Part 2: Deep dive on Spotify ($SPOT)

In order to read this deep dive writeup on Spotify (SPOT) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber then I thank you for your support. Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +33% YTD), all of my daily activity, my investment models and my daily webcasts.

In addition to my newsletters and my podcast, I also run a Stocktwits room where I post about both of my portfolios/strategies plus you get my morning newsletter and my daily webcasts.

Company: Spotify

Ticker: (SPOT)

Website: Spotify.com

IPO date: April 3, 2018

IPO price: $165.90

Stock price at the time of writing: $133.76

Outstanding shares: 193.4 million shares

52 week high: $138.74 on April 19, 2022

52 week low: $69.29 on November 04, 2022

ATH: $364.59 on February 19, 2021

Market cap: $25.87 billion

Net cash/debt: +$1.751 billion

Enterprise value: $24.12 billion

Headquarters: Stockholm, Sweden

Number of employees: 8,300+

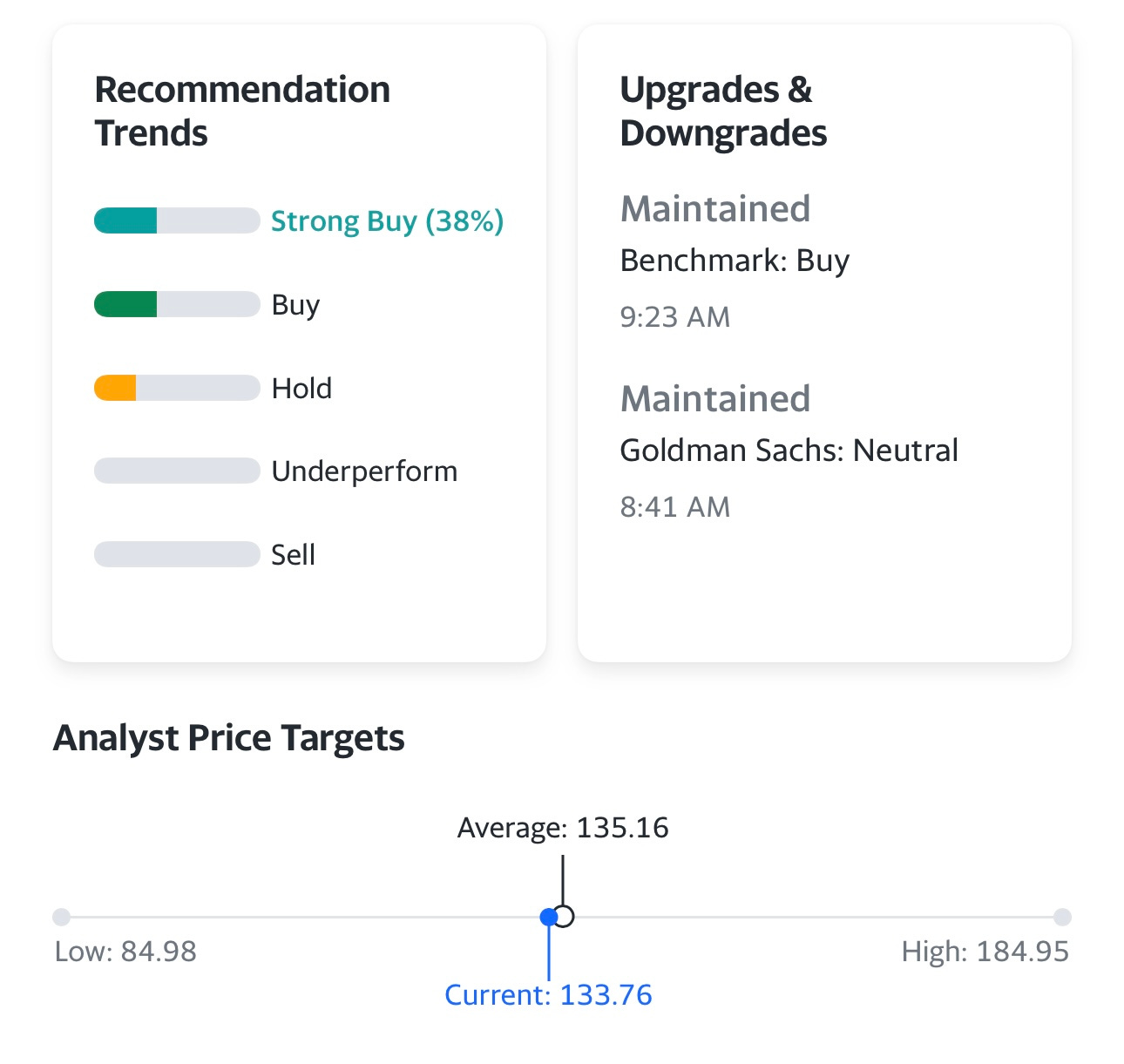

Average price target from analysts: $135.16 — 1% from current price

In case you missed part 1 of the Spotify writeup, you can read it here…

Next earnings report (Q1 2023): Tuesday, April 25th, 2023

Investor Relations [click here]

Q4 2022 Earnings Report [click here]

Q4 2022 Earnings Call Transcript [click here]

Q4 2022 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1 and part 2]

Just as a reminder I don’t currently have a position in SPOT and since they’re reporting earnings this week (Tuesday), it’s very unlikely that I start a position ahead of that report not to mention the stock is already up 93% since the October lows.

SPOT is no longer a high-growth company but they’ve built an incredible foundation and subscriber-base but now they need to show they can expand margins and increase profit/FCF margins.

There’s more than 30 analysts that cover SPOT so I doubt we’ll see any big surprises this week from earnings but then the analysts will tweak their estimates and price targets depending on the results.

SPOT would be so dominant right now if Apple, Amazon and YouTube weren’t competing against them, I’m guessing they’d have another 100+ million paid subs, perhaps at higher prices.

Apple Music launched in 2015, I wonder if they approached Spotify about potentially acquiring them, the company was private back then and had already raised a ton of VC money but I don’t know what the valuation would have been. I’m guessing they had conversations but no clue how far they went — I’m guessing SPOT was only willing to sell at a crazy high multiple which clearly isn’t Apple’s style considering that Beats was their biggest acquisition ever at just $3-4 billion.

As I mentioned in part 1 of this writeup, SPOT’s revenue growth will most likely continue to slow in the coming years (despite the CEO’s wild predictions about 2030 sub numbers & financials) so the only way this stock compounds for investors at greater than 15-20% per year is if the company can improve margins which means getting those gross margins to 28% or higher by 2027 which might give them a shot at 6-7% net income margins by 2027 but they’ll need to manage costs & headcount much better and more efficiently than they have the past few years. It still blows my mind that a company like SPOT has 7,500+ employees — I wonder what would happen if they did a 15% layoff? Would the company continue running as normal? Would user growth slow down? would new product launches/innovation not happen? The company did announce 6% workforce cut in January 2023 but I wonder if that’s the only one they do? I suspect the stock price bouncing 93% off the lows helps alleviate pressure in the c-suite however I believe many of these companies are still too bloated especially when you see headcount growth outpacing revenue revenue, that’s never a good thing. I’m never rooting for companies to do layoffs but sometimes it’s necessary after they over-hired for 2-3 years and now need to “right size” the operations.

Valuation

SPOT is a tricky one to value since they’re still losing money and looking at Price/Sales is useless because their margins suck. Price/Sales was more of a cloud/software metric where gross margins are 60-90%.

Once way to value SPOT on 2023 estimates is to look at FCF (free cash flow), expected to be $229.8M this year and $609.2M next year which would significant YoY growth and than another 87.% growth from 2024 to 2025.

If we focus on FCF and use $24.12B as the enterprise value, SPOT is trading at 104.9x 2023 EV/FCF (not cheap) but then if you look out over the next couple years (using estimates of course), SPOT is trading at 39.6x 2024 EV/FCF (much more reasonable) and 21.1x 2025 EV/FCF (pretty good).

I don’t care which 2023 numbers you look at, there’s no way to justify SPOT’s current valuation using 2023 numbers. If you buying SPOT at current prices ($130s) than you are looking 2-3 years out hoping they can put up $1B+ of FCF in 2025 and $1.5B+ of FCF in 2027. If they can do $1.5B of FCF in 2027, give them a 25x multiple and add in the cash you have a $40B company (EV) versus $24B today so that would be 67% upside over the next 4 years (decent but I think you can do better elsewhere).

Where the upside is greater than 100% over the next 4 years would be if they expand net income margins by 1.0% to 1.5% every year for the next 4 years and get to 4-5% in 2027 and maybe 6-7% in 2028. If revenues are still growing close to double digits in 4 years and NIMs are expanding by 1.5% per year the YoY net income growth will look really good so maybe the stock can trade at 40-50x earnings in 2027 on $1B of net income — if this scenario plays out than maybe you have 100% or more upside over the next 4 years but alot would have to go right and so far SPOT has not proven they can get to 6-7% NIMs in 2027. In order for me to own the stock I’d need to be relatively confident they can pull this off.

Investment Model

Once again, if you’re a long-term investor like many of us are it’s hard to value a company like SPOT on NTM (next twelve month) estimates so we need to look out a few years. As I’ve tried to do below, if SPOT can get to $24B+ of revenues in 2027 with 4.5% NIMs (net income margins), growing NI (net income) at 65% in 2027 and 45% the next year which would justify a 55x P/E multiple (I know it sounds high but it’s all about PEG ratios) than SPOT has a shot at $300+ per share in 2027 which would be 128% higher than the current price — I’d say there’s a 50% chance they can hit these numbers but it’s much harder to predict where multiples might be in 4 years even if fundamentals (ie earnings growth) are strong.

If I’m being honest I think SPOT investors will be unlikely to pay 55x earnings in 2027 because they know revenue growth is still slowing and margins can only expand so far which means in 2028 and beyond you’ll see much slower earnings growth in which case a more realistic multiple in 2027 might be 35-40x which would get the valuation to $40B on $1B of net income which is similar to the FCF scenario I presented in the last section.

Analysts

Just skimming the ratings below it looks like analysts are relatively split between buy/overweight and hold/neutral ratings which is fair considering how well SPOT has performed over the past 6 months. We did see a few analysts raise their price targets last week ahead of earnings, they probably realize that even if SPOT misses estimates it won’t be by much so the stock is unlikely to drop more than 5-10% so they’d rather have their price targets closer to the current price. '

Please don’t put much thought into these ratings or price targets because if you look at where they were in late 2021, most of these analysts had price targets above $300+ and we know how well that worked out :)

What the analysts have been saying:

April 21st: Benchmark raised the firm's price target on Spotify to $150 from $140 and keeps a Buy rating on the shares ahead of the company's report due on April 25. The firm, which expects progression of Podcast profitability to be materially accretive to Spotify's terminal value, from nearly zero or "perhaps negative" today, it says, adding that FY23 and FY24 consensus expectations continue to understate both Premium and Ad-supported gross margin leverage.

April 21st: Morgan Stanley analyst Benjamin Swinburne raised the firm's price target on Spotify to $160 from $130 and keeps an Overweight rating on the shares. Gross margins should begin to expand year-over-year in Q2 and "medium-term" guidance of 10%-plus EBIT margins are not reflected in consensus or valuation, the analyst tells investors. Upward earnings revisions should support continued appreciation for Spotify shares, the analyst argues in a preview note for the streaming music and audio group.

April 19th: Truist analyst Matthew Thornton raised the firm's price target on Spotify to $154 from $132 and keeps a Buy rating on the shares ahead of its Q1 results. Despite the strong start to the year, the stock can continue to work while the service is at a discount to peers, with the added prospect of the company taking price later this year, the analyst tells investors in a research note. A TikTok ban could also serve as a sentiment catalyst, Truist added.

April 19th: KeyBanc analyst Justin Patterson raised the firm's price target on Spotify to $160 from $140 and keeps an Overweight rating on the shares. KeyBanc's latest U.S. Audio Survey showed Spotify experiencing gains in paid penetration and usage in a backdrop where paid audio penetration is largely stagnant. The firm believes this reinforces Spotify's recent momentum, and positions the company to benefit from pricing, ad and marketplace monetization, and cost controls.

March 22nd: As previously reported, Guggenheim analyst Michael Morris upgraded Spotify to Buy from Neutral with a price target of $155, up from $120, citing the view that the global music industry has the potential for "market-leading financial growth" over the next several years. Music is "intrinsically valuable to consumers" and with a decade-long period of largely promotional pricing ending for on-demand streaming music, the firm sees an attractive revenue growth runway for the industry that will exceed current consensus estimates, the analyst tells investors.

March 10th: BofA analyst Jessica Reif Ehrlich raised the firm's price target on Spotify to $143 from $120 and keeps a Buy rating on the shares after the company shared new developments in the platform's creator ecosystem in its "Stream On" event. Following a "strong" Q4, the firm said it remains "bullish" on Spotify and raised its terminal growth rate to 9% from 7% to reflect improving growth prospects.

March 1st: Redburn analyst Nick Delfas upgraded Spotify to Buy from Neutral with a new fair value estimate of $140 per share. The firm forecast gross margins of 26.7% in 2023 and 30.4% in 2026, which are each higher than consensus, supported by waning headwinds from investments, publishing royalty increases and marketplace growth. Reburn also said it expects a "sharp slowdown" in hiring and marketing cost cuts along with a scaling of other costs and expects subscribers from emerging markets to offset slowing growth from developed markets.

Technicals

This first chart shows SPOT on the weekly going back to the IPO, you can see how well it did from April 2020 until the summer of 2021 but then it was in free fall mode from $387 down to $69 for a drop of 82%. SPOT is still below the VWAP from the IPO and it’s coming up against a big volume shelf, both of which could be resistance.

This chart below is my favorite of the three because it shows SPOT is on the verge of a potential downtrend line (DTL) breakout from the all time high (ATH). If we do see a breakout this week (mostly likely from earnings if it happens) than I’d consider a position in my trading portfolio with the DTL as my stop loss meaning once it breaks out it needs to stay above the DTL otherwise my stop loss would get triggered and I’d be out of the position.

As I’ve mentioned several times, SPOT is already up 93% from those October/November lows so I don’t think you need to chase here. If you’re looking to trade the stock than you can buy it on a pullback/bounce off 21/23d ema or 50d ema/sma or a breakout and close on decent volume above $137. There’s also the DTL breakout that you can buy if it happens but if you’re trading this name make sure you’re managing your risk. No reason to take a big loss on SPOT after a big run. The time to be aggressive with this name was 6 months ago, not now on the way into Q1 earnings. As a long term investor I’d be more interested in SPOT if it pulled back to the 200d sma however if that happens it means the fundamentals are getting worse or the overall markets are getting hammered, I’d probably prefer the latter because if the fundamentals are not panning out than I don’t want to buy it on a pullback because it means the upside potential just got worse, not better.

Conclusion

Just to recap, SPOT is on the verge of a DTL breakout, if it happens than I might start a position in my trading portfolio but I don’t think I’ll be adding SPOT to my LT investment portfolio anytime soon because I just don’t see enough upside over the next 3-4 years compared to some of my other positions. However, if the CEO of SPOT comes out and says they’re doing some major cost cutting/layoffs and he thinks they can get NIMs to 10% or higher by 2027 than my investment thesis changes and I’d be way more interested in owning the stock. SPOT is similar to companies like CPNG (Coupang) which I did a deep dive writeup on earlier this year — growth is slowing at these companies but they’ve built an amazing moat and customer base however now the story pivots away from growth and over to “margins and profits” which is still a “show me story” in most of these cases since investors aren’t ready to believe them yet.

SPOT might be the classic example of a great product but not a great stock, mostly because monetization has been hard and the company doesn’t seem to have much pricing power compared to companies like NFLX but I’m not sure if that’s because they’re more focused on “more subs at less margin per sub” or are they worried if they raise prices than it opens the door for Apple, Amazon and YouTube to steal some customers? I’d love to hear what everyone else thinks about this.

Additional Sources

Management [click here]

Board of Directors [click here]

Ownership, page 78 [click here]

Key Business Metrics, page 46 [click here]

Hope you enjoyed this writeup. I’m planning to do 1-2 webcasts every quarter where I discuss some of the quarterly results so I’m sure I’ll have the opportunity to share my thoughts on the SPOT Q1 earnings report in the next month or so.

Have a great week!!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.