Part 1: Deep dive on Toast ($TOST)

In order to read this deep dive on Toast ($TOST) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support.

Paid subscribers receive ~3 deep dives per month (~8,000 words) and ~3 mini deep dives per month (~2,000 words) plus access to my current investment portfolio (up +125% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up +120% YTD) and my trading portfolio (up +93% YTD) including lots of activity updates, charts, market opinions, macro analysis, earnings analysis, analyst upgrades/downgrades, webcasts and much more.

Company: Toast

Ticker: (TOST)

Website: https://pos.toasttab.com

IPO date: September 2021

IPO price: $40.00

Current stock price: $16.07

Outstanding shares: 540.20 million

52 week high: $27.00 on July 18, 2023

52 week low: $13.77 on November 22, 2023

ATH: $69.93 on November 3, 2021

Market cap: $8.68 billion

Net cash/debt: $1 billion

Enterprise value: $7.68 billion

Headquarters: Boston, Massachusetts, United States

Number of employees: 4,500+

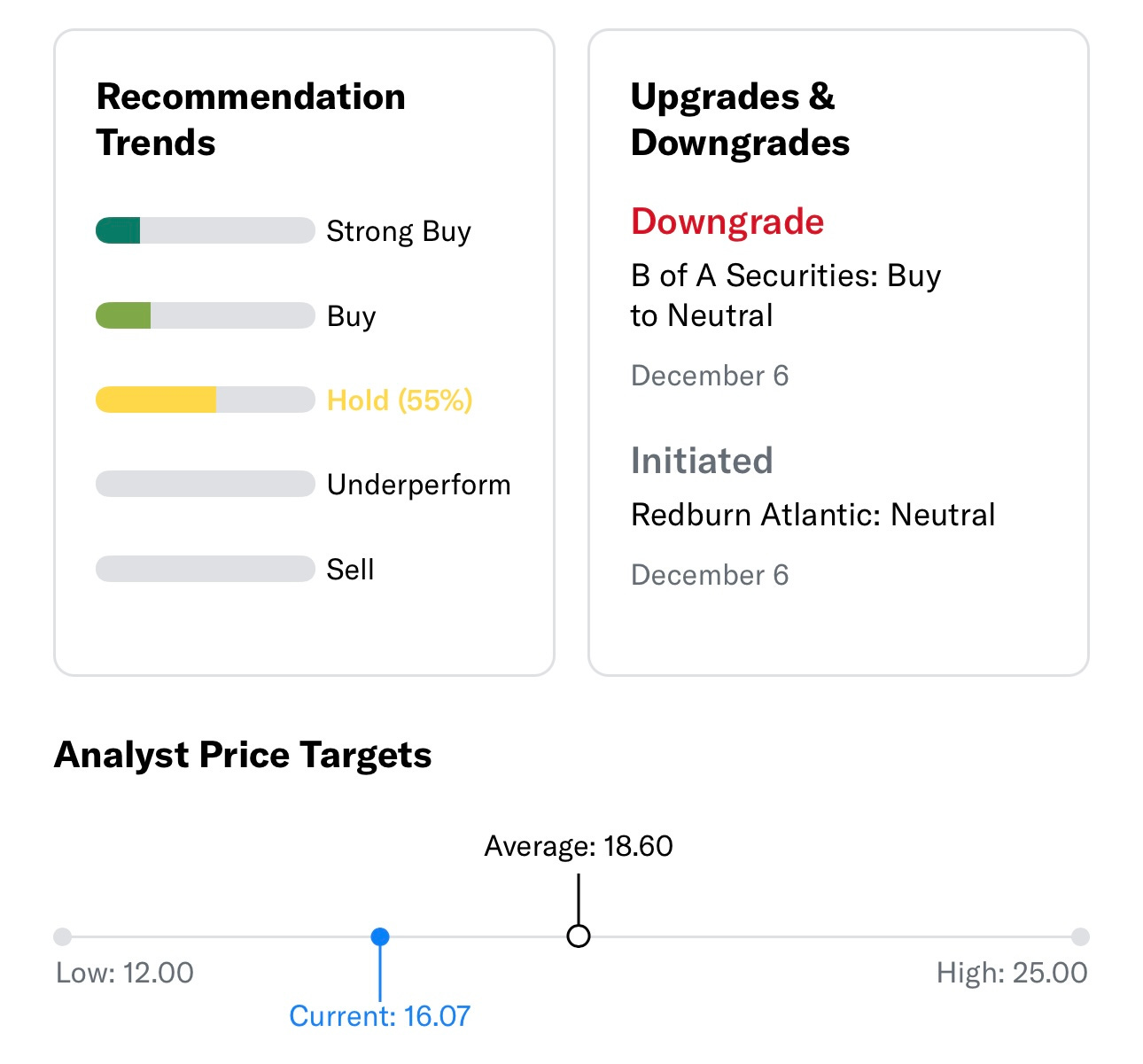

Average price target from analysts:

Investor Relations: https://investors.toasttab.com

Q3 2023 Earnings Report: https://investors.toasttab.com/overview/default.aspx

Investor Presentation November 2023: https://s28.q4cdn.com/141746709/files/doc_financials/2023/q3/TOST-Investor-Presentation-Q3FY23.pdf

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1]

As a paid subscriber you have access to my:

Investment portfolio: https://docs.google.com/spreadsheets/d/1oqNvhyZH76EWdQPM7faTjqCthvskiNPNCOIEG295raE/edit#gid=0

Investment models: https://docs.google.com/spreadsheets/d/1kQnr_KNJVBXOdFb6fxWrpyQp4PpjE8wLjxTjqO3LJXQ/edit#gid=527845503

Daily webcasts: https://docs.google.com/spreadsheets/d/1oqNvhyZH76EWdQPM7faTjqCthvskiNPNCOIEG295raE/edit#gid=1687267844

Introduction

I do not currently have a position in TOST (in either of my portfolios) however it’s definitely on my watchlist for a variety of reasons. TOST is down -75% from the all time highs and the valuation has gotten more compelling however they do operate in a very competitive industry which is one of the major risks. I currently have positions in FOUR and SQ which do have some overlap with TOST so it’s unlikely that I need to own all three of them. If I did buy TOST it’s more likely that I’d buy it in my trading portfolio once it pushed through the 50d sma/sma which could happen as soon as tomorrow.

TOST valuation does look more compelling (compared to the IPO) but this is still not a cheap stock. TOST currently trades at 60x NTM EV/EBITDA which sounds high however if the analyst estimates are correct, TOST will increase EBITDA from $46M in 2023 to $617M in 2027 which is a 91% annualized growth rate (which justifies the current EV/EBITDA multiples)

Speaking of analyst estimates, the numbers look fantastic for TOST, the question is whether they’ll be able to achieve them and to be honest I just don’t know. If I had more conviction in their ability to hit these estimates I’d probably be more aggressive buying the stock at these prices. If TOST can grow revenues from $3.8B in 2023 to $8.4B in 2027 while expanding net income margins from 1.4% to 7.0% then the stock will do very well.

If we plug the analyst estimates into my investment model there’s definitely some decent upside over the next ~3, FWIW, $16 to $45 over the next ~3 years would be a ~41% CAGR which most investors would be very happy with.

I do think TOST has made a couple execution missteps in the past year, first of which was their decision to add a new $.99 cent fee but then the blowback was so vicious they had to backtrack that decision. This fiasco did lead to a stock selloff in the summertime, with recovery and then they reported a disappointing Q3 results (although it was mostly the guidance that missed) which took the stock down another 15-20%. Personally I think we need to see some consolidation in this industry otherwise it’s a “race to the bottom” on pricing which hurts margins for everyone.

If I do start a position in TOST in the coming days or weeks, I’d either buy the stock after it pushes through the 50d ema/sma then use that spot as my risk management (ie stop loss) or I’d consider buying TOST on a pullback to the 21/23d ema.

Company Background

Toast was founded in 2011 by three ex-Endeca (a software company that sold eCommerce search, customer experience management, enterprise search, and business intelligence applications and was acquired by Oracle for $1 billion in 2011) employees, Steve Fredette, Aman Narang, and Jonathan Grimm.

All three co-founders are still with the company, with Steve Fredette serving as Toast's president and director and leading product and innovation initiatives (Fredette still owns approximately 6% of the company worth nearly $500 million), Aman Narang is an in-coming CEO of Toast (effective January 1, 2024), after taking over this position from Chris Comparato, who served as the CEO since 2015 (Narang owns about 4.4% of the company worth circa $360 million), and Jonathan Grimm, who served as Toast's CTO for ten years before moving on to lead Toast.org, the philanthropic branch of Toast (Grimm owns around 4.7% of the company worth about $388 million).

The trio originally started by building a mobile payment app for restaurants, but there wasn’t a lot of demand for it. However, after talking to several dozen restaurants in the Boston area, they found a need for a better point-of-sale (POS) system.

At that time, POS systems were limited in their functionality and pretty slow. Taking orders and payments at the table took much longer, and the overall user experience was different than it is today. Every single restaurant that the Toast co-founders talked to said they were not satisfied with current solutions and wanted their POS to do more.

It took almost two years and $500,000 in seed investment to build a point-of-sale device and software for restaurants from the ground. It was not just a simple transaction processor but a comprehensive tool that could manage menus, process orders, track sales, and provide analytics. In late 2013, Toast had its first pilot customer before hundreds of new restaurants started to form a line to join Toast.

This early success was due to many reasons, but perhaps the primary one was the choice of the operating system on which Toast was built. Unlike most competitors that were running on iOS, Toast chose Android, which allowed the company to offer a more cost-effective and customizable solution to restaurant owners. It helped win many new customers.

By 2015, Toast POS had become highly adopted in Boston and nearby area restaurants, and the company began expanding to new markets. Starting in 2016, the company saw parabolic growth, substantially increasing the number of restaurants from a couple of hundred to tens of thousands all across the US.

Between 2016 and 2018, the company introduced a number of new features, including online ordering, delivery service integration, and advanced reporting and analytics, becoming the most comprehensive POS for restaurants on the market. In 2018, Toast also introduced Toast Go, the first generation of its fully integrated point-of-sale handheld, which combined hardware, software, and payments in one handheld device. This completely revolutionized point-of-sale transactions in restaurants.

2019 marked a year when Toast began expanding beyond products to run the restaurant. The company diversified into team management, introducing offerings to help restaurants manage their staff more effectively.

Restaurants are very complex businesses, and they need much more than just being able to accept orders from guests. They must manage the entire team, including payroll and HR, run inventory, attract new guests, grow their business online, and much more.

The latter is where Toast shined the brightest when the pandemic hit the restaurant industry. This industry was actually among the hardest hit, with many restaurants forced to close and operate for takeaway and delivery only. Toast responded immediately by adapting its offerings to support restaurants in these challenging times, introducing features like contactless payments, online ordering, and delivery integration with third-party delivery services.

Despite restaurant sales declining by 80% in most cities, Toast had the best year in its history (at that time), delivering $823 million in revenue, which represented an increase of almost 24% compared to the pre-pandemic year of 2019. The growth accelerated into 2021 with the sales rapid rebound. The company delivered a 64% YoY increase in revenue in Q1 2021 and a 193% YoY increase in Q2 2021 before it went public.

Toast had a highly successful IPO in September 2021, initially pricing its shares in the range of $30 to $33 but starting to trade at $40. The stock soared 56% on the first day of its trading and closed at $62.51, valuing the company a whopping $31 billion.

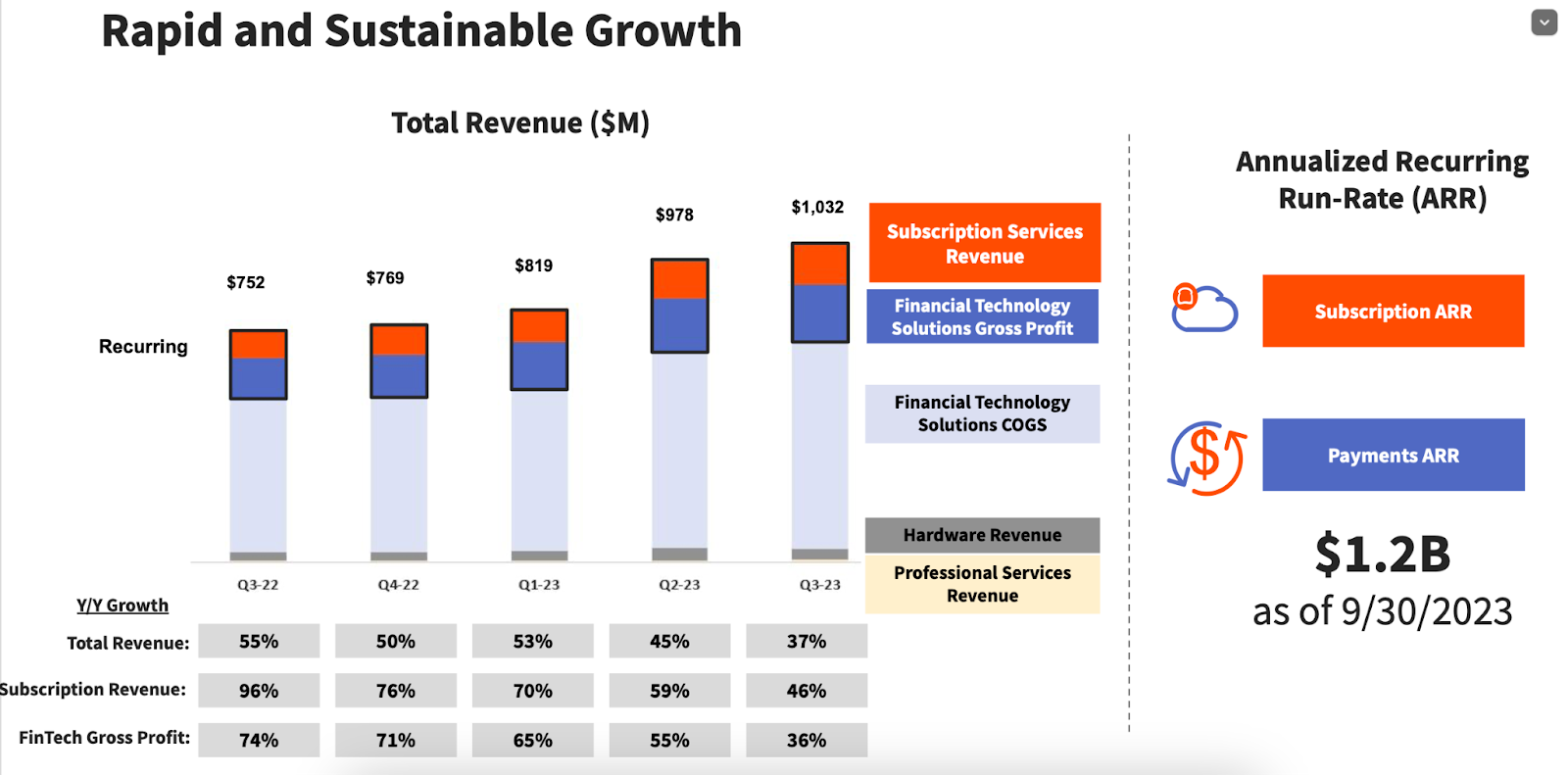

However, since its IPO, Toast lost more than 70% of its value, trading at ~$15 per share at the moment of this writing, though revenue growth has been pretty strong in the past two years: $1.7 billion in 2021 (+107% YoY) and $2.73 billion in 2022 (+60% YoY). The company is on the path to delivering $3.84 billion in revenue in 2023 (+41% YoY).

What has been dragging Toast down is its valuation at which the company went public and its continuous losses in a high-interest rate and inflation environment. Though the company is several years away from becoming profitable on a GAAP basis – current estimates suggest that Toast will deliver positive earnings only sometime in 2026 – Toast finally turned adjusted EBITDA positive in Q2 2023. The company is projected to significantly accelerate the growth of adjusted EBITDA in the coming years.

Overall, the focus in the near term is on balancing long-term growth with durable operating leverage (through payment processing revenue – acquiring a restaurant increases payment processing revenue without a significant increase in S&M, R&D, or G&A expenses) as the business continues to scale. Today, Toast is no longer just a POS for restaurants; it is an all-in-one, integrated platform for all restaurant's needs, covering both front-of-house and back-of-house operations.

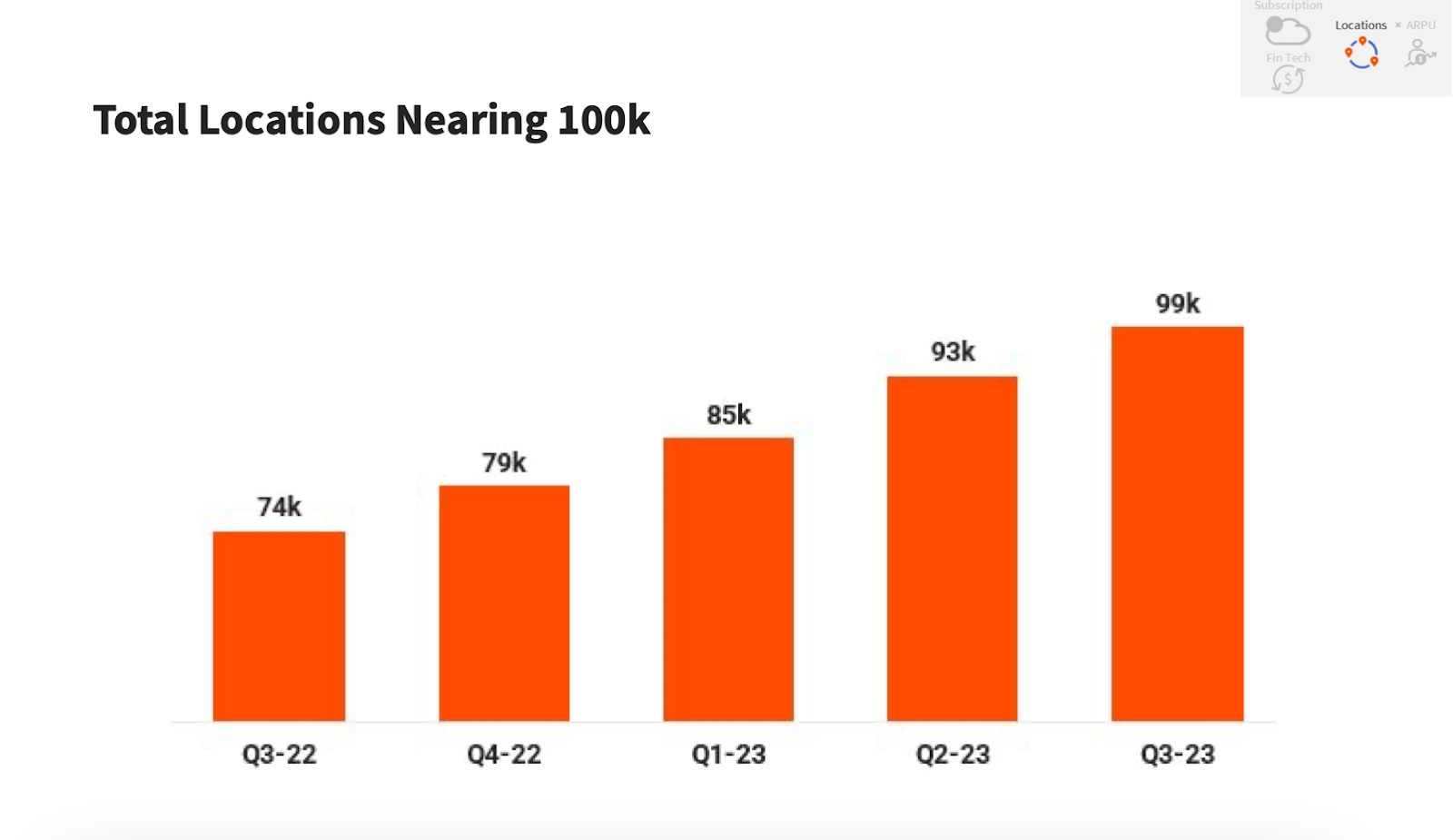

As of Q3 2023, approximately 99,000 restaurant locations, processing roughly $118 billion of gross payment volume in the trailing 12 months, used the Toast platform to optimize operations, increase sales, engage guests, and maintain happy employees. But it is a tiny fraction of the overall market opportunity. So, for Toast, the main goal going forward is to capture as much market share as possible in a highly competitive market that will only get more competitive. Once the critical mass of restaurants join and use Toast more, and thanks to high switching costs, the earnings will follow eventually.

Opportunity

Toast operates as a technology platform in the restaurant industry, which has experienced significant evolution and growth in recent years. This growth has been driven by a number of trends, including the increasing adoption of digital solutions, demand for integrated solutions, the rise of online ordering and delivery, contactless and mobile payments, the need for efficient operational management in restaurants, and others.

Trends

Shift to cloud-based solutions

Restaurants have historically struggled to adopt technology at the same pace as other industries, primarily due to the lack of dedicated IT resources. This is particularly evident in small and independent restaurants without dedicated IT staff, making implementing and managing complex technology systems challenging and also expensive.

The emergence of cloud-based solutions like Toast has addressed these challenges, enabling more restaurants to leverage technology to improve their operations, customer experience, and, ultimately, their profitability.

Cloud-based solutions don't require extensive hardware installations, significant upfront investments (they operate on a subscription model vs. extensive upfront costs of traditional systems), or any maintenance (usually done by the vendor). These solutions are tailored for each restaurant specifically and can be scaled up or down based on the restaurant's size and needs at any given moment.

Ease of implementation and use, flexibility, and cost-effectiveness are not the only advantages of cloud-based solutions. They provide something that legacy systems can't, from real-time data analytics and insights to integration with other tools and platforms (such as online ordering systems, delivery services, and customer relationship management software) to enhanced security, compliance, and accessibility.

The shift to cloud-based solutions like Toast represents a significant advancement in the management of restaurants, and more and more restaurants will turn to such solutions in the coming years to drive more growth and operate more efficiently.

Consumer preference change towards omnichannel dining

The omnichannel experience in restaurants is a trend that reflects the evolving landscape of how consumers interact with food service businesses, from how they order and where they eat to the means they use to pay.

It involves integrating various channels, including dine-in, drive-thru, takeout, delivery, and digital ordering. The COVID-19 pandemic has led to a significant increase in consumer demand for omnichannel dining options. But this trend is driven by not only changing consumer preferences but also technological advancements.

Companies like Toast have enabled restaurants to provide an omnichannel experience at a low cost and more effectively. There is a strong pattern in an increased number of service models restaurants offer today, allowing guests to choose the type of service that best suits them. The trend of omnichannel dining is expected to continue growing with more innovative approaches as technology evolves, further expanding the number of restaurants offering such an experience.

The growing need for efficient operational management in restaurants

Efficient operational management involves optimizing restaurant performance, enhancing customer satisfaction, and ensuring financial viability. This starts with simplifying and optimizing daily operations such as order taking, food preparation, service delivery, and payment processing. Streamlining these reduces wait times, minimizes errors, and improves overall customer experience.

Next is managing staff schedules, roles, and responsibilities to ensure adequate staffing during peak hours while avoiding overstaffing during slower periods. It also includes training staff to enhance their productivity and service quality.

Implementing effective inventory management practices is also an important task. This helps reduce waste, control costs, and ensure the freshness of food items.

Other processes are overall cost control, quality assurance, compliance and safety, and a few others. All of these processes require different technologies, from point-of-sale systems to inventory management software to digital ordering platforms. It is only possible with all-in-one solutions like Toast.

As the restaurant industry evolves, efficient operational management will become even more critical and will drive demand for solutions like Toast.

Total Addressable Market

The restaurant industry is one of the largest consumer industries in the US and globally. There are approximately 860,000 restaurant locations in the United States and over 22 million in the rest of the world.

Having been on the market for more than ten years and having already experienced rapid growth, Toast is still in the early stages of capturing its addressable market opportunity. As of Q3 2023, Toast served less than 10% of the total number of restaurants in the US, while its Annualized Recurring Run-Rate (ARR) was approximately 2% of the addressable market opportunity of $55 billion. Globally, this opportunity is twice as large as in the US.

Currently, the core segment that Toast serves is small-to-medium businesses, which also drive most of the company's growth. More recently, the company has seen some momentum in the mid-market segment and is slowly but surely moving to up-market.

Management believes that the whole restaurant TAM will open up for Toast over time, and it is one of the key priorities for the company to unlock it.

Growth Drivers

Toast has seen incredible revenue growth in the past two years, exceeding consensus expectations. The company is expected to deliver yet another strong year in 2023, growing its revenue by 41% despite numerous challenges the restaurant industry has started to face.

Despite the current consensus that revenue growth will decelerate in the next several years, Toast is still estimated to grow its revenue at 20%-25 % CAGR while Adjusted EBITDA will increase by triple-digits.

Investing in its core market (the US) remains the company's primary focus in the coming years. With available cash from it, Toast plans to invest in other bets, like international expansion and going beyond restaurants into different verticals.

New customers

The biggest opportunity for Toast in the near term lies in growing its market share in the US. The relatively small current market share (~99,000 locations, representing <10% of the total number of restaurant locations in the US) suggests a long runway for expansion domestically. And Toast must grab as much market share as possible in the coming years while it has the advantage of a more restaurant-focused product than its competitors.

There is a vast number of restaurants across the US that Toast can target. Small restaurants remain the primary focus, as they either use legacy solutions or several products from different vendors.

To capitalize on this opportunity, the company heavily invests in its field-based go-to-market engine and customer success through a combination of tailored onboarding services, customer support, and intuitive product design. Building strong customer communities is Toast's secret sauce. As a result, 3 out of 4 new locations come from inbound channels, while 1 out of 5 new locations come from other restaurant or partner referrals.

Toast uses a land-and-expand motion, where most customers start with one product and expand to more over time. Most recently, the company started to roll out new packaging plans, combining more products in one than previously, leading to more sales.

While Toast focuses on the ARR metric, ARPU per customer is also important. With more innovation, new packaging, and pricing, the company can significantly drive ARPU over time.

Existing customers

While growing the market share is undoubtedly the primary long-term growth driver, in the near term, growing existing customers is Toast's bread and butter.

This growth comes from continued location growth among the existing customers, as well as upselling these customers with new products and offerings.

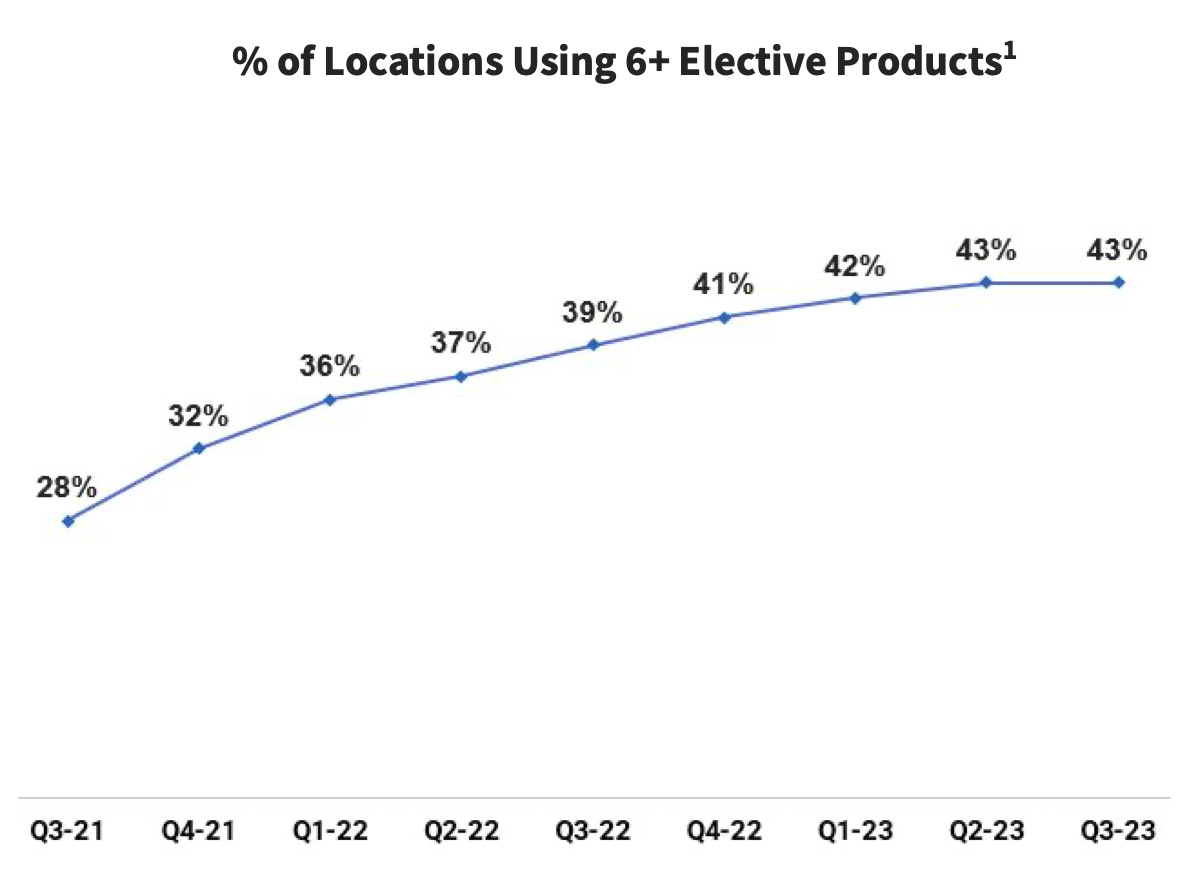

The company has been highly successful in the latter in the past several years, increasing the adoption of its full suite of products among existing customers. The number of customers using 6 or more products increased from 28% in Q3 2021 to 43% in Q3 2023.

The adoption of more products has significant benefits for restaurants. For example, as more restaurants start to offer online ordering solutions, they begin to collect guest data that was previously unavailable. This data can then be used to fuel marketing and loyalty solutions, which will help them bring guests back to the restaurant either physically or online. Driving more guests to the restaurant’s online ordering channel with Toast also helps restaurants eliminate third-party commissions.

Thus, Toast is focused on two areas: investing heavily in the upsell team and introducing new products and offerings. The former is working well for the company: upsell motion is as strong as ever. Not only is the number of customers above the $10k ARPU threshold growing fast, but about half of these customers come from the upsell channel.

The latter is where Toast has been historically strong and excelling. The company has built the most sophisticated platform on the market, offering various products across several categories: restaurant operations & point of sale, digital ordering & delivery, marketing & loyalty, team management, supply chain & accounting, financial technology solutions, and platform & insights.

The company keeps innovating (spending on R&D has been solid at around 10% of the total revenue in the last three years) and expanding the functionality of its current platform while broadening the subscription services and financial technology solutions.

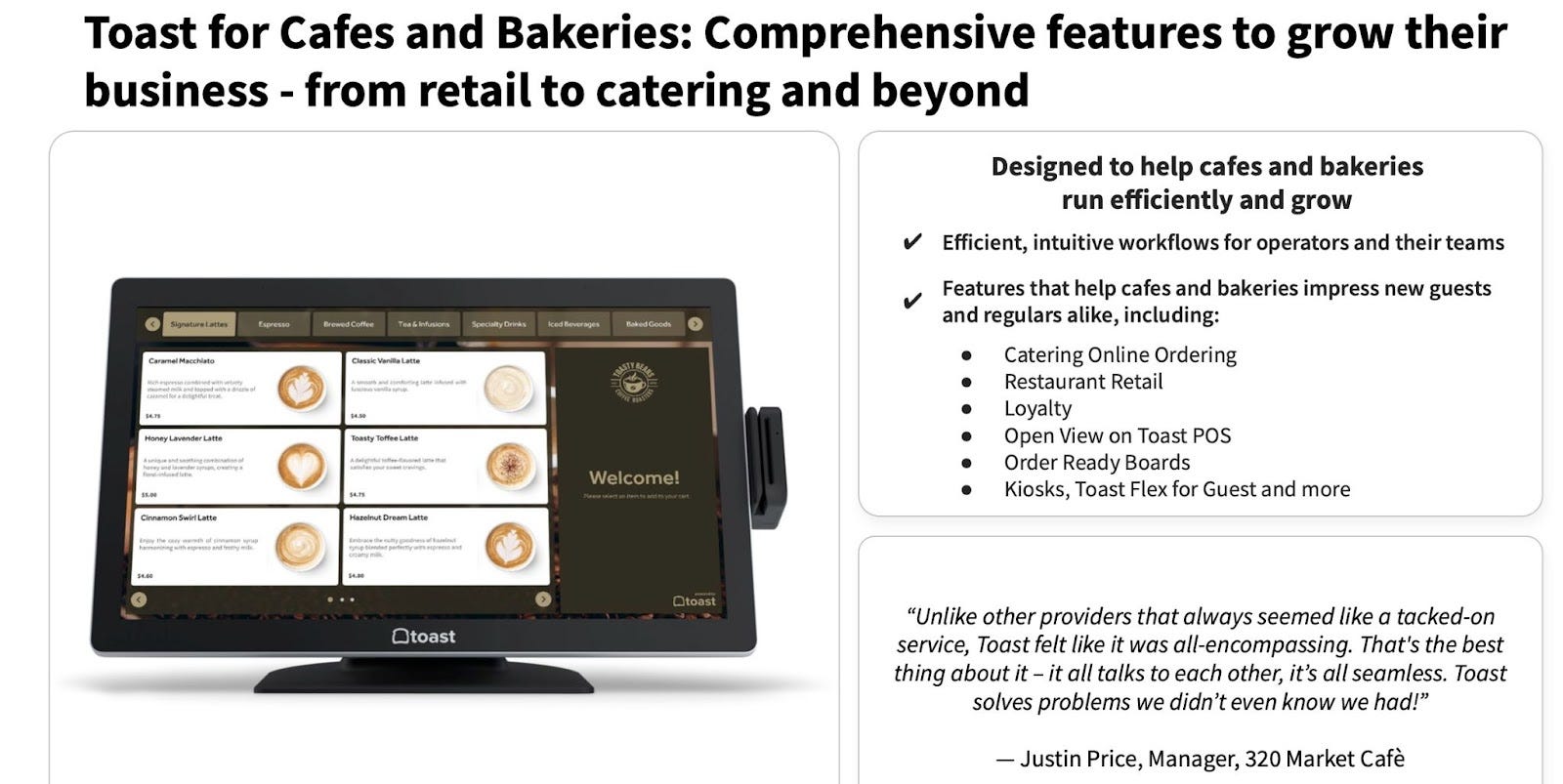

Just recently, Toast introduced a solution for cafes, coffee shops, and bakeries to help them add new revenue streams, speed up service with faster workflows, and grow their business overall.

Toast also announced significant updates to the overall Toast platform, including the launch of a new mobile app (Toast Now) and an enhanced point-of-sale experience. The new Toast Now mobile app is designed to meet the dynamic nature of how owners and operators manage restaurants, and Toast’s new POS experience has been reimagined from the ground up, resulting in a system that is easier to set up, learn and use. About 20% of restaurant owners downloaded the Toast Now app, which resulted in 3x engagement with the Toast backend.

The company continues to expand the ways in which it leverages the data on its platform to help customers succeed. These innovations will help to grow ARPU over time.

International expansion

Toast has been slowly rolling out its platform outside of the US. It is far from the offering available in the US, but more products will be launched in the coming quarters. The company has started seeing momentum in international markets, so more investments will follow in this initiative.

The international opportunity is in the very early stage and is a long-term initiative for the company, but it presents a huge opportunity to drive ARPU as the company grows internationally.

As of Q3 2023, Toast is in the process of building an international sales team and investing in targeted research and development efforts to address this $110+ billion market opportunity.

New verticals

Toast is known for its restaurant all-in-one platform, but the company has recently introduced a solution for the so-called restaurant/retail hybrid. The company utilizes its one unified POS for food service & retail – these are restaurants that also have shops (like wineries).

Last quarter, Toast tapped into the hotel restaurant vertical by announcing a giant global deal with Marriott Hotels. This is another example of how the company is opening its TAM. We should expect more of such deals in the coming future.

Partnerships

Finally, the further development of its partner ecosystem provides Toast with additional opportunities to grow its platform. Today, the Toast platform can connect to over 200 partners, providing its customers with the tools and features they need to run their business, including employee management, reservations, inventory, accounting, security, analytics, marketing and customer relationship management, loyalty, mobile pay, gift cards, online ordering, and digital signage.

Having more partners does not directly lead to new customers, but it helps to deliver more value to existing customers and increase the strategic nature of the Toast platform.

Business Model

Toast operates an integrated software and payments business model. The company generates revenue from four main sources, two of which are on a recurring basis, and two are one-time.

Subscription services revenue comes from fees charged to customers for access to Toast software applications. The subscription services revenue is primarily based on a rate per location, which varies depending on the number of software products purchased, hardware configuration, and employee count at each location. It is a recurring revenue stream, and subscription services are generally offered over a term ranging from 12 to 36 months.

Revenue from financial technology solutions consists primarily of transaction-based fees customers pay to facilitate payment transactions. So, every time a guest pays for the meal, the restaurant bears a percentage of the total transaction amount processed plus a per-transaction fee. Toast handles the credit and debit card processing for all of its customers. When restaurants grow, Toast grows through higher payment volume.

This revenue stream also includes fees earned from working capital loans provided to restaurants through Toast Capital. A third-party bank originates these loans, and Toast Capital then services them using Toast’s payments infrastructure to remit a fixed percentage of daily sales until the loan is paid back. Toast Capital earns a servicing fee as well as a credit performance fee that is tied to the portfolio performance.

Toast also generates one-time revenue from hardware sales that include terminals, tablets, handhelds, and related devices and accessories, as well as professional services that include fees charged to customers for installation services, including business process mapping, configuration, and training.

As of Q3 2023, subscription services accounted for 12.6% of total revenue, financial technology solutions – 82.6%, hardware – 3.7%, and professional services – less than 1%.

Recurring revenue growth is the top priority for the company. It includes the fintech gross profit and subscription gross profit – both are continuously growing.

Gross Margin

Since over 80% of total revenue comes from processing fees, a big part of which is paid back to card networks and other payment processors, Toast's blended gross margin is pretty thin at around 21%. It is important to note that hardware and professional services have negative gross margins.

However, some margin expansion has been seen in 2023 (~23%) and is expected more in the coming years (up to 26%) due to the growing recurring part of the business, which carries much higher margins. For example, subscription services have a gross margin of approximately 77%.

Financial Snapshot

Based on Q3 2023, reported on November 7, 2023

Revenue

Actual:

2022 – $2.73 billion (+60.2% YoY)

Q3 2023 – $1.03 billion (+37.2% YoY)

Nine months of 2023 – $2.82 billion (+30.6% YoY)

Guidance:

The company tightened its 2023 financial outlook to $3.83-$3.86 billion, representing 40%-41% YoY revenue growth, versus a prior outlook of $3.81-$3.87 billion. For Q4 2023, the company now expects $1-$1.03 billion vs. prior guidance of $1.03 billion.

Estimates:

2023 – $3.84 billion (+40.9% YoY)

2024 – $4.84 billion (+25.8% YoY)

Operating Expenses

2022 – 32.85% of total revenue

Q3 2023 – 27.71% of total revenue

Operating expenses as a percentage of total revenue remained at the same rate (~30%) in the past three years. However, the company has yet to generate operating profit due to the high cost of revenues.

Stock-based compensation (SBC)

2022 – 8.35% of total revenue and 2.69% of the market cap

Nine months of 2023 – 7.28% of total revenue and 2.43% of the market cap

The company is on its way to exceeding SBC in 2023 compared to 2022, but management promised to constrain the shares issued soon.

Since going public, Toast has increased its shares outstanding by a moderate 8.14%, while its stock price has depreciated by over 75%.

Profitability

Toast became profitable on an adjusted EBITDA basis in Q2 2023 thanks to a greater revenue mix into software as well as growing economies of scale. The company has been increasing adjusted EBITDA by triple digits since then.

The company anticipates adjusted EBITDA in the range of $38 million to $48 million (up from $15 million to $35 million) in 2023.

SBC, alongside a high proportion of operating expenses vs gross profit, continues to drag down profitability.

Toast is currently forecasted to turn profitable on a GAAP basis in 2026, when the benefits of economies of scale start to play out.

Balance Sheet

As of Q3 2023, the company had $1.03 billion in cash, cash equivalents, and marketable securities, compared to $1.02 billion at the end of 2022. The company has just $32 million in debt on its balance sheet.

Cash Flow

Toast reached positive free cash flow (FCF) for the first time in its history in Q2 2023, the same quarter it turned profitable on an Adjusted EBITDA basis. Since then, the company generated $76 million in FCF. It is now expected to finish the year with $47 million in FCF and accelerate FCF growth from there.

Competitive Advantages

Toast operates in a highly competitive market, facing competition from both traditional POS systems (like NCR, Micros, and PAR) and other SaaS companies, including Posist, Clover, Foodics, as well as broader vendors like Shift4, Square, Lightspeed, and others that work with restaurants too.

However, Toast's focused approach on the restaurant industry gives it a unique edge. Legacy players like NCR, Micros, and PAR have been the traditional go-to solutions for POS systems, but their offerings are often not as specialized or integrated as Toast's, and Toast has been increasingly capturing market share from these legacy on-premise POS players. Toast also outgrew other vertical SaaS companies that offer solutions to restaurants.

The primary reason for this is Toast's differentiated offerings that are purposely built for restaurants in an all-in-one, integrated platform. This integration provides restaurant owners a comprehensive solution, reducing the need for multiple disparate systems. Toast is so much more than just a POS for restaurants, something that other competitors can't offer at this stage.

This is why Toast is aggressively investing in acquiring new customers and growing the usage among existing customers. The further Toast expands its platform, the further it embeds into a restaurant's ecosystem, making it quite hard for a restaurant to switch to another vendor. Switching costs increase incrementally with every new product an existing customer adds to its arsenal. Over time, this leads to increased revenue, both from subscriptions and payments.

And Toast has a proven track record and continued strategy to build products that not only directly address its customers' key pain points but also adapt to market needs, as evidenced by its willingness to explore and capture new market segments, like restaurant hotels.

Toast has been recognized as the top restaurant POS by G2.

Risks

Stay competitive in the evolving market, with companies like Square, with much deeper pockets and more extensive ecosystems, doubling down on the restaurant niche and already taking Toast's market share. Square is also offering much better payment processing services, for example, waiving any fees for the new restaurants for the first 12 months since joining the platform.

A significant deceleration in revenue growth starting in 2024. It could turn out to be even worse if a recession hits the US when a significant portion of existing customers could not only stop using Toast but go out of business entirely.

Profitability on a GAAP basis may not come in 2026 as forecasted right now, and the company will continue losing money for a much longer period while its market share will remain the same or stagnant.

Valuation is still a concern.

G2, which collects reviews from actual customers, ranks Toast below other solutions like Square, Clover, and Posist. While Toast offers the most comprehensive portfolio of offerings, it is certainly not the best solution on the market based on other criteria.

The primary revenue stream (payments) that generates over 80% of total revenue depends on third-party payment processors that can change the conditions at any time, leading to increased costs of goods sold (COGS) and decreased gross profit, further limiting the company's profitability.

The company's common stock's dual-class structure places significant control in several people's hands.

Additional Sources

Management / Board of Directors – https://pos.toasttab.com/leadership

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/1650164/000165016423000131/tost-20230424.htm#i879cb7f0bade441fb656fe524832d584_37 (page 60)

Have a great week!!!

~Jonah

You can follow me on Twitter [click here]

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.