Part 1: Deep dive on Sea Limited ($SE)

In order to read this entire deep dive on Sea Ltd ($SE) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (up +101.7% YTD) with my daily activity, my investment models and my webcasts.

Here are some of my other newsletters…

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus my daily commentary and morning newsletter.

Company: SEA Limited

Ticker: (SE)

Website: Sea.com

IPO date: October 20, 2017 (traditional IPO)

IPO price: $15

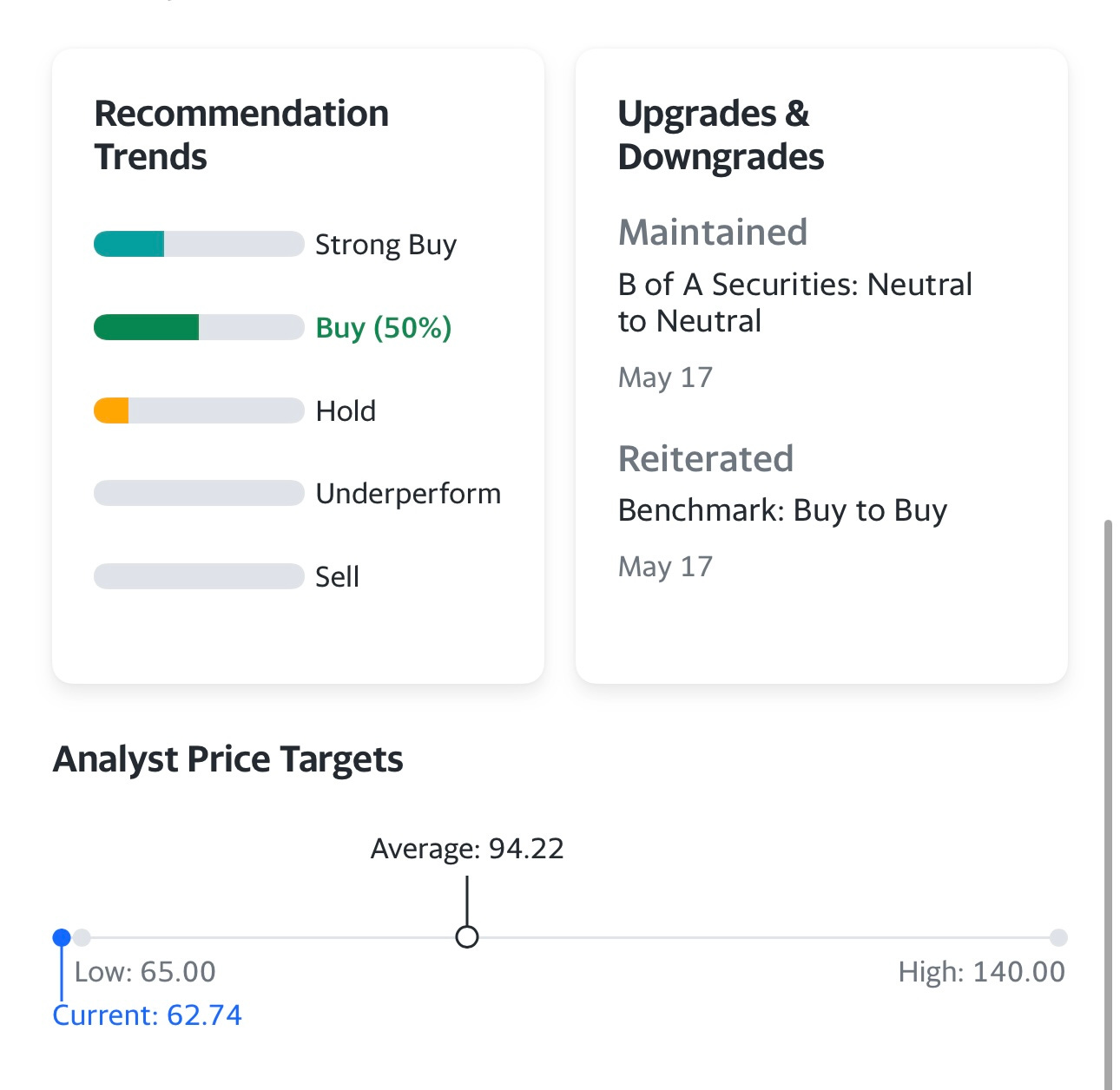

Current stock price: $62.74

Outstanding shares: 568.75 million (dual-class structure)

52 week high: $93.70 on August 11, 2022

52 week low: $40.67 on November 09, 2022

ATH: $372.70 on October 19, 2021

Market cap: $35.683 billion

Net cash/debt: +$2.071 billion

Enterprise value: $33.612 billion

Headquarters: Singapore

Number of employees: 64,000+

Average price target from analysts: $92.44

Next earnings call (Q2 2023): N/A

Investor Relations: https://www.sea.com/investor/home

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Q1 2023 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, part 2]

Below the paywall is part 1 of the Sea Ltd ($SE) deep dive along along with links to my investment portfolio (up 101.7% YTD), investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

Introduction

Disclosure: I started a 2% position in SE on June 30th, however I’ve trimmed my entire portfolio a couple times this month so my current SE position is closer to 1.8%

I made alot of money on SE in 2020 when I got into the stock in the $60s and rode it all the way to $350+ however I also rode it down to $200 before finally selling it in early 2022.

I have not owned SE in ~18 months until I started a position three weeks ago. I felt like the SE’s valuation finally made sense after the company decided to pivot from “growth at all costs” to “responsible, profitable growth” however the company needs to live up to these expectations or I’ll sell my shares.

If we look back over the past few years, we can see how much multiple contraction there has been for EV/SALES…

and EV/GP (gross profit)…

Back in 2020 we used to call SE the three-headed monster because it had three main parts to the business: (1) gaming, (2) ecommerce, (3) fintech

When I first bought the stock in 2020 all three pieces of their business were growing very fast however only gaming was profitable and those profits were being used to fund the growth in ecommerce and fintech. As the pandemic came to an end and gaming slowed down the rest of the business was still losing money because SE was trying to expand into international markets and losing a ton of money doing it. Finally the founder and CEO (Forrest Li) came to his senses and decided to shut down some of their international growth plans which helped slow down the losses.

Over the past 6 years SE has lost more than $6 billion however it appears we’re now at an inflection point because SE is expected to be profitable in 2023 (GAAP and non-GAAP) with 12.7% net income margins.

Analysts are expecting those net income margins to expand to 16% over the next few years while revenues grow at 10-15% per year. From 2017 through 2022, SE grew revenues at 86.4% per year so obviously the story has changed quite dramatically from insane growth with insane losses to slower growth with decent profits.

Here is my investment model… [here’s the link]

I got into SE on June 30th at ~$58 because I think the stock can double over the next few years (based on my estimates and investment model) however this is still a low conviction stock for me which means if my investment thesis falls apart and SE is growing slower than expected or not expanding net income margins than I’ll sell my shares. I also don’t love the current SBC ($706 million for last 12 months) but it’s not bad enough where it would be a deal breaker like COIN or SNAP.

I like that SE is still founder led and Mr. Li still owns a large chunk of the company so he’s definitely motivated to increase shareholder value. Tencent used to own 25-30% of SE but they’ve been selling down their stake quite aggressively which is certainly a risk. I’m still trying to figure out exactly how many shares Tencent still owns.

I still prefer MELI as a company and I think they have a better management team that has proven to have more financial discipline but it’s possible SE has slightly more upside over the next few years if they can hit my estimates. Whereas MELI is up +70.9% over the past 12 months and up +39.4% YTD, the same can not be said for SE which is down -9.3% over the past 12 months and only up +20.6% YTD.

MELI is expected to grow much faster over the next 3-5 years however SE is expected to have better profit margins — it will be interesting to look back in a few years and see which of these two companies was the better investment.

Company Background

Sea Limited was initially founded as Garena (now one of the group's three core businesses) in 2009 in Singapore by Forrest Li (who still runs the group and owns approximately 18% of all outstanding shares and 59% of the aggregate voting power), Gang Ye (who serves as a group Chief Operating Officer and owns approximately 6% of the group), and David Chen (who seats on the board of directors and holds around 2% of the group).

Garena started from Li's passion for gaming. At the time when he studied engineering at Shanghai Jiaotong University (China), he spent most of his free time playing games in local internet cafes. After finishing his undergraduate and having some corporate experience, he went to the US to complete an MBA course at Stanford Graduate School of Business, remaining committed to his love for gaming.

During his time at Stanford, Li experienced two significant events that ultimately led to the creation of Garena. Firstly, he met his future wife, who later landed a job in Singapore, prompting them to move there. Secondly, Li attended Steve Jobs' renowned 2005 Stanford Commencement Address, which left a profound impression on him and instilled the courage to finally launch Garena.

After moving to Singapore, Li met the other two founders, and together they launched Garena+, a platform for gamers to play and socialize with one another, join groups, and participate in online multiplayer battles.

Garena+ essentially acted as a game distributor first in Singapore and then across the entire Southeast Asia and Taiwan region. It published several high-profile games, including League of Legends (Riot Games), FIFA Online 3 (Electronic Arts), and Call Of Duty Mobile (Tencent Games). The platform also provided game-related news, updates, events, and promotions.

The pivotal moment for the company came in 2017 with the launch of Free Fire, a battle royale game. This game was not only published by Garena+, but it was developed entirely by Li's company.

Free Fire became an instant success, propelling Garena to one of the global leaders in game development and publishing. Just two years after its launch, Free Fire became the most downloaded game in the world (over 1 billion downloads), reaching a whopping 60 million daily active users in 2019. By 2023, the game had tripled its daily number of players worldwide (over 180 million).

Before the Free Fire game, Garena substantially generated all of its revenue from selling other games on its Garena+ platform. At the time (2014), the Southeast Asia region was highly unbanked. A tiny percentage of the population had banking accounts and credit cards, with some regions staying unbanked almost entirely.

To enable seamlessly buying games online on Garena+, the company launched AirPay (which later became Sea Money), a mobile payment network that also enabled Garena users to conveniently and securely pay for telephone bills, utilities, and e-commerce transactions. Over time, Sea Money grew beyond gaming users and expanded to various offerings, including loans, to become one of the largest payment players in the region.

Around the same time as launching AirPay (in mid-2015, concretely), as a way to diversify its business beyond just gaming, the company started Shopee, an e-commerce platform. The rapid increase in smartphone usage and internet penetration in the region enabled exponential growth for e-commerce, making this opportunity highly lucrative.

Shopee began its operations in Singapore but quickly grew to Malaysia, Thailand, Taiwan, Indonesia, Vietnam, and the Philippines, before going internationally to Brazil, Mexico, and India. Today, Shopee is arguably the leading e-commerce platform in Southeast Asia and of the key players in Brazil, the biggest market where Shopee operates.

In 2017, Garena underwent a significant rebranding effort, changing its name to Sea Limited in order to more accurately reflect the company's diverse range of businesses. That same year the company went public, raising approximately $884 million, including $100+ million from its already largest shareholder, Tencent. The stock opened at $16.25 (a small pop from the $15 initial price) and closed slightly below, at $16.20.

At the time of the IPO, 90% of the total revenue came from the company's gaming business. Sea Limited generated $414 million in revenue in 2017, while its losses have widened (from $222.8 million to $560.4 million) as the company was heavily reinvesting its snowballing profits from Garena into two other arms. The company followed this strategy for the next several years.

By 2021, Sea Limited became one of the most valuable companies in the Southeast Asia region, having hundreds of millions of users across all of its three thriving businesses.

In 2021 the company saw the biggest acceleration of its entire business in its history, growing its revenue by 127% compared to already incredible 2020 (revenues grew 101% YoY) and 2019 (revenues grew 163% YoY).

Sea Limited was undoubtedly one of the biggest beneficiaries of the pandemic, especially its gaming business. Millions of people poured tens of millions of dollars into in-game purchases in Free Fire, bringing the paying users ratio to its all-time high.

The stock price followed and reached its all-time high in October 2021 ($372.70 per share). However, it was the peak for Sea Limited, and the company has seen a sharp decline in its stock price by over 80% since then.

2022 was an especially challenging year for Sea Limited: tough comps with previous years, transition to post-pandemic life (which led to a sharp decline in both growth and profits of Garena), the macroeconomic environment, and other challenges. Despite all these difficulties, Li managed to quickly pivot the company and eventually turn around its entire business.

After years of losing money, Sea Limited is finally shifting to profitability. Garena was the company's main profit driver for a long-time (helping to fuel the other two businesses), but not anymore. While Garena is currently experiencing a difficult period, SeaMoney and Shoppe are having the best time in the company's history: the first has recently become profitable, while the second is close to profitability. Most importantly, both businesses continue growing at very decent rates with no projections to slow down anytime soon, primarily due to improving monetization in the e-commerce business and the growth of the credit business.

Sea Limited continues to fine-tune its operations and navigate near-term macro uncertainties on its way to becoming a highly profitable company with expanding profit margins. It is perhaps a pivotal moment for the company, which should see unprecedented growth in its earnings from a negative $1.65 billion in 2022 to a positive almost $1 billion in 2023 while long-term opportunities remain strong as ever.

Opportunity

Trends

Sea Limited primarily operates in the Southeast Asian region, which has a number of its own emerging trends, such as rapid digitalization, a significant increase in internet usage, a growing middle class, an expanding e-commerce sector, and a growing demand for digital financial services.

Additionally, Sea Limited benefits from the overall growth of the gaming industry, which is expected to continue its upward trajectory in the coming years in the pursuit of becoming the largest entertainment segment in the world.

Below are the key trends that will profoundly impact the continued growth of Sea Limited:

Growth of the Southeast Asian region

The Southeast Asian region comprises eleven countries (Brunei, Burma (Myanmar), Cambodia, Timor-Leste, Indonesia, Laos, Malaysia, the Philippines, Singapore, Thailand, and Vietnam) at different stages of development.

But this region is characterized by a relatively young population, with a median age of about 30, compared, for example, to China (38.4) and Europe (44.1). These young people are more open to adopting digital technology, driving digitalization and Internet penetration in the region.

According to ASEAN.org, more than 460 million people in Southeast Asia used the Internet in 2022, which is a penetration rate of 80%, with countries like Singapore and Malaysia having higher penetration rates (over 90%). It is one of the main reasons why Southeast Asia's economy is one of the fastest-growing in the world.

Over the past few years, the region's economy has become more robust and diversified. All countries in the region are in the growing mode, together outpacing the growth of developed countries such as the United States, Europe, and China. By 2030, this region is set to become the biggest market globally.

E-commerce growth in the region

The widespread Internet usage has led to the rapid growth of e-commerce in the region. More and more consumers are opting to shop online (now including food and beverage, beauty products, and home and living goods) because of its convenience and wide range of options. The expanding middle class, with its rising disposable income, further propels the growth of e-commerce.

The value of the e-commerce market in Southeast Asia has seen a dramatic increase in recent years, from $43 billion in 2019 to $74 billion in 2020 to $112 billion in 2021 to $131 billion in 2022. The market size has tripled within this period, and according to Statista, it will further grow to reach a minimum of $211 billion by 2025.

There is a long growth runway for e-commerce in the region, as per McKinsey, which suggests that Southeast Asia's average e-commerce penetration rate (excluding food and beverage) is only 20% (for example, China’s penetration rate is 47%).

Indonesia and Singapore are leading the region with approximately 30% e-commerce penetration, while the Philippines, Thailand, and Vietnam are trailing slightly behind, at about 15%.

Indonesia, Southeast Asia’s largest economy, is the biggest driver of growth and contributes about 51% of the total incremental gross merchandise value (GMV) in the region.

Further growth of the e-commerce sector will highly depend on logistics capabilities. The growth of logistics businesses is a large trend within the e-commerce sector that will unfold in the next five to ten years.

Growing demand for digital financial services in the region

According to McKinsey, Asian consumers are expected to account for half of global consumption growth between 2020 and 2030, which is around a whopping $10 trillion. By 2030, around 70% of Asia’s total population will be considered the consuming class (could spend more than $11 per day in 2011 purchasing power parity terms).

As more consumers experience growing incomes, their financial needs also increase, boosting the demand for digital financial services.

Yet, most of Southeast Asia’s population is still unbanked (more than six in ten people). Furthermore, the majority of the working population is in the informal sector (not officially hired), making it difficult for such workers to obtain a banking account in the first place and then build a credit history.

Primarily because of this, digital payments have surged in the region in recent years. E-wallets have seen a dramatic increase in use (many call Southeast Asia the "wallet first" region), making this payment method the most popular in almost all countries of the region, far outpacing credit cards.

Today, only about 17% of transactions are cashless, providing massive opportunities for growth. The digital payments industry is expected to experience significant growth in the coming years, with transaction values estimated to reach between $600 billion and $1 trillion by 2030.

E-wallets provide a natural transition into financial services where real monetization happens, specifically in lending (there is also credit, insurance, and other minor services like wealth management that includes investing). Something that was previously available only for “the wealthier” is now increasingly becoming available for the masses.

Additionally, lending is becoming a primary source of capital (to pay suppliers, rent and bill, and cover unexpected business cash flow needs) for hundreds of thousands of micro, small, and medium-sized enterprises (MSMEs). More and more companies of all sizes are relying on P2P lending services to fund their growth and expansion plans.

Lending is expected to see near-exponential growth in the coming years and is the biggest opportunity within digital financial services.

Gaming popularity

In recent years, the digital entertainment industry in Southeast Asia has experienced a remarkable surge in popularity, especially online gaming.

With the increasing affordability of smartphones and growing internet penetration, mobile gaming has seen a significant rise in the region. It is the primary reason games like Free Fire have achieved massive success in Southeast Asia.

It is estimated that there are more than 250 million mobile gamers in the region (about half of which are paying players). Almost every second person plays a mobile game at least once a month, with Indonesia, Malaysia, Thailand, Vietnam, Singapore, and the Philippines being the six biggest markets for mobile games.

Additionally, Asians, in general, are massive fans of eSports, which has seen a dramatic increase in popularity in recent years. This region specifically has a vibrant esports scene, with an increasing number of skilled players and professional teams, competing for millions in cash prizes (and medals since 2019) and attracting millions of viewers worldwide.

In recent years, play-to-pay (and other variations) games have become increasingly popular in the region. More and more people now see playing games as a way of earning income.

While most research firms do not expect tremendous growth of the gaming industry in the region going forward (it seems it has saturated already), the market is still large and offers great opportunities.

For companies like Garena, with the games like Free Fire, there are further opportunities outside the Southeast Asian region.

Total Addressable Market (TAM)

The Southeast Asian countries have a total population of 662+ million people and a combined gross domestic product (GDP) of a minimum of $3.5 trillion. GDP is forecasted to grow further this decade at a much faster pace than the global average.

Southeast Asia will soon become the largest region in the world, with Internet penetration level unmatched by any other region. People in this region are experiencing a generational transition to the new digital economy that includes shopping online and using digital wallets for payments, all from mobile.

With an average age of 30, this region's workforce is one of the main driving forces of economic growth for decades ahead.

Separately, gaming is the second-largest entertainment segment in the world (after Television) but is the fastest-growing among all of them. Today, mobile gaming accounts for around 70% of all gaming, and this percentage is expected to grow as mobile devices continue to improve each year.

Growth Drivers

Sea Limited is now primarily focused on Shopee and SeaMoney segments, as both businesses have reached the turning point of becoming profitable while still having plenty of opportunities ahead.

Garena has been stagnating in recent quarters and will likely continue doing so in the upcoming future, though it also has some opportunities that may help to turn around this business segment.

Further are the main growth drivers (per each business segment) that should help Sea continue to increase revenue in the coming years (bringing it from $12.44 billion in 2022 to over $17 billion by 2025, a CAGR of about 12%) while dramatically accelerating earnings (from a loss of $1.65 billion in 2022 to almost $2 billion in 2025).

Garena

Garena offers localized mobile and PC online games of third-party developers and develops its own mobile games for the global markets.

Free Fire, Garena's biggest and only hit game (so far), has been under fire recently. A continuous decline in bookings, quarterly active users, and the paid player ratio that has been going on for multiple quarters has led many investors to believe this is the beginning of the end of this gaming franchise, which will significantly impact Garena's business.

However, Free Fire remains one of the largest mobile games in the world. The active user base has seen initial signs of recovery in the recent quarter, growing from 485 million at the end of 2022 to 492 million in the first quarter of 2023. Although it had over 615 million players a year ago, having nearly 500 million active players is still a significant number.

Certainly, the number of paying players has declined sharply, from around 10% (as a result of the pandemic) to 7.7% in Q1 2023. But it is back to 2019 levels, indicating the normalization of the business in the post-pandemic world where many players have gone back to school or work.

Furthermore, in April 2023, the company saw positive user trends in Free Fire, achieving a new peak in monthly active users for the first time in the last eight months period.

Right now, Garena's team is actively focused on enhancing gameplay and user engagement for Free Fire. The goal is to stop user churn, get back to growing the number of monthly active users, and then find new ways to monetize its gigantic user base of active players.

The biggest opportunity for Garena right now is in popularizing Free Fire in Western countries, where this game is less popular than other battle royale hits like PUBG and Fortnite. Furthermore, players from the West are more likely to become paying players, which will significantly help the company at least bring the lost revenues back.

But Free Fire is not the only game in Garena's portfolio. Its second largest game, Arena of Valor, has shown strong performance recently. The game once again achieved a new peak in quarterly active users and bookings, and it is after more than six years since its initial launch, indicating that the game is still popular and growing.

The company has two more new titles in its pipeline. One particular, Undawn, a free-to-play open-world survival RPG, was launched in June 2023 in selected markets across Southeast Asia. Pre-registrations are available for other countries.

The second game, Black Clover Mobile, an RPG mobile title based on the popular anime series “Black Clover,” is now being tested in selected markets across the globe. Pre-registrations are expected to open within the first half of the year.

Both games are promising (especially Undawn) and may help lift the gaming division's revenues. Garena has already gained access to millions of users who can now be introduced to its new games.

Bottom line: The current weakness of Free Fire could be a massive long-term win for Sea Limited. Having a minimal impact on the top and bottom lines from Garena is a highly advantageous position for the group's overall business. Once Garena is back to growth, it will only benefit the company.

Shopee

Shopee's e-commerce platform is a mobile-centric, social-focused marketplace with integrated payment and logistics infrastructure and comprehensive services that the company offers to sellers.

Shopee is currently the largest online marketplace in Southeast Asia, holding a 30% to 50% traffic share across the region in the last three months, while Lazada is in second place with 10% to 30% traffic share.

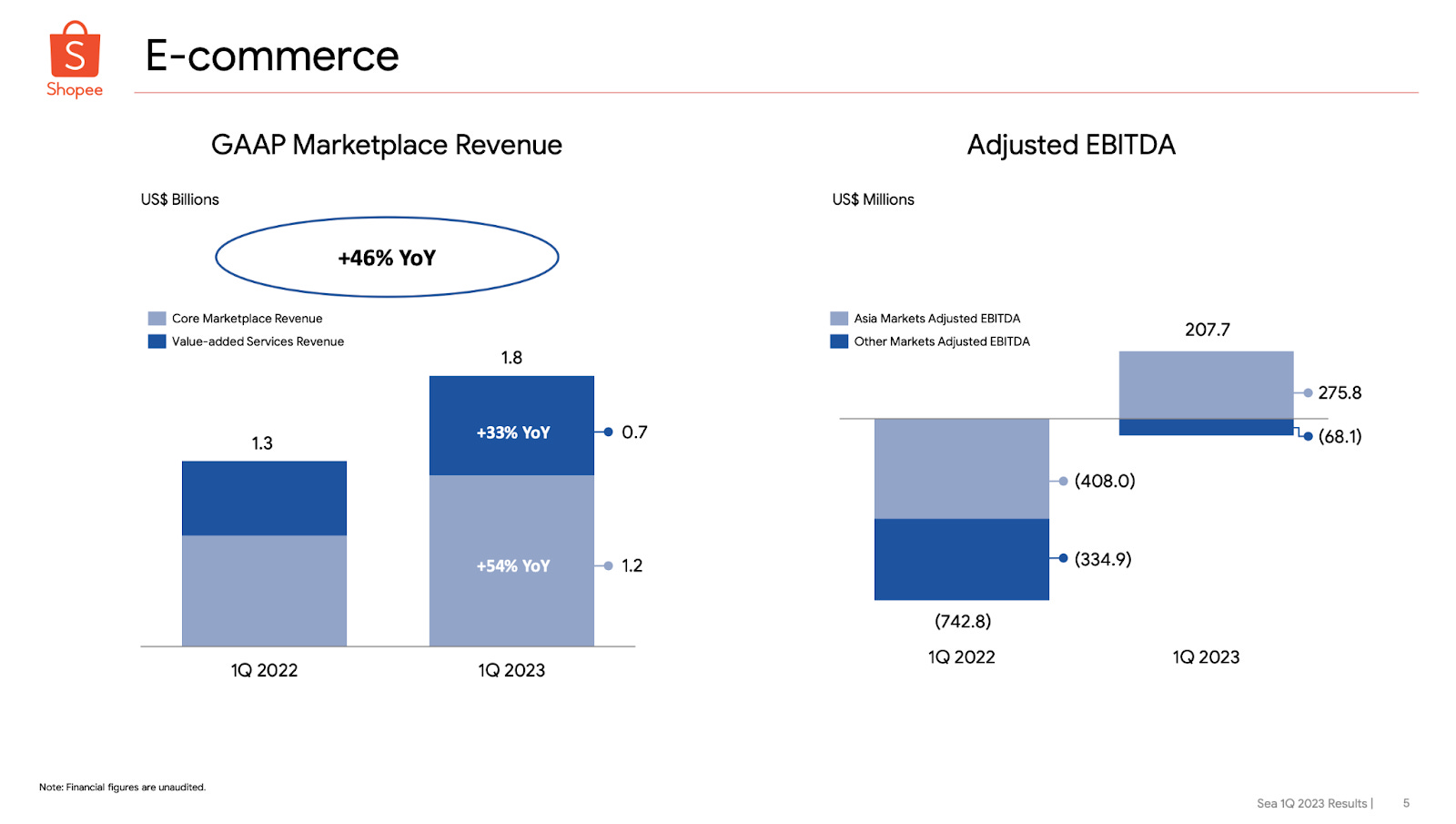

The performance of the e-commerce business has been strong lately. In the first quarter of 2023, revenues grew by 45.5% YoY to $1.8 billion, while profitability (on an Adjusted EBITDA basis) improved immensely from a hefty loss of $742.8 million in the same period last year to $207.7 million profit.

While the company no longer reports gross merchandise volume (GMV) on a quarter-on-quarter basis, the management sees a general upward trend in GMV, especially in the key markets (Indonesia, Thailand, and Malaysia).

More brands are joining the Shopee platform, and more sellers are contributing to GMV than previously. Additionally, a lot of partnerships are signed that further increase the number of products available on the platform and improve the overall user experience.

User experience is also greatly improved by implementing AI. AI helps to recommend more relevant and personalized offerings to the users, driving higher order conversions as users discover products more quickly and easily.

The company has also adopted large language models to improve the AI-powered chatbot’s ability to understand its users in different languages and return the most relevant solutions given the context. This enhanced resolution rates and helped reduce waiting times.

Shopee is now actively expanding its footprint in Malaysia and overall working on deeper monetization in all Southeast Asian markets, which includes increased transaction-based fees and growing advertising revenue.

Brazil stands out. It is possibly the biggest opportunity for Shopee, especially after exiting other Latin American countries and seizing its European operations.

Just four years after entering the market, Shopee has reached 3 million local sellers in Brazil (which now account for around 85% of all Brazil orders). While it is still early, Shopee has already achieved the scale of being one of the leading e-commerce players in the country, especially on the local-to-local level, which targets mass market segments.

Given this scale and high operational efficiency, the company is near breakeven in Brazil. However, management prefers to invest further in this market to capture significant long-term opportunities.

Targeting underserved mass markets is perhaps the company's biggest opportunity, not only in Brazil but also in other markets where Shopee operates. Shopee is best positioned to capture this gigantic target group.

Bottom line: Shopee is the main growth driver for Sea Limited for the very long term. The company's focus on building long-term structural advantages in its e-commerce ecosystem will drive growth for decades.

SeaMoney

SeaMoney is one of the leading digital financial services providers in Southeast Asia. SeaMoney currently offers offline and online mobile wallets, payment processing, and other offerings across credit, insurtech, and digital bank services. It operates under different brand names, including ShopeePay, SPayLater, SeaBank, SeaInsure, and others.

SeaMoney is deeply integrated into Shopee and is the main payment option on the platform. But the company is actively working on integrating SeaMoney into various third-party merchants, including telecommunications companies, online and offline entertainment services providers (game operators or app stores, movie theaters, concert/event venues), utility service providers, food delivery service providers, credit card issuers, banks, insurance companies, and car leasing companies.

The more merchants will accept SeaMoney, the more users SeaMoney will have on its platform and the more digital financial services the company will be able to provide them, such as credit, insurtech, and digital bank services.

SeaMoney has been doing incredibly well in the past several quarters. In the most recent, Q1 2023, the revenue from digital financial services grew 75% YoY and reached $412.8 million. Most importantly, the company achieved positive Adjusted EBITDA (of almost $100 million) for the second straight quarter, signaling that SeaMoney is fast approaching profitability.

Credit is currently the biggest part of SeaMoney's business. Total loans receivable stood at $2 billion as of Q1 2023. Despite a large part of loans already being funded by alternative sources instead of cash on the company's balance sheet, the company is looking to increase the quality of funding sources vs. getting more funds. As a result, the loan book is unlikely to grow significantly in the short term, but the overall credit business should improve in the long term.

Additionally, SeaMoney is looking to expand its product offerings and features within each product (both on and off the Shopee platform and across different markets) so that users can enjoy a more comprehensive suite of products and services that meet their underserved financial needs.

For example, most recently, SeaMoney piloted new insurtech products and expanded use cases, features, and services in its banking apps. This should enable even greater convenience for the users and provide more access to financial products for all types of users on the platform. These products are also now a part of Sea's broader ecosystem that combines SeaMoney, Shopee, and Garena.

Or SeaMoney's digital wallet, ShopeePay, lately became a payment method for Apple services in all Southeast Asia markets, further driving use cases for SeaMoney.

Bottom line: SeaMoney has the potential to evolve into a "super-app" that combines multiple functionalities in a single app, a concept that is highly prevalent in China. Although the company may not accomplish its intended goal with the "super-app," it is still in a favorable position to seize the substantial and overlooked opportunities in every market where SeaMoney operates.

Business Model

Garena

Free Fire (and other games developed by Garena) are free-to-play (users can download and play fully functional games for free).

Garena generates revenue primarily from selling in-game items, such as virtual items (aesthetic customization options or functional advantages that can enhance the gameplay experience, like skins, characters, weaponry or equipment, pets, and diamonds) and season passes (a tier-based system where players can earn rewards (like exclusive character and weapon skins, emotes, vouchers, and more) through completing in-game challenges).

Players can purchase in-game items through various payment methods embedded into the games, including SeaMoney, Google Play Store, iOS App Store, other online payment gateways, bank transfers, credit/debit cards, mobile phone billing, and prepaid cards (including Garena's own prepaid cards, which are sold through agents).

Shopee

The company primarily monetizes Shopee in three different ways:

by charging transaction-based fees,

by charging for certain value-added services (including logistics),

and by offering sellers paid advertising services.

Transaction-based fees are the biggest source of income, and the company was able to successfully increase these fees recently, which are now more than 5% on average.

The company also sells its own products directly on the Shopee platform. It sources these products from various manufacturers and third parties and sells them with a little markup (the gross margin is only 10%). However, the primary goal is to fulfill buyers' demands for certain products on the platform rather than generating significant revenue.

SeaMoney

SeaMoney is also monetized in three ways:

by charging fees (for mobile wallet services, payment processing services, and various financial products (including lending to SeaMoney users) offered by third-party financial institutions),

by earning interest from credit provided by SeaMoney,

and by earning a premium from its insurance business.

The interest revenue from providing credit is the largest income source for SeaMoney.

Gross Margin

Garena has higher gross margins (~72%) than the other two business segments that are reported combined (~30.4%).

Garena's primary cost of revenue consists of channel costs (like App Store / Google Pay fees), which are generally deducted as a percentage of gross billings. Other costs include server and hosting costs, upfront licensing fees (for non-Garena games), and staff compensation (including the share-based compensation).

Shopee costs include expenses associated with its logistics and other value-added services, bank transaction fees (for all transactions conducted on the Shopee platform), server and hosting costs, and staff compensation.

SeaMoney costs primarily consist of interest expenses for deposits payable, bank transaction fees (for all transactions conducted on the SeaMoney platform), commissions the company pays to counter operators, server and hosting costs, and staff compensation.

The combined efforts of the three businesses have resulted in an impressive gross margin of approximately 42% (in 2022). The total gross margin has been in an upward trend for several years, growing from just 1.8% in 2018 to 27.8% in 2019 to 30.83% in 2020 to 39.1% in 2021. In the latest quarter (Q1 2023), the gross margin was 46.58%, while the record was in Q4 2022 when Sea Limited reported a staggering gross margin of almost 50%. These figures speak volumes about the outstanding performance of Shopee and SeaMoney in the past year.

Operating Expenses

Sea Limited continues to show operating efficacy. Operating expenses as a percentage of total revenue have been improving significantly in the past five years, down from 120% in 2018 to 51% in 2022. In the past two quarters (Q4 2022 and Q1 2023), operating expenses were 34% and 39%, respectively.

The company has been exceptionally successful in cutting sales & marketing expenses while still growing revenues and posting operating income for the first time in its history.

Profitability

Sea Limited was unprofitable for over a decade due to aggressive reinvesting into its businesses. The inflection point happened in Q4 2022 when the company surprisingly posted $426.8 million in net income before delivering another $88 million in Q1 2023 (it would have been over $205 million if not a one-time impairment cost). The company reached its profitability much faster than Wall Street expected it.

Now, the analyst's consensus is that Sea Limited will post an astonishing almost $1 billion in net income in 2023, from a loss of $1.65 billion a year ago. Furthermore, analysts expect that the company will accelerate its earnings going forward.

Even a considerably high share-based compensation (6.54% of total revenue in Q1 2023 or $199 million, which the company decided to spend on employee compensation in the form of shares instead of cash) is not stopping the company from aggressively growing its earnings.

But Sea Limited has been significantly diluting its shareholders in the past five years (over 65%). The bright side is that the stock price has appreciated by 435% (over 3000% at a peak in 2021).

Balance Sheet

Sea Limited is in a great financial position, even with $3.33 billion in debt (convertible notes). A large part of this debt ($2.5 billion) was issued at a time when the stock price was much higher ($318 per share). The company has already repurchased $611 million of that debt and will most likely buy back all notes before the expiration date while making a considerable amount (in hundreds of millions) in gains.

With over $8 billion on its balance sheet (cash and investments), the company has plenty of capital to continue investing in the growth of all its three businesses and potentially add more (including acquiring others).

Most recently, management announced that the company would boost the pay of most of its employees by 5% starting July 2023, which is another strong indicator that it is doing well financially.

Cash Flow

The cost optimization can also be seen in the free cash flow generation, which has improved dramatically since the second half of 2022: from a negative $398 million in Q3 2022 to a positive $168 million in Q4 2022 to a whopping $504.5 million in Q1 2023.

Analysts expect Sea Limited to deliver over $800 million in positive free cash flow in 2023, giving the company even more leverage to invest in business optimization (including logistics) and further growth.

*

Sea Limited is on its way to becoming a highly profitable and cash-generative company. Switching from "growth at all costs" to profitable growth highlights the power of its business model, where one business segment may experience a temporary decline while the other two are just starting to scale and provide the necessary backup, a luxury that only a few companies possess.

Competitive Advantages

Competition

Sea Limited faces severe competition in all three business segments.

Shopee

In the Southeast Asian markets, Shopee primarily competes with Lazada (and also Tokopedia in Indonesia, the largest market in the SEA). Shopee overtook Lazada to become Southeast Asia’s biggest e-commerce platform in 2020, and the recent traffic numbers confirm this. Still, the competition is there, and it is intensifying.

In recent years, global e-commerce and internet companies have also been trying to enter the SEA markets. One such company, TikTok, is making significant splashes.

TikTok Shop is aggressively expanding in Southeast Asia (already present in Singapore, Malaysia, Indonesia, the Philippines, Vietnam, and Thailand), growing its GMV four times in 2022 to $4.4 billion. Analysts expect that TikTok's GMV in 2023 will reach about 20% of Shopee's.

In Brazil, Shopee faces even more intense competition from the absolute market leader, MercadoLibre, as well as Americanas (the largest online retailer in Brazil, which has experienced significant difficulties lately) and many other smaller players.

Garena

Since Garena operates globally (in over 130 markets), it competes with a wide variety of game publishing companies, especially those that develop and publish games in the battle royale genre. Among the main competitors are Epic Games (Fortnite) and Tencent (PUBG).

PUBG is the most popular among these three main battle royale games, and it has been the top-grossing game worldwide in 2022 (despite the 44% decline in revenue), 2021, and 2020. It remained number one in the first half of 2023.

Additionally, Garena competes with games in other genres, other similar gaming platforms, and other entertainment formats (like TV) for time, attention, and spending on entertainment by its players.

SeaMoney

SeaMoney primarily faces competition in the digital banking space from traditional banks and financial institutions (both regional and local), other digital banks, neobanks, non-bank fintechs, and other financial providers that may provide loans at more attractive rates, credit, or other terms.

Competitive Advantages

Each of the three Sea's businesses has a set of competitive advantages that helps differentiate them from rivals and allows the company to capture a significant share of the Southeast Asian market.

Shopee

Shopee's main competitive advantage is its wide ecosystem. It starts with sellers, which the company supports with various services, including shipping, marketing, and financing.

While companies like TikTok may take a certain percentage of GMV from Shopee because of its viral nature of content and great implementation of buying options, the real battleground is in logistics, where Shopee currently has a strong advantage over every competitor.

This comes from continuous investments in building out a logistics infrastructure in certain markets and partnering with local providers in others, creating the most sophisticated logistics network in the region.

For example, Shopee’s delivery services now cover 95% of its customer base in Indonesia (the largest market in the region), and it has been expanding its first and last-mile hubs in Brazil.

Investing in logistics capabilities provides an advantage in customer experience (significantly cut down delivery times) and cost efficiency (better delivery prices).

The more value Shopee creates for sellers, the more sellers join the platform. It triggers positive network effects as more sellers attract more buyers, creating an endless loop that drives growth.

Another part of Shopee's ecosystem is its Affiliate Program, which invites social media influencers to promote products sold on Shopee. The company recently reported having 4 million registered influencers across all markets. In one particular market, Indonesia, the company's largest market, orders generated by affiliate partners more than tripled in 2022.

Shopee also enjoys the pricing power advantage. The company stopped giving out as many coupons as it did previously. It also increased transaction-based fees for merchants. None of this resulted in any slowdown in revenue growth, pointing to Shopee's resilience and strength.

Garena

Garena's previous success with Free Fire is its main competitive advantage. Out of thousands of game development companies publishing tens of thousands of games every year, Garena is in a league of its own.

Free Fire showcases not only the company's ability to create high-quality (AAA) games but also bring the game to such a massive audience. And while the company did not publish any new hit game since 2017, when it launched Free Fire, its in-house development team is one of the best in the world, without any doubt. They may very well be in the process of creating the next big hit right now.

SeaMoney

The competitive advantage of SeaMoney stems from its seamless integration with Garena and Shopee. Both these platforms encourage their massive users to use SeaMoney for transactions, acting as an effective (and perhaps free) user acquisition channel.

Once users start using SeaMoney for transactions, the company tries to offer them digital financial services, which include credit, insurance, and other services.

The more users end up using SeaMoney, the more value it creates for other merchants to connect SeaMoney as one of its payment methods (and maybe even make it a primary one). This, in turn, brings even more users for SeaMoney, to whom the company can offer digital financial services.

Risks

Macroeconomic environment

Changes in the macroeconomic environment (both locally and globally) profoundly impact companies like Sea Limited. All of its three businesses are sensitive to economic downturns, especially Garena. With less disposable income, users buy fewer in-game items, shop online less, and take fewer loans.

Regulatory risks

Sea Limited primarily operates in developing countries (including Brazil), which are prone to various regulations and changing laws risks. Countries in emerging markets generally differ from developed markets in the level of government involvement and control, making operating in these countries unpredictable. For example, if a new government is elected in a certain country, it may change policies overnight at any time, which will profoundly affect Sea Limited.

Growth

The company showed how quickly it can turn profitable by mostly cutting on promotions and other operating expenses. However, this could significantly stall the growth perspectives, which are already down dramatically from 2021 and 2020 levels. Sea Limited is no longer a growth company and will likely never return to previous growth levels.

Profitability

Despite the projected remarkable increase in earnings in the coming years, the company may not sustain such growth for long. The company's monetization efforts of Shopee may require more cash for a much longer period, which will drag the profitability down. There is no guarantee that the company will sustain profitability at all in the future.

Dependence on Free Fire

Garena substantially depends on its most popular and only hit game, Free Fire. Recent quarters have already shown how dramatically this business segment can suffer if Free Fire sees a decrease in usage and paying users.

Furthermore, the popularity of games tends to shift over time. The new hot game can quickly replace long-standing favorites. In the world of limited user time, where thousands of games compete with hundreds of TV shows and other forms of entertainment, it is absolutely critical for Garena to have the next big hit as soon as possible or at least introduce something radically new in Free Fire that will attract both new and returning users and boost the number of paying users.

Shopee

Being the number one growth driver of revenue and earnings for Sea Limited going forward, Shopee has a number of its own risks, from not reporting a quarterly GMV number anymore and seeing a significant decrease in the advertising business to growing competition (and increasing costs on promotion as a result) and concentrating most its revenue in three top markets to failing effectively monetize the entire business.

Logistics stands out from this list as it is the most critical piece of Shopee's current and future success. Logistics could make or break the company.

Shopee overall is absolutely critical for Sea Limited and should be monitored by investors much closer than the other two segments.

Competition

Growing competition in the Southeast Asian region will remain one of the critical risks for Sea Limited, making it even harder to expand revenues and sustain earnings growth.

More information about the competition is in the Competitive Advantages section.

Credit risks

SeaMoney, which also contributes to the company's profitability from now on, highly depends on its credit business, which carries a number of its own risks, including credit cycle volatility and risk of credit losses.

Additional Sources

Corporate Governance – https://www.sea.com/investor/corporategovernance

Ownership (note dual-class structure)

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.