Part 2: Deep dive on Pinterest ($PINS)

Part 2: Deep dive on Pinterest ($PINS)

In order to read this entire deep dive on Pinterest (PINS) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (up +85.5% YTD) with my daily activity, my investment models and my webcasts.

Here are some of my other newsletters…

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus my daily commentary and morning newsletter.

Company: Pinterest

Ticker: (PINS)

Website: Pinterest.com

IPO date: April 18, 2019 (traditional IPO)

IPO price: $19.00

Stock price at the time of writing: $27.24

Outstanding shares: 683.7 million (594.3 million Class A and 89.4 million Class B)

52 week high: $29.27 on March 27, 2023

52 week low: $16.77 on July 26, 2022

ATH: $89.90 on February 16, 2021

Market cap: $18.624 billion

Net cash/debt: +$2.57 billion

Enterprise value: $16.054 billion

Headquarters: San Francisco, California, United States

Number of employees: ~4,000

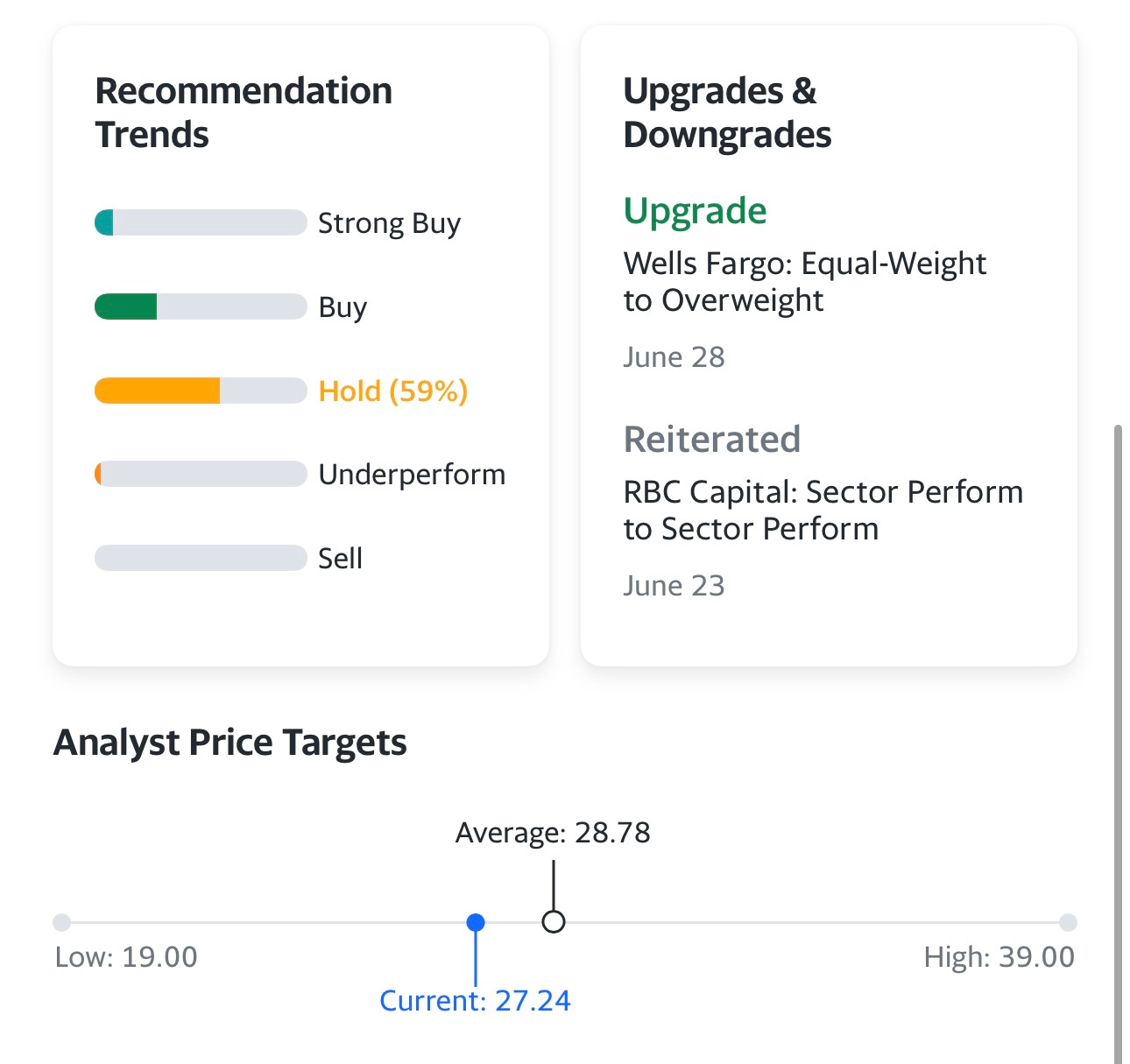

Average price target from analysts: $28.78

Next earnings call (Q2 2023): N/A

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Q1 2023 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

Here’s part 1 of the PINS deep dive in case you missed it…

Below the paywall is part 2 of the Pinterest (PINS) deep dive along with links to my investment portfolio (up 85.5% YTD), investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Weekly webcasts [click here] — I’m bringing the webcasts back this week, just haven’t finalized the times yet

Even though I'm not too bullish on PINS, I thought it was important for me to do this deep dive just to make sure I wasn’t miss any potential opportunity plus it’s a popular stock with retail investors and I’ve had several subscribers ask me about the company. I’m pretty sure I know the next 4-5 large caps that I’ll be covering in this Substack newsletter and I’m definitely more bullish on most of them for the next 3-5 years but I will say this… many growth stocks are up alot since their lows last year so it’s getting a little harder to find companies that I’m still bullish on at current prices. In terms of large caps and companies that I have not covered yet… I like DECK, LULU, ADBE, AMD, NVDA, BKNG, ZS, PANW, WDAY, LYV, ENPH, AXON, and several others but many of them have slowing growth with frothy valuations so it’s hard to get excited about them. It’s almost impossible to find large cap companies with revenue & earnings growth above 20% with a PEG ratio at 1.0x or below — because of this I’m definitely finding more opportunities in small/mid cap stocks so I’d recommend subscribing to that newsletter as well.

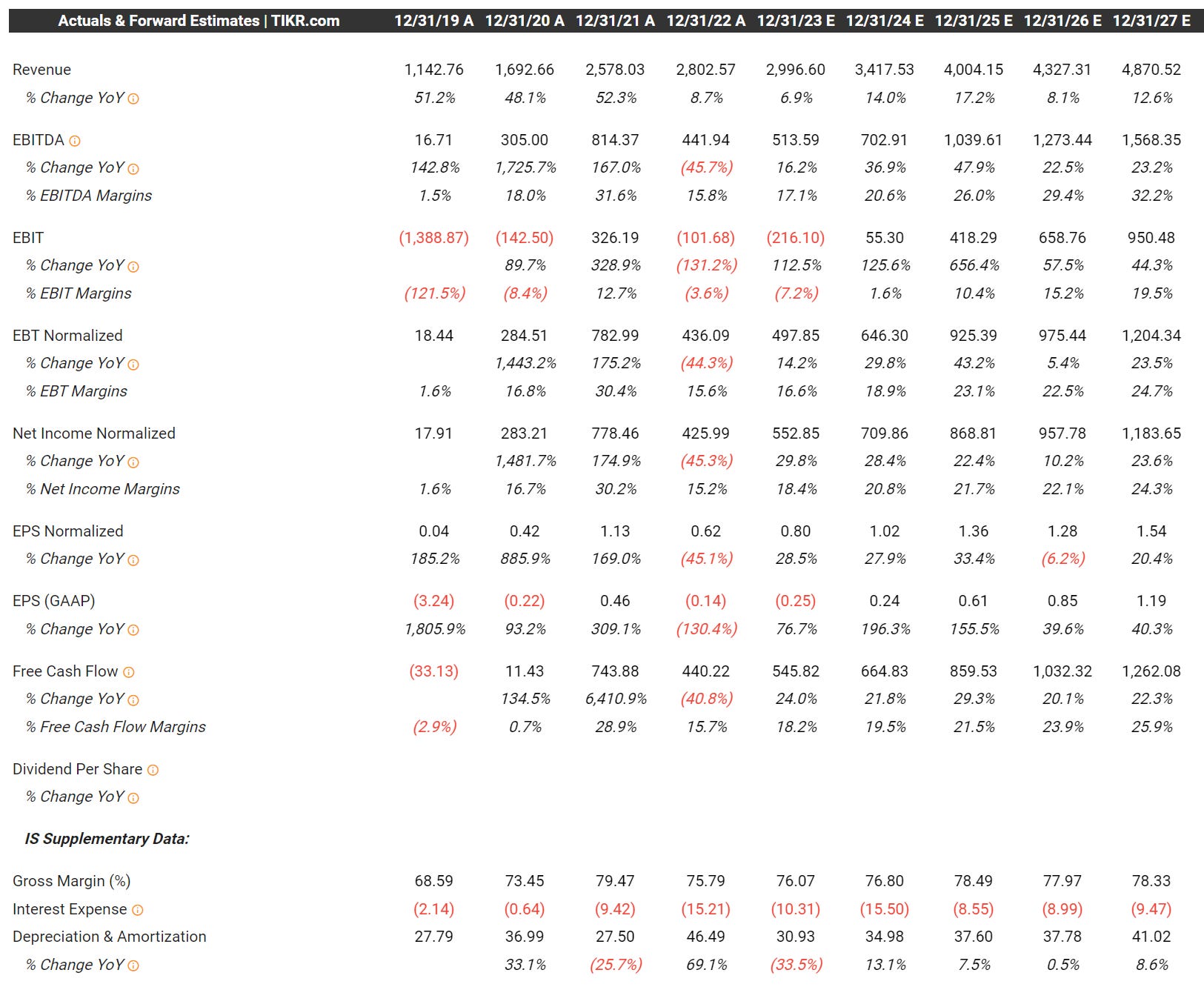

Valuation

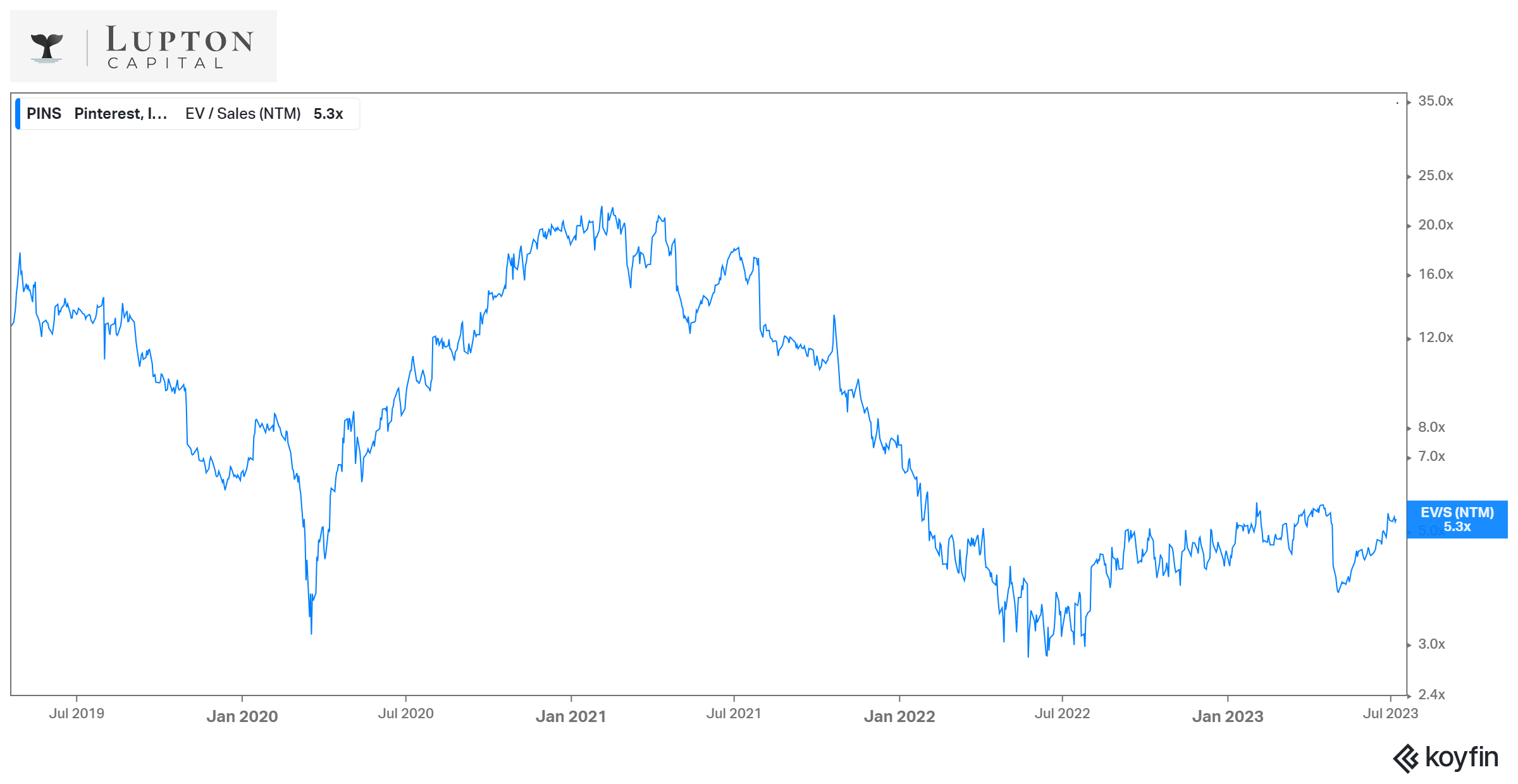

Regardless of what metric you use, PINS is much cheaper than it was a few years ago but the problem is that the growth rates have also come way down. Several years ago when PINS was trading at 25x EV/Sales (which was an insanely high multiple), at least the company was growing revenues by 50% per year. Now the stock is trading at 5.3x NTM EV/Sales but that because growth has slowed down to 8-12% YoY and it might accelerate back into the high teens or even low 20s but the days of 40-50% growth are over so investors need to understand this is not a growth stock anymore and it’s still way too expensive to be a value stock so it’s stuck in the middle — not even sure it’s fair to call it a GARP stock although it’s possible that’s the group it belongs in with companies like ADBE, LULU, DIS, PYPL, ISRG and others that are growing revenues by 10-20% with 15-30% earnings growth but trading at PEG ratios closer to 2.0x.

If we look at EV/EBITDA, the multiple has also dropped significantly over the past few years — 30x NTM EV/EBITDA looks much more reasonable that 400x EV/EBITDA from several years ago. According to the current analyst estimates, PINS is expected to grow EBITDA by 30% per year for the next 3-5 years so the current multiple is reasonable but not cheap with revenue growth in the single digits.

If we use the current enterprise value of $16 billion, PINS is trading at 31.1x 2023 EV/EBITDA and 22.7x 2024 EV/EBITDA, since we’re now in the second half of 2023 it’s reasonable to start looking at 2024 estimates.

If we look at non-GAAP net income, PINS is current trading at 28.9x 2023 EV/NI and 22.5x 2024 EV/NI — both multiples are reasonable considering the growth rates but you probably won’t see much more multiple expansion unless the company surprises to the upside on revenues and/or margins.

If PINS is only expected to grow non-GAAP net income by an average of 22% over the next 4-5 years then it’s not reasonable to pay more than 30x net income, I’d say 33x at the most which would be a 1.5x PEG ratio.

Investment Model

As you can see from my investment model, there’s just not enough upside to get me excited about owning this stock. I don’t think PINS can double over the next few years unless they surprise to the upside with both revenues and margins which is always possible if they continue pushing into ecommerce and crush it with some of their strategic partnerships like they one they recently announced with Amazon.

Assuming that PINS gets revenues to $5.2 billion in 2027, with 24% net income margins and a 23 P/E multiple, it only gets you to $43.80 once you add back the cash. If we use a 1.5x PEG ratio and a 28 P/E now we’re getting closer to 100% upside by end of 2027.

Analysts

There are approximately 20 analysts that cover PINS with a rating and price target — the average rating is a buy/overweight but the average price target is $27-28 depending on what platform you’re using for this information. PINS closed on Friday at 27.45 so the analysts will need to drop their ratings from buy to hold or raise their price targets.

Here’s what the analysts are saying:

June 28th: Wells Fargo analyst Ken Gawrelski upgraded Pinterest (PINS) to Overweight from Equal Weight with a price target of $34, up from $23. The analyst says the company's Amazon (AMZN) partnership going live ahead of the 2023 holidays, improving engagement trends and higher advertising load will allow Pinterest to deliver "accelerating and above-consensus" revenue growth. The firm sees a "strong catalyst path" for the shares over the 12 months. Wells expects Pinterest's Q3 revenue guidance accelerating to low double digits versus 7% year-over-year in Q2 on impression growth accelerating, improving end-market trends and "Premiere Spotlight."

June 7th: Wells Fargo analyst Ken Gawrelski initiated coverage of Pinterest with an Equal Weight rating and $23 price target. The firm said Pinterest must drive deeper and more frequent user engagement and secure enhanced visibility into conversion attribution, either through native checkout or third-party retail media partnership. Either drives significant value unlock, the analyst tells investors in a research note.

June 2nd: Piper Sandler analyst Thomas Champion reiterates an Overweight rating on Pinterest (PINS) with a $31 price target after digging into the company's partnership with Amazon.com (AMZN). While details are limited on the partnership, "the construct is compelling," the analyst tells investors in a research note. The firm thinks the alliance should be "win-win" and sized the third party revenue opportunity for Pinterest at mid-single-digit upside in 2024 and higher in 2025. The opportunity could be "much larger" if Pinterest sees exposure to all Amazon advertisers, writes Piper. It thinks the partnership at its most basic level is for the purchase of third party ad sales via Amazon's demand-side platform. Amazon will take a cut of ad sales and in return Pinterest will reserve inventory for Amazon, the firm contends.

May 2nd: Loop Capital analyst Rob Sanderson lowered the firm's price target on Pinterest to $28 from $32 but keeps a Buy rating on the shares. The company reported a "solid" Q1 with "conservative" guidance, and the 19% decline in the stock price reflects a valuation reset on an expectations miss rather than fundamental concerns with the business, the analyst tells investors in a research note. Loop Capital adds that the uniqueness of the Pinterest platform and monetization opportunity has been "growing more visible to investors".

April 28th: Rosenblatt analyst Barton Crockett raised the firm's price target on Pinterest (PINS) to $27 from $26 and keeps a Neutral rating on the shares. The company's Q1 results were better than expected, but its Q2 guidance was "squishy," the analyst tells investors. The firm raises its price target on the stock because a new Amazon (AMZN) partnership looks "interesting," Rosenblatt says.

April 28th: BofA analyst Justin Post lowered the firm's price target on Pinterest to $29 from $30 and keeps a Neutral rating on the shares. While the company beat expectations on revenue, EBITDA and users in Q1, the Q2 outlook and ad deal "underwhelmed" and patience will be required, the analyst tells investors. The firm, which sees "near-term disappointment [and] long-term opportunity," is lowering its 2023 revenue and and EBITDA estimates by 2% and 6%, respectively.

April 28th: Credit Suisse lowered the firm's price target on Pinterest to $28 from $29 and keeps a Neutral rating on the shares following the Q1 results. Pinterest is executing well, but the macro environment is weighing down growth, the analyst tells investors in a research note.

April 28th: UBS analyst Lloyd Walmsley lowered the firm's price target on Pinterest (PINS) to $34 from $35 and keeps a Buy rating on the shares. While Pinterest's Q2 revenue outlook was slightly disappointing, the key story is partner monetization and continued progress on shopping functionality, which stands to improve both monetization and engagement, the analyst tells investors in a research note. The firm thinks the partnership with Amazon (AMZN) is likely to drive a step-function improvement in top line growth in 2024 at high incremental margins.

April 28th: RBC Capital analyst Brad Erickson lowered the firm's price target on Pinterest to $28 from $30 and keeps a Sector Perform rating on the shares. The company's Q1 report saw "disappointing" out-quarter commentary that overshadowed the management's ongoing bullishness around rising engagement and monetization, the analyst tells investors in a research note.

April 28th: Bernstein lowered the firm's price target on Pinterest to $23 from $28 and keeps a Market Perform rating on the shares. While the company said users were up, engagement was up even more, ad impressions were up even more than that in Q1, revenue growth was similar to last quarter, and expected to be the same next quarter in the mid-single-digits, with higher expenses, the analyst tells investors in a research note.

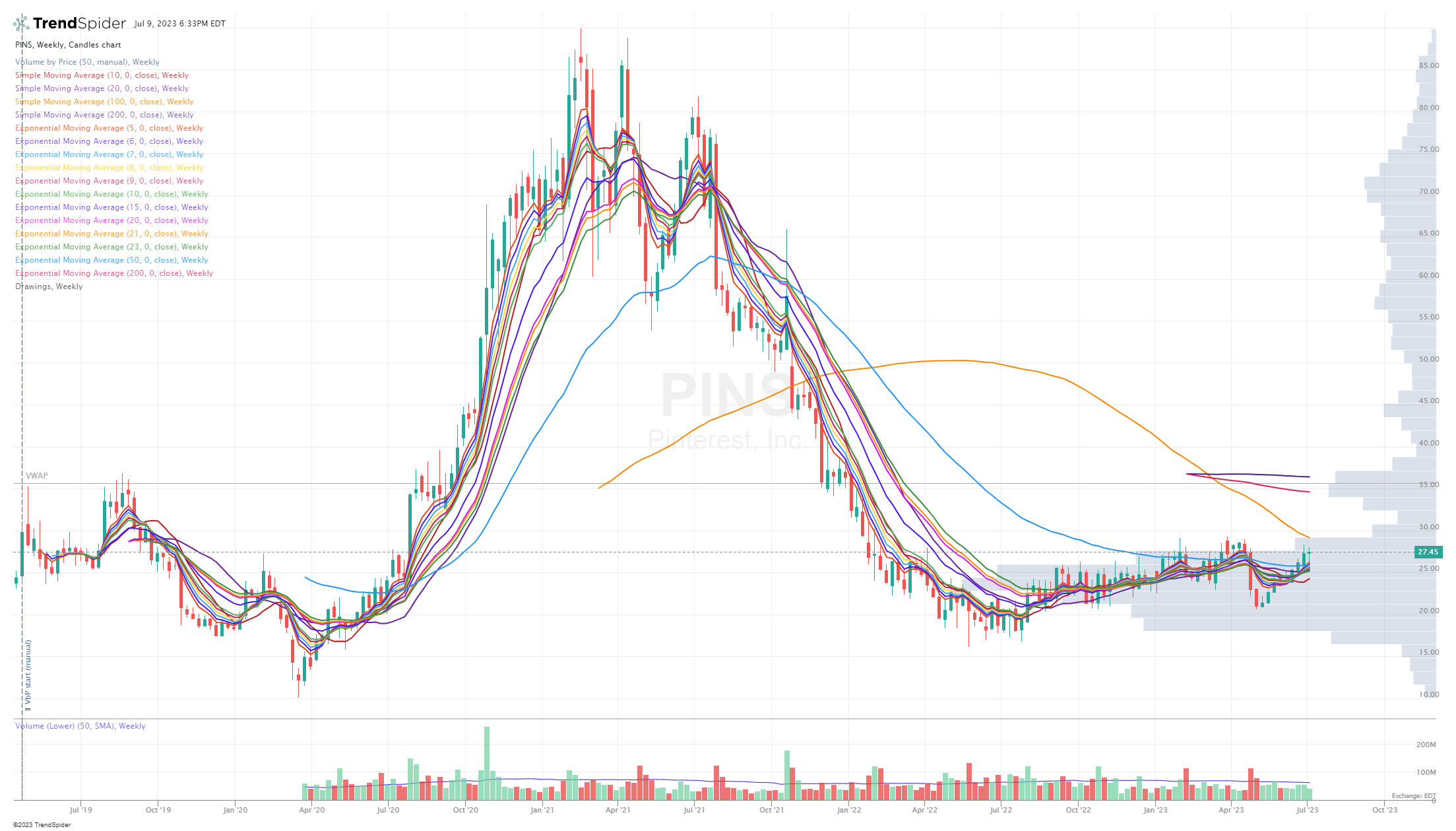

Technicals

As you can see from this weekly chart, PINS is back to where it was trading in mid-2019 despite revenues going from $1.14 billion in 2019 to $2.99 billion in 2023 (estimated). As we’ve discussed, revenue growth has really slowed which is major reason why the stock is still down 70% from the all time high. It’s possible that PINS gets back to that all time high of $89.90 but it could take another 10 years if they’re only growing revenues by high single digits or low double digits because there’s also a significant amount of dilution thanks to SBC. If they continue diluting the outstanding shares by 3-4% per year the share count in 10 years could be 40% higher than it is today which is approximately 300 million shares — this won’t be good for shareholders and will definitely be a drag on the stock’s performance.

I’m not ready to own PINS, for me to even consider a position I’d probably need the stock to pullback at least 20% and that might not happen unless Q2 earnings are bad and in that scenario it’s probably not a stock I’d find compelling.

If you’re looking to trade PINS, I think you can buy on a pullback to the 10d ema or 21/23d ema or wait for it to breakout above 29.29 — I’m certainly open to trading PINS, it’s just not investable in my opinion.

Conclusion

PINS is a solid company with an impressive userbase, the valuation has certainly gotten more interesting but I think there’s too many better companies to own with stronger fundamentals and cheaper valuations. It’s certainly possible that PINS surprises to the upside on revenues and/or margins but I’m not willing to make that bet.

There were rumors last year that PayPal (PYPL) was looking to acquire PINS which didn’t make a ton of sense to me however there are a few companies like Google and Amazon that might make more sense. Just hard to know if anything happens. I doubt any of those companies would want acquire PINS unless they thought they would accelerate both revenue growth and margin expansion.

There are very few platforms in the world that have 450+ million monthly active users like PINS which means each of those MAUs is worth approximately $6.60 of revenues in 2023. Now compare that to Facebook with 2.9 billion MAUs and Instagram with 2.35 billion MAUs, add them up and you get 5.25 billion MAUs and since META is expected to do $126 billion in revenues this year, it puts each of those MAUs at $24 per year — I’m not including WhatsApp or some of META’s other business groups (ie Reality Labs) so this is not an exact apples to apples comparison but my point is that META is probably monetizing their users 3x better than PINS but maybe that means there’s room for PINS to improve their monetization through ecommerce.

Additional Sources

Management – https://investor.pinterestinc.com/governance/Executive-profiles/default.aspx

Board of Directors – https://investor.pinterestinc.com/governance/board-of-directors/default.aspx

Ownership – https://www.sec.gov/Archives/edgar/data/1506293/000150629323000060/pins-20230412.htm#i1046ec6f9dfc4c4a95bdb1784da38721_1446 (page 64)

If you have any strong thoughts or opinions on PINS, please feel free to share them with me.

Since I’m not a user of their platform it’s very possible that I missed some key aspects/features that could contribute to the future success of PINS.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.