Part 1: Deep dive on Unity Software ($U)

Part 1: Deep dive on Unity Software ($U)

In order to read this deep dive writeup on Unity (U) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber, I appreciate your support.

Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +69% YTD), my daily activity (buys, sells, trims, adds plus hedges), my investment models and my daily webcasts.

Here are some of my other newsletters…

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus you get my daily commentary and morning newsletter.

Company: Unity Software

Ticker: (U)

Website: Unity.com

IPO date: September 18, 2020 (traditional IPO)

IPO price: $52

Current stock price: $36.32

Outstanding shares: 378.6 million

52 week high: $58.62 on August 12, 2022

52 week low: $21.22 on November 09, 2022

ATH: $210.00 on November 18, 2021

Market cap: $13.750 billion

Net cash/debt: -$1.500 billion

Enterprise value: $15.250 billion

Headquarters: San Francisco, California, United States

Number of employees: 7,700+

Average price target from analysts: $39.29 based on 14 analysts

Next earnings call (Q2 2023): N/A

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1 & 2]

Below the paywall is part 1 of the Unity (U) writeup along with links to my investment portfolio, investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models for current portfolio companies [click here]

Daily webcasts [click here]

**These are new links, I have to switch them up at the beginning of every month so former subscribers don’t have access. Sorry for the inconvenience.

Introduction

This is only going to be a partial introduction because of the information below, I’ll send some additional thoughts in part 2. After the Apple announcement today I need a couple days to digest that huge news and re-evaluate my investment thesis and investment models. I need to determine how bullish this news is for Unity over the next 3-5 years (spoiler: I think it could be very, very bullish)

Disclosure: Because I think this news could/should be bullish for Unity I started a 1.8% position today and here’s why… Apple had their big developer conference today where they unveiled their new AR/VR headset called VisionPro and during the presentation they announced some sort of exclusive partnership with Unity. I wasn’t able to watch that presentation today (I will tomorrow) but several of my friends texted me the news and I immediately bought some U because this has the chance to be a game changer for the company — it’s what we call a “needle mover”

I’ve been working on this U deep dive for the past couple weeks and I was going to send it out on Sunday but decided to hold off until after the Apple event just in case something meaningful was said that would impact Unity in a good or bad way. Unfortunately when that news broke today Unity’s stock price jumped by 20% in a matter of minutes (as you can see from the chart below) and cleared the 200d sma in the process but was unable to close above the 200d ema. I wasn’t able to buy at the lows today — my entry price was $36.75 and I’m willing to add on a pullback from here. The question is whether I continue to hold Unity if it can’t stay above the 200d sma at $32.36 — to be honest I’m not sure so I’ll cross that bridge if needed. I’m up 69% YTD in my investment portfolio and I’m willing to start new positions but I want to manage the downside and not get stuck in a big drawdown which means 10-12% max loss.

Even with the big move today Unity is still down 83% from the all time high in November 2021 so even if you don’t own the stock yet, if the news today is a true “needle mover” than there should be plenty of upside left for us.

Now that this news is out there regarding the Apple VisionPro and their partnership with Unity I’m really curious to see what that analysts do/say over the next couple weeks. I would expect some of them to raise their estimates and increase their price targets but the question is by how much? If the average PT is $39.29, I could see them increasing it by 20-30% with some very optimistic commentary.

Before today’s announcement I had Unity at $4.3 billion of revenues in 2027 but it’s possible this news means that number could be somewhere closer to $6 billion which changes everything. Using $4.3 billion of revenues in 2027 with 21% net income margins I was getting a 2027 price target of ~$65 which wasn’t quite enough to get me into the stock but now I think that 2027 revenue number could be closer to $6 billion and maybe that puts net income margins even higher (ie 24%).

Using the $6 billion of revenues and 24% net income margins (these are just my personal estimates as of now) gets me to ~$130 by end of 2027 which means that news today might have just changed the upside over the next 3-4 years from 100-150% to 250-300% but I don’t want to get too excited yet, it’s still very early and the VisionPro won’t even be out until next year so it’s hard to know exactly when Unity will see a meaningful bump in revenues.

Company Background

Unity Software was originally founded as a game development company called Over the Edge Entertainment in Denmark in 2004 by Nicholas Francis (left the company in 2013), David Helgason (ex-CEO, still at the company, serves as a Board member, and holds approximately 2.4% of the company), and Joachim Ante (served as a CTO until March 2023, still holds 5% of the company).

The trio was eager to launch a desktop game, despite having no prior experience in gaming. After a year of development, Over the Edge Entertainment released GooBall, an arcade-puzzle video game available on Mac OS X. Though this game was highly downloaded, it was not commercially successful. However, the founders discovered value in something else.

GooBall was built on the early beta version of what later became the Unity engine. In 2005, if you wanted to create a game, you had to build the game engine from the ground up. So the company decided to shift its focus from game development to creating an engine for other developers with the mission "to democratize game development."

In one of his interviews, David Helgason recalled, "We built a tool that was actually quite terrible from a performance perspective and a features perspective but somehow was easy enough that people could figure out how to use it. But we had no funding; we tried to talk to some venture capitalists, and they looked at us like – "Who the f*ck are you?" Back in 2004, it was just a fundamentally bad idea."

It took four years before investors started to take Unity seriously (Sequoia Capital was the first investor in the company, netting $7.8 million in 2009). The inflection point was Apple's introduction of the App Store in 2008. Unity quickly became the go-to platform for mobile game developers.

As part of its transformation from a tool into a platform, Unity followed Apple's success and introduced its own store, "Asset Store," in 2010, enabling developers to buy and sell artwork, audio, and other game products. Though it never became a big business for the company, the Asset Store played a massive role in forming a community of developers.

Just in several years, Unity grew to over 1 million registered developers. By 2012, over half of all mobile games were developed using the Unity engine. However, the company was still searching for a viable business model (Unity was free for anyone making less than $100,000 per year, which essentially was most of its users at that time).

In the hopes of growing revenue, Unity acquired Applifier in 2014. Its mobile video ad network later became Unity Ads. In less than six years, Unity became one of the top players in the global gaming ads market, with Unity Ads becoming the company’s largest revenue stream.

One of the main creators of this success is the company's current CEO, John Riccitiello, who joined Unity in late 2014 after serving as the CEO of Electronic Arts for more than six years.

Riccitiello helped the company sign many AAA studios and brought Unity beyond gaming into other industries. He also greatly contributed to Unity's successful IPO in 2020.

The company went public in the midst of the pandemic in September 2020, raising more than $1.3 billion at a staggering $13.6 billion valuation. Initially priced at $34-to-$42 per share, the interest in Unity was much higher. The stock began trading at $52 and closed at $68.35 per share.

Interestingly, the company chose who got the initial allotment of the shares instead of the investment bankers picking the investors. It allowed management to partner with investors who would hold the stock long-term.

At the time of the IPO, Unity had over 1.5 million monthly active users using the Unity platform, developing not only games but other applications across mobile, PC, and console. Unity software has been used to create almost half of all games across all platforms, including approximately 70% of the world's top 1000 mobile games.

Though the company crossed a $1 billion revenue run rate in 2021, it was still losing money heavily, and the net loss kept increasing. The company doubled its loss from 2020 to 2021, growing from $282 million to $532 million, mostly due to absurdly high stock-based compensation. Since its inception, Unity has accumulated a deficit of more than $2.5 billion.

In November 2021, the stock price hit an all-time high of $210 per share and reversed alongside all tech growth stocks. Since then, Unity's shares have seen a dramatic fall down, losing more than 80% of their value and trading 50%+ below the IPO price.

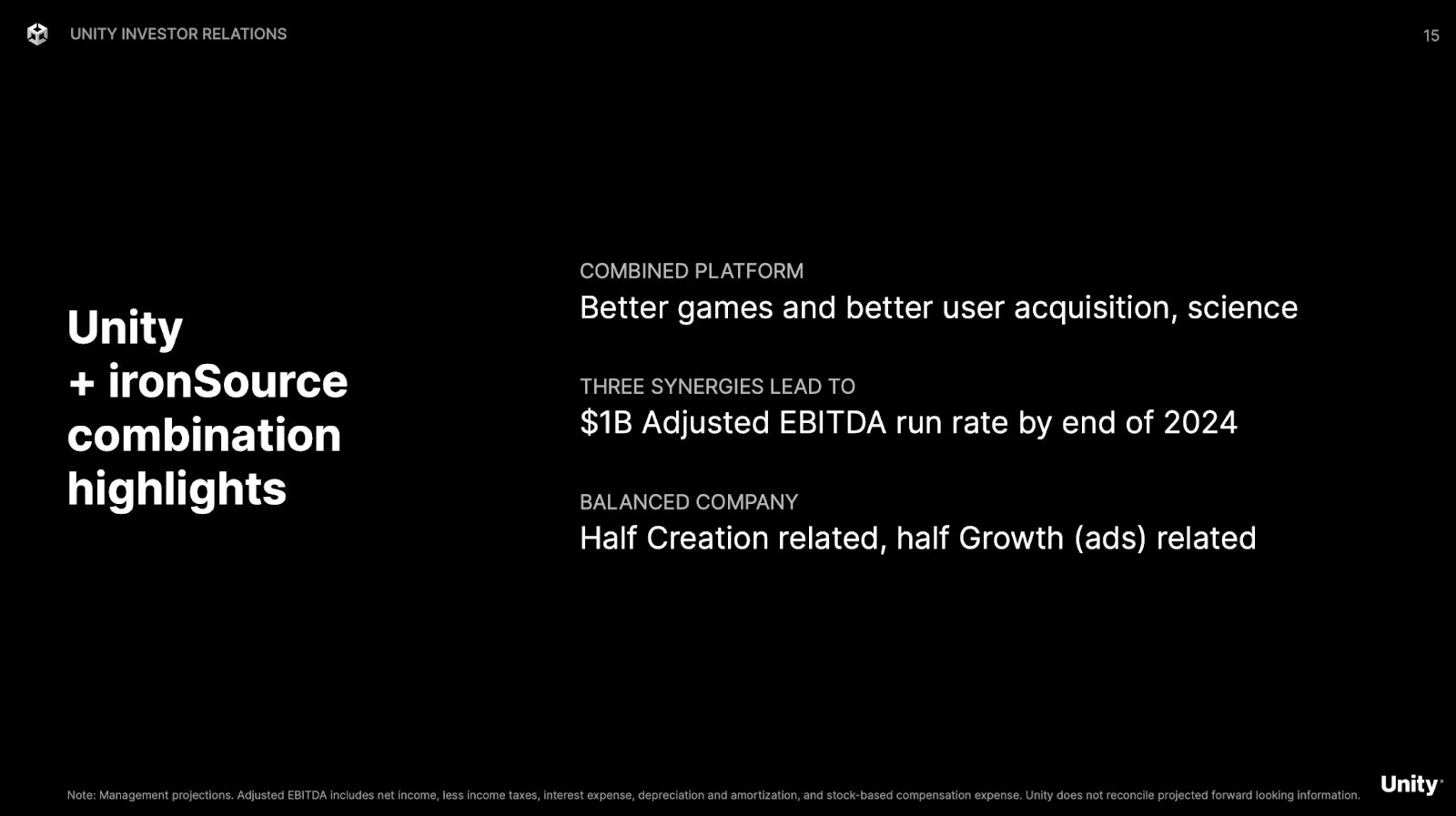

To shake things up, management began the company transformation in the second half of 2022. The first major move was the acquisition of ironSource, an Israeli-based software company focused on app monetization and distribution, in an all-stock deal worth $4.4 billion.

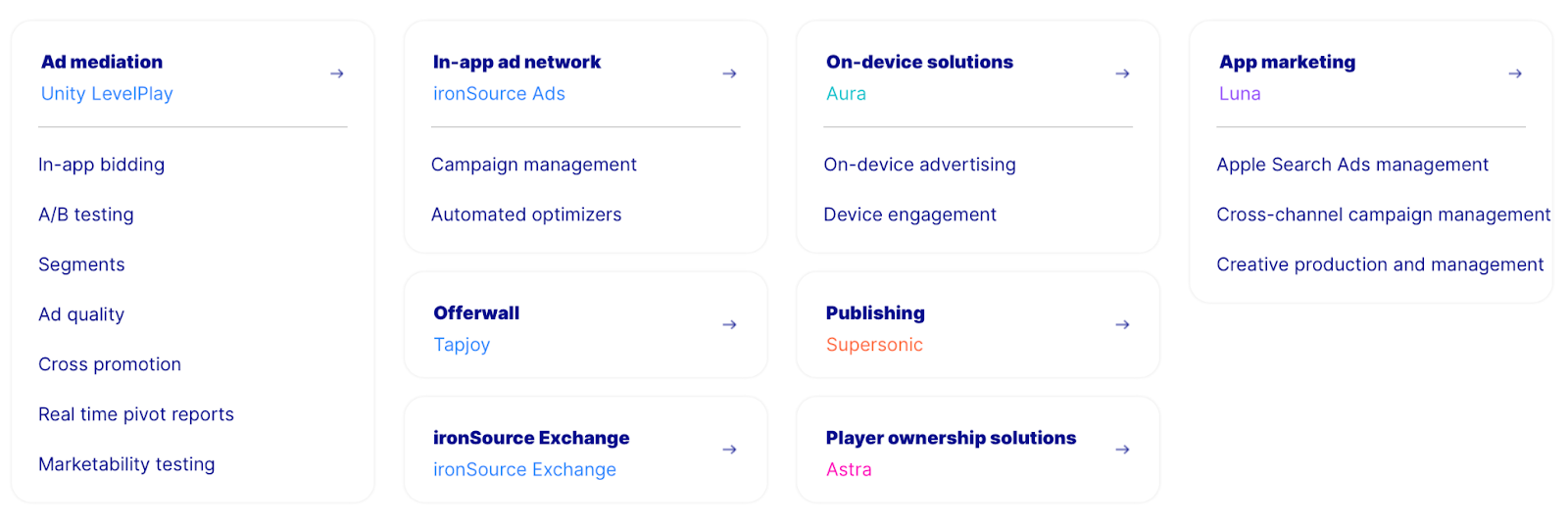

This merger is set to transform Unity's business and create a leading end-to-end platform designed to help creators build a game or app into a fully scaled business. The combined company now has best-of-breed offerings from development (Unity) to publishing (Supersonic), mediation (LevelPlay), ad networks (Unity and ironSource), marketing (Luna), and device management (Aura).

After the merger was completed, Unity reduced around 8% of its workforce (600 roles) in an attempt to restructure certain teams. The company also reduced the number of managerial layers to make the organization more agile and effective. Finally, the company is in the process of reducing the number of Unity offices to concentrate people and teams together and make it easier to collaborate and solve problems for its customers.

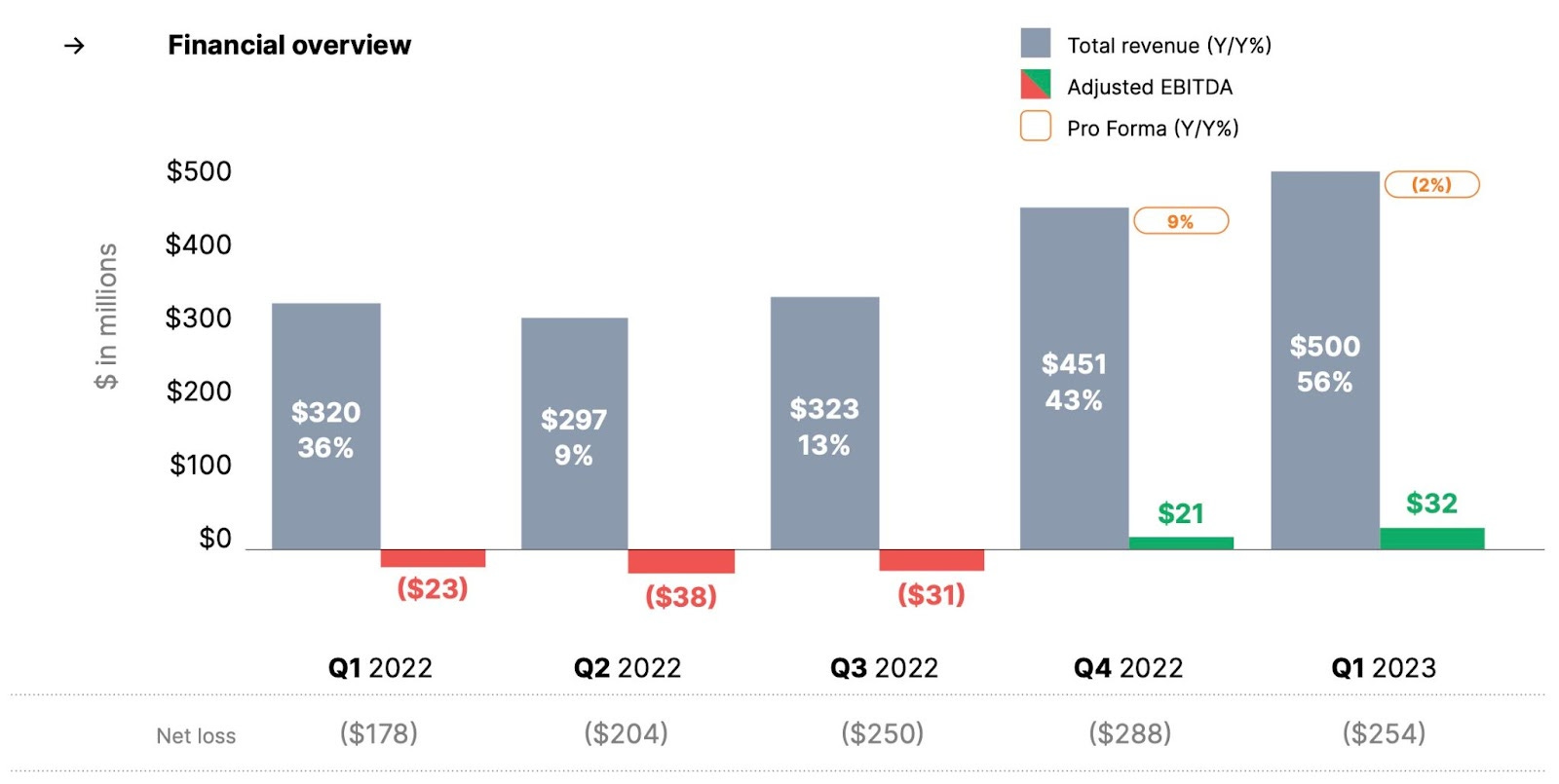

And it seems these efforts started to show some results. For the first time in its history, the company delivered a profitable quarter (on a non-GAAP basis, it is still deeply unprofitable on a GAAP basis) in Q4 2022 before showing another quarter with positive Adjusted EBITDA in Q1 2023 (thanks to ironSource). Management now expects to reach $1 billion in Adjusted EBITDA by the end of 2024.

Though there is still no clear path to real profitability (on a GAAP basis), the company is finally moving in the right direction. Unity aims to become the world’s leading and defining platform for real-time 3D content creation, operation, and monetization, and with the acquisition of ironSource, it is just getting started.

Opportunity

Trends

Unity benefits from several secular trends, some within the gaming industry (like the rise of in-game advertising and the increase in games being published), while others are in content creation in general.

Below are the major trends that will profoundly impact the company for many years ahead.

RT3D transformation

It is a very early stage of a substantial technology transformation, as content changes from mostly 2D to 3D, mostly from not real-time to real-time, and mostly linear to deeply interactive.

RT3D stands for real-time 3D, which offers a fundamentally more engaging and immersive experience than non-interactive, static content (2D).

With real-time 3D software, fully interactive 3D models, environments, and entire virtual worlds can be digitally rendered at lightning speed compared to traditional content-creation tools.

RT3D content can be deployed to mobile devices, computers, augmented reality (AR) and virtual reality (VR) devices, and other platforms.

Initially built for gaming, the RT3D technology is now driving innovation across various industries. It changes how products and buildings are designed, engineered, made, sold, serviced, and maintained across the lifecycle: from creating to building to monetizing.

RT3D is also the primary enabler of the metaverse, the next generation of the internet. Optimized 3D models are required to support this whole new interactive experience.

For companies from all sorts of industries, RT3D provides a number of critical benefits, including cost savings (reducing reliance on expensive physical prototypes and eliminating costly design and engineering flaws as early as possible), faster time to market, improved product margins, and increased sales (presenting products in compelling ways beyond traditional multimedia formats).

AI revolution

Generative AI will forever change the gaming industry. It will save so much time and money for game developers. AI won't replace artists but instead will boost their productivity. Creating a high-quality image will now take several hours instead of several weeks.

But Generative AI will be used not only for images but for virtually all assets involved in games, including dialog and music.

AI won't replace game engines like Unity, either. On the contrary, increased productivity in game development will mean a lower barrier to entry that will result in more games being developed and at a much faster pace. More games mean more business for game engines, as they are a critical part of the process.

AI will affect not only game development but also its monetization. More advanced AI models are now used to make bidding more effective and allow networks to win auctions at a much lower price.

The adoption of AI tools in gaming (and beyond) will be a tailwind for many years to come.

Total Addressable Market (TAM)

Unity has been constantly adding new capabilities and expanding its total addressable market with various acquisitions.

Gaming remains the largest and fastest-growing segment of media. The game development software market represents a small share of the total gaming market, with a size of approximately $1.15 billion in 2022, according to 360iResearch. This market is projected to grow at around 10% CAGR through 2030 and reach $2.5 billion. As of 2022, Unity already owned more than 50% of the game development software market (based on $716 million in revenue from game development tools). But it still leaves the company with a considerable growth opportunity.

A much bigger opportunity is in mobile game ads. According to Research Dive, the global in-game advertising market was around $8 billion in 2022 and is expected to grow to $17.5 billion by 2030, representing a CAGR of 11%. As of 2022, Unity penetrated less than 10% of the total market opportunity. Now combined with ironSource, Unity may significantly increase its market share in the coming years.

Finally, the market outside of gaming (the digital twin market) represents an opportunity larger than game development software and in-game advertising combined. According to Markets & Markets, the global digital twin market was estimated to be around $7 billion in 2022, but it is projected to grow to a whopping $74 billion by 2027 and may exceed $100 billion by the end of the decade, showing a CAGR of more than 40%.

Growth Drivers

Unity's growth strategy is primarily based on expanding the Create and Grow businesses worldwide.

Create

Create business primarily consists of everything related to development and operations. Growth in this part of the business is driven by new customers and expansion of relationships with existing ones.

Within the growing gaming industry, customers of all sizes are increasingly looking for various tools to accelerate development, and most of them choose Unity (and alternative engines) vs. building proprietary engines in-house.

Unity began with low-end studios but, in recent years, changed its focus to AAA studios. These larger studios (approximately 100 companies), which account for all the highest-grossing games, have historically been investing in the development of their proprietary game engines. One of the biggest opportunities here lies in driving migration from proprietary technology stacks to the Unity platform.

With those who already chose the Unity platform, the company has plenty of opportunities to broaden its relationships by selling additional subscriptions and services and cross-selling other solutions (from Grow segment).

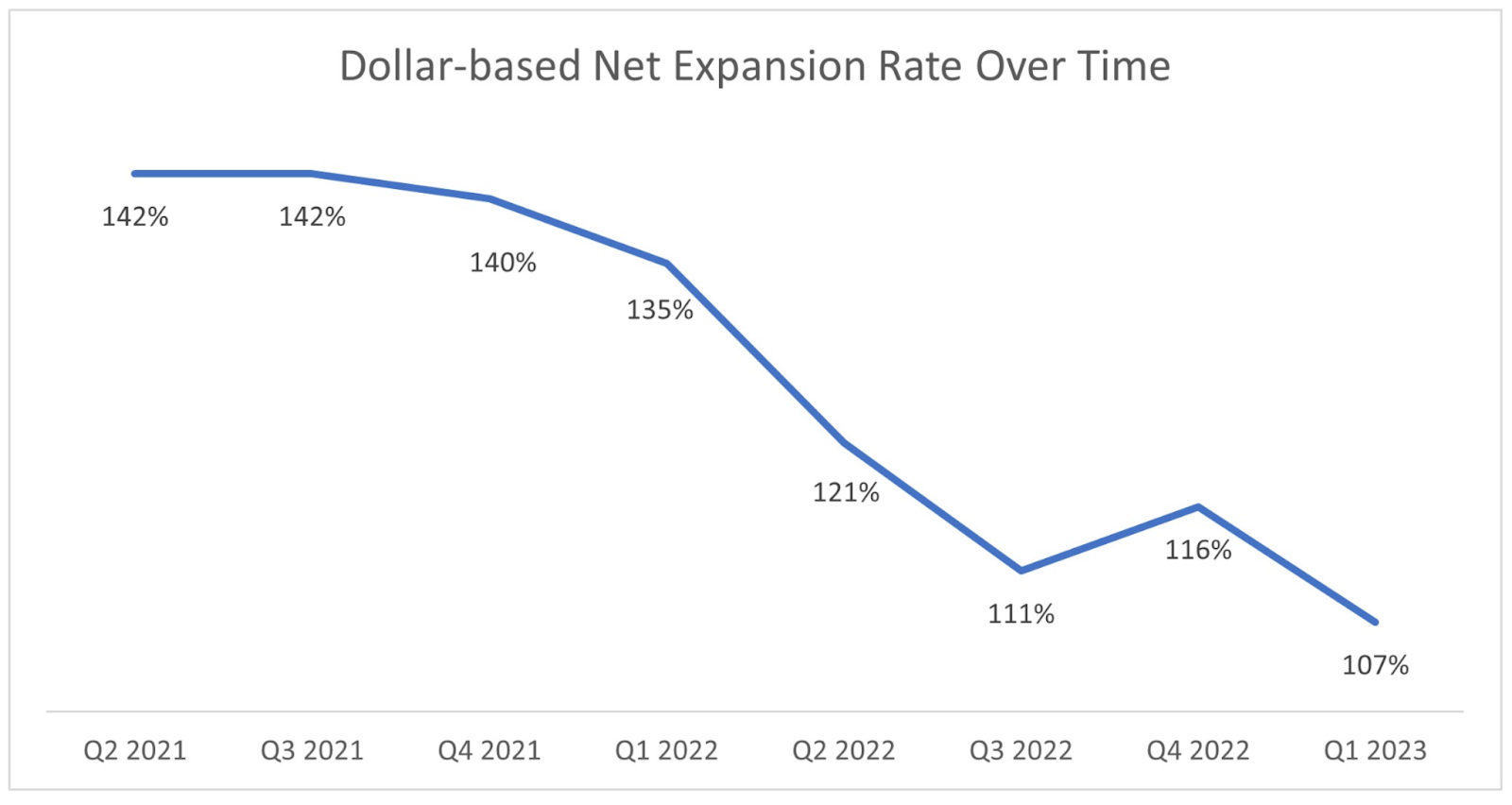

Until recently (due to the Grow business), Unity has been exceptionally strong in expanding relationships with existing customers, reflected in its dollar-based net expansion rate. It remains above 100%, meaning the company continues its expansion in existing customers' revenue even in the challenging economic environment.

While one of the company's main goals has always been to establish dominant leadership in gaming, management now wants to become the leading RT3D solution across various industries, with the most emphasis on energy, infrastructure, manufacturing, and eCommerce. As a result, the growth opportunities in Create business go far beyond gaming.

The Digital Twins solution (a dynamic virtual copy of a physical asset, process, system or environment that looks like and behaves identically to its real-world counterpart) saw over 100% YoY growth in 2022 and has already grown to around 40% of all Create business revenue, with hundreds of customers (including Volvo, VW, Mercedes Benz, eBay, Walgreen, Deckers Brands, Boeing, many more) leveraging its RT3D technology.

These are remarkable results for a product that went live for general use only in Q3 2022. Furthermore, management has repeatedly stated that demand for its Digital Twins solutions far exceeds the company's current ability to satisfy it.

Today, revenues from Digital Twins are insignificant, but they may surpass revenues from gaming in the coming years. The growth in this part of the business is Unity's hidden gem.

There is also a prospect of several tools like Weta (acquired back in 2021 and is a digital visual effects tool used mostly in cinematography, for example, the recently released Avatar: The Way of Water was made with Weta) and Ziva (technology that brings digital humans and creatures to life for films, television, and games). Both tools are coming to market in 2023 and will provide an additional opportunity for Unity in the Create business.

In the recent quarter (Q1 2023), the company shed light on its AI efforts and its implementation in the current set of tools. Embracing AI years ago, Unity is well-positioned to benefit from this long-term tailwind. Adopting AI tools will significantly accelerate Unity's business based on four structural and sustainable competitive advantages: the Unity Editor, the Unity runtime, the Unity Network, and Training Data.

The Unity Editor is a workflow and toolset for creating real-time experiences for both games and digital twins. Implementing AI inside the Unity Editor will enable creators to be more productive and bring even more creators, as building real-time 3D content and experiences will become much easier with the help of natural language and deterministic tools.

The Unity Runtime is what essentially makes 3D content interactive, real-time, and available on any device, as well as responsive to user input, physics simulations, lighting, and more. The company has been working on project Barracuda for five years, which brings an inference engine (an important part of generative AI capabilities) to the Unity runtime, enabling creators to do things that were not possible before, like populating game worlds with non-player characters that seem alive and capable of dynamic, responsive language dialogue with player characters and behaving in ways that will seem “real,” alive and not scripted. The Unity Runtime and Barracuda are also used in industries outside of gaming, making AI available at runtime and economically by delivering inference on the device.

The Unity Network, which includes analytics tools, ad networks, publishing systems, and cloud services, has also been using the power of neural networks for several years already, making Unity's services and tools constantly better.

Finally, AI tools, large language models, and generative AI tools all require training on data. What Unity does differently is it enables the training of models on 3D experiences and in real-time, which is far more valuable than training on just the language or visual output like a photo, film frames, or a rendering of a building. Through this training, Unity can create ever richer services built on top of the Unity platform, providing extraordinary capabilities to its customers and partners that others can't.

With the pace of investing in R&D and the history of acquisitions, Unity will keep introducing new tools, creating new growth opportunities beyond the current ones.

While Unity sells its development tools in all regions, the most significant opportunity comes from the Greater China region (China, Hong Kong, and Taiwan), which is currently insignificant for the company.

But China is the single largest market for mobile games. According to Statista, most revenue in the gaming industry in 2023 will be generated in this country.

Furthermore, China recently began giving out licenses to permit new games (it is mandatory to obtain permission to publish a game, even for domestic companies, and there is a special agency responsible for licensing video games in the country) more favorably than in previous years, with some saying that licensing will be lifted entirely very soon. It is a net positive for Unity as the company will be able to sell more Create solutions to developers in that region.

Grow

Grow business includes Unity monetization and all ironSource businesses, which in combination provide customers with a platform that encompasses testing, user acquisition, growth, and retention capabilities.

With Grow solutions, the company eyes becoming an integral part of the fundamental infrastructure of the gaming and app ecosystem.

Management wants to make Unity LevelPlay (a solution for managing and optimizing the entire monetization ad stack) and two Ad Networks (Unity Ads and ironSource Ads) as the leading mediation and Ad platforms for Android and iOS, as well as to establish Supersonic (the mobile game publisher) and Aura (on-device solution) as the leading players for independent publishing and device management.

Grow business is more dependent on the macro environment. Though it has seen more than 100% YoY growth in Q1 2023 (primarily because of the addition of the ironSource business, which has not been a part of Unity in Q1 2022), the management does not forecast a recovery in the in-game ads market in 2023. This market is expected to contract by approximately 10% compared to an uneven 2022. As a result, the company expects a pretty flat 2023 in this business.

But management plans to use this weak period to its advantage by scaling mediation and strengthening its Ad Networks by better meeting the needs of developers of all sizes, expanding into mid-market and apps beyond games.

Once the economy improves and the mobile ad market returns to growth, Unity will be in a much better shape with a much larger market share.

Business Model

Unity has a history of transforming its business model. The company began by providing its software on a license basis before shifting to a SaaS-based model in 2016.

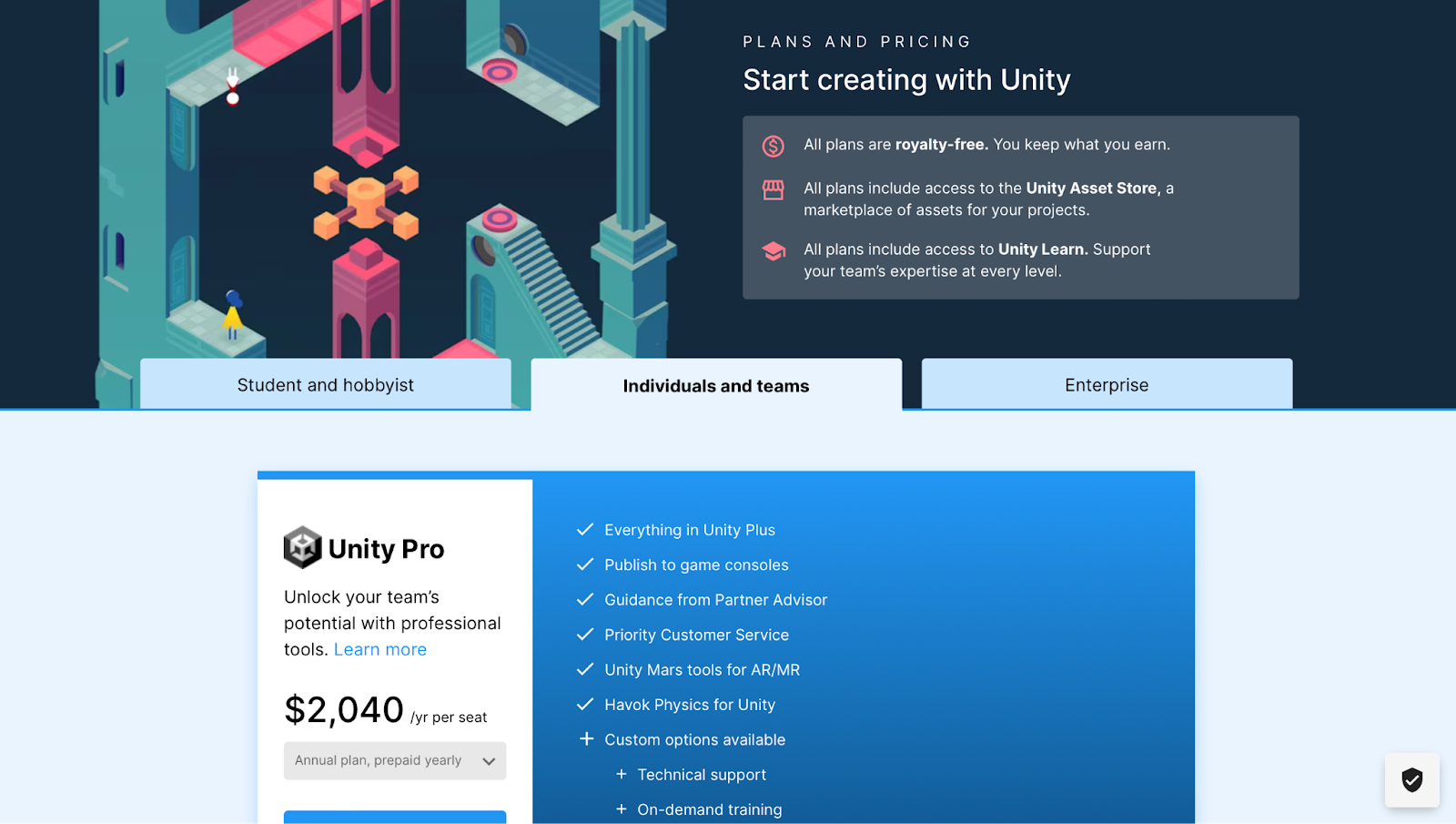

Anyone can begin using Unity software for free (Unity Personal) if he matches the criteria of having less than $100,000 of revenue or funds raised in the prior 12 months. If the revenue or funds are less than $200,000 in the prior 12 months, a user is eligible to use the Unity Plus plan, which costs $399 per seat / per year. For everyone else, the Unity software is available for $2,040 per seat / per year (Unity Pro). There is also an Enterprise plan, which includes everything from the Unity Pro plus expert engineering support, source code access, and extended Long Term Support. It costs $3,000 per seat / per year.

For customers from other industries, Unity offers a different plan. Unity Industry includes creation tools and enterprise-level support needed to transform CAD and 3D data into immersive apps and experiences available on any device. Unity Industry costs $2,950 per seat / per year.

The company has recently increased its pricing for all paid plans, the first increase in the last three years.

Unity does not charge developers a percentage of game revenues. But if a developer wants to monetize his game with ads, Unity takes a cut if Unity Ads or ironSource Ads are utilized in the app.

Revenue Streams

So, Unity generates revenue from two large revenue streams. First is the revenue from Create Solutions, which includes various subscriptions (discussed above), enterprise support, professional services, and cloud and hosting services.

Subscriptions provide customers access to Unity software that allows them to edit, run, and iterate interactive, RT3D, and 2D experiences that can be deployed to various platforms.

Support services are provided to enterprise customers and are sold separately from the subscriptions. The same applies to professional services (including consulting, platform integration, training, and custom application and workflow development) and cloud and hosting services.

The second revenue stream is from Grow Solutions, which primarily comes from monetization, user acquisition, and Supersonic. Such revenue is primarily generated under a revenue-share or profit-share model.

Monetization solutions allow publishers, original equipment manufacturers, and mobile carriers to sell available advertising inventory on their mobile apps or hardware devices to advertisers for in-app or on-device placements.

Unity retains an amount from the transaction it facilitates through its Unified Auction and Mediation platform.

Supersonic (part of ironSource) provides game developers with the infrastructure and expertise to launch their mobile games and manage their growth. For this, Unity takes a cut from in-app advertising in published games and, in some cases, in-app purchase revenue.

Revenue from Grow Solutions represents approximately 60% of total revenue, while the rest comes from Create Solutions. Over time, management expects Create Solutions to represent over half of the company's revenue as it adds new cloud and ratable services to its offering.

Gross Margin

Unity's costs consist of hosting expenses, personnel costs (including stock-based compensation), some overhead, third-party license fees, credit card fees, as well as amortization expenses related to intangible assets acquired through business acquisitions.

The costs have been on the rise in the past several years (primarily due to several acquisitions), growing from 22.35% of total revenue in 2021 to 31.58% in 2022. In the most recent quarter (Q1 2023), they were 32% of total revenue, providing the company with still a pretty healthy gross margin of 68%. Excluding hefty stock-based compensation and amortization of intangible assets, the gross margin would be 79%.

Operating Expenses

Operating expenses keep exceeding the total revenue. In 2022, they accounted for almost 130% of the total revenue.

The most significant component of the operating expenses is personnel-related costs, which include salaries and wages, sales commissions, bonuses, benefits, stock-based compensation, and payroll taxes.

The company has recently started implementing various strategies for keeping operating expenses under control, such as decreasing headcount, slowing down hiring efforts, reducing the number of managerial layers, and others.

Profitability

Though management made progress in reducing costs and putting a strong cost control program in place for 2023 to drive profitability, including reducing the impact of share-based compensation and dilution, the company is far from becoming profitable.

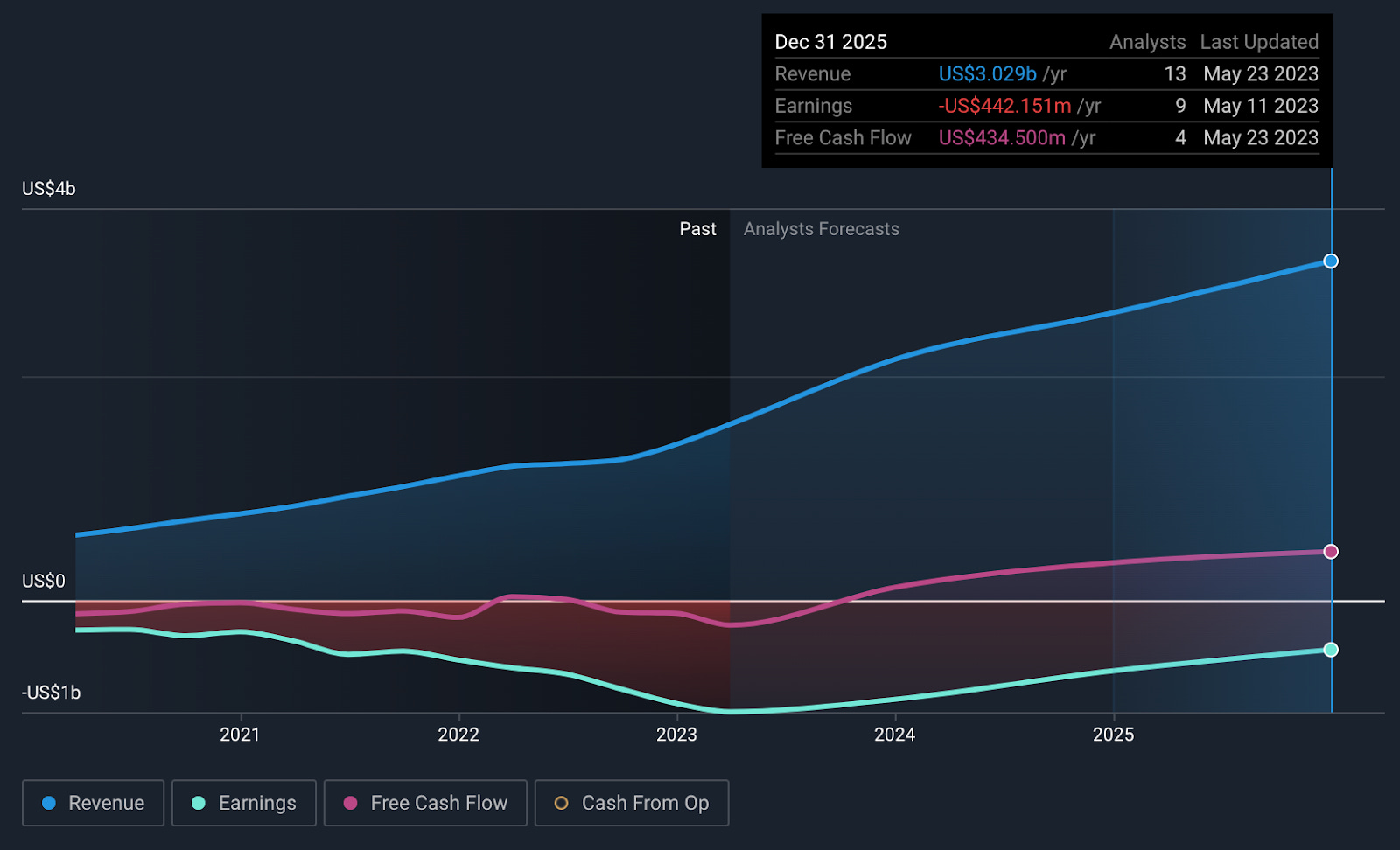

Yes, Q4 2022 and Q1 2023 were profitable on an Adjusted EBITDA basis, but real losses keep expanding: $289.3 million and $253.7 million, respectively.

While management promises to reach $1 billion in Adjusted EBITDA by the end of 2024, the consensus among analysts covering the company is that it won't reach positive earnings until after 2025 at a minimum.

Profitability prospects are getting killed by extremely high stock-based compensation and amortization expenses related to intangible assets.

SBC in 2022 was 39.5% of the total revenue and 5.25% of the company's market cap. In Q1 2023, the company added another $163 million in SBC, representing 32.5% of the total revenue in the quarter.

Since going public in 2020, despite share buybacks (based on a stock repurchase program according to which the company announced the repurchase of up to $2.5 billion of shares to offset the dilution after the merger with ironSource), the company has diluted its shareholders by more than 40%, while the stock price has declined by almost 60%.

Balance Sheet

Unity still has a pretty healthy balance sheet with total cash, cash equivalents, and restricted cash of $1.61 billion as of Q1 2023.

There is a long-term debt of $2.70 billion, $1.72 billion of which matures in 2026 under a 0% interest rate and $1 billion in 2027 under a 2% interest rate. Both borrowings are in convertible notes that can be converted into cash, shares of the common stock, or a combination of cash and shares of the common stock.

Cash Flow

Unity continues to burn cash, posting negative $116.5 million in free cash flow in 2022 while adding another $19.4 million in Q1 2023.

However, analysts covering the company expect it to turn free cash flow positive already in 2023, and the consensus is somewhere between $100 million and $120 million, a massive improvement from 2022 and much-needed cash to bolster either further growth or/and repayment of the debt.

*

Unity keeps innovating on its business model by introducing new differentiated offerings and pricing for different market segments and consumption models.

Furthermore, the company expects to increase its take rate through better-segmented pricing, adding ratable cloud services, and serving more creator roles.

At the same time, the company needs to take stock-based compensation under control to make all these efforts worth doing.

Competitive Advantages

Competition

Unity faces intense competition in all parts of its business.

In the Create business, the company competes against game engines built in-house by large developers on one side and some notable game engines like Cocos2d-x (Chukong Technologies) and Unreal Engine (Epic Games) that are used by thousands of other developers.

Perhaps, the main competitor on the game development front is the Unreal Engine, which has seen increased popularity with the success of Fortnite.

Unity and Unreal dominate the game development market. The main difference between them for a long time was their respective strategies: Epic Games began with higher quality games on PC and console, while Unity was used mainly by lower-end developers developing primarily mobile games.

Right now, both companies are meeting somewhere in the middle, with Unity moving to higher-quality tools for AAA studios and Epic Games moving down to mobile developers.

Unity and Unreal further compete beyond gaming, for example, in film and television production.

They face competition from established players like Autodesk, Adobe, and SideFX (Houdini), as well as various smaller software companies offering digital visual effects tools. With the recent purchase of Weta Digital, Unity has significantly boosted its position in this segment.

The competition in the Digital Twins market is also intense and comes from more mature companies, including Ansys, Autodesk, Amazon, Bentley Systems, Dassault Systèmes, GE Digital, IBM, Microsoft, Siemens, and Schneider Electric, among others. Unity is a relatively new player in this market.

In the Grow business, the company operates in a much more fragmented ecosystem, which comprises various companies, from small and private to specific divisions of large, well-established corporations like Amazon, Facebook, Google, Microsoft, and Tencent. For some parts of the Grow business, for example, the app publishing, Unity competes with companies like AppLovin.

Competitive Advantages

While Unity is only establishing itself outside the gaming industry, in the gaming space, even though it competes with other game dev engines and various Ads networks, there is really no other company that offers an end-to-end platform: from game development and publishing to user acquisition and monetization. Unity is in a league of its own.

Furthermore, the company has built some other competitive advantages that help it further win new customers and retain existing ones on the platform.

Technology

The breadth and depth of Unity's platform are the company's core competitive advantage. It is perhaps the most advanced platform for game developers (especially for mobile games).

And the amount of capital the company invests in research and development is beyond comparison. This allowed the company to build a market-leading position for real-time 3D tools and a reputation for innovation, which goes far beyond gaming.

Some technologies will drive future applications of real-time 3D in many new use cases, including autonomous driving, robotics, industrial automation, and virtual reality-based education and training.

Brand

Unity has established an industry-leading brand in the gaming industry. The company is now a true market leader for creating all types of video games, ranging from games developed by the largest global publishers, including AAA studios, to games developed by mid-sized, small, and independent developers and freelancers.

The numbers back this up: 70% of the world's top 1000 mobile games and 50% of all mobile, PC, and console games combined were made with Unity.

Furthermore, the brand recognition the company has achieved is also backed by the Unity Creator community, one of if not the largest, most active, and highly engaged global community of RT3D creators. This scale of this creator community provides a competitive advantage on its own. In addition, Unity strategically partners (through integrations) with various third-party platforms to further expand this community and retain Unity's platform’s position as the leading hub for RT3D content creation.

Switching costs

Once the developer chooses a game development engine and begins building out the ecosystem around it (with various tools and integrations), he will most likely remain a user for the life span of his operations.

If the developer further adds other solutions offered by Unity (like game publishing and monetization), the switching costs increase multifold.

Pricing power

Unity certainly has pricing power, being able to increase the subscription price (for all tiers) by almost 25% without losing key customers.

Unity additionally plans to increase the take rate in its monetization business later in 2023.

Risks

Profitability

Covered in detail in the Business Model section

Growth

The growth in the past several quarters and guidance for 2023 are supercharged by the ironSource merger. Without this merger, the company would likely report a much lower growth rate or even a decline in revenue growth. For example, in Q1 2023, on a Pro Forma basis, the company already saw a 2% YoY decline, meaning that a legacy business saw a decline in growth compared to the same quarter in 2022, indicating the possible maturation of this business.

ironSource merger

Unity's recent merger with ironSource presents a whole different set of risks for the company. Despite many synergies and benefits from this merger, it may require more capital and time to implement both businesses into one (especially the monetization part since both companies had competing products). There is no guarantee the merger will be successful in the end and contribute to the company's long-term growth.

Stock-based compensation (SBC)

Covered in detail in the Business Model section

Dilution

Covered in detail in the Business Model section

Indebtedness

Covered in detail in the Business Model section

Macro

Since the company generates more than 60% of its total revenue from the Grow business, it will be continuously impacted by the macroeconomic conditions, as well as longer sales cycles and reduced advertiser spending, until the conditions improve. The revenue from Grow Solutions will be adversely impacted in 2023.

Competition

Covered in detail in the Competitive Advantages section

Additional Sources

Management – https://unity.com/our-company#our-leadership

Board of Directors – https://unity.com/our-company#board-directors

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/0001810806/000181080623000037/unity-20230418.htm#ib5fd52273c00478bb2b940e23227c5d8_82 (page 36)

Key Metrics – https://www.sec.gov/Archives/edgar/data/1810806/000181080623000059/unity-20230331.htm#i8231058b7d3944318ea08e6e9b1a5fab_25 (page 17)

Enjoy the rest of your week.

As I mentioned before I need a couple more days to process this new development with Apple and then I’ll send part 2 with some additional thoughts on what I think it means for Unity longer term.

As a reminder, you can track my investment portfolio, my daily activity and join my daily webcasts through this spreadsheet [click here]. Please let me know if you have any questions.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.