Part 2: Deep dive on Toast ($TOST)

In order to read this deep dive on Toast ($TOST) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support.

Paid subscribers receive ~3 deep dives per month (~8,000 words) and ~3 mini deep dives per month (~2,000 words) plus access to my current investment portfolio (up +129.7% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up +128.6% YTD) and my trading portfolio (up +96.4% YTD) including lots of activity updates, charts, market opinions, macro analysis, earnings analysis, analyst upgrades/downgrades, webcasts and much more.

Company: Toast

Ticker: (TOST)

Website:

https://pos.toasttab.com

IPO date: September 2021

IPO price: $40.00

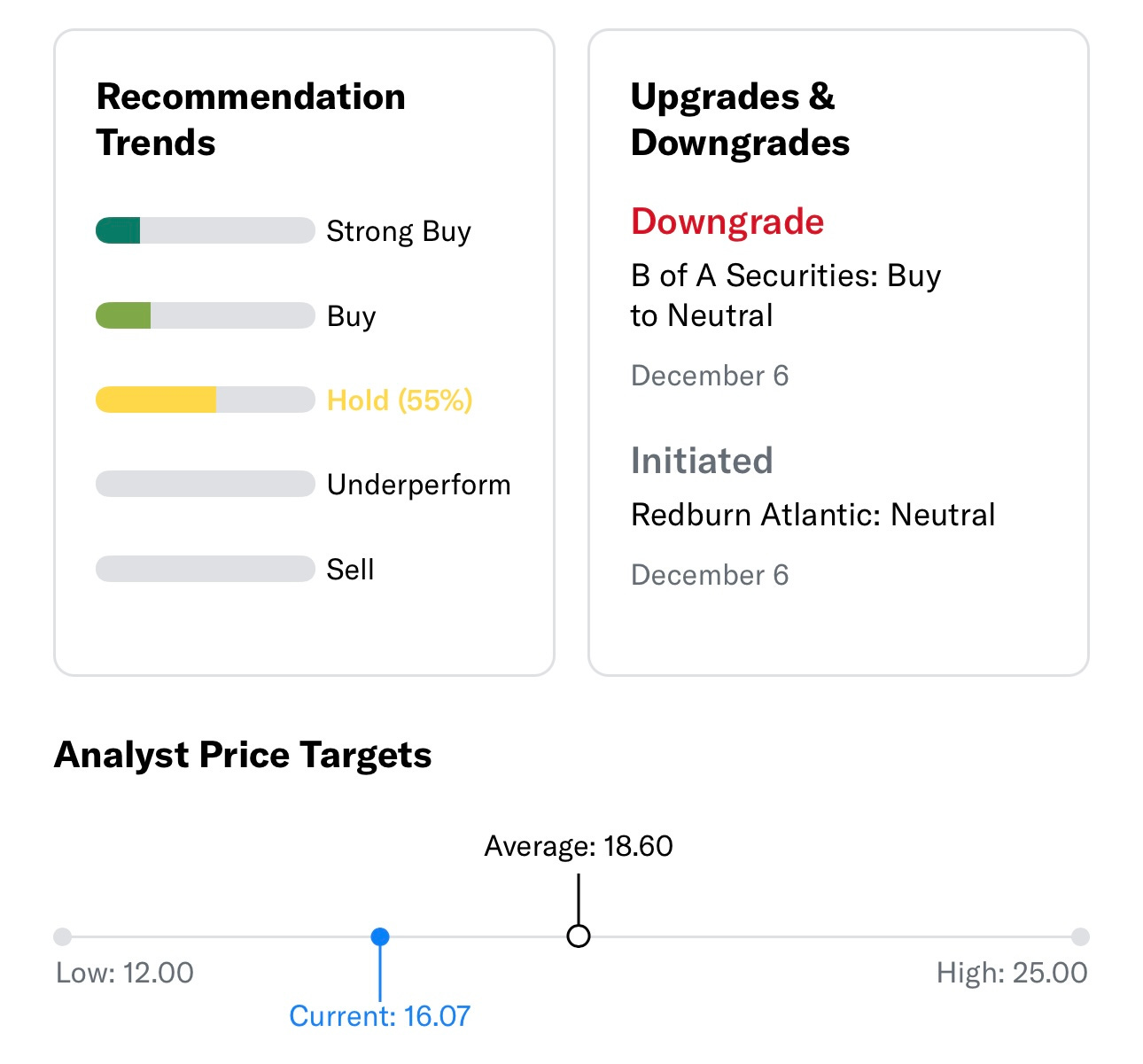

Current stock price: $16.07

Outstanding shares: 540.20 million

52 week high: $27.00 on July 18, 2023

52 week low: $13.77 on November 22, 2023

ATH: $69.93 on November 3, 2021

Market cap: $8.68 billion

Net cash/debt: $1 billion

Enterprise value: $7.68 billion

Headquarters: Boston, Massachusetts, United States

Number of employees: 4,500+

Average price target from analysts: $18.60

Part 1: Deep dive on Toast ($TOST)

In order to read this deep dive on Toast ($TOST) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive ~3 deep dives per month (~8,000 words) and ~3 mini deep dives per month (~2,000 words) plus access to my current investment portfolio (up +125% YTD), my investment models and my daily webcasts.

Investor Relations:

https://investors.toasttab.com

Q3 2023 Earnings Report: https://investors.toasttab.com/overview/default.aspx

Investor Presentation November 2023: https://s28.q4cdn.com/141746709/files/doc_financials/2023/q3/TOST-Investor-Presentation-Q3FY23.pdf

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

As a paid subscriber you have access to my:

Investment portfolio: https://docs.google.com/spreadsheets/d/1oqNvhyZH76EWdQPM7faTjqCthvskiNPNCOIEG295raE/edit#gid=0

Investment models: https://docs.google.com/spreadsheets/d/1kQnr_KNJVBXOdFb6fxWrpyQp4PpjE8wLjxTjqO3LJXQ/edit#gid=527845503

Daily webcasts: https://docs.google.com/spreadsheets/d/1oqNvhyZH76EWdQPM7faTjqCthvskiNPNCOIEG295raE/edit#gid=1687267844

My apologies for not sending out part 2 of this deep dive earlier this week, I just forgot. My next mini deep dive will be out today ($ONON) and my next full deep dive will be out tomorrow ($VTEX)

Introduction:

As I mentioned in part 1 of the TOST deep dive, I don’t currently have a position in TOST in either of my portfolios but it remains on my watchlist. I do think TOST looks compelling at these prices which is why I wanted to do this deep dive and learn more about the company. As you can see from my current investment portfolio [click here], I already have positions in FOUR and SQ so it’s unlikely I also need TOST also however FOUR is up +70% in the past 6 weeks and SQ is up +90% in the past 6 weeks so if I trimmed those positions perhaps I’d start a 1.5% position in TOST.

TOST is barely up in the past 6 weeks because of the disappointing Q3 earnings report which caused a 15-20% gap down. If you read the analyst notes below, most of them remain bullish on TOST and recommend buying the stock on any weakness. However, after the disappointing Q3 report several analysts did lower their price targets and changed their ratings from buy to hold.

FOUR spiked this past week on rumors that Global Payments ($GPN) might be looking to acquire them. If indeed FOUR gets acquired or goes private (which the CEO said is always possible) then I’d probably start a 2% position in TOST after I sold FOUR on the takeover pop since I don’t care about owning GPN (assuming it was a stock deal). Right now FOUR looks more attractive than TOST, both in terms of fundamentals and valuation. If FOUR gets acquired I’ll be very annoyed if it’s anything less than $100 because I think fair value is closer to $115. FOUR had been getting punished the past 6 months on fears about an incoming recession however now that inflation is coming down, the FOMC is on pause and no recession looks possible we’re seeing FOUR get re-rerated to a more appropriate multiple.

Personally I think TOST got hit too hard on the Q3 earnings miss and if you look out several years this stock has the potential to deliver strong returns for shareholders.

Even though Q3 was technically a miss for TOST, they still put up some impressive numbers including… ARR up 40% YoY to $1.2 billion, gross payment volume up 34% YoY to $33.7 billion and total locations up 34% YoY to 99,000

TOST obviously came public at a crazy valuation during a tech bubble in the markets but now that the stock is down 75% from the highs and the fundamentals remain strong with lots of room for margin expansion over the next 3-5 years, I think it’s finally time to start paying attention to TOST.

Valuation

When TOST was trading at the all time high in late 2021, it had a market cap of approximately $37 billion which means it was trading at 121x 2025 EBITDA, and now fast forward two years and the stock is trading at 26x 2025 EBITDA — I would say the current valuation makes a lot more sense.

Based on Friday’s closing price TOST has a current enterprise value of $8.1 billion, using this number and the consensus estimates below, here are the current multiples looking out to 2024 and 2025 since this year (2023) is over in less than 2 weeks:

1.67x 2024 EV/SALES

53.2x 2024 EV/EBITDA

53.6x 2024 EV/NET INCOME

40.9x 2024 EV/FCF

1.35x 2025 EV/SALES

26.5x 2025 EV/EBITDA

27.0x 2025 EV/NET INCOME

24.6x 2025 EV/FCF

If you’ve been reading my deep dives for the past couple years you know that I talk alot about PEG ratios and I try to stay away from stocks that have a PEG ratio above 1.5x which means if earnings are growing at 20% then the P/E should not be above 30x. In the case of TOST, they are expected to grow net income (aka earnings) by 273% in 2024 which clearly helps justify the stock at 53.6x 2024 net income, obviously this growth is not sustainable so looking out at 2025 when net income growth is expected to be 92% also helps justify the current P/E multiple and in fact you could see a little bit of multiple expansion especially with rates coming down and the economy remaining strong. If TOST can continue growing revenues by 20-30% per year for the next 4-5 years while expanding net income margins then the multiple won’t need to come down too quickly. Just look at the estimates below, if TOST is growing net income and non-GAAP EPS by 39.5% in 2027 then the stock could easily trade at 40x earnings would be $40 per share… and this doesn’t even account for their strong balance sheet which currently has $1 billion of net cash and will have even more cash (assuming no buybacks) in 2027, so add back the cash and you could have a $50 stock in 2027 based on these estimates below which is 3x or 200% from the current price.

Obviously the numbers below are just estimates and they will certainly change over time which is why it’s never “buy and hold” but instead “buy and continue to reassess”

Investment Model

Now we take the estimates from above (although I typically make them more linear for my models) and plug them into my spreadsheet to see where they might take us. Over the next 3-5 years, looking at the TARGET PRICE, I’m seeing some pretty decent upside potential while using P/E multiples inline with net income growth which implies a PEG ratio of around 1.0x which is very reasonable.

FWIW, the potential upside in this TOST investment model is almost identical to my FOUR investment model [click here] but considerably higher than my SQ investment model [click here].

With regards to TOST, the big gap down on Q3 earnings does make me nervous and I have a soft rule about not buying stocks after a gap down until we get to the next earnings report and they can earn back my trust however I’d consider breaking that rule for TOST if I decide to sell/trim FOUR and/or SQ because they get acquired or valuations get too rich.

Analysts

Overall I’d say the analysts are neutral on TOST; you can see below that the majority of them lowered their price targets back on November 8-10 which was right after the Q3 earnings report. There are still a handful of price targets in the low $20s but most of them are now $15-19 which doesn’t leave much upside from the current price. I think analysts and many investors are now in “wait and see” mode with TOST but sometimes that allows investors with a longer time horizon to jump in at great prices while everyone is a little scared.

Here’s what the analysts have been saying:

December 6th: As previously reported, BofA downgraded Toast (TOST) to Neutral from Buy with a price target of $16, down from $22. Shares have lagged significantly since the Q3 print, notes the analyst, who sees risks that could inhibit re-rating higher in the near-term. In addition to uncertain macro-driven restaurant spending trends, the firm believes Toast faces intensifying competition from the likes of Block (SQ), Fiserv's (FI) Clover, and Shift4 Payments (FOUR), who it says have been narrowing gaps in product and/or distribution.

December 6th:Redburn Atlantic initiated coverage of Toast with a Neutral rating and $18 price target. The analyst has positive views on the duration of the company's growth, but "cannot ignore the vast competitive landscape." Competition in the restaurant vertical from payment providers is intensifying, the analyst tells investors in a research note.

November 10th: Baird upgraded Toast to Outperform from Neutral with an unchanged price target of $18. While the stock "was a bit burnt to a crisp" on the Q3 earnings report, Baird appreciates Toast's "strong" growth profile, the analyst tells investors in a research note. The firm likes likes big market share gainers and says Toast is one of the best companies and products on its list. Baird expects 20%-25% revenue growth for several years.

November 8th: Piper Sandler analyst Clarke Jeffries downgraded Toast to Neutral from Overweight with a price target of $17, down from $27. The company reported a "healthy" Q3 but managements commentary suggests "degrading conditions," the analyst tells investors in a research note. The firm sees increased uncertainty on Toast's growth outlook based on descriptions of modest slowdowns in same-store transaction volume and moderating consumer spend. Piper believes it is prudent to lower revenue assumptions for next year and says the stock's risk/reward is "turning less attractive here."

November 8th: UBS lowered the firm's price target on Toast to $22 from $24 and keeps a Buy rating on the shares post the Q3 results. The company's revenue was in line, with little change to the fiscal 2023 guide due to macro conditions, the analyst tells investors in a research note. The firm says the shares appear attractively valued assuming moderate levels of success in Toast's international segment and path toward market leadership with U.S. restaurants.

November 8th: Needham lowered the firm's price target on Toast to $20 from $31 and keeps a Buy rating on the shares. The company's Q3 results were solid as revenue was in-line with consensus expectations and GPV strength, 6,500 location adds, and ARPU gains drove impressive recurring revenue growth, but the midpoint of the Q4 guide is below consensus and management called out some moderation in GPV per location due to tough macro conditions and increased mix shift towards smaller locations, the analyst tells investors in a research note.

November 8th: Morgan Stanley lowered the firm's price target on Toast to $22 from $28 and keeps an Overweight rating on the shares. While results in Q3 fell short of expectations and management acknowledged weaker GPV per location, the firm expects total ARR to grow at about a 30% CAGR to over $2B in two years from $1.2B today, the analyst tells investors in a post-earnings note.

November 8th: Canaccord analyst David Hynes lowered the firm's price target on Toast to $22 from $25 and keeps a Buy rating on the shares. The firm said despite its execution missteps they believe Toast is still a very well positioned business and the confidence in the opportunity ahead is not shaken. We would be buyers of Toast on weakness.

Technicals

This first chart shows TOST going back to the IPO and as you can see it’s a total disaster. TOST is down 75% from the all time high however it’s been building a base for ~18 months; still has some work to do but if it can clear the 200d sma at $19.20 it could rally up to the July 2023 highs at $27.00, once it pushes through that resistance there is lots of white space above for a bigger move into the $30s and $40s.

If you’re looking to invest in TOST long-term I’m not sure if it matters whether you get in at $14, $16, or $18 however if you’re trading the stock I’d probably buy it on a bounce off the 50d ema/sma (if it fills the gap from last week) or once it pushes through the 200d sma (just above $19.00).

Conclusion

Even though I don’t own TOST yet, I probably will at some point because I think the stock has been de-risked at these prices. I know investors are worried about competition, low margins and macro/recession which are all valid concerns and good reasons not to own a stock but we could use these same reasons for hundreds of other stocks that have done well over the past decade.

Every industry has tough competition, it’s up to TOST to differentiate themselves and provide a compelling value proposition to their customer however they’re never going to have much pricing power and margins will never be super juicy because this isn’t a pure software company. I think macro would be my biggest concern, for instance if the economy got much worse in 2024 and we entered a recession it would be very bad for a company like TOST in which case we see slower growth and lower profits which probably leads to multiple contraction so instead of TOST trading at 26x 2025 EBITDA, it’s more like 18x 2025 EBITDA

I do think 2024 has the potential to be a record setting year for M&A, therefore it’s always possible we see TOST get acquired as many industries need to consolidate with too many companies getting into pricing wars which isn’t good for any of them. If TOST can continue growing ARR/TPV by ~30% per year while expanding profit margins and keeping dilution at a reasonable level then I expect TOST’s stock price to be much higher in 3-5 years.

Please keep an eye on my investment portfolio so you’ll know if/when I start a position in TOST however even if I do I’ll probably use a stop loss so I know my max downside.

Additional Sources

Management / Board of Directors – https://pos.toasttab.com/leadership

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/1650164/000165016423000131/tost-20230424.htm#i879cb7f0bade441fb656fe524832d584_37 (page 60)

Have a great weekend!!!

~Jonah

You can follow me on Twitter [click here]

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.