Part 1: Deep dive on Pinterest ($PINS)

Part 1: Deep dive on Pinterest ($PINS)

In order to read this entire deep dive on Pinterest (PINS) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 dives per month plus they get access to my current investment portfolio (up +86.09% YTD), all of my daily activity (buys, sells, trims, hedges), my investment models and my webcasts.

This is a screenshot of the YTD performance in my investment portfolio, taken on Friday after the market close. All paid subscribers have access to this portfolio.

Here are some of my other newsletters…

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus my daily commentary and morning newsletter.

Company: Pinterest

Ticker: (PINS)

Website: Pinterest.com

IPO date: April 18, 2019 (traditional IPO)

IPO price: $19.00

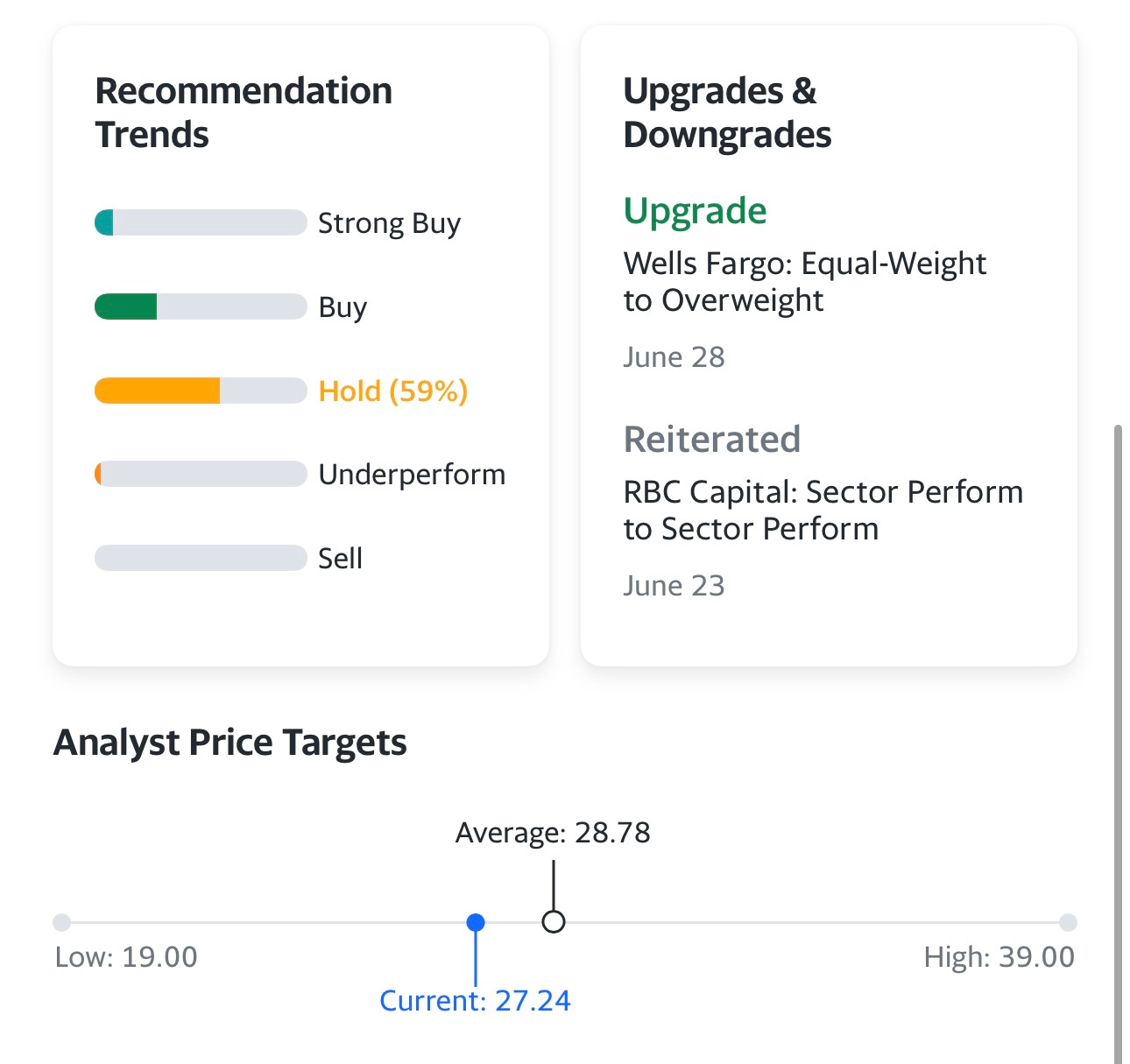

Stock price at the time of writing: $27.24

Outstanding shares: 683.7 million (594.3 million Class A and 89.4 million Class B)

52 week high: $29.27 on March 27, 2023

52 week low: $16.77 on July 26, 2022

ATH: $89.90 on February 16, 2021

Market cap: $18.624 billion

Net cash/debt: +$2.57 billion

Enterprise value: $16.054 billion

Headquarters: San Francisco, California, United States

Number of employees: ~4,000

Average price target from analysts: $28.78

Next earnings call (Q2 2023): N/A

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Q1 2023 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

Below the paywall is part 1 of the Pinterest (PINS) deep along along with links to my investment portfolio (up 86% YTD), investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Weekly webcasts [click here]

Introduction

Disclosure: I do not have a position in PINS (investment portfolio) and I don’t see myself starting one anytime soon. I do have a PINS position in my trading portfolio which I started today when the stock bounced off the 5d ema however my stop loss is below the 6d ema so I could be out of that position within the next few days.

Even though PINS is still down 70% from the all time high in February 2021, I still don’t think the current valuation is attractive because the growth has really slowed down. If we go back 4 years… PINS grew revenues by 51.2% in 2019, 48.1% in 2021 and 52.3% in 2022 which is why the stock went up 290% from the IPO to the peak of the bull market for growth stocks but since then it’s a complete disaster.

I did own PINS during the pandemic because the userbase was growing rapidly and those users were spending significantly more time on the platform. However, once the pandemic ended the daily usage started to drop and now the YoY revenue growth is in the single digits and is expected to grow low double digits for the next 3-5 years. The only two things that could get me into PINS would be meaningful revenue acceleration and meaningful margin expansion — I don’t expect either of these to happen so I’ll be sitting on the sidelines for now.

If I’m going to buy a stock that is only growing revenues in the teens, they better have 40-50% net income margins like INMD with low SBC so they’ll be compounding profits and doing big stock buybacks. PINS is generate free cash low ($532 million expected in 2023) however they also have very high SBC ($567 million over the last 12 months) which basically wipes out the FCF.

It’s very impressive that PINS has 463+ million monthly active users but the user growth has gotten stagnant and the company has been unable to increase monetization. They did bring in a new CEO last year who used to run ecommerce at Google so it’s possible we see PINS continue pushing harder into new revenue channels including ecommerce but I’ll need to see more evidence that it’s working because I got bullish on the stock.

FWIW, based on my investment model using the current analyst estimates, I’m just not seeing enough upside over the next 3-4 years to justify a position. I’m looking for stocks that have 100-150% upside or more over the next 3-5 years and PINS doesn’t meet that criteria. Even if the stock dropped 50% from here it might not be any cheaper or more attractive because in that scenario it probably means they missed the estimates and the fundamentals are getting worse, not better.

I’d love to own a social media company but none of them are attractive at current prices. LinkedIn is owned by Microsoft. Twitter is owned by Elon Musk. Facebook/Meta is up 225% in the past 8 months. SNAP has some of the worst SBC and insider selling that I have ever seen. PINS has single digit growth with high SBC. It’s very frustrating because social media has become a major part of our lives yet none of these stocks look compelling to me. I’d rather buy more CELH, UBER, LNTH, FOUR, GLBE, etc!!!!

I will say PINS has a decent chance of surprising investors and analysts to the upside if they can better integrate ecommerce and affiliate links into the Pinterest platform. FWIW, I don’t know a single guy that uses Pinterest but there’s nothing wrong with that. It’s always been a platform that appealed more towards women and gave them a place to find inspiration, recipes, interior designs, travel ideas, etc.

Currently, 75-80% of Pinterest users are female and I don’t see that changing anytime soon. If PINS could find a way to attract more males it would probably be good for revenues but I’m not sure what they could do to make that happen. Men have different hobbies and interests when it comes to spending time online and PINS doesn’t appeal to most of them, including me. I still have a hard time understanding the purpose behind PINS and why some people choose to use it so frequently.

Not only has growth slowed while SBC remained high but the founders still have a lot of voting power. It doesn’t feel like PINS is a shareholder friendly company which is another reason I don’t find the stock attractive at these prices. They do have $2.5 billion of net cash on the balance sheet but I’m not sure what they’re planning to do with it — I don’t think a stock buyback would be the best use of capital because it doesn’t fix their (lack of) growth problem.

Company Background

Pinterest was launched in 2010 by three co-founders, Ben Silbermann (who stepped down as a CEO in June 2022 but still serves as executive chairman of the board of directors and holds approximately 5.6% of the company and 32% voting power), Evan Sharp (who served as a Chief Design & Creative Officer until October 2021 and now serves as an advisor to the company), and Paul Sciarra (who does not work in the company at any role but holds similar 5.6% and 32% voting power to Ben Silbermann), as a visual discovery platform for finding ideas like recipes, home inspiration, and fashion looks.

Pinterest co-founders Ben Silbermann (in the middle), Evan Sharp (in the right), and Paul Sciarra (in the left)

Pinterest came out of Cold Brew Labs, a startup incubator with a focus on social commerce applications launched by Paul Sciarra and Ben Silbermann. It was initially an experimental project, but it quickly gained traction.

Originally, Pinterest was in closed beta and accessible on an invitation-only basis. During this period, the social cataloging platform reached over 17,000 registered users and almost one million 'pins.' Pins are bookmarks people use to save content they love on Pinterest, like images, videos, or products.

Pinterest was first available as a web-only website before launching an iPhone app in 2011. That same year, the platform exited the invite-only mode and began gaining the attention of a much larger audience. The company also got recognized by Time as one of the "50 Best Websites of 2011" and won the Best New Startup of 2011 at the TechCrunch Crunchies Awards. At the end of 2011, Pinterest joined the list of top 10 social websites in the world.

By 2013, Pinterest had evolved into one of the major players in the social media space and became a household name. The user growth was exponential, from one million in 2011 to 49 million in 2013. Pinterest broke the all-time record (at that time) to reach 10 million users the fastest.

Until 2014, Pinterest did not generate a single penny when the company introduced "Promoted Pins," allowing advertisers to pay to appear in search results and category feeds with their pins. This was the company's first monetization effort.

In 2016, Pinterest introduced "Shopping Ads" in an effort to increase monetization, which eventually started the company's long-going shift from an ad-only to an ad-and-commerce platform.

In early 2019, the company secretly filed for an IPO. In April of that year, Pinterest became a public company, raising around $1.4 billion at an approximately $12.7 billion valuation. The stock began its first day of trading at $19 per share before closing at $24.40 (+28%).

By the time of the IPO, Pinterest had generated $756 million (in 2018, up 60% compared to the year prior) and reported a net loss of just $63 million, eyeing profitability for the first time in its history.

The first and only (yet) profitable year came in 2021 after a huge boost Pinterest received in the second half of 2020 and the first half of 2021 (with Q2 2021 seeing a record 125% YoY growth). The pandemic caused a significant rise in the usage of Pinterest, as individuals sought inspiration and ideas online during lockdowns.

At its peak in 2021, Pinterest's shares reached almost $90 per share. But since then, the stock has fallen dramatically, more than three-fold. So did the business. From a high-growth company in 2021, Pinterest suddenly turned into a mature-like company with mid-single digits growth.

Pinterest's double-digit revenue growth of a minimum of 50% YoY started to slow down, first to 20% in Q4 2021, then to 8.6% in Q2 2022, before reaching just 3.61% in Q4 2022.

Yes, 2022 has seen a number of headwinds, the most notable one being the weak ad market. However, the problems at Pinterest were forming much earlier.

Ben Silbermann got increasingly criticized not only for constantly missing quarterly user growth expectations but also for a number of workplace complaints by his employees.

But, perhaps, the number one reason why Silbermann stepped down as the company's CEO was his poor execution of user monetization. Pinterest has historically been bad at monetizing its user base, so changes were needed eventually. They began with the appointment of the new CEO.

Bill Ready, ex-president of Google Commerce & Payments and ex-CEO of Venmo and Braintree prior to their acquisitions by PayPal, joined Pinterest in June 2022. After his appointment, the company changed the entire C-level.

New management essentially continued Pinterest's ongoing transformation to more of a commerce platform, but more aggressively and with one critical change: a pivot from transaction to shopping directly, which provides better monetization.

"When comparing the ad model vs. commission model, the ad model performs better. Most commission-based platforms effectively moved to an ad model. Most content you now see on these platforms is sponsored. They still have commissions, but they are the floor of the auction. Auction is outperforming because if you have just commissions, you either overprice or underprice." – Bill Ready said at the J.P. Morgan Global Technology, Media, and Communications Conference in May 2023.

His vision is now to connect the consumer with the retailer, deepening user engagement. The latter became the forming idea of the new strategy.

Additionally, when Bill Ready joined the company, there was a huge acceleration in expenses. He immediately implemented cost control, paused hiring (and also made a 4% reduction in the workforce), and slowed infrastructure spending. Most recently, the company reduced its real estate footprint by downsizing or completely closing several of its offices around the globe. Pinterest's focus shifted more to efficiency with the goal of reaching profitability.

While it is early to say if Pinterest has passed the inflection point (revenue growth is still below mid-single digit, expenses are still growing, and profitability is moving further and further away from the company), but the company is undeniably sitting on a tremendous opportunity to capitalize on its more than 460 million monthly active users that seek to get inspired by new products to buy they don't know about yet.

"We’re confident that the intent-based shopping mindset that our users bring when they come to Pinterest, coupled with improvements in shopping on the platform and our conversion-based ads business will bode well for advertisers in the long term." – said Bill Ready in Q1 2023 earnings call.

Opportunity

Trends

Pinterest is benefiting from several trends in both commerce and entertainment that should aid in the growth of its user base and revenue generation for years to come.

Below are the most notable trends that will profoundly impact the company.

Social shopping

Pinterest has really never been a social network but rather a community-curated catalog of inspirational content. But, in recent years, Pinterest has been actively transforming into a commerce platform with more emphasis on shoppable content.

Social shopping, which refers to when consumers' shopping experience occurs directly on a social media platform (shoppable posts, in-app checkout, product tagging in images and videos, and even storefronts), has been a trend for some time. Insider Intelligence estimated that about half of all US adults made a purchase via social media in 2021.

While social shopping is growing in the US, it is already the primary way users purchase products online in China. For example, WeChat, the country's most popular app, allows merchants to host virtual storefronts on its platform, acting as a one-stop shop for ecommerce.

Within social shopping, the discovery of products is a critical component. People increasingly turn to social platforms to discover new trends and products. Furthermore, since all social platforms collect a wealth of data on users' preferences and behaviors (know users better than they think they know themselves), they can provide a deeply personalized shopping experience with a high chance of matching with the right product at the right time and lead to completing the purchase.

Social commerce will remain the main driver of ecommerce growth globally and will become an integral part of every social platform, new or old.

Gen-Z

Generation Z (born between 1997 and 2012) will represent the largest consumer group in the US by 2026, with approximately 82 million people. This group is fast approaching the workforce and gaining significant purchasing power.

Gen Z is the first generation in human history that is digitally native, almost from birth. They grew up with smartphones, using social networks from a very early age, and tend to stay highly active there (from following trends to influencing their peers) ever since.

It is also ubiquitous for this group to shop online, making them a key demographic for ecommerce businesses. And because Gen Zs trust influencers and user-generated content more than any other demographic group, they will likely engage with social commerce more often.

Gen Z customers represent long-term value for any business, making winning their loyalty as early as possible the most critical goal that will define success for many years. Pinterest is no exception in understanding this. Gen Z users have already become the platform's fastest-growing demographic, and the company is heavily investing in capturing them further.

Short videos

The short video format has taken social media by storm, primarily thanks to the popularity of TikTok. Short videos have become a significant trend in online shopping as well. Often referred to as "shoppable videos," this format has changed the way how consumers discover and buy products.

Short videos offer a more engaging and immersive shopping experience than static images. They can display a product in action, emphasize its features, and demonstrate its use, providing potential customers with a better understanding of the product. This added layer of detail can be the deciding factor for customers who are on the fence about making a purchase. Ultimately, short videos lead to higher conversion rates and more satisfied customers.

Short videos are also an essential part of influencer marketing. Influencers use them to showcase products and inspire their followers, leading to an increase in product visibility and sales.

Pinterest has embraced the trend of short videos and integrated them into its platform's core experience. Users can now upload videos directly to the platform to showcase products in action, provide tutorials, and share other engaging content. This includes Story Pins (similar to Instagram Stories, Snapchat Stories, or TikTok Stories) that allow creators to tell dynamic, visual stories with videos, images, and text overlays.

Pinterest also made video content shoppable, allowing businesses to tag their products directly in their Video Pins or Story Pins.

Short videos are a huge growth tailwind for Pinterest, as seen from the growth of video content on the platform (increased by almost 40% QoQ in Q1 2023 compared to Q4 2022).

Conversion-based advertising

There is an ongoing trend in moving from impression-based advertising (the number of times an ad is shown, regardless of whether the viewer interacts with the ad or not) to conversion-based advertising (specific user actions or conversions like making a purchase).

Conversion-based advertising pays 5x (greater revenue potential) more than impression-based advertising, and it is the number one reason why most social platforms are pushing conversion-based ads. They are also easier to track and attribute with various tracking tools that social platforms now provide.

ML and AI further enable more precise targeting, increasing the chances that more and more users will convert (make a purchase).

Total Addressable Market

With the shift to social commerce, Pinterest now targets a much larger TAM.

In 2022, US social commerce sales reached $45.74 billion. Business Intelligence projects social commerce will be a $79.64 billion industry in the US by 2025. But it is only a small fraction of the worldwide opportunity.

A recent report from Accenture predicts global social commerce will grow 3x as fast as traditional ecommerce, more than doubling from $492 billion in 2021 to $1.2 trillion in 2025.

The main driver of such astonishing growth will be countries in the Asian region where social shopping becomes the primary way of buying things online.

Growth Drivers

Pinterest is focusing all of its efforts on driving better monetization, primarily by inserting commerce into its platform's core.

Unlike other social platforms that have an entertainment aspect, Pinterest has a commercial intent. In a commercial setting, Pinterest can have more ads as they are deemed more relevant and accepted by users. Having relevant ads also enhances the overall user experience.

Further are the main growth drivers that should accelerate Pinterest's revenue growth in the coming years and bring it from $2.8 billion in 2022 to over $4 billion by 2025.

Shopping

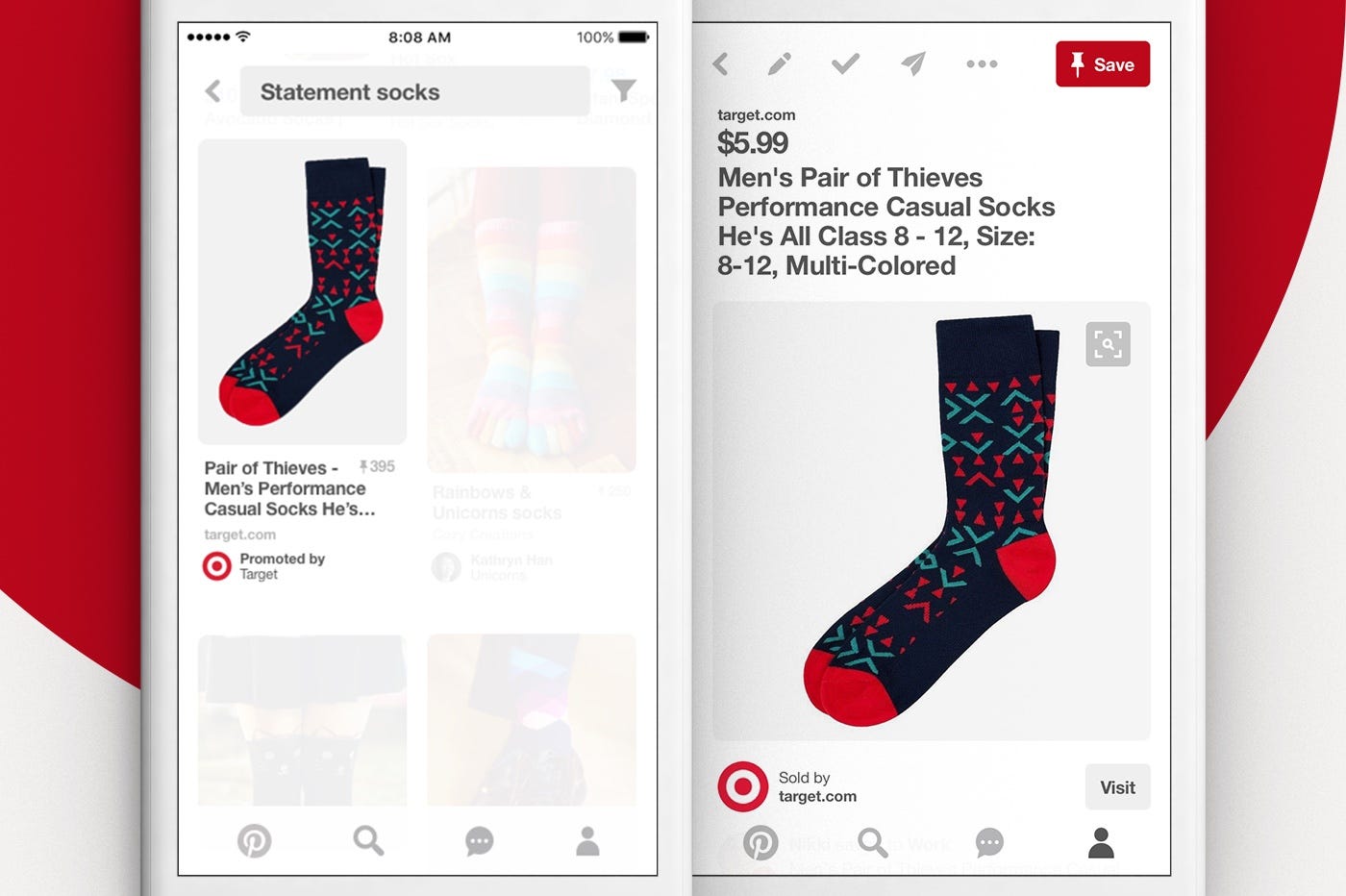

The biggest opportunity for Pinterest is to turn as much content as possible into shoppable content. As Bill Ready says, "Our mission now is to make every Pin shoppable." Shoppable content deepens engagement with users and ultimately drives more revenue as it pays much more than impression-based advertising.

The company has been unsuccessfully addressing shopping for many years. Most recently, shopping has been placed in a separate corner (section) in the app.

The shopping experience is absolutely critical for Pinterest. According to numerous surveys made by the company throughout the years, more than 50% of users on Pinterest are coming to the platform for shopping. However, historically actionability was very low. People find what they are looking for but cannot take much action on it. As Bill Ready said, “Pinterest offered a great digital window shopping but all stores were closed.”

So with the arrival of Bill Ready, the company has completely shifted its strategy and implemented a shopping experience in the core of the app (home page and search). Results started to come immediately, with engagement uplift by 35%+.

Retailers are now getting much more value from Pinterest's new strategy: they get a customer, not a transaction. This is a fundamentally different value proposition, which is a win-win for both retailers and Pinterest and something that significantly differentiates Pinterest from other social platforms. As a result, more and more retailers are now integrating the entire product catalogs into Pinterest.

“We've seen 35% plus increases in engagement on shoppable pins and 30% plus year-on-year increase in attributed checkouts for merchants who are uploading their catalogs to us.” – said Bill Ready in Q1 2023 earnings call.

Going forward, the company expects to see more slots on the page not only actionable (with links / mobile deep linking) but also paid (with high relevance to users). This is what the company calls “the whole page optimization.”

And the focus is on growing ad load in a way that enhances the users’ experience. Generally, the more ads social apps have, the more it annoys users, so the majority of social platforms have to trade off between ads and the experience. But Pinterest is a different story. The company can get users straight to the checkout when they click on the content, which is a completely different experience that most users will only support.

Moving to become a social shopping platform is ultimately the birth of Pinterest 2.0, which should eventually lead to higher engagement and better monetization.

Advertising

Advertising has been the core growth driver for Pinterest since its inception. Throughout the years, Pinterest has made significant efforts to improve its ad measurement features and demonstrate the value of its ads to advertisers, convincing them to invest more ad dollars in Pinterest.

From the recent developments, the company introduced its own first-party measurement tools. Currently, only ~10% of advertisers have adopted them, providing a massive opportunity for the company, giving the value these tools offer advertisers: those advertisers that have adopted the measurement tools see better outcomes (higher engagement and conversions. As a result, they spend, on average, 30% more on Pinterest ads.

To accelerate the adoption, the company has started hooking to larger platforms that advertisers already work with, like Amazon Advertising.

Pinterest was the only major ad platform not ingesting third-party demand. Other ad platforms have been complementing their auctions with third-party demand for a while. With the Amazon partnership announcement, Pinterest officially opened up third-party ad demand on its platform.

Amazon is the first deal for the company of many more to come. The choice of Amazon was obvious: Amazon has one of the greatest product catalogs and offers one of the best buying experiences. This partnership will bring more brands and relevant products to Pinterest.

The multi-quarter implementation is expected to begin rolling out later in 2023, and Pinterest's management plans to work with Amazon exclusively for a certain period before bringing in other partners.

International

While more than 50% of total monthly active users come from outside North America and Europe, Pinterest is either under-monetizing these users or not monetizing them at all.

There is a huge monetization gap between users from North America and users from the rest of the world, which provides Pinterest with a great revenue growth opportunity.

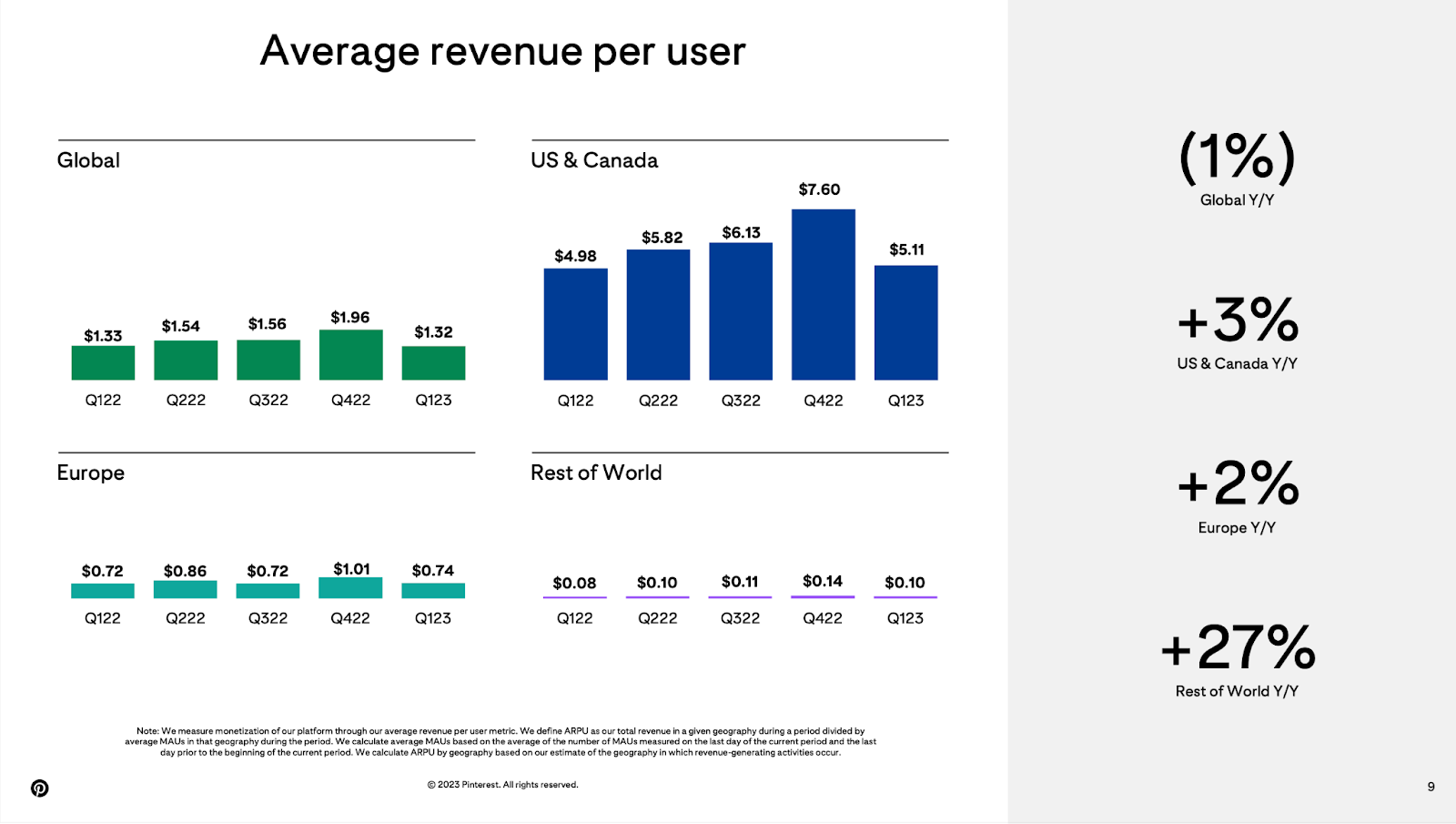

The average revenue per user (ARPU), which is the total revenue in a given geography during a period divided by the average of the number of MAUs in that geography), was $24.53 in North America in 2022. Compare this to just $0.43 ARPU in the Rest of World. One user in North America earns Pinterest the same amount as 57 users in the Rest of World.

While ARPU in the Rest of World is tiny compared to North America and Europe, it is growing faster than in any other region. In the most recent quarter, Q1 2023, the Rest of World ARPU increased 27% YoY compared to an increase of just 3% in North America and 2% in Europe. This resulted in a 38% YoY increase in revenue generated in the Rest of World, which remains in that range for many quarters in a row.

Bonus: TikTok ban

While it is yet uncertain whether TikTok will be banned in the US or not, but if it does – it will create an unexpected tailwind for Pinterest as many ad dollars will move elsewhere, and certainly, some will reach Pinterest.

Business Model

Pinterest operates an advertisement-based business model, where the company generates revenue by selling ads to users.

The company does not charge its users for accessing the platform or offer premium features. Pinterest also does not charge a commission for shoppable pins.

Revenue Streams

Pinterest currently has just one revenue stream coming from delivering ads on its website and mobile application.

Advertisers purchase ads directly with Pinterest or through various advertising agencies engaged in advertising on Pinterest on behalf of its clients.

Pinterest offers different ad formats, from static images to multi-image collections or videos:

Standard ads feature only one image;

Standard width video ads are videos that are the same size as a regular Pin;

Max. width video ads are videos that expand across people’s entire feed on mobile;

Carousel ads feature multiple images for users to swipe through;

Shopping ads feature one image at a time, allowing users to purchase products directly on Pinterest;

Collections ads appear as one main image above three smaller images in feeds on mobile devices;

Idea ads appear as a set of multiple videos, images, lists, and custom text in a single Pin.

Once the advertiser selects the ad format, the next step is to set a budget, timeline, targeting audience, and bids for the ads within the group.

Pinterest charges for user clicks on an ad contracted on a cost-per-click (CPC) basis, views of an ad contracted on a cost-per-thousand impressions (CPM) basis, and views of a video ad contracted on a cost-per-view (CPV) basis.

Although advertising is Pinterest's main source of revenue, the company has been striving to expand its revenue streams and improve its value proposition to businesses by creating and implementing new features and products. This has yet to transform into something meaningful, but the potential is there.

Gross Margin

The costs of running Pinterest primarily include the costs of hosting its website and mobile application, as well as personnel-related expenses (salaries, benefits, and share-based compensation) for employees in operations teams.

While the costs of hosting the platform are increasing due to higher compute utilization, Pinterest continues to enjoy a high gross margin, typical for SaaS companies.

The gross margin has been improving in the last five years, growing from 62.2% in 2017 to almost 80% in 2021. The gross margin in 2022 was lower at 75.9%, but the company is committed to meaningful margin expansion in 2023, actually more than the Wall Street consensus (200 bps vs. 100 bps).

Operating Expenses

Operating expenses remain high, almost 80% of total revenue.

While management promises to control costs while still accelerating the business, in Q1 2023, operating expenses were above 100% (112%) for the first time in many years.

Yes, the main contributor to these elevated expenses was restructuring charges ($117.3 million), but stock-based compensation continues to grow from quarter to quarter.

Profitability

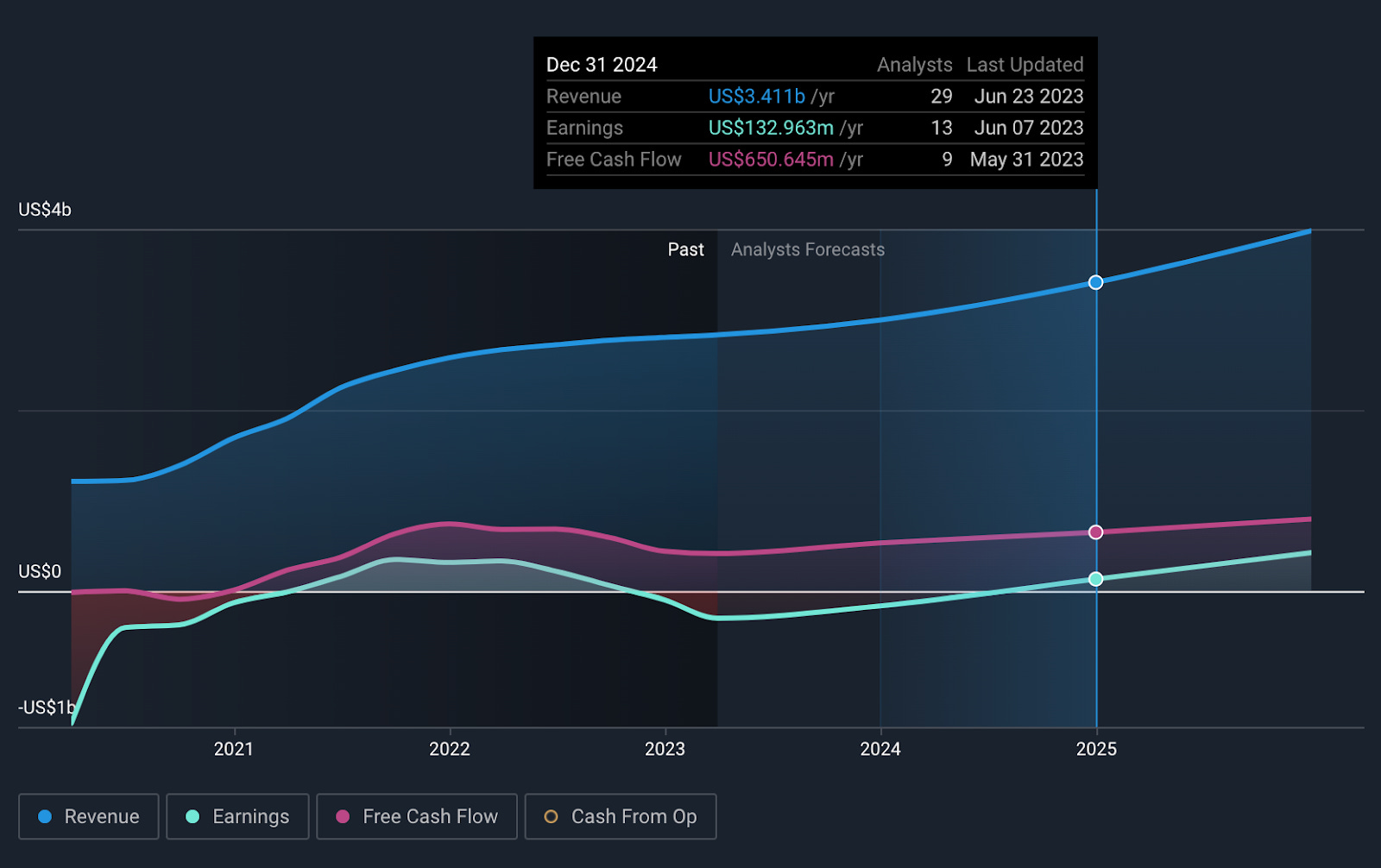

After an exceptionally successful 2021, when the company generated $316 million in net income with a 2% profit margin (the first and only year of positive earnings), it returned to being unprofitable (on a GAAP basis).

The current analysts' consensus is that Pinterest will keep running at a loss until 2024. The company must invest heavily in developing new features to address its shift to a social commerce platform. In addition, the company needs to significantly improve monetization in the international markets. Both efforts should ramp up by the end of 2024 and propel Pinterest to significant growth in earnings.

However, expenses keep growing and much faster than the top line. Until management sorts the cost control issue, Pinterest will further move away from becoming profitable again.

Stock-based compensation remains an issue for Pinterest. In Q1 2023, SBC was 23.75% of total revenue and 0.8% of the company's market cap, representing a 95% YoY increase compared to Q1 2022. SBC has been growing quarter-on-quarter for the past four quarters, eating profitability.

Since going public in 2019, the company increased the number of shares outstanding by almost 30% while the stock appreciated only by 7%.

Balance Sheet

Pinterest has an exceptionally strong balance sheet, with $2.7 billion in cash, cash equivalents and marketable securities, and no long-term debt. In addition, the company has access to a $400 million revolving credit facility.

The company has also begun share buybacks ($69.4 million in Q1 2023), indicating that management believes the current stock price is undervalued. As of Q1 2023, $428.4 million remains available for repurchases under the stock repurchase plan.

Cash Flow

The company's strong financial position is also supported by positive free cash flow. As of Q1 2023, Pinterest has generated $181 million in FCF.

Analysts expect the company to generate more than $500 million in FCF by the end of 2023 and continue growing it in double digits for the next several years.

*

Despite many headwinds that the company has been experiencing since the start of 2022, in a normal demand environment, Pinterest should be a highly profitable business.

The return to profitability is not far away for the company, but the cost control should be executed much better than it is now.

Competitive Advantages

Competition

Pinterest competes with various consumer internet companies that operate either as tools (search and ecommerce) or media (social networks, newsfeeds, and video platforms).

In the tools category, Pinterest primarily competes with:

Google is one of Pinterest's main competitors, as the majority of people use traditional search to discover ideas and products. Google is a major player in the search engine market and has one of the best advertising systems that further enhance its competitiveness. Additionally, Google has expanded its reach into ecommerce through Google Shopping.

Amazon is a major player in ecommerce and has a rapidly growing advertising empire that primarily serves sellers on its platform. Many people start their search directly on Amazon without visiting platforms like Pinterest or even search engines like Google.

Etsy is another major competitor in this category, and though it is significantly smaller than Google and Amazon, the platform's emphasis on one-of-a-kind and handcrafted items can appeal to the same users who look for inspiration and shopping suggestions on Pinterest.

In the media category, Pinterest principally competes with:

Meta (Facebook/Instagram) is the principal competitor with whom Pinterest competes for user attention and advertising dollars. Both platforms have rich shopping features.

TikTok, which has seen explosive growth in recent years, became a serious competitor with its short videos. This format proved to be extremely popular among the Gen-Z audience. TikTok is successfully driving advertising dollars away not only from Pinterest but from all major US-based social media companies.

Smaller companies in one or more of what management calls "high-value verticals" and which offer engaging content and commerce features. Among such companies are Allrecipes (a food-focused online social network), Houzz (provides the best experience for home renovation and design, as well as connects homeowners and home professionals with the best tools, resources, and vendors), and Tastemade (creates award-winning video content and original programming in the categories of Food, Travel, and Home & Design).

While engaging and retaining users, as well as attracting, retaining, and growing a base of creators and publishers, are important factors for which the companies compete, the primary aspect for which Pinterest competes for the most is advertisers and advertising budgets. Pinterest has enough users and content but not enough advertisers and budget spending.

Furthermore, while Pinterest's value proposition accurately sits between discovery/inspiration and shopping, which sets it apart from all other competitors, the lines are increasingly blurring as other platforms add new features (including ecommerce), which helps attract new users and advertisers. The competition is getting more and more intense every year.

Competitive Advantages

In the highly competitive landscape where Pinterest operates, establishing a distinctive advantage is a daunting task.

Pinterest does have a number of unique characteristics that define its platform and set it apart from all other platforms.

For example, Pinterest's user base predominantly comprises women, and many of them are in certain life stages, like planning a wedding, decorating a new home, or expecting a baby. They come to Pinterest specifically to look for ideas and discover products they intend to buy. Such a targeted demographic is of high value to advertisers.

Furthermore, Pinterest has a wealth of first-party data about its users, from their preferences to interests and habits. It makes Pinterest even more attractive for advertisers, especially in the post third-party cookies world.

Pinterest is also rapidly evolving into a platform that combines discovery and shopping. While other platforms all have ecommerce features, Pinterest seems to fully shift its focus toward ecommerce with the goal of making every piece of content shoppable. Shopping features have already been launched in 13 international markets, the catalog of products has doubled in the latest quarter, and seamless checkout with integrated payments is somewhere around the corner.

Another unique characteristic of Pinterest is the content on its platform. Unlike other social media, Pinterest is only about home decor, fashion, recipes, and other positive content. Unlike other social media, there is no news, politics, or personal opinions to be found.

This brings us to the point that, perhaps, Pinterest's real competitive advantage is its brand.

Brand

Pinterest has a reputation for being a positive online space where people come for inspiration, ideas, and shopping.

The company is very serious about moderating the content on its platform. It continuously battles misinformation and harmful content, rigorously deleting anything that is not relevant to its audience or could distrust users.

This positive environment attracts quality users that have a much deeper user engagement with the platform. In turn, it attracts quality advertisers that seek to build relationships with these users, making it a win-win situation for all parties, including Pinterest.

Pinterest is also quite conscious of user privacy protection. Most recently, the company made it mandatory for users to provide their birth dates to provide age-appropriate features and functionality. Pinterest is now private by default for existing and new users under the age of 16. Their content and profiles are not discoverable by others.

"Our investments in being a positive platform also make good business sense. As advertisers often side our positivity and brand safe environment as a reason for spending on the platform." – from Q1 2023 earnings call.

Maintaining a positive brand will be the company's main goal and one of the biggest challenges, but it is what provides it with the competitive advantage that no other company in this space can or will match.

Risks

Ad market

Pinterest generates substantially all of its revenue from advertising. Attracting more advertisers / expanding relationships with existing ones by getting more advertising dollars has been a challenge for the company in general and, more specifically, in the weak ad market in 2022.

Until the ad market recovers, Pinterest's revenues and growth perspectives will suffer significantly. Plus, the company needs to continue to invest in new tools and expand the sales force to increase the advertising budgets spend with its platform.

New management

While it is too early to evaluate the performance of the new CEO and his team (it's been only one year since the appointment), the market seems to grow impatient with not-so-impressive results during this period.

Plus, the company continues to make significant changes with the recent appointment of the new Chief Financial Officer in May 2023. The results are needed now, within the next few quarters maximum. It is still unclear if the new management is going to be able to deliver.

The US growth

Pinterest generates the majority of its revenue in the US. The user growth in this market has reached its pinnacle for some time. It is a reflection of Pinterest's high penetration within its target audience in this market, leaving no room for growth. Expanding competition does not make the situation any better.

Competition

Covered in more detail in the Competitive Advantages section, but competition remains a bottleneck for Pinterest, especially on the advertising front. Competing for ad dollars is getting harder and harder.

Plus, historically, advertisers were devoting a small portion of their advertising spend to Pinterest. While it is a huge opportunity for the company to increase this portion, it is also a high risk.

Monetization problems

Pinterest has been historically bad at monetizing its users. The company drastically needs not only to continue developing and offering effective products and tools for advertisers but also introduce new ways of monetizing its large user base. Depending on one revenue stream (which has its own set of risks) is a significant risk.

Brand reputation

Pinterest's reputation plays a crucial role. Any harm to its brand may cause losing advertisers at large. Pinterest, like no other, depends on maintaining its brand, which is capital-intensive and requires a lot of effort from the company.

International expansion

International growth is a large part of Pinterest's investment thesis. So far, growing revenues outside North America has been a huge problem for the company, despite showing promising growth rates. A lot of effort and capital will be needed to continue international expansion and revenue generation.

Voting power

The voting power is concentrated in the hands of the ex-CEO and co-founder, Benjamin Silbermann, and another co-founder, Paul Sciarra, who are no longer with the company in operational roles. There could be a significant conflict of interest between these two and the new CEO, Bill Ready, limiting the latter's decisions.

Acquisition target

Pinterest was rumored to be acquired several times in the past. Most recently, PayPal was reportedly ready to acquire Pinterest in 2022.

However, being down more than 70% from its all-time-high level in 2021, Pinterest (if that happens) may be sold at a much lower price than the majority of investors would anticipate.

Additional Sources

Management – https://investor.pinterestinc.com/governance/Executive-profiles/default.aspx

Board of Directors – https://investor.pinterestinc.com/governance/board-of-directors/default.aspx

Ownership – https://www.sec.gov/Archives/edgar/data/1506293/000150629323000060/pins-20230412.htm#i1046ec6f9dfc4c4a95bdb1784da38721_1446 (page 64)

As a reminder, you can track my investment portfolio, my daily activity and join my daily webcasts through this spreadsheet [click here]. Please let me know if you have any questions.

I’ll try to get part 2 out in the next couple days which should be easier with the holiday tomororw.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.