommerce players, VTEX has not seen any significant deterioration in the growth of new customers.

The company is starting to see a stabilization in the ramp-up periods and implementation times, leading to more new logos coming online.

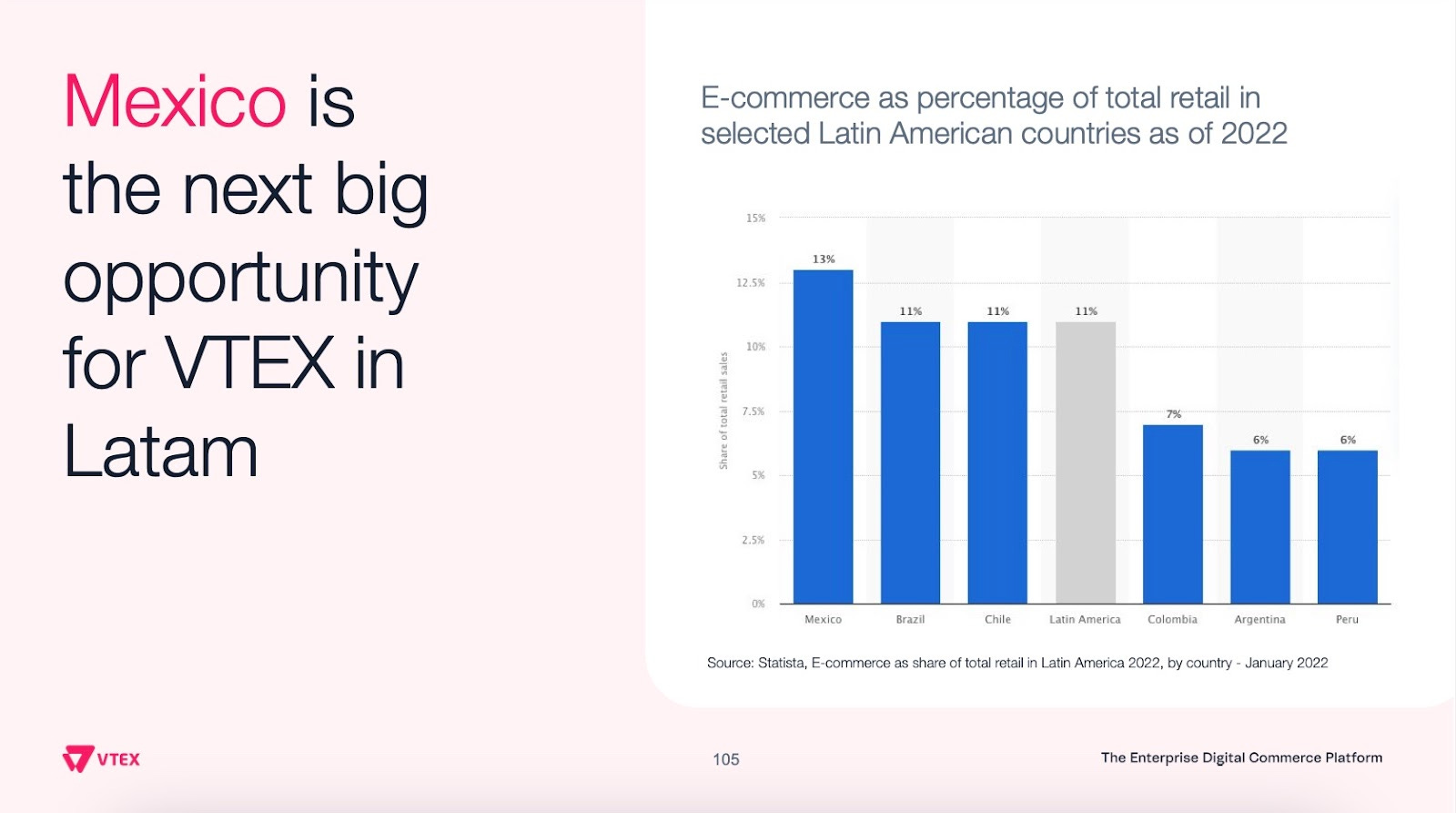

The next big opportunity for VTEX to grow new customers is within LatAm, specifically in Mexico. According to Statista, Mexico has the largest e-commerce as % of total retail in LatAm.

In the third quarter, VTEX saw some significant additions from this region. HEB, a supermarket chain with over 380 stores across the US State of Texas and Mexico, completed its migration to VTEX. In just one quarter, HEB has seen incredible ecommerce results never seen before.

VTEX's LatAm expertise and ecosystem make it the best-positioned platform to conquer Mexico.

In the third quarter, VTEX also added several new international customers that migrated from other platforms, including Beautycounter and Pierce Manufacturing B2B in the US.

International B2B commerce is actually the primary growth driver in new customer growth.

International Expansion

In the US alone, B2B ecommerce (wholesale, manufacturers, distributors) is expected to reach $2.47 trillion in 2023. There is a growing number of B2B organizations that are looking to implement/migrate B2B digital commerce solutions with a new modern front-end compared to their legacy solutions.

Management has identified three key drivers of B2B adoption in North America and EMEA. The first driver is the modernization of processes and systems. According to Forrester, 35% of decision-makers in B2B firms said that they had increased their investments in B2B ecommerce technology.

One of the biggest areas, which is the second driver for B2B adoption and in which a significant amount of capital is invested, is the B2B marketplace. Amazon, with its Amazon Business, showed how successful this model could be, and now many other retailers are following it.

For example, the Foschini Group, a leading South African retailer with a diverse portfolio of 26 brands, successfully transformed its diverse ecommerce ecosystem into one innovative marketplace (powered by VTEX). They successfully consolidated 18 of its brands into one while retaining the flexibility for each brand that allows for full customization. Since its marketplace launch, the Foschini Group has seen a remarkable 73% increase in multi-brand orders.

Finally, B2B ecommerce is still heavily conducted between people. Even the most tech-savvy B2B buyers seek human interaction, so there is a need for a hybrid to connect sales reps with B2B buyers. According to Forrester, 33% of all B2B transactions globally were a hybrid of digital and human-assisted. This creates a growing need for hybrid digital-plus-human-assisted solutions.

VTEX has already seen a significant increase in B2B customers in the US and Europe, which will only increase in the coming years. B2B will remain the primary focus for VTEX, but not the only one. The other one is the migration from legacy providers.

According to management, about 20% of US ecommerce GMV is still based on legacy platforms, and a similar percentage is in Europe. This is about a $300 billion market opportunity. VTEX is not the only vendor that goes after this opportunity, with companies like Shopify trying to take the majority of it, but VTEX is getting closer and closer to larger incumbents and, in several years, will be able to compete with them head-to-head.

Some recent wins show this in motion: Beautycounter, a Carlyle portfolio company that sells skincare and cosmetic products, has successfully migrated from its legacy platform to VTEX. This migration enabled the consolidation of all of Beautycounter's channels into a unified commerce experience provided by VTEX. We should expect more of such migrations in the following years.

And there are several reasons why VTEX will win many new customers migrating from legacy solutions. First and foremost, VTEX offers a comprehensive data privacy and compliance solution. It is such a critical issue, as illustrated by the Gartner survey: for 84% of software buyers, data privacy is one of the key concerns when they are choosing which software to use.

Furthermore, legacy solutions have been historically far behind in shipments and fulfillment. Forrester estimates that 25% of businesses with a digital presence will double down on solutions that will provide operational efficiency in these areas.

To conclude, international expansion is still in its initial stages. Only 10% of its total revenue today comes outside of LatAm. VTEX is only starting to grow GMV in these markets, which should only accelerate going forward.

Business Model

VTEX operates a subscription revenue model that includes both fixed and GMV-based fees. This revenue model strategically aligns with customers: VTEX grows when customers grow.

Approximately 2/3 of total revenue comes from a variable monthly take rate, while the rest comes from fixed fees for subscription plans. The transaction-based fee accounts for most of VTEX's subscription revenue and is primarily structured as a take rate or percentage of the total value of the orders (GMV) processed through its platform, including value-added taxes and shipping.

VTEX works with each customer individually, having multiple tiers of subscription plans and transaction-based fees based on the size of the customer and its expected GMV. Those customers who generate higher GMV can pay less in transaction-based fees but substantially higher fixed fees.

Subscription fees are also growing regardless of the GMV as the company introduces more products that it upsells or cross-sells to existing customers.

Approximately 85% of annual recurring revenue (ARR) comes from enterprise customers. In addition, VTEX also serves small-to-medium sized businesses (SMBs) and a smaller segment of business-to-business enterprises (B2B) on a separate on-demand platform that represents approximately 6.4% of total revenue. The remaining represent service revenue and other revenues, comprising VTEX platform adjacencies, including payment, logistics, and tracking solutions.

VTEX's revenues are pretty diversified across verticals and customer tenure, with insignificant customer concentration: the largest customer represents less than 3% of total revenue, and the 10 largest customers represent less than 15%.

VTEX's business model is also driven by strong land-and-expand motion. Earlier cohorts keep growing, while new cohorts grow much faster than older ones.

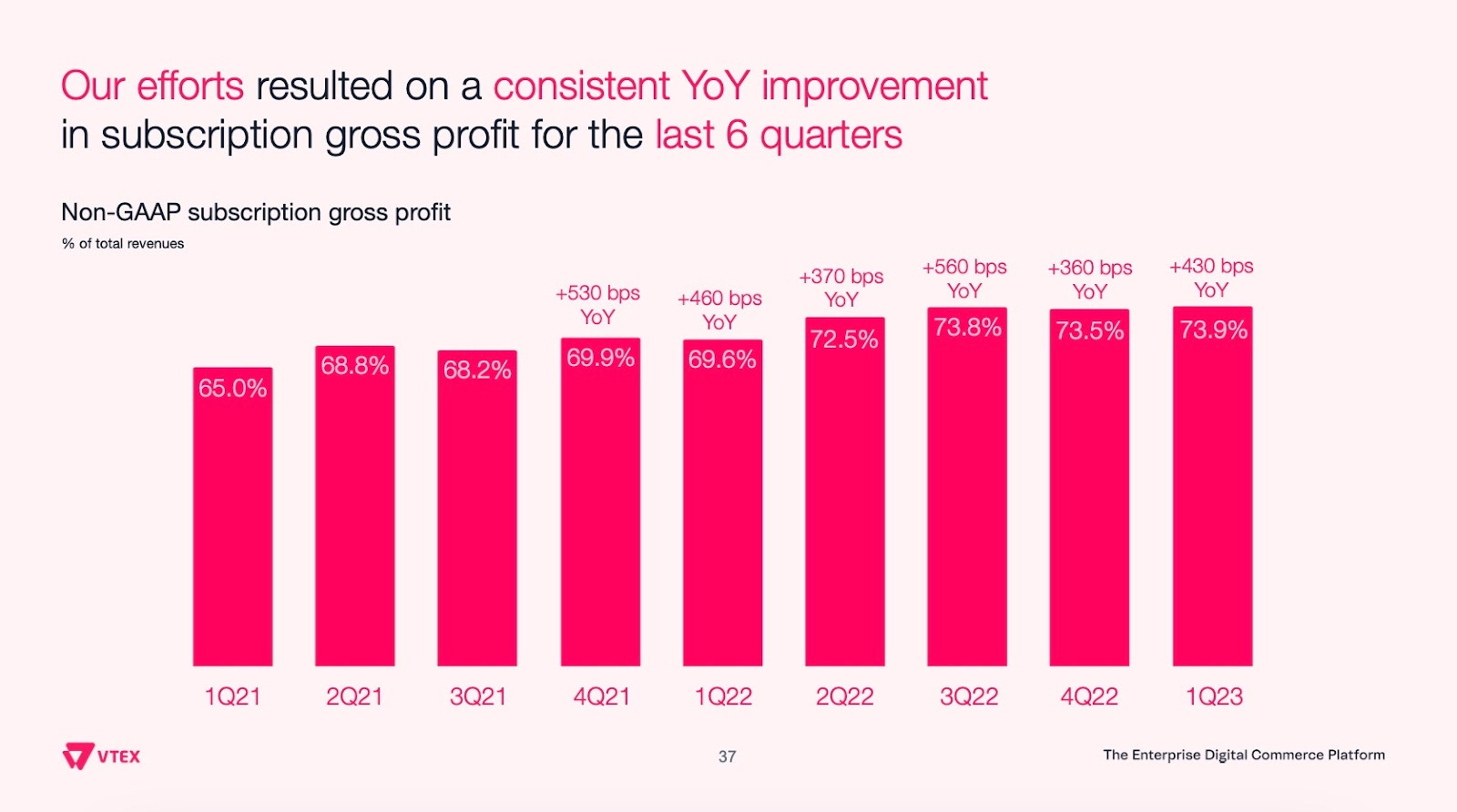

Gross margin

As a SaaS business, VTEX enjoys pretty high gross margins. The company keeps expanding its subscription gross margin and has seen growth in the past six quarters. This expansion was due to driving business efficiency, including migration to Linux, CPU diversification, and elimination of a legacy vendor that has improved observability.

In Q3 2023, the company reported a non-GAAP gross margin of 76.2%, up from 75.2% in Q2 2023 and 73.8% in Q3 2022. On a GAAP basis, the gross margin in the latest quarter was 70.33%, the highest since the company became public.

Analysts are in good agreement that VTEX will continue to expand its gross margin in the coming years.

Financial Snapshot

Based on Q3 2023, reported on November 7, 2023

Revenue

Actual:

2022 – $157.6 million (+25.32% YoY)

Q3 2023 – $50.6 million (+30.64% YoY)

Nine months of 2023 – $140.79 million (+25.56% YoY)

Guidance:

The company expects FX-neutral YoY revenue growth of 22% to 23%, implying a range of $196 million to $198 million based on the October average FX rate and assuming a devaluation of Argentina’s currency aligned with market futures rates.

Estimates:

2023 – $197.8 million (+25.5% YoY)

2024 – $241.7 (+22.2% YoY)

Operating Expenses

2022 – 98.15% of total revenue

Q3 2023 – 77.19% of total revenue

Operating expenses as a percentage of total revenue have been on a constant decline in recent years. The company is very close to generating GAAP operating income and has already turned positive on a non-GAAP basis in Q3 2023. Management expects considerable YoY improvements in the Non-GAAP operating income in the fourth quarter of 2023.

Stock-based compensation (SBC)

2022 – 7.74% of total revenue and 0.98% of the market cap

Nine months of 2023 – 10.23% of total revenue and 1.15% of the market cap

The company has already exceeded SBC in 2023 compared to 2022. However, the company is actively repurchasing its shares to offset the dilution caused by issuing extensive stock-based compensation.

As of Q3 2023, the remaining balance under the current share repurchase authorization was nearly $10.1 million. Under the previous plan, which concluded in August 2023, the company repurchased 9 million shares for a total cost of $37.9 million.

Since going public, VTEX decreased its shares outstanding by almost 1%. During the same period, the stock price plummeted by nearly 80%.

Profitability

VTEX has just turned adjusted EBITDA positive in Q3 2023, and FY 2023 is expected to be the first profitable year on a non-GAAP basis.

On a GAAP basis, the company is still unprofitable, but analysts expect it to break even in 2024 and finish the year generating a positive net income. Positive earnings should accelerate in the coming years with growing margins.

Balance Sheet

The company still has a pretty strong balance, with $21.3 million in cash and cash equivalents (down from $24.3 million at the end of 2022) and $192.4 million in short-term investments (down from $214.1 million at the end of 2022). There is no debt on the balance sheet.

Cash Flow

VTEX is still burning cash. However, it is estimated that the company will reach positive free cash flow (FCF) in 2024, slowly growing from there.

Competitive Advantages

VTEX operates in a highly competitive market of various ecommerce solutions for enterprises. Among its competitors are dozens of giants like SAP (SAP Hybris), Oracle (Oracle Commerce), Magento (an Adobe company), and Salesforce (Salesforce Commerce Cloud), as well as almost 100 mid-size platforms and popular small-size platforms like Shopify (Shopify Plus).

When it comes to choosing the vendor for commerce, enterprises have two options: either go for easy-to-use yet rigid software (software that is designed for smaller and medium businesses and is typically restricted to limited use cases) or choose on-premise or open-source platforms that can provide the needed level of customization but requires a higher initial investment and time-consuming customization and integration periods, which leads to higher developer dependency and increasing total cost of ownership.

While existing vendors may have substantially broader product lines, greater name recognition, larger sales and marketing budgets and resources, greater customer support resources, and so on – VTEX has two distinct advantages. First, the company is the king domestically. So, VTEX has a serious competitive advantage in the LatAm market over any other solution and will outdo everyone else there.

Second, and perhaps most vital, is that VTEX supports all business models: B2C, DTC, B2B, and Marketplace. VTEX does it globally and through the most comprehensive list of channels. This is something no other competitors, including the industry giants, currently offer. Furthermore, VTEX's omnichannel capabilities are on the next level, creating some solutions that no one else has.

This all is supported by a powerful ecosystem with significant network effects. This ecosystem includes over 3,000 integrated solutions, 1,000 systems integrators, 300 marketplaces, 150 payment solutions, and 90 logistics companies. With a growing number of partners (that now go beyond just LatAm), VTEX customers can seamlessly execute their commerce vision and strategy.

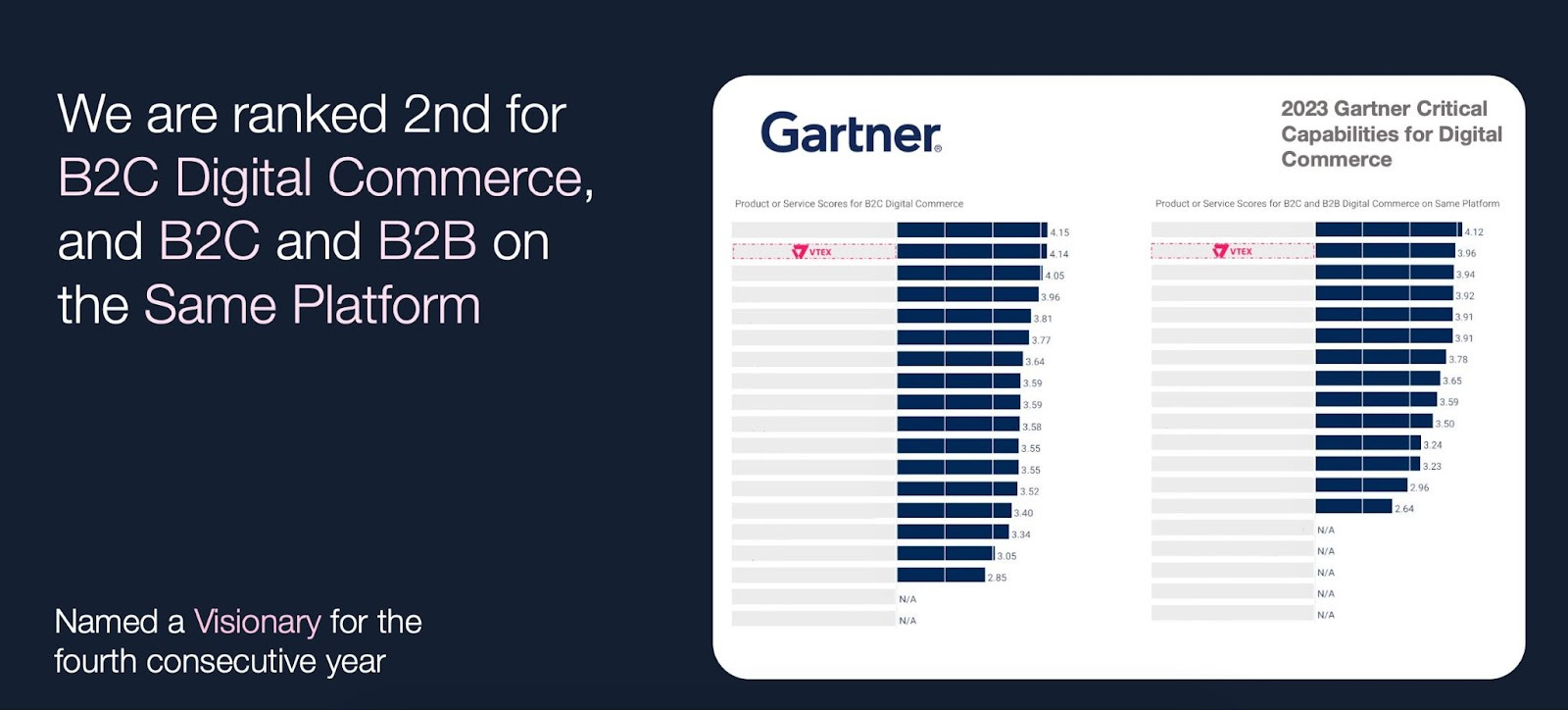

And VTEX is getting more and more recognized by the industry experts. The company was named a Visionary in the 2023 Gartner Magic Quadrant for Digital Commerce for its ability to execute and completeness of vision.

VTEX has also ranked second for the following use cases: B2C Digital Commerce, B2C and B2B Digital Commerce on the Same Platform and Complex Business Models. Additionally, VTEX was one of the top-rated digital commerce platforms by Gartner Peer Insights over the last twelve months.

This really helps drive new customers. For example, the Casino Group mentioned earlier chose to migrate to VTEX because of these recognitions. And none of these recognitions would happen without a really advanced platform that VTEX has built. The company outspent every one of its competitors in R&D in the past several years, and it is exactly when VTEX made a significant step further. These investments will now start to pay off.

Risks

Currently, 90% of total revenue comes from the LatAm market, which possesses a wide range of risks, from currency exchange risks to political and regulation risks.

The company is facing severe competition, especially in international markets.

The success of the company's expansion into the US and Europe is the single most crucial component for the investment thesis.

VTEX is based in London, United Kingdom, and reports as an international company, which allows it to disclose information differently than US-based companies. The company reported a material weakness in its internal controls over financial reporting as of December 31, 2022.

The company does not provide updated information in its quarterly presentations. In Q3 2023, the company refers to data from 2022.

The company's sales cycles are long and expensive due to the nature of its target customers (enterprises).

The company's revenues primarily depend on GMV growth, which could significantly slow down in times of economic downturns and crises.

Voting control is in the hands of several shareholders.

Additional Sources

Management – https://www.investors.vtex.com/governance/executive-management/default.aspx

Board of Directors – https://www.investors.vtex.com/governance/board-of-directors/default.aspx

Ownership: individual investors (~31%), VC/PE (~29%), General Public (~25%), Institutions (~15%)

Have a great week!!!

~Jonah

You can follow me on Twitter [click here]

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.