Part 2: Deep dive on Super Micro Computer ($SMCI)

In order to read this deep dive on Super Micro (SMCI) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber, I appreciate your support.

Paid subscribers receive several deep dives per month plus they get full access to my investment portfolio (up +76% YTD) including my daily activity, my investment models and my daily webcasts.

Here are some of my other newsletters…

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus my daily commentary and morning newsletter.

Company: Super Micro Computer aka Supermicro

Ticker: (SMCI)

Website: SuperMicro.com

IPO date: March 29, 2017 (traditional IPO)

IPO price: $8.00

Stock price at the time of writing: $216.06

Outstanding shares: 52.5 million

52 week high: $265.00 on June 09, 2023

52 week low: $37.01 on July 05, 2022

ATH: $261.65 on June 07, 2023

Market cap: $11.343 billion

Net cash/debt: $155 million

Enterprise value: $11.188 billion

Headquarters: San Jose, California, United States

Number of employees: 4,600+

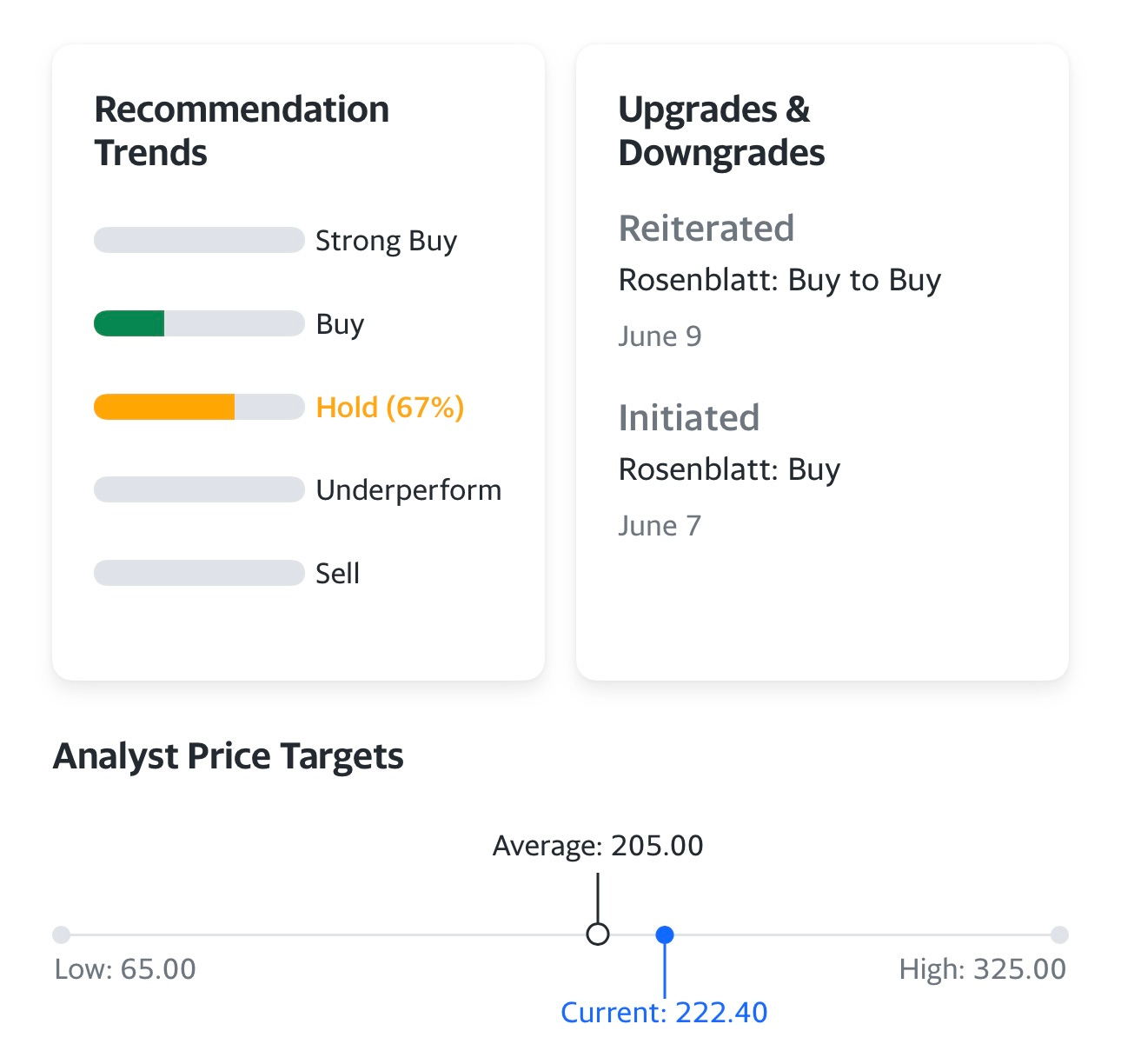

Average price target from analysts: $205.00 — 7.8% below current price

Next earnings call (Q4 FY 2023): N/A

Investor Relations [click here]

Q3 FY 2023 Earnings Report [click here]

Q3 FY 2023 Earnings Call Transcript [click here]

Q3 FY 2023 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1 and 2]

In case you missed part 1 of the SMCI deep dive…

Below the paywall is part 1 of the SMCI deep along along with links to my investment portfolio (up 76% YTD), investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

**These are new links, I have to switch them up at the beginning of every month so former subscribers don’t have access.

Disclosure: I added to my SMCI position several times this past week as the stock pulled back to the 21/23d ema, it’s now 2.5% of my portfolio which you’d already know if you followed my investment portfolio using the spreadsheet link above.

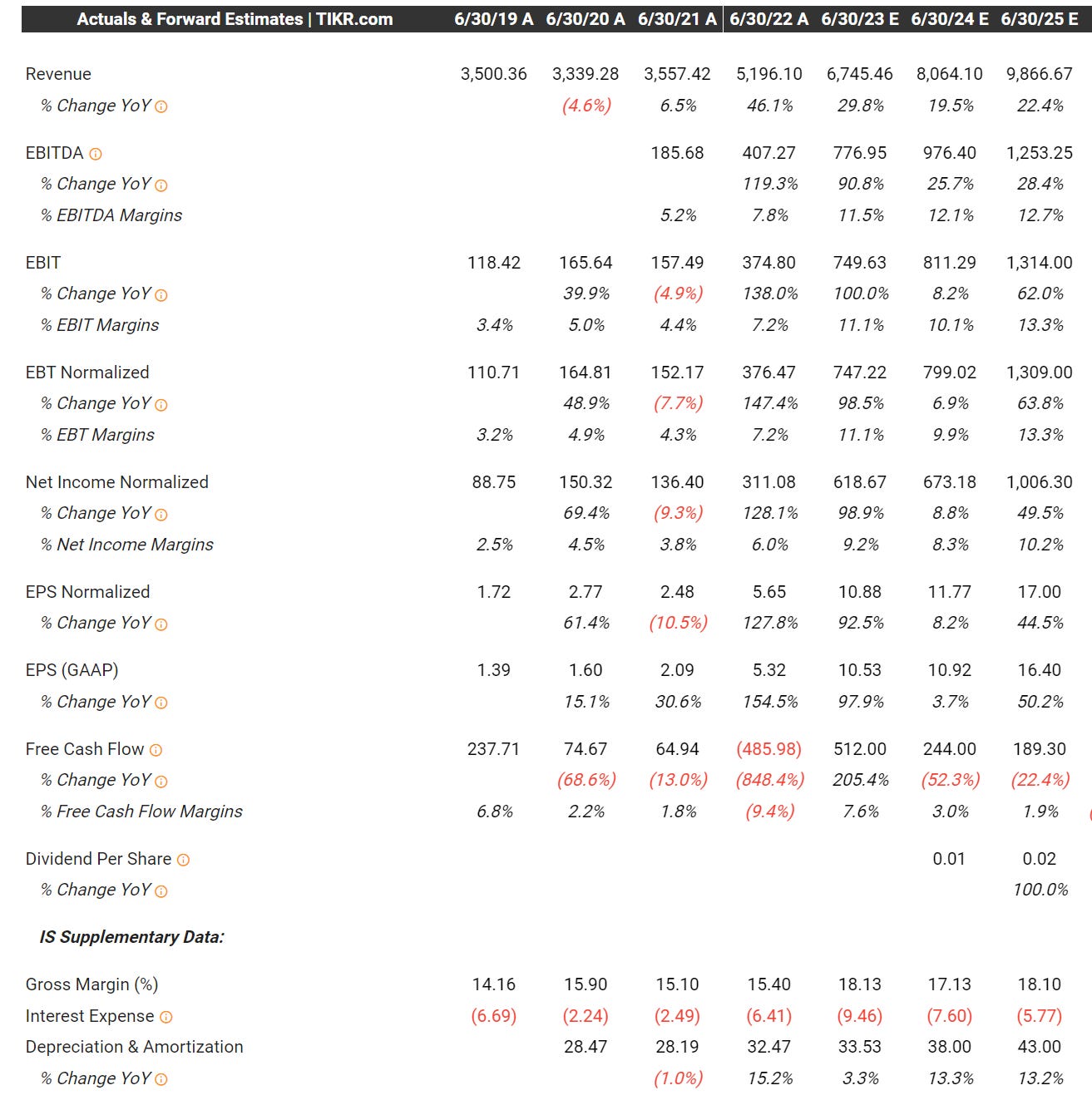

Valuation

As I mentioned in the introduction of part 1, the analysts are only giving us estimates through FY2025. Keep in mind that SMCI has already started their FY2024 which will end next June so I’ll be using FY2024 and FY2025 estimates in this exercise.

Using the estimates below and the current enterprise value of $11.2 billion it means that SMCI is trading at…

1.38x FY2024 EV/SALES

1.13x FY2025 EV/SALES

11.4x FY2024 EV/EBITDA

8.9x FY2025 EV/EBITDA

16.6x FY2204 EV/NET INCOME

11.1x FY2025 EV/NET INCOME

Even though SMCI is already up huge over the past 12 months, it’s still not an expensive stock, given the expected growth rates over the next 24+ months these are very reasonable multiples to pay for a company in a very strong industry with tremendous tailwinds around AI, ML and high-performance computing.

FWIW, here are the current 2024 and 2025 multiples for NVDA using the current $1,040 billion enterprise value…

24.3x FY2024 EV/SALES

19.8x FY2025 EV/SALES

55x FY2024 EV/EBITDA

44.1x FY2025 EV/EBITDA

54x FY2024 EV/NET INCOME

42.6x FY2025 EV/NET INCOME

Just to be fair, this is not an apple to apples comparison, NVDA is obviously a much stronger company and positioned very well for this AI-boom plus they have a better balance sheet and much better net income and free cash flow margins but it’s fun to compare. I love NVDA but I do think SMCI will be a better investment over the next 3-5 years because the valuation is much more reasonable.

I think NVDA and SMCI will have similar growth rates over the next few years but SMCI is trading at 11x FY2025 net income while NVDA is trading at 42x FY2025 net income, it will be much easier for SMCI to benefit from some multiple expansion over the next few years on top of the revenue and earnings growth — this is how SMCI can triple AGAIN over the next 4-5 years from current prices.

Investment Model

Like I’ve already mentioned, the analyst estimates only go out the next couple years through FY2025 so I had to come up with my own estimates which I think are very realistic. Based on my model/estimates, if SMCI grew revenues from $10.64B in FY2025 to $17.47B in FY2028 it would be an 18% CAGR for revenues, I think that’s very doable given how quickly their TAM is expected to increase which includes their proprietary cooling technology to make server racks more efficient and powerful which is what the data centers will be looking for.

In addition to 18% CAGR from FY2025 through FY2028, I’m also expecting SMCI to increase their net income margins by 0.5% per year from 10% in FY2025 to 11.5% in FY2028. I think this is possible because they’ll have pricing power given the demand for their superior products and the enhanced performance it can support.

Assuming SCMI can get to $15.2B of revenues in FY2027 with 11.0% net income margins, give them a very conservative 22 P/E, add back the cash and divide my 53.6M outstanding shares (assuming dilution stays at just 0.4% per year) and you have a $792 stock in just a few years. I know 266% upside from here seems impossible but not if they hit these numbers.

Even if they only do $13B of revenues in FY2027 with 10.0% net income margins, with a 20 P/E we’re still talking about a $550 stock which is 100% upside from here. FWIW, I don’t think NVDA or AMD have more than 100% upside over the next ~3 years, perhaps 4-6 years for both of them assuming AI lives up to the hype. NVDA needs to grow into their $1+ trillion valuation and AMD needs a product suite that can compete with NVDA.

Analysts

There’s currently 6 analysts that cover SMCI but as you can see they’re not super active with their ratings and price targets. No clue who the person at Wedbush is that covers SMCI but a sell rating and $65 price target with the current fundamentals makes me think that person should find a new job. They did run into some supply chain problems back in April and lowered Q3 revenue guidance by $200M but most investors & analysts believe that was just a short-term hiccup and doesn’t impact the long-term growth story for SMCI.

Just to keep the laughter going, a $65 PT would imply an enterprise value of approximately $3.2 billion which means the stock would be trading at 3x FY2025 EV/NET INCOME which is NEVER going to happen. That analysts from Wedbush is the Gordon Johnson of the semi/server industry :)

Here’s what the analysts are saying… unfortunately very few analyst notes to share from the past 3-6 months and two of them are from Loop Capital:

June 14th: Loop Capital analyst Ananda Baruah raised the firm's price target on Super Micro Computer to $325 from $200 and keeps a Buy rating on the shares. The firm's work suggests the Gen AI compute build has both legs and commercial commitment, with Gen AI going to 30%-40% of all Hyperscale applications from less than 5% today, the analyst tells investors in a research note. Loop Capital thinks Super Micro has at least a 12-24 month "attractive lead" on competition at their "Complexity At Scale" sweet spot.

June 6th: Rosenblatt analyst Hans Mosesmann initiated coverage of Super Micro Computer with a Buy rating and $300 price target. Super Micro's long history in "green" computing, building block architecture, plug-and-play, twin architecture, rack scale integration, and software platform optimization have "resulted in a formidable business model aligned with the critical factors for success in an AI driven world," the analyst tells investors. Supermicro's liquid cooling technology can increase rack compute power by over two times, which the firm calls "a disruptive dynamic in a power constrained data center."

May 24th: Loop Capital analyst Ananda Baruah raised the firm's price target on Super Micro Computer to $200 from $150 and keeps a Buy rating on the shares. The company's investment story continues to resonate with investors at a deepening level, and while the stock has appreciated "tremendously", investors will ultimately pay for a company of Super Micro's value-add, the analyst tells investors in a research note. The firm adds that AI is the stock's most recent and perhaps most prominent catalyst, but Super Micro's core value-add is deep server customization providing a differentiated impact for increasingly strategic applications, including AI / ML, Data Analytics, Strategic Video Streaming, etc.

April 24th: Wedbush analyst Matt Bryson made no change to the firm's Underperform rating or $65 price target on Super Micro Computer after the company updated its Q3 outlook. Super Micro pointed to component delays for the Q3 revenue shortfall, and the firm continues to have concerns around high expectations for both sales growth beyond FY23 and margins, the analyst tells investors in a research note. The firm says additional investment in AI at the enterprise/smaller cloud level could potentially mitigate some concerns around 1H24 estimates.

Technicals

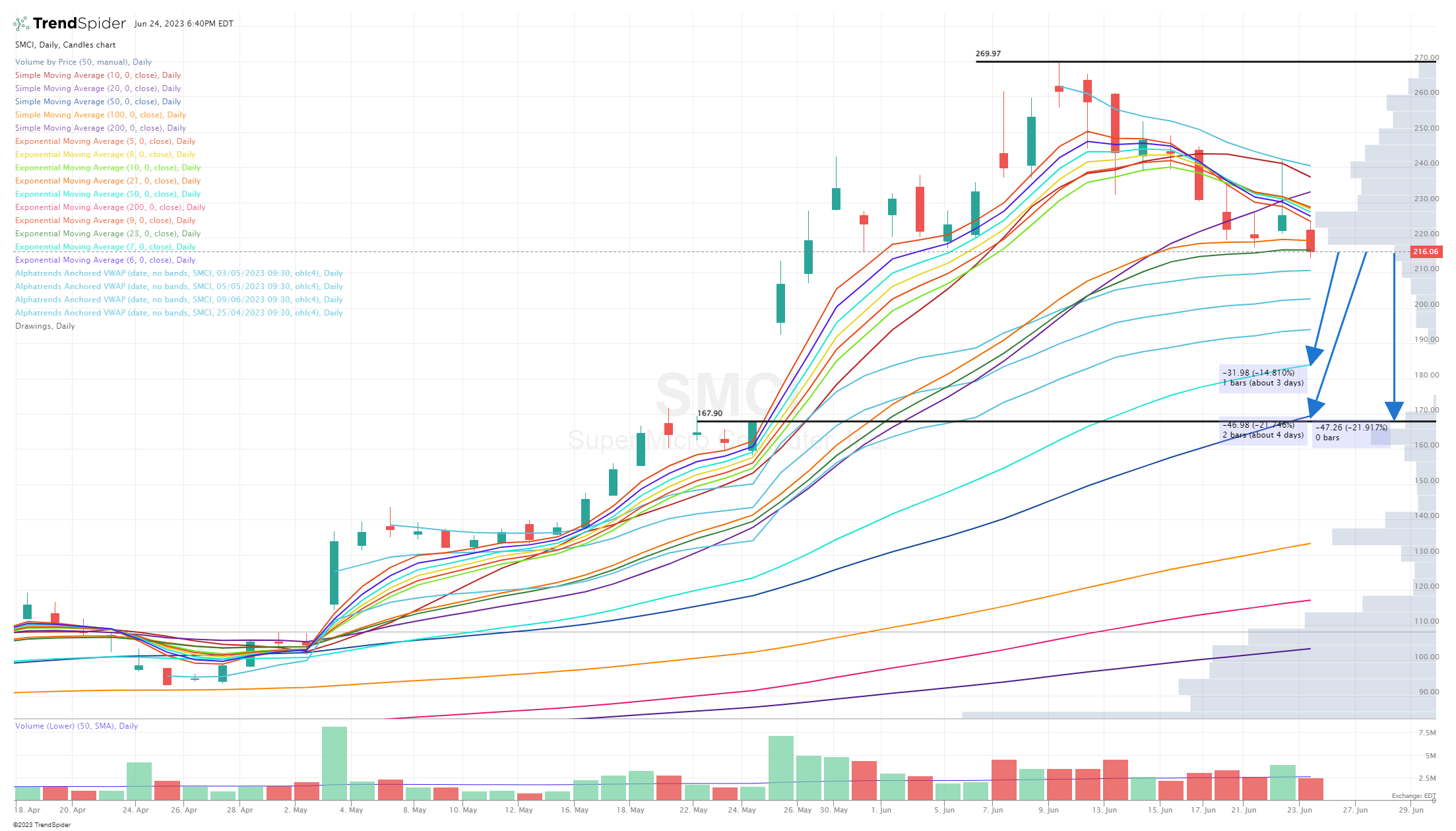

I already have a position in SMCI and since I think the stock has ~200% upside over the next 3-5 years I’m willing to be patient and add on pullbacks. SMCI closed this past week right at the 23d ema, I have no clue if it holds up. There are a bunch VWAPs below the current price but impossible to know which ones (if any) provide a bounce. If the 23d ema does not hold up it’s very possible that SMCI pulls back to the 50d ema at $184 (-14.8% lower). If that doesn’t hold up then we could test the 50d sma at $170 (-21.9% lower); at that point we might as well fill the gap down to $167.90

Currently my SMCI position is 2.5% but I’m willing to average down into the 50d ema/sma (if needed) in order to lower my cost basis while increasing my position to ~4%

Given the fundamentals and valuation, I’d be surprised if SMCI goes below the 50d sma, if that happens it means they missed on earnings and lowered full year guidance in which case the 100d sma at $133 could be a possibility. Not sure I’d be willing to hold in that case because a miss on earnings might change my investment thesis in which case I’d need to re-evaluate my conviction and strategy.

Conclusion

I know NVDA is a sexier story than SMCI and certainly has more momentum with big funds buying (lots of reasons to like NVDA) but the question is whether you can still make money in NVDA over the next 12-24 months or could SMCI be a better investment.

FWIW, here’s my investment model for NVDA which shows minimal upside over the next 3-5 years compared to SMCI. I also gave NVDA a premium P/E multiple (higher PEG ratio) compared to SMCI — if you give NVDA a P/E multiple closer to their net income growth rate the upside over the next 3-5 years is closer to 0% which would not get me too excited.

I’m definitely not an expert on SMCI (maybe someday), but I’m continuing to learn more about the company since it’s a newer position… after digging in these past few weeks I remain very bullish. I just wish I had done this work 12 months ago and started a position when this was a $50 stock versus a $200+ stock but investors can’t worry about where a stock has been, we need to focus on where it’s going which will be determined by their fundamentals so I’ll keep my SMCI position as long as they remain strong.

Additional Sources

Management – https://ir.supermicro.com/governance/executive-management/default.aspx

Board of Directors – https://ir.supermicro.com/governance/board-of-directors/default.aspx

Ownership – https://www.sec.gov/Archives/edgar/data/1375365/000137536523000024/proxystatement2022.htm#i63fcc62f6f5c4141932c1e4b8ee6e08c_76 (page 15)

As a reminder, you can track my investment portfolio, my daily activity and join my daily webcasts through this spreadsheet [click here]. Please let me know if you have any questions.

I’ll try to get part 2 out in the next couple days. Enjoy the rest of your week.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.