Part 1: Deep dive on Spotify ($SPOT)

In order to read this deep dive writeup on Spotify (SPOT) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber then I thank you for your support. Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +33% YTD), all of my daily activity, my investment models and my daily webcasts.

In addition to my newsletters and my podcast, I also run a Stocktwits room where I post about both of my portfolios/strategies plus you get my morning newsletter and my daily webcasts.

Company: Spotify

Ticker: (SPOT)

Website: Spotify.com

IPO date: April 3, 2018

IPO price: $165.90

Stock price at the time of writing: $133.76

Outstanding shares: 193.4 million shares

52 week high: $138.74 on April 19, 2022

52 week low: $69.29 on November 04, 2022

ATH: $364.59 on February 19, 2021

Market cap: $25.87 billion

Net cash/debt: +$1.751 billion

Enterprise value: $24.12 billion

Headquarters: Stockholm, Sweden

Number of employees: 8,300+

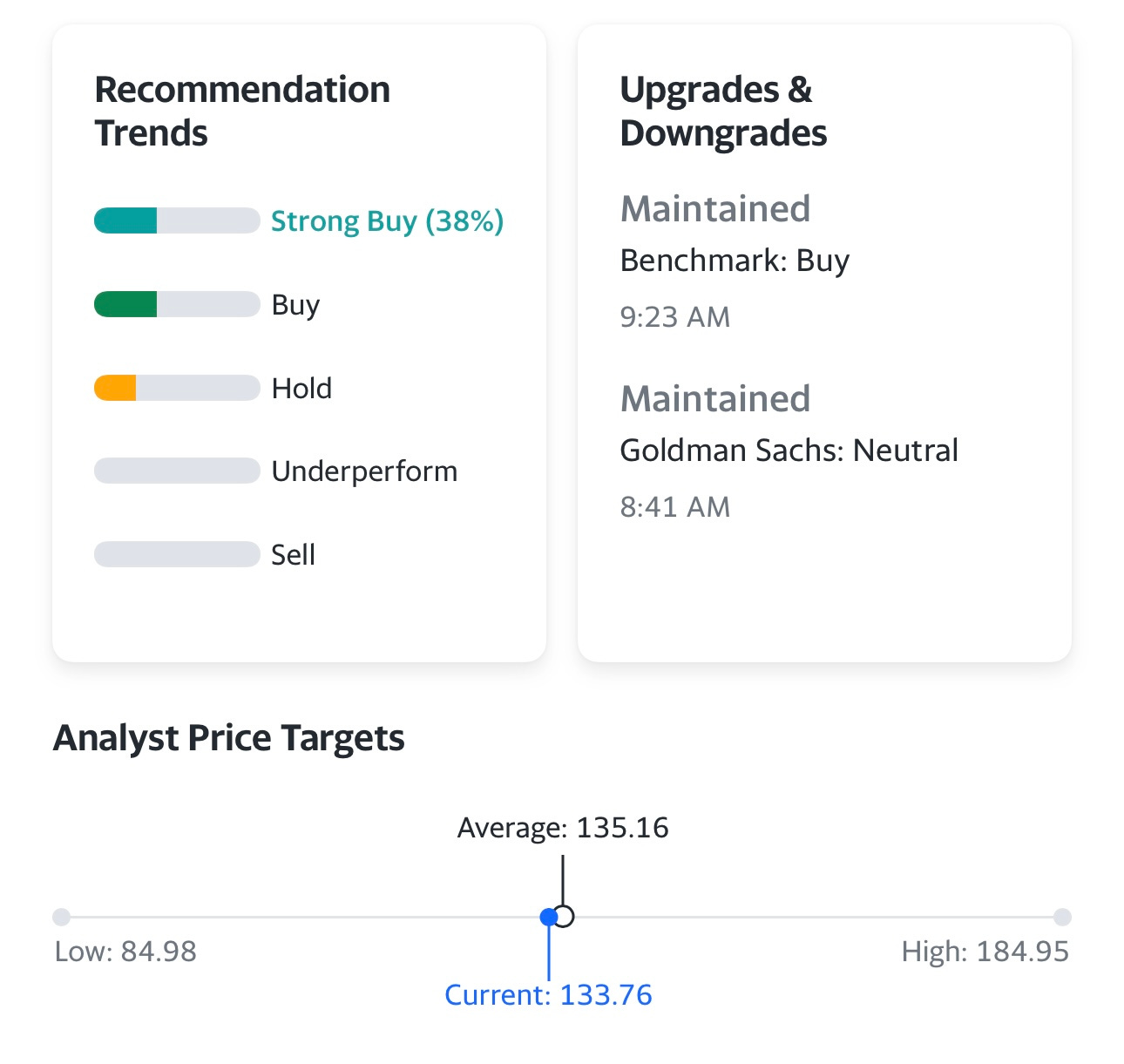

Average price target from analysts: $135.16 — 1% from current price

Next earnings report (Q1 2023): Tuesday, April 25th, 2023

Investor Relations [click here]

Q4 2022 Earnings Report [click here]

Q4 2022 Earnings Call Transcript [click here]

Q4 2022 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1 and part 2]

Introduction

Disclosure: I do not currently have a position in SPOT. I did own the stock in my trading portfolio earlier this year but already closed out the position. I don’t think I’ve ever owned SPOT in my investment portfolio.

Even though I’ve never owned SPOT in my long-term investment portfolio it’s still a stock/company that I watch closely because I’d consider owning it someday but also because I’m a huge fan/user of their products. I’m guessing 99% of the people that read this writeup will be familiar with SPOT and most of their products but hopefully we can help you better understand their business model and whether it might be a stock that can make us money over the next 3-4 years. SPOT literally has hundreds of millions of users so the real question lies in their ability to monetize the free users, bring in more advertising partners, expand podcasting, develop their own audio content and ultimately expand margins while generating significant free cash flow.

I’d say that SPOT has proven they can scale into an enormous streaming platform for music & audio but we still don’t know if they can actually make money or is their business model flawed with razor thin margins and a bloated cost structure.

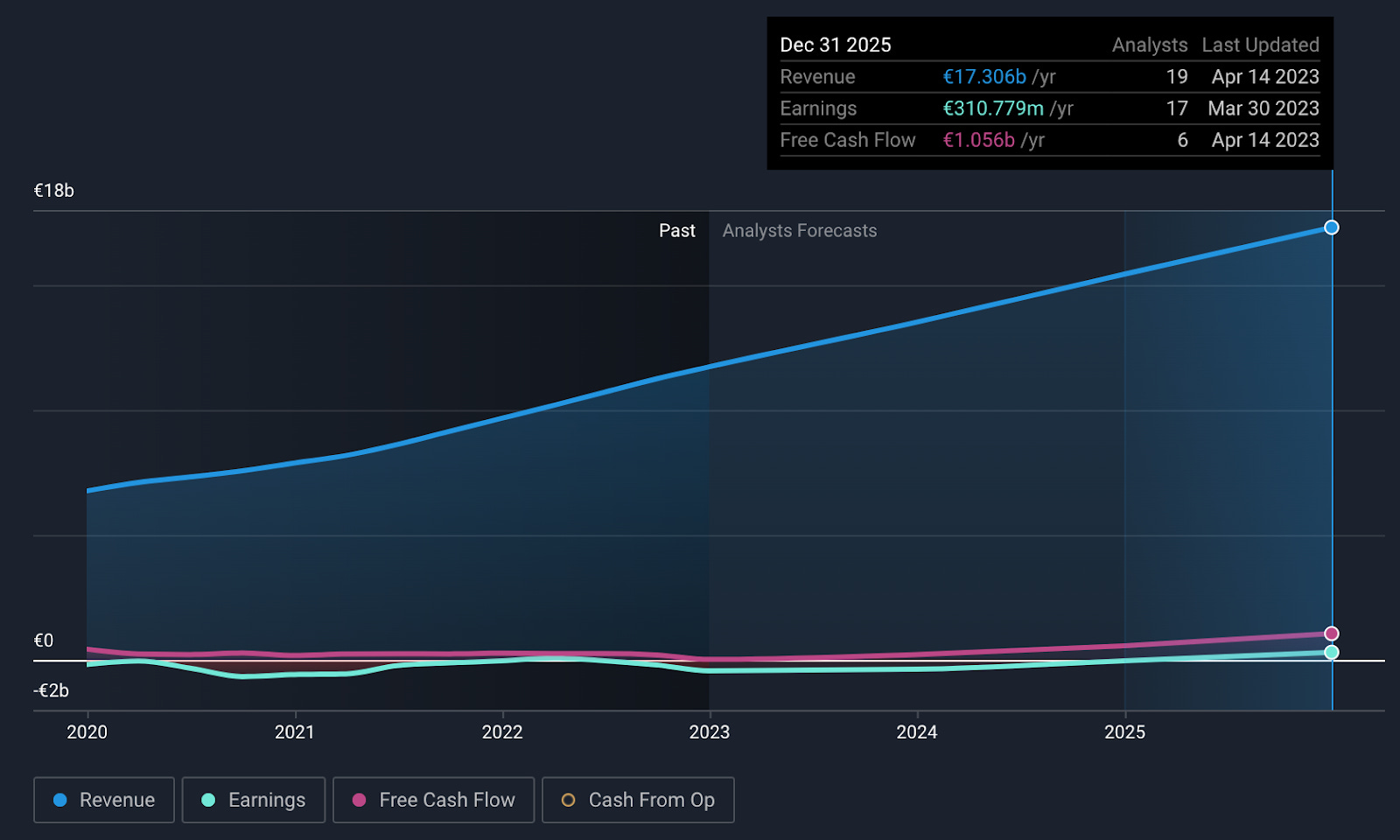

As you can see from the analyst estimates (above), growth is slowing and there could be some margin improvement over the next few years but I need to see more in order to justify a position. SPOT is still down 65% from the all time high however it’s already bounced 93% off the November lows so I need to see better growth, better operating margins and better earnings/profits before I’m ready to own this stock. This is where we need to separate a great product/service from a great company/stock. Kudos to anyone that bought SPOT back in November in the $70s but those estimates above don’t justify the stock in the $130s unless you are solely focused on FCF which can be misleading at times. For a $20+ billion company these are some really mixed financials so you can look at the earnings section and probably build a great “bear case” or look at the free cash flow section and build a decent “bull case”.

FWIW, FCF doesn’t include SBC (stock based comp) which clocked in at $381M which is still on the higher side for a $20B company but there are plenty of smaller companies that give out way more stock to employees ie COIN and DKNG.

Even though I think it’s possible SPOT turns into a solid investment for the next 3-4 years, the most interesting thing about SPOT right now are the technicals and as you can see from the chart below the stock is right up against the downtrend line (DTL) from the ATH (all time high). Even though I’m not super bullish on SPOT at the current prices I’d consider a position in my trading portfolio if we get a DTL breakout HOWEVER please keep in mind that SPOT reports earnings next week so this might be a good time to do your research and then after earnings you can decide if this is a stock you want in your portfolio. I’m planning to do the same. Given the recent runup from the $70s to the $130s over the past 6 months I don’t think you need to be chasing SPOT into earnings, nothing wrong with being patient and waiting for the next pullback plus there’s still an unfilled gap down to $102.43 — and even though not all gaps have to fill, many of them do.

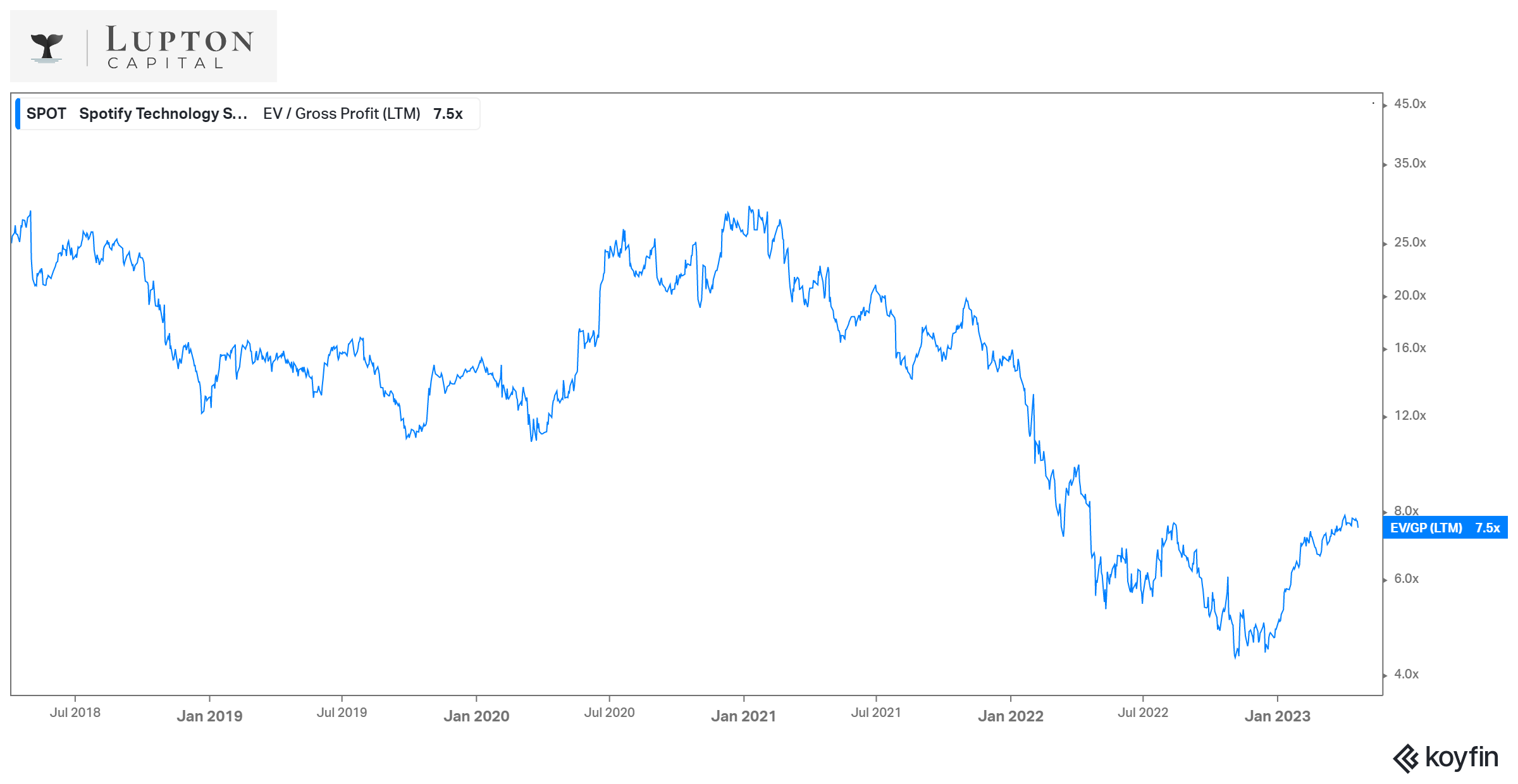

Even though the fundamentals are hardly breathtaking, the valuation seems somewhat reasonable, trading at 7.5x EV/GP (LTM) but we’re not going to see any multiple expansion without margin expansion and I don’t know if SPOT can pull it off without doing some major layoffs and other cost cutting, similar to what META has done over the past 6 months. It’s not apples to apples but META did have their metaverse capex spending (which was out of control) whereas SPOT has their content & podcast strategy which has also proven to be very expensive considering the talent they were bringing in and the amount of money they were throwing around — so far I don’t think it’s paid off and the company appears to be pulling back on some of the reckless spending.

Based on my investment model [click here], I think there’s the potential for SPOT to double from here over the next 3-4 years but that’s based on revenues getting to $24+ billion in 2027 with 4.5% net income margins and then a 55x P/E multiple which sounds high but it would be reasonable if earnings were growing at 65% in 2027 and expected to grow at 45% the following year (2028).

Personally I think SPOT is one of the most valuable subscriptions I have for the money, I probably use it 3-4 hours per day and I’m still only paying $9.99 per month. I’d gladly pay at least $14.99 per month and I’m guessing most current paying subs feel the same way. NFLX has been able to increase their prices multiple times over the past few years with very little churn so I wonder if SPOT would consider a similar strategy.

I think increasing prices by $1 per month for the next 5 years would be very fair and I doubt they’d lose many paying subs.

If you’re a shareholder you should want the company to start increasing prices — this is part of my investment thesis and would make it easier for them to hit my margin targets over the next few years or possibly surpass them. If SPOT announced tomorrow they were planning to raise prices by $1 per month for 2023 (to $10.99) with a goal of getting to $14.99 or $15.999 by 2027 then I’d be more likely to own the stock because it would show they are serious about making money for shareholders.

The CEO of SPOT is on the record as saying he thinks the company can hit $100B of revenues someday with 1+ billion paying subscribers, I think he even mentioned 2030 for these goals which seems a overly ambitious. I’d be more likely to believe these goals were achievable if Spotify wasn’t competing against Apple Music and Amazon Music. If SPOT had a total monopoly over streaming music than I do think 1 billion paid subs by 2030 would be possible. FWIW, they finished 2022 with 205M paying subs which means they’d need to grow their paid subs by 22% per year for the next 8 years to reach 1 billion paying subs by 2030 which seems very unlikely however if by some miracle they pull that off than the stock has enormous upside from here, perhaps 4-5x over the next 7-8 years but this is not something I can endorse yet, it’s just the CEO’s pipe dream for now.

One of the reasons I use SPOT so much is that I sometimes prefer listening to music during the day when I’m writing or going through charts, versus listening to CNBC or Bloomberg — just depends on my mood and the time of day but I’ve also gotten into music as both a DJ (just for fun) and a music producer (I’m still a newbie) but because of these two new hobbies I use Spotify for inspiration and discovery.

Someday I hope to have my own music on Spotify and the other music services like Tidal, Soundcloud, Beatport, Apple Music and so on. As a DJ, I use Beatport the most for finding/downloading music which I then sync up to Rekordbox which is the software that analyzes the songs for my Pioneer DJ controller (XDJ-RX3).

Hope you enjoy this writeup, let me know if you have any questions. Part 2 should be out in the next couple days, I just need to finish up a couple more sections.

Company Background

Spotify was founded back in 2006 by two Swedes, Daniel Ek (who remains a CEO and owns approximately 16.5% of the company and 31.7% of total voting power) and Martin Lorentzon (who sits on the board of directors and owns 11.1% of the company and 42.6% of total voting power) with the goal to create an ad-based music streaming service with the ease of iTunes and the massive music library of Napster but legal.

Back then, music was mainly distributed physically through CDs. The move to online was just getting started, and music was primarily available on piracy and file-sharing sites like Napster. Then came iTunes with buying (for $2/piece) and owning songs, which evolved as a standard for music distribution for several years before Spotify entirely disrupted the traditional music ownership model, both offline (CDs) and online (digital downloads).

The Swedes duo transformed the music industry forever by allowing users to move from a “transaction-based” experience of buying and owning music to an “access-based” model, which allows users to stream music on demand on multiple devices, including smartphones, desktops, cars, game consoles, and in-home devices.

Spotify was first launched as a desktop app in late 2009 – beginning of 2010. It was a pilot version available to users in the United Kingdom only. The initial interest was so high that the company had to switch to registration by invite only within the first few months since the launch.

The launch of Spotify was met with some resistance from the major record labels, who were skeptical about the potential of music streaming. It took about three years for Ek and Lorentzon to negotiate the rights to stream music from major labels in the US while proving that music streaming is the future.

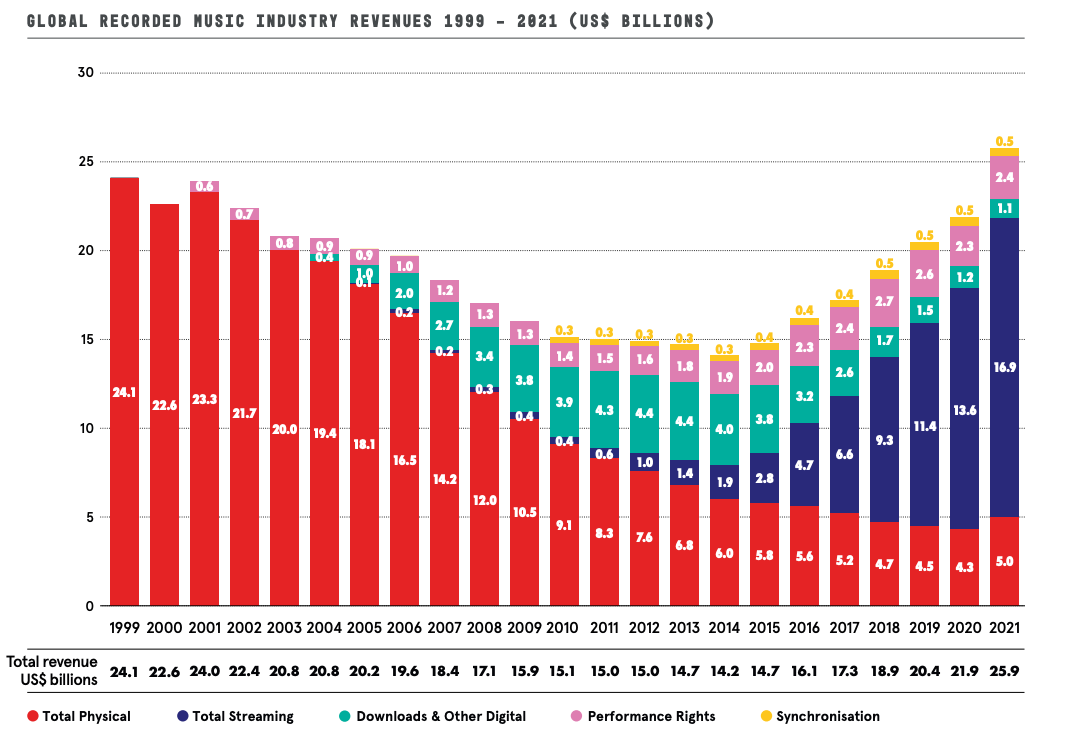

Music streaming was just a $600 million global industry when Spotify launched in the US in 2011, while physical album sales and downloads totaled $14.4 billion that year. Today, streaming accounts for 65% of the music industry's revenues, and according to various industry experts, this share will only grow further.

Spotify went public in 2018 via a direct listing, an untraditional way of listing shares, through which the company didn't raise any additional capital by issuing new shares and instead allowed existing shareholders to sell their stakes in the open market. The stock opened at $165.90 on April 3, 2018, already higher than the “reference price” of $132 provided by Morgan Stanley, and despite 90% of all shares ending up trading immediately, it closed at $149.01 per share.

Since its IPO, Spotify has strengthened its market leadership, growing users exponentially. It was the first streaming platform to surpass 200 million paid subscribers (205 million as of Q4 2022 compared to the closest rival, Apple Music, which had 88 million at the end of 2022), while almost half a billion users from 184 countries are listening to Spotify on a monthly basis.

The company's mission also transformed from changing the way people consume music to unlocking the potential of human creativity by giving a million creative artists the opportunity to live off their art and billions of fans the opportunity to enjoy and be inspired by it.

Spotify today is more than just a music app. It became an audio streaming service with discovery features. Every day, millions of users turn to Spotify for audio entertainment, which they would never find on their own. And Spotify does a fantastic job helping people discover new music and podcast shows through various playlists and charts that are based on personal preferences and past history.

Spotify has also built various tools and analytics for creators to help them better understand their fans, support themselves, and effectively monetize their creative work, essentially becoming a two-sided marketplace for listeners and creators.

But it is still a money-losing business (the company never had an annual profit, losing $460 million in 2022 alone), and the stock has been down significantly in the past several years, going down from the all-time high of $364.59 in February 2021 to below an IPO price, where it currently trades.

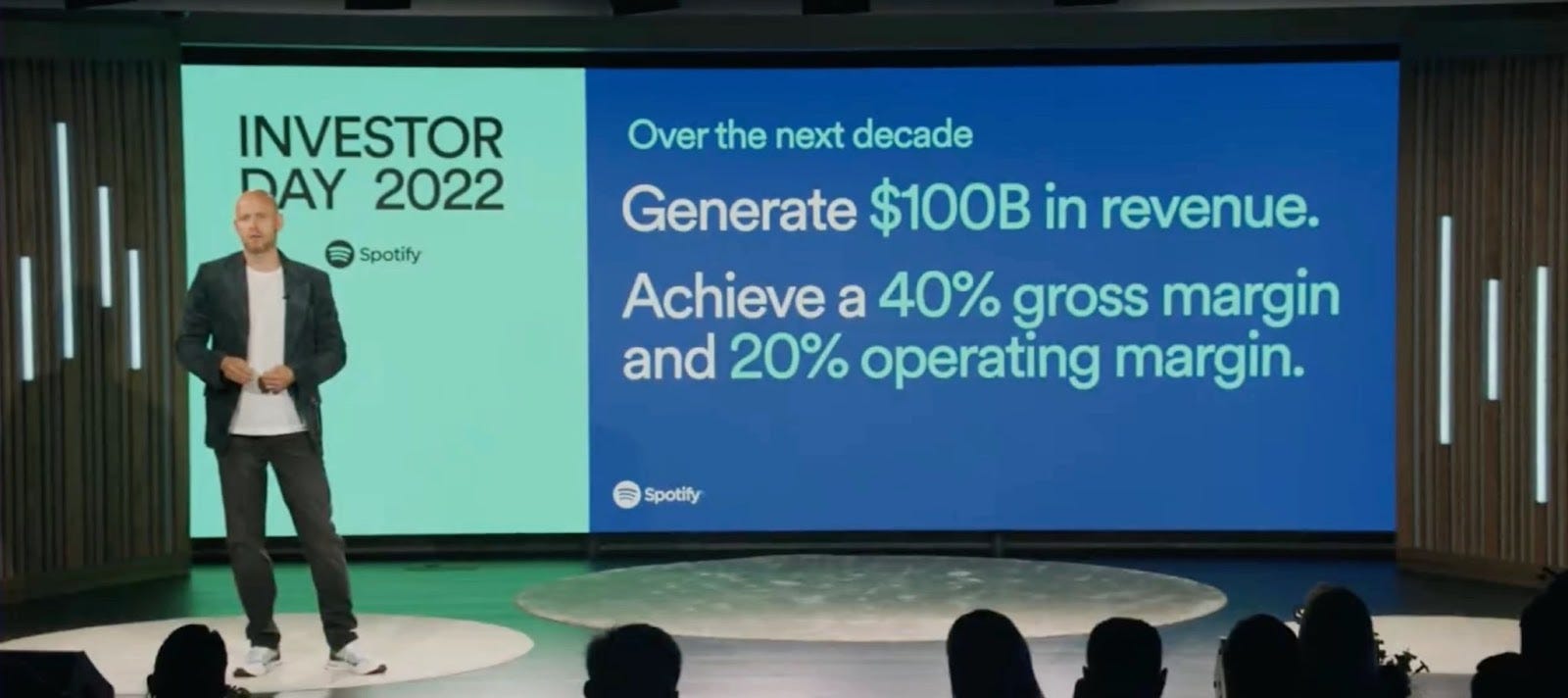

Nevertheless, CEO Daniel Ek has high ambitions that he set on Spotify's Investor Day back in June 2022: he sees the company not only reaching $100 billion in revenue ($12.55 billion in revenue in 2022) and 1+ billion in subscribers (205 million paid subscribers as of 2022) by 2030 but also becoming the go-to destination for all digital sound, including music, podcasts, audiobooks, news, live talk, storytelling, and education.

“Everyone underestimates audio. It should be a multi-hundred-billion-dollar industry.” – Daniel Ek.

2022 was a critical year for Spotify on its way to accomplishing this ambitious goal. The company made a lot of investments in its business and set 2023 as a new chapter in its history where it begins to improve profitability.

“We aren’t profitable yet because we keep investing. I focus on cash flow. It’s positive, and we’re not dependent on investors to fund us. We want to keep growing because there is such a big prize at the end of the tunnel.” – Daniel Ek.

Management has established a new organizational structure that streamlines decision-making and prioritizes speed and efficiency. The goal, going forward, is to move away from sharing revenues with record labels and publishers (which eat most of the gross margin) and become a producer of its own content. Spotify has everything to become Netflix but in audio.

Opportunity

Trends

After experiencing a period of over a decade during which the music industry faced a decline due to a shift from physical sales to streaming, the industry reached a significant turning point in 2015, where it witnessed a substantial increase in digital growth.

Since then, the global recorded music industry has continued to thrive and expand every year, with an 18% growth in 2021. Streaming accounted for 65% of almost $26 billion of total revenue (or $16.9 billion).

This trend will accelerate in the coming years, with expected continuous growth in all major markets, especially in emerging ones, where penetration of smartphones and high-speed, low-cost broadband is growing, and more and more people are discovering music streaming.

For example, only about 0.5% of India's total population was estimated to be paid subscribers in 2021. People there are on the stage where they are only getting used to music streaming services and ready to consume them for free. But as the market matures (users become more dependent on music streaming), more people will be happy to pay for such services.

Offering a more diverse content selection (podcasts, audiobooks, news, etc.) will only help accelerate the growth of streaming services, leading to a more enriching experience and higher user engagement.

The second trend is the move of audio advertising online. In the US alone, advertisers spend about $30 billion each year on audio ads, which mostly go to radio. Radio remains extremely popular, with an estimated 3 billion daily listeners (in the US). Globally, the numbers are even more impressive. It is estimated that the overall global audio advertising market is $100+ billion, and it will significantly shift online in the coming years.

Total Addressable Market (TAM)

Spotify's management estimates that the audio market presents a $350+ billion opportunity, which includes music, live events, podcasts, audiobooks, news, sports, and education.

As of 2022, the company only targeted three of these market opportunities (music, podcasts, and, most recently, audiobooks), generating $12.55 billion in revenues (only 3.5% of the total opportunity). All current market opportunities are projected to grow immensely in the coming years.

According to Grand View Research, the global music streaming market (~$34 billion in 2022) will grow at a 14.7% CAGR and reach over $100 billion in revenues by 2030.

The global podcasting market will see even more significant expansion, growing from $18.5 billion in 2022 to over $130 billion in 2030, a whopping 27.6% CAGR.

The global audiobooks market will see a similar CAGR of ~26%, growing from $5.36 billion in 2022 to $35 billion by 2030.

In Spotify's June event, Daniel Ek teased more acquisitions that will help the company enter new categories/verticals in the near future.

"What our successes in music and podcasting has clearly demonstrated is that we've built a powerful machine and solid infrastructure that enables us to go after new verticals, and we're not waiting around." – Daniel Ek.

Growth Drivers

Spotify is already the world's most popular audio streaming subscription service, with a community of 489 million MAUs (monthly active users), including 205 million Premium Subscribers, across 184 countries.

The app keeps growing in all four of the company's major regions. Europe, the largest region, grew to 148 million MAUs, accounting for 30% of the total MAUs, while the North American region accounts for 21% of total MAUs. The two fastest-growing regions, Latin America and the rest of the world, account for 21% and 28% of total MAUs, respectively. The latter region saw tremendous growth in 2022, increasing 50% YoY.

Users are increasingly using Spotify. Combined, all users streamed 132 billion hours of content in 2022, an increase of 20% compared to 2021.

But there is still so much room for growth. The company is actively developing new products and introducing initiatives, constantly looking for new ways to monetize its large and growing audience.

Premium Subscribers

About 42% of total MAUs are paid subscribers, leaving plenty of opportunity for the company to convert free listeners to paid subscribers, especially in the more developed markets.

Historically, when the company has seen growth in free users, it has also seen growth in paid subscribers with a 9 to 18 months lag. Spotify added a record high of 83 million MAUs in 2022 that would start to convert into paid subscribers later in 2023 and early 2024.

Furthermore, the company can increase the price for a premium subscription, as many other companies like Netflix and Amazon have done in recent years. An increase of just $1 will add an additional $2.4 billion in revenue annually.

Podcasts

Spotify turned to podcasts in late 2019 – early 2020, when the podcast market was just starting off. The pandemic has dramatically accelerated the growth of this segment, as well as the company's investments in it. Spotify became the first company to commit $1 billion to podcasting when the entire industry was valued at less than this amount.

“We realized everything we built for music could be adapted to podcasts. And the reason why we've been so successful is because we've been able to upsell people who never listened to podcasts before to start listening on Spotify, and that is what got us to the #1 position in podcasting.” – Daniel Ek.

In the past several years, the company made many acquisitions of both content and tools, allowing it to expand and scale the podcast monetization and product offering for advertisers and publishers.

In 2019, Spotify acquired one of the largest then podcast networks Gimlet Media for $194 million, a true-crime studio Parcast for $55 million, and Bill Simmons’ sports and culture network, the Ringer, for $190 million. In 2021, Spotify signed massive exclusive deals with Alex Cooper (Call Her Daddy) and Joe Rogan (Joe Rogan Experience) for $60 million and $100 million, respectively, that differentiate its services, attract incremental users, and enhance engagement. Next came partnerships with A-listers, including Barack and Michelle Obama (the exclusive deal expired in 2022), Prince Harry and Meghan Markle, Kim Kardashian, and filmmaker Ava DuVernay.

For tools, Spotify acquired Anchor, which makes software for recording shows, for $154 million, and Megaphone, a content distribution and ad network, for $236 million. The company also saw some additional but smaller deals.

Podcasts play a critical role in the company's goal of building an ecosystem where people engage not only with music but also with podcasts, making them more engaged, spending more time in the app, having more incentives to come back, and eventually paying for the service or listening to ads, though Spotify serves ads even to those who have a premium subscription.

In 2023 and beyond, podcasts will start to deliver ROI for Spotify as it will put more monetization of its podcast business. The company not only expects the podcast segment to continue growing at a rapid pace but also to turn profitable in the next 12 to 24 months, helping Spotify to lift its gross margins.

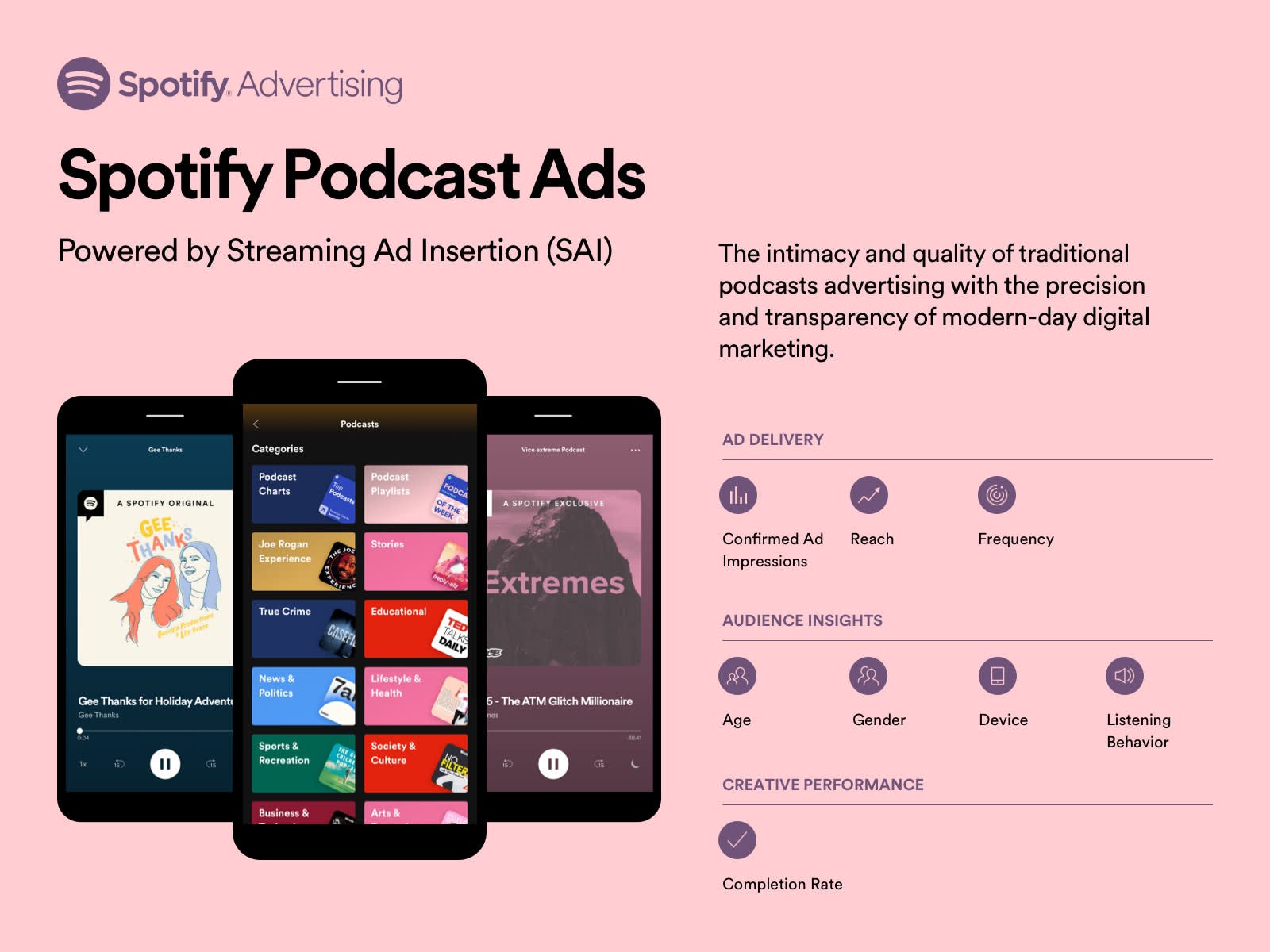

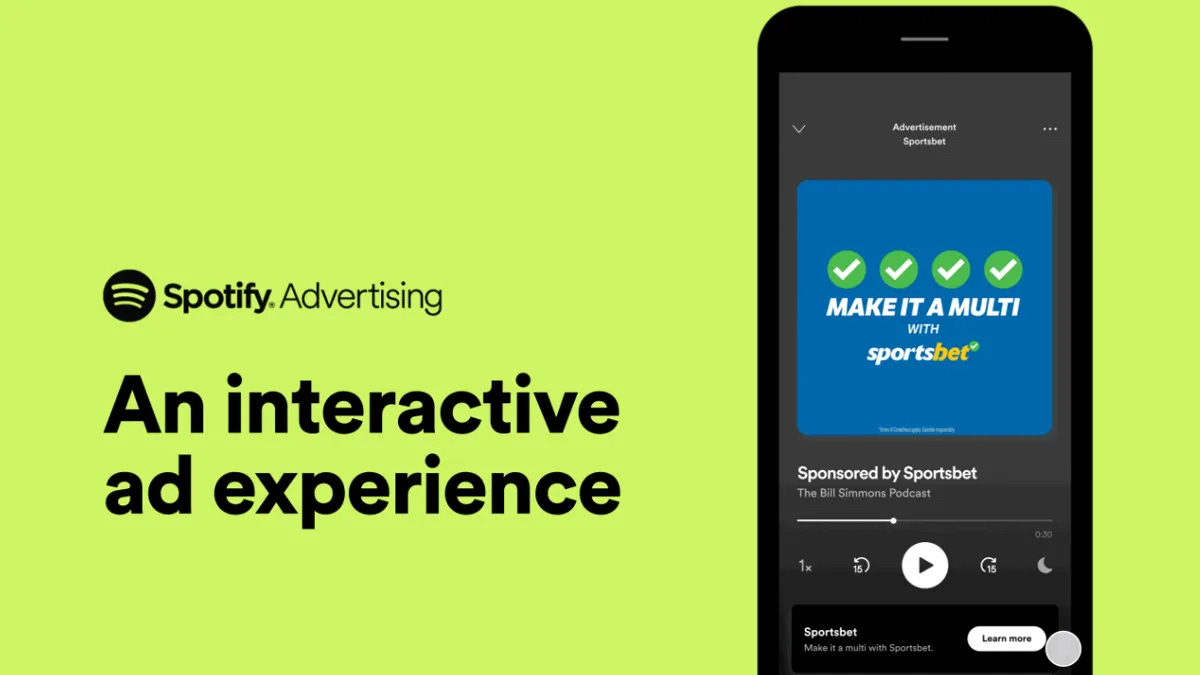

Advertising

Spotify's ad-supported business saw a slowdown in 2022 due to the microenvironment and various associated headwinds. But in the second part of 2023, the advertising business should see a turnaround.

Spotify has been preparing for this return for the entire of 2022, not only by growing the number of users and engagement that creates more opportunities for advertisers but also by introducing new advertising products across both music and podcast content.

Offering advertisers additional ways to purchase advertising on an automated basis is a key way that Spotify expands its portfolio of advertising products and enhances advertising revenue.

In 2021, the company introduced the Spotify Audience Network (SPAN), an audio advertising marketplace that connects advertisers to listeners across Spotify's owned and exclusive podcasts, podcasts from enterprise publishers via Megaphone, and podcasts from emerging creators via Anchor. Through SPAN, the company provides hosting and ad-insertion capabilities for audio publishers that allow it to sell targeted advertising to brand partners that enables them to reach listeners both on and off the Spotify platform.

A large percentage of ad-supported users are between 18 and 34 years old, a highly sought-after demographic that has traditionally been difficult for advertisers to reach. Spotify has a wide range of data points (not only age but also listening habits, location, and device). It provides advertisers with better ad-targeting features, making advertising on Spotify more effective, eventually leading to higher ARPU.

The US still dominates the advertising business for Spotify, but the company is heavily investing in international growth, especially in Europe. Monetizing via ads in Latin America and in the rest of the world will be more difficult for the company, but it still presents opportunities worth pursuing.

As audio ads shift online, more prominent brands from different industries (retail, consumer packaged goods, automotive, etc.) will start investing heavily in podcast ads, and Spotify will be at the forefront of this trend.

Audiobooks

In June 2022, Spotify acquired Findaway, a digital audiobook distribution platform, to enable the audiobook offering, creating a tremendous cross-selling opportunity for the company.

Later that year, Spotify launched the first iteration audiobook listening experience in select markets (the US, the United Kingdom, Ireland, Australia, and New Zealand), allowing users to access more than 300,000 audiobooks alongside a massive catalog of music and podcasts.

This new format should help expand Spotify's user base into a new category of potential listeners and connect diverse creators to new and existing fans.

Audiobooks are still a small segment of a global $140 billion book market, representing just 7% of it. As the audiobook market continues to expand, Spotify sees it as another multi-billion opportunity.

“And so our belief when you look at the audiobooks market is that while books is a pretty big industry, audiobooks is still a niche offering only enjoyed by tens of millions of consumers around the world. And if you think about that from first principles, it's pretty clear that audiobooks should be something that should be enjoyed by hundreds of millions of people, if not billions of people, around the world. So to grow that market is absolutely key for us.” – Spotify's management.

The best part of the audiobook business, and precisely why Spotify is interested in it, is its gross margins of around 40%.

Just three years ago, Apple Podcasts dominated the podcasts market, but now Spotify is the number one podcast app in most of the world. Audiobooks are currently dominated by Audible (Amazon), but a similar story could happen here. The secret sauce is Spotify's better UI and ecosystem (all audio in one place).

Marketplace

The two-sided Marketplace is one of many nascent opportunities for Spotify. First introduced back in 2019, it offers tools for creators to promote their content to people who already listen to them or have similar tastes. The company recently added more options that will let creators charge for exclusive content, early access, and interactive experiences.

The Marketplace was a huge success for the company in 2022, contributing over $200 million. It plays a critical role because Spotify gets royalty relief from three major record labels in exchange for using marketing tools to promote certain artists, which in turn helps the company increase its music gross margins (Spotify does not include the Marketplace contributions in revenue).

The Marketplace currently is a $2 billion opportunity, which should increase in the coming years as in-app marketing will be more adopted by not only three leading labels but also by much smaller ones.

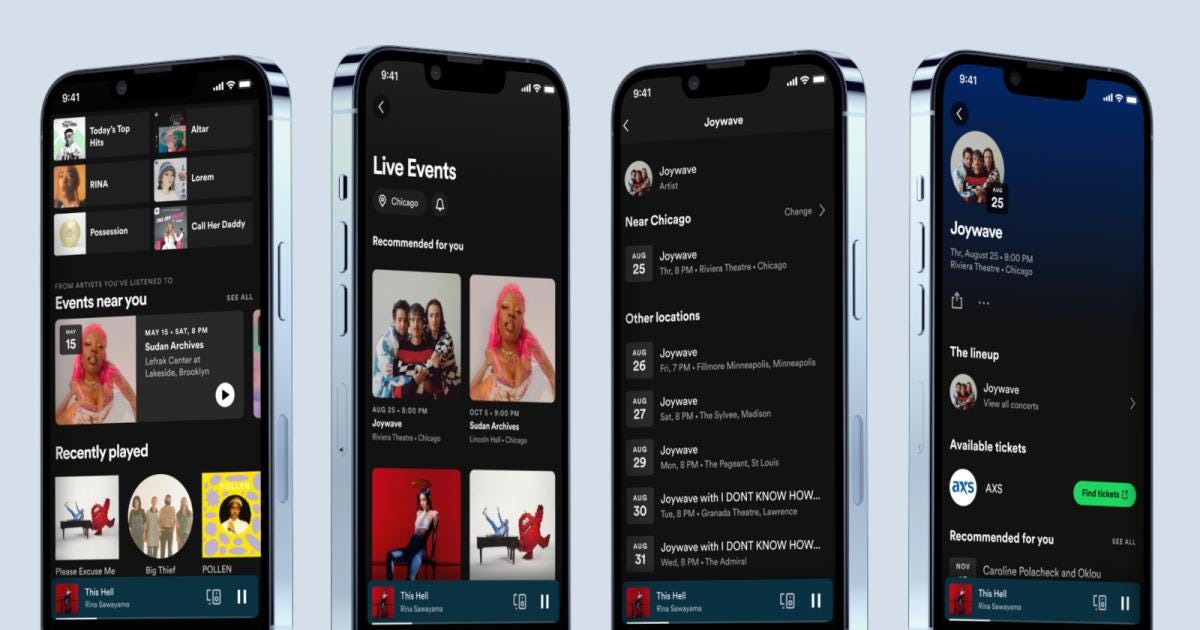

Live Events

Live events like concerts are vital to every creator (a cornerstone of most artists’ income) and the broader music industry. The live music market is estimated to be over $35 billion by 2030.

Spotify has just recently revamped its Concerts section. Live Events Feed helps fans find their favorite creators’ live events. Users also can discover all the live events in their local area, personalized to them.

The company sources these listings from ticketing partners (that pay a commission to Spotify for every purchased ticket) like Ticketmaster, AXS, DICE, Eventbrite, and See Tickets. Spotify now has most of the world’s concerts listed on its platform in the major markets.

“The artists have been thrilled with the presales we’ve had and our ability to target and sell tickets to their super fans and get that audience engaged very quickly. What we’ve also seen is when people buy tickets through Spotify, they actually then tend to listen to more music of that artists on Spotify as well.” – Spotify's management.

Long-term Investments

Spotify is not available in China due to regulations. Instead, the company formed a joint venture with Tencent to develop QQ Music, which is now one of the three largest Chinese music streaming services.

Spotify owns shares in Tencent Music Entertainment Group. During 2022, the market value of its investment increased by €242 million from €852 million as of 2021 to €1.09 billion as of 2022 due to the increase in TME’s share price.

Business Model

Spotify operates a freemium model, where users can access the service for free but with some limitations, such as advertising interruptions (every 3-4 songs) and the ability to listen to only shuffled songs on playlists.

This ad-supported service serves as a funnel that continuously drives new users to Spotify, a large portion of which later convert to premium (paid) subscribers.

This approach proved to be very successful for the company and allowed it to achieve scale with attractive unit economics. Management believes that an ad-supported service can work as a viable stand-alone product that can generate significant revenue over time.

Revenue Streams

So Spotify monetizes its service through subscriptions (Premium service) and advertising (Ad-supported service). Subscriptions represented almost 90% of total revenue in 2022.

Premium

Premium provides users unlimited access (without commercial breaks) to a high-quality catalog of music and podcasts, which are available both online and offline. Audiobooks are not included in the premium subscription; users can purchase them on an á la carte basis.

The company generates revenue from selling various premium subscriptions: Standard Plan ($9.99 / month), Duo Plan ($12.99 / month), Family Plan ($15.99 / month), and Student Plan ($4.99 / month).

Plans will vary from country to country. For example, in India, there is a Mini Plan, which includes only one account available on the mobile device, and it is limited to 30 offline songs.

The price for premium plans also significantly varies depending on the market to align with consumer purchasing power, general cost levels, and willingness to pay for an audio service.

There are some markets where recurring subscription services are less common. Spotify offers prepaid options for durations other than monthly (the Mini Plan in India starts from 7 days).

The premium plans are also sold through partners, who are generally telecommunications companies that bundle the subscription with their own services. For example, Vodafone UK includes Spotify Premium for the entire duration of the contract (12 to 24 months).

New Premium users are primarily sourced from the conversion of the Ad-Supported users. As of 2022, Spotify had 205 million Premium users in 184 countries (compared to 180 million in 2021).

Additionally, Premium users are converted from special trial programs that Spotify continuously runs. These trial campaigns typically offer certain features of the Premium plan for free or at a discounted price for a certain period of time (for example, the first 3 months are free).

Ad-Supported service

Ad-supported service is free of any subscription fees. It is a robust option for users who are unable or unwilling to pay a monthly subscription fee but still want to enjoy access to a wide variety of high-quality audio content.

Spotify monetizes such users by selling display, audio, and video advertising delivered through advertising impressions (on a cost-per-thousand basis) across the music and podcast content.

The company generally enters into agreements with advertising agencies that purchase advertising on behalf of their clients, and sometimes Spotify works with large advertisers directly. The company also works with certain advertising automated exchanges, internal self-serve, and advertising marketplace platforms to distribute advertising inventory for purchase on a cost-per-thousand basis.

Advertising revenue is recognized based on the number of impressions delivered. Ad-supported revenue grew 22% YoY in 2022 and accounted for 12.5% of total revenue.

Gross Margins

Licensing is a large part of Spotify’s business model. To stream content to users, the company needs to obtain intellectual property rights to this content by getting necessary licenses from rights holders. Spotify then pays them royalties or other considerations depending on the agreement.

Spotify has license agreements with the three largest music companies (Universal Music Group, Sony Music Entertainment, and Warner Music Group, which own rights to almost 90% of all the music streamed on Spotify). These license agreements have a multi-year duration, are not automatically renewable (renegotiated every couple of years), and apply worldwide.

Spotify also has direct license agreements with hundreds of independent labels and companies known as “aggregators” (CDBaby, Distrokid, and TuneCore). The majority of these agreements have a multi-year duration, are generally automatically renewable, and apply worldwide.

Some agreements (typically with the three largest record labels that have monopolistic rights) require Spotify to pay minimum guaranteed payments, including marketing commitments, advertising inventory, financial and data reporting obligations, and numerous prescriptions about how the Spotify service operates.

Royalties are typically calculated monthly based on the combination of several different variables, like the number of subscriptions and advertising to the proportion of total streams.

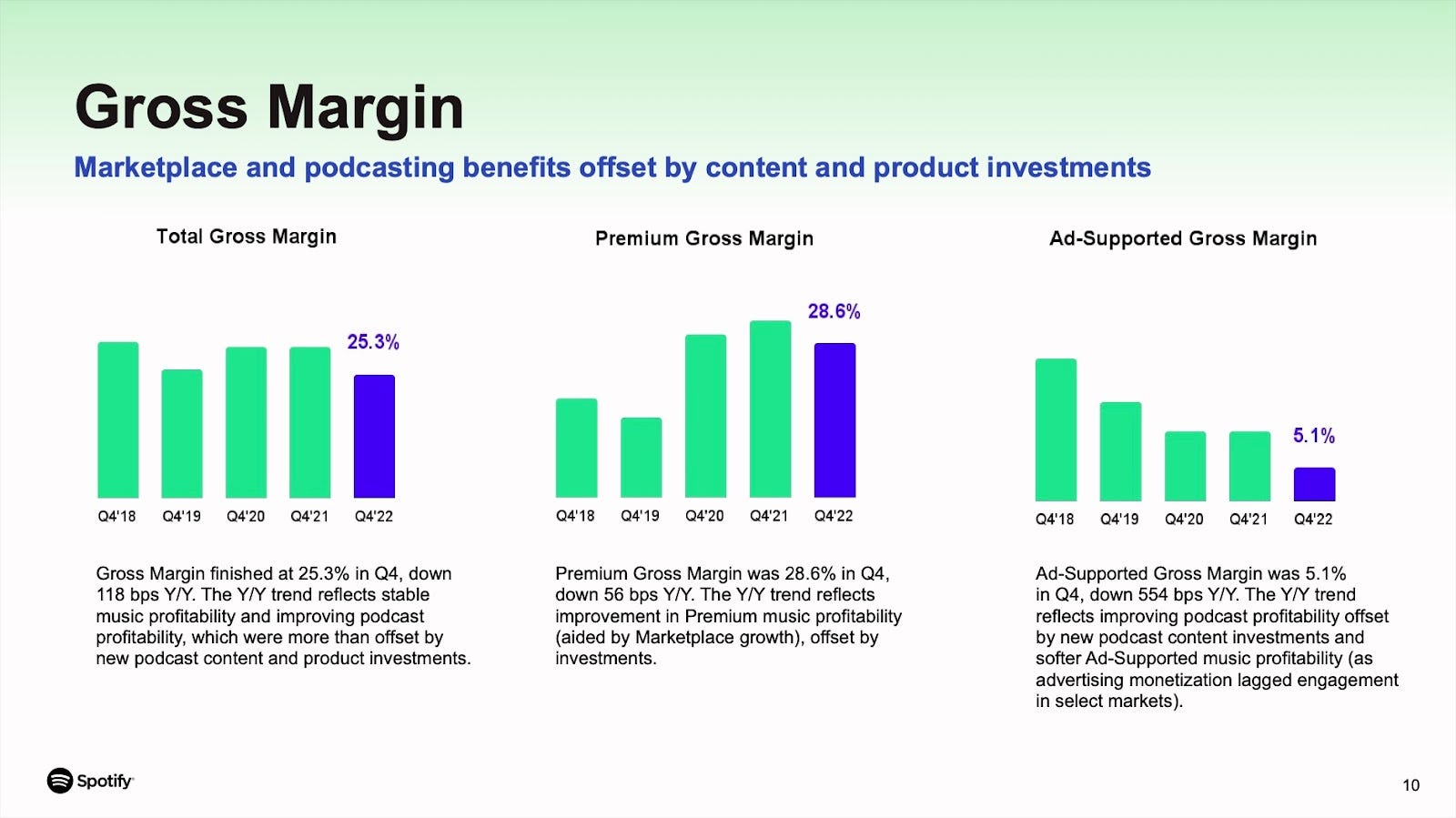

Music streaming has always been a low-margin business. Spotify pays approximately 70% of its revenue to rights holders (~55-60% to record labels that then pay out artists and ~15% to composers). It leaves Spotify with approximately a 25% gross margin.

However, management expects to increase the overall gross margin significantly in the coming years and even reach the 40% range through a combination of different factors: the introduction of new products with higher margins, a mix shift to podcasts (podcasts margins could reach 40%-50% thanks to an extensive and growing portfolio of original content), higher advertising rates, improved music gross margin by increasing the use of the Marketplace.

The latter has already been in play: the music gross margins recently increased from 25% to 28% as a result of the increased usage of marketplace tools by major record labels in exchange for royalty relief. Management expects to increase music gross margins to 35% in the next three to five years.

Profitability

Spotify continues to be unprofitable, delivering $460 million in a net loss in 2022 after a pretty positive 2021 when a net loss shrunk from a whopping $709 million in 2020 to just $38.7 million.

The company recently announced layoffs and hiring slowdowns in 2023. Management also promised to have more discipline in spending on personnel, including stock-based compensation. The company is undergoing a number of optimizations that should help reach profitability.

All analysts who currently cover Spotify do not expect the company to become profitable at least until 2025.

The two positive news are: first, Spotify has a solid balance sheet with cash and cash equivalents (€2.48 billion), restricted cash, and short-term investments of €3.4 billion in total (vs. €1.12 billion 0% exchangeable notes debt due 2026); and second, the company will continue to generate plenty of free cash flow (it averaged over €200 million of positive Free Cash Flow on a trailing 12-month basis for the past three years, and on a cumulative basis, generated over €1.3 billion of Free Cash Flow since the first quarter of 2016).

The further success of Spotify will depend on how quickly the company will be able to increase its overall gross margins and how disciplined it will be in its spending. Currently, too little gross profit is left from selling the services, and the operating costs to run this business are too high. But Spotify has everything to turn around its business and finally become a profitable company, something that all investors are patiently waiting to happen for many years.

Competitive Advantages

Competition

Despite being the world's number one music streaming and podcasts app (though its market dominance has been shrinking from approximately 34% in 2019 to 30%-32% in 2022, depending on the source), Spotify faces intense and increasing competition in all segments where it operates.

In the music segment, Spotify competes with:

digital music streaming providers, such as Apple Music (one of the main competitors with 88 million paid subscribers as of 2022), YouTube Music, Amazon Music, Deezer, Joox, Pandora, and SoundCloud (the other large competitor with approximately 130 million MAUs);

online or offline providers of on-demand music, which may be purchased, downloaded, owned, or available for free, such as iTunes audio files, MP3s, or CDs;

internet radio, such as Pandora;

terrestrial radio (which is still widely popular all around the world);

satellite radio, such as SiriusXM and iHeartRadio;

In the podcasts segment, Spotify competes with:

podcast streaming providers, such as Apple Podcasts, Google Podcasts (including YouTube), Audible, Facebook, Pandora, Deezer, and TuneIn;

podcast creation and hosting platforms, including SoundCloud and other smaller new entrants such as Acast, Buzzsprout, Podbean, and Libsyn;

In the audiobooks segment, Spotify competes with:

audiobook content providers, such as Amazon’s Audible, Apple Books, Google Audiobooks, Librivox, Kobo Audiobooks, Downpour, Storytel, and BookBeat;

Spotify also indirectly competes with live talk audio content providers, such as Twitter, Clubhouse, Discord, Meta (including Facebook and Instagram), and ByteDance (including TikTok and Resso).

With all these companies, Spotify competes for users, user listening time and advertisers.

For advertising specifically, Spotify competes with companies that offer advertising inventory and opportunities, including extensive online advertising platforms and networks such as Google, Apple, Amazon, AppNexus, Criteo, and Meta (including Facebook and Instagram).

Competitive Advantages

Spotify's long-term market leadership is guarded by several strong competitive advantages the company built throughout the last decade.

Ecosystem

Spotify is building an ecosystem of all audio content. Unlike other companies like Apple, Amazon, or Google, Spotify does it in one app.

Music, podcasts, now audiobooks, and soon other content are available from a beautifully designed app, which is accessible on literally any device, from smartphones and tablets to TVs and cars, both iOS and Android.

App

Spotify generally has the best UI/UX experience than any other music, podcasts, and audiobooks app. Combined with its algos that bring recommendations to the next level, Spotify, hands down, is the best app on the market.

It explains why it has an outstanding rating of 4.8 / 5 based on over 26 million ratings (!) on the US App Store alone and a solid 4.4 / 5 rating on Google Play based on 28.4 million reviews.

Spotify continuously holds the number one position in the music category on both app stores thanks to its fantastic app.

Switching costs

Spotify is a very sticky service with very little churn. Once users build their playlists and subscribe to podcasts, they have very few incentives to switch to different services.

Furthermore, the more you use the service, the more it learns your behavior, tastes, and preferences, allowing it to recommend new content with the maximum precision, which leads to more engagement. No other app does this job as well as Spotify.

Pricing power

Spotify has done over 40 price increases in the last two years in many developed and developing markets while its churn rate has been going down, a testament to exceptionally high user loyalty.

Spotify remains one of many subscription services which is still below $10 per month. For example, Apple Music costs $10.99 per month in the US.

Risks

Content rights

Major music labels have monopolistic leverage over Spotify, and it is extremely hard to negotiate anything with them, even with the help of Congress. The company will always feel pressure on gross margins from music behemoths.

Profitability

The current gross margins are too low to be a meaningful contributor to the company's profitability. Spotify must increase gross margins significantly to have a chance to turn profitable. At the current pace, it won't happen in the next three years, minimum.

Ad spending

Most companies have reduced ad spending in the current macro environment and economic slowdown. The ad spending will be softer in 2023, with a possible rebound not earlier than the second half of 2024.

Expenses

The company's operating expenses keep growing, outpacing the revenue 2x in 2022. They will likely remain high in the coming years, leaving no chance for the company to generate positive operating income.

Growth

The growth in new users will dry up at some point, and the company will need to turn to converting free users into paid ones (or generating more revenue from free users) to be able to continue showing revenue growth.

Ownership

The voting power is concentrated in the hands of just two people: Daniel Ek and Martin Lorentzon. No one else, including the board of directors, can influence any decisions in the company.

Additional Sources

Management [click here]

Board of Directors [click here]

Ownership, page 78 [click here]

Key Business Metrics, page 46 [click here]

Have a great weekend!!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.