Part 2: Deep dive on Sea Limited ($SE)

In order to read this entire deep dive on Sea Ltd ($SE) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (~100% YTD and ~1,000% over the past 3-years), my investment models and my daily webcasts.

I also run one of the largest Stocktwits rooms where I post about both about my investment portfolio and my trading portfolio with full access to both plus my daily activity, market commentary, webcasts and much more. Click the button below to signup with a free trial.

Here are some of my other newsletters…

Company: SEA Limited

Ticker: (SE)

Website: Sea.com

IPO date: October 20, 2017 (traditional IPO)

IPO price: $15

Current stock price: $62.74

Outstanding shares: 568.75 million (dual-class structure)

52 week high: $93.70 on August 11, 2022

52 week low: $40.67 on November 09, 2022

ATH: $372.70 on October 19, 2021

Market cap: $35.683 billion

Net cash/debt: +$2.071 billion

Enterprise value: $33.612 billion

Headquarters: Singapore

Number of employees: 64,000+

Average price target from analysts: $92.44

Next earnings call (Q2 2023): N/A

Investor Relations: https://www.sea.com/investor/home

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Q1 2023 Earnings Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, part 2]

Here is part 1 of the SE deep dive…

Below the paywall is part 2 of the Sea Ltd ($SE) deep dive along along with links to my investment portfolio (up ~100% YTD), investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

Just as a reminder, I still have a position in SE which I started a couple weeks. I felt like SE had been beaten down far enough so there’s now 100% or more upside within the next 3 years (perhaps sooner).

SE is still a low conviction name for me so I’m nervous about Q2 earnings which will be sometime in mid-August. When SE reported Q1 earnings on May 16th the stock fell 15% because they missed on revenues by ~$115M but they also referenced “near term macro uncertainty” so it’s possible those comments were a signal that Q2 and the rest of the year could be disappointing. Revenue growth at SE continues to slowdown so the only way this stock will generate substantial returns for investors (which for me is 100% in 3 years or less) is is they’re able to grow the top line by 10-20% per year while expanding net income margins to 15% or higher. If SE disappoints on margins than I don’t want to own the stock. If I still want ecommerce exposure I can look at SHOP (overvalued), MELI (I own it), or other names like CPNG, CHWY, BIGC or others.

From this secondary list of ecom names I think MELI is still the most attractive and remains a top 6 position for me. MELI has better growth, better margins and better management than SE, but MELI is up 44.3% YTD while SE is only up 17.6% YTD so I’m hoping SE can provide decent Q2 results and rally into year end. If I hold SE into earnings (still unsure about this) and they disappoint then I’d probably sell my position and put the money elsewhere.

Valuation

In part 1 of this writeup I provided a couple charts that showed how much multiple contraction SE has seen over the past couple years.

From the highs in 2021, SE’s EV/SALES multiple has gone from 25x NTM down to 2.4x NTM. From the highs in 2021, SE’s EV/GP multiple has gone from 120x LTM down to 6.2x LTM

All of this multiple contraction has happened while the stock price has dropped 84% over the past 20 months but none of that matters anymore because investors should only be looking forward so that’s what we’ll do now.

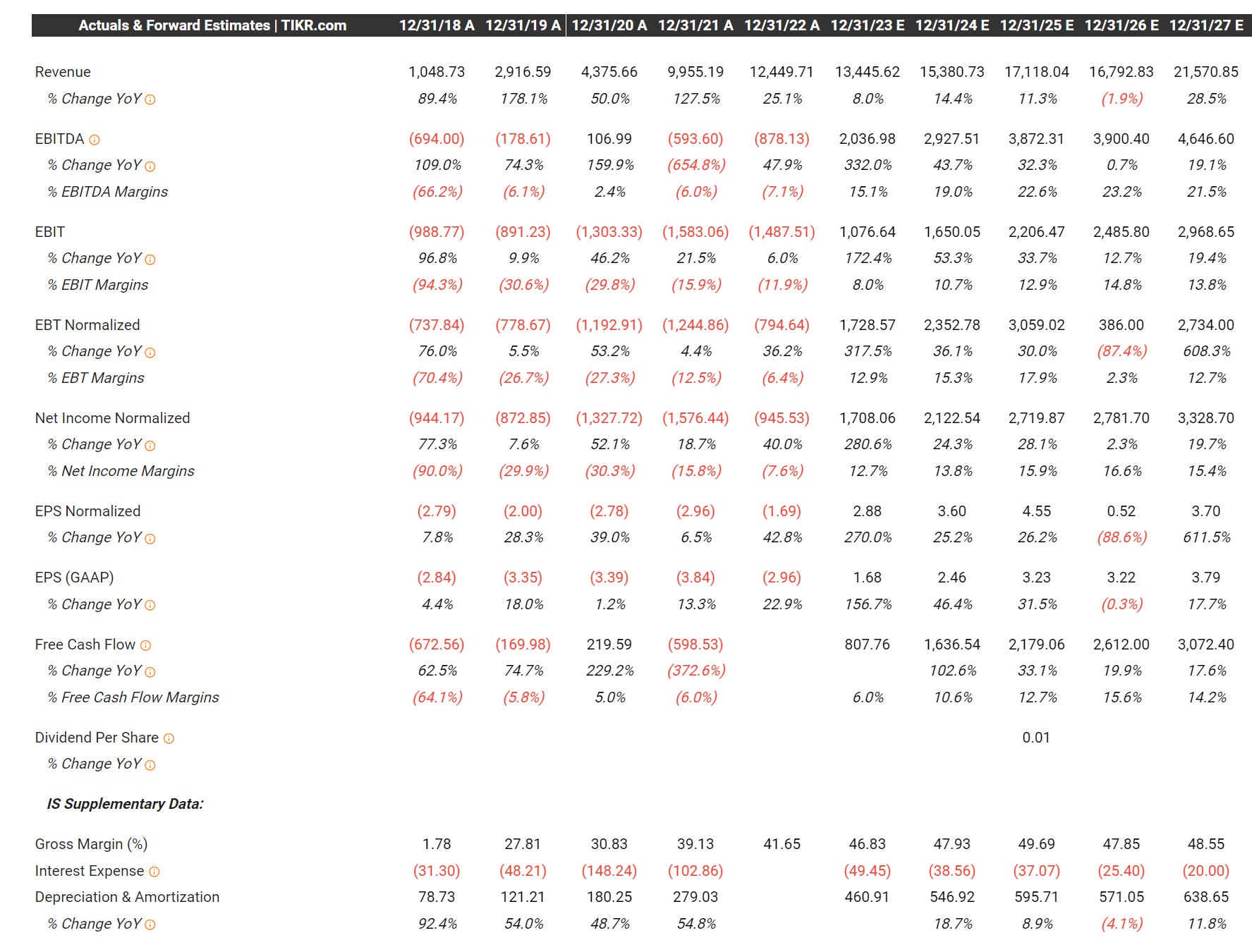

Using the current enterprise value of ~$33.6 billion and 2023 estimates, SE is now trading at 16.5x 2023 EV/EBITDA and 19.6x EV/NET INCOME — both of which seem very reasonable.

Using the current enterprise value of ~$33.6 billion and 2024 estimates, SE is now trading at 11.4x 2024 EV/EBITDA and 15.8x 2024 EV/NET INCOME — both seem reasonable.

It’s hard to know what SE will do in the short term so looking out over the next 18 months, let’s say they do $1750M of net income in 2023 and $2200M of net income in 2024, that’s 25.7% YoY growth, I think it’s fair to apply a 28x multiple to that number assuming that 2025 growth will look similar. If you apply a 28x multiple to $2200M, then add back the $2B of cash you get $63.6B which is 89.2% upside from here. I think that’s the potential over the next 18 months if almost everything goes right which is a combination of top line growth and bottom line margin expansion.

Investment Model

The purpose of my investment models is to look out 3-5 years which is what long-term investors should be doing. Like I’ve mentioned multiple times, SE is no longer the high-growth company that is was from 2017 through 2021 when revenues literally compounded at a 106% CAGR because now SE is a low double-digit grower which is fine as long as they’re expanding margins, keeping SBC low and then using those profits and FCF to reinvest in the business, make acquisitions, buyback stock, etc.

If SE can get to ~$20 billion oof revenues in 2026 with 15% net income margins (both of which might end up being slightly conservative) and we give the stock a 24x P/E multiple then we’re looking at 120% upside over the next 2-3 years. If revenue growth is better and/or margin expansion is higher than the upside over the next 2-3 years could be north of 150%. It’s also hard to predict what P/E multiple the market will pay for SE’s earnings, there are also lots micro and macro factors to consider and sometimes SE trades like a China stock which is certainly a risk.

I mentioned above that SE trades at 11.4x 2024 EV/EBITDA, as a comparison, SHOP trades at 118x 2024 EV/EBITDA. I will say that SHOP is growing faster but not by much. I’ll be surprised if SE doesn’t outperform SHOP over the next few years mostly because SE’s multiple is so much lower. It’s possible in 3-4 years that SE is still trading at 11.4x EBITDA but there’s no way SHOP will still be trading at 118x EBITDA.

I’ll say it again, SE needs to keep growing revenues at ~15% per year for the next 3-5 years with continued NIM expansion. If you’re really a long-term investor, I think there’s a decent chance SE gets to $5 billion of FCF by end of the decade, throw an 20x multiple on that, add back the cash and SE could have 250% upside over the next 6-7 years which would be a 22% CAGR.

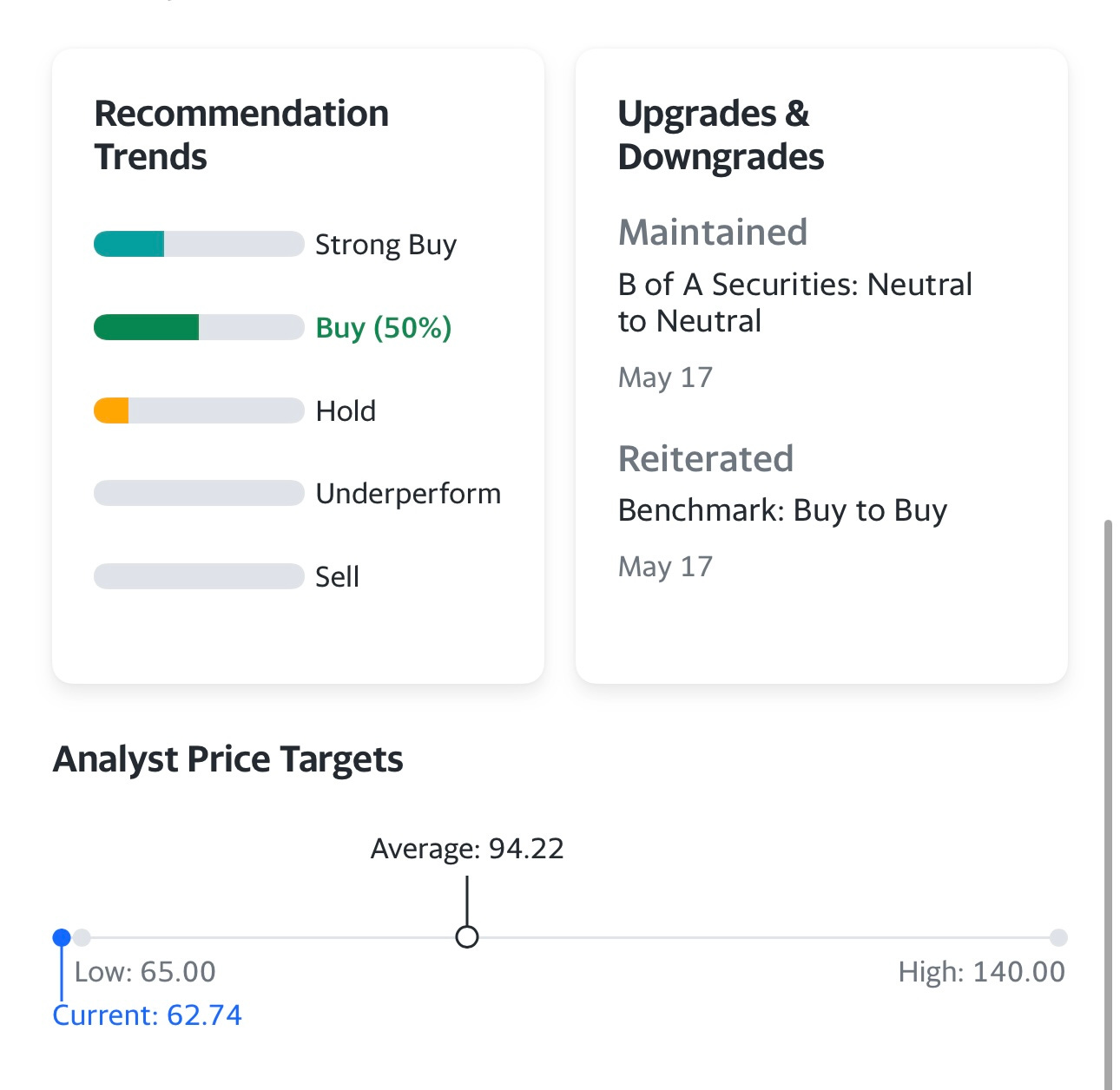

Analysts

If we went back 2 years, these same analysts had $300-400 price targets on SE but alot has changed since then, mostly grow rates falling off a cliff while the company was trying to expand across the globe and burning alot of cash. SE has pivoted into a more sustainable, profitable growth model but let’s see if they can stick to it and deliver what analysts and investors want to see.

Overall the analysts remain bullish at current prices with alot of buy/overweight rates and price targets in the $80-110 range for most of them. The average price target is $92-94 depending on which website you look at.

Here’s what the analysts have been saying…

June 22nd: DZ Bank reinstated coverage of Sea Limited with a Buy rating and $75 price target.

May 17th: BofA analyst Sachin Salgaonkar lowered the firm's price target on Sea Limited to $90 from $92 and keeps a Neutral rating on the shares following the company's Q1 revenue miss and EBITDA beat. The firm's sum-of-the-parts-based target moves lower following the Q1 report due mainly due to a cut in BofA's gaming estimates.

May 17th: HSBC analyst Piyush Choudhary raised the firm's price target on Sea Limited to $94 from $92 and keeps a Buy rating on the shares. The company's Q1 EBITDA came ahead of estimates, but a key concern is slower revenue growth, the analyst tells investors in a research note. However, the firm expects Sea's revenue growth to improve with higher growth at Shopee and game launches.

April 20th: Benchmark initiated coverage of Sea Limited with a Buy rating and $105 price target as part of the firm's industry launch of Southeast Asia e-commerce stocks. Sea is a leading platform player offering gaming via Garena, e-commerce via Shopee and fintech services through SeaMoney, the analyst tells investors in a research note. The firm's positive view is based on its belief that growth of Shopee and SeaMoney should continue to benefit from favorable structural factors and the "impressive delivery of profitability" in Q4, which it notes was one year ahead of its guided timeline.

April 20th: UBS analyst Navin Killa downgraded Sea Limited to Neutral from Buy with a price target of $92, down from $105. The analyst says competition is increasing in e-commerce and that the firm has no conviction on a gaming recovery. In addition, Sea is trading at premium valuation to peers despite slower near-term growth and competition headwinds, the analyst tells investors in a research note.

April 13th: Loop Capital analyst Rob Sanderson raised the firm's price target on Sea Limited to $88 from $62 and keeps a Hold rating on the shares. Ecommerce profitability has arrived much more quickly than was expected, driven by a jump in take rate, the closure of several loss-making growth initiatives and strong cost controls, the analyst tells investors in a research note. The firm's current forecast assumes that blended e-commerce take rate increases another 220bps in 2023 to 10.6% and 60bps in 2024 to 11.2%.

March 22nd: Bernstein analyst Venugopal Garre raised the firm's price target on Sea Limited to $100 from $80 and keeps an Outperform rating on the shares. The firm also revised estimates materially led by e-commerce business where it increased take rates, and gross profit margins and reduce S&M intensity. Bernstein, however, continues to see Gaming scale down but remains a business that offers option value for the future. Fintech profitability is improving as well, which the firm now factors into its model.

March 9th: BofA raised the firm's price target on Sea Limited to $92 from $68 and keeps a Neutral rating on the shares after the company reported Q4 results that beat the firm's as well as Street expectations. While management did not provide FY23 guidance, commentary remained "optimistic," said BofA, which adds that it remains watchful of the company's ability to maintain revenue growth with profitability. While its revenue estimates are largely unchanged, BofA has increased its EPS estimates for FY23/24E "materially" as the firm expects positive net income on an annual basis to be sustained.

March 8th: TD Cowen analyst John Blackledge raised the firm's price target on Sea Limited to $64 from $60 and keeps a Market Perform rating on the shares. The analyst said color around the 2023 outlook was limited with management citing near-term weakness in some markets and continued focus on efficiencies.

March 8th: Citi raised the firm's price target on Sea Limited to $110 from $105 and keeps a Buy rating on the shares. The company exited 2022 by reaching the profitability target for Shopee a year ahead of expectations, the analyst tells investors in a research note. The analyst citers faster growth and improved profitability for the target raise. Citi thinks regional investors will revisit the investment thesis for Sea with the prospect of "normalized growth yet healthier profitability."

March 8th: HSBC analyst Piyush Choudhary raised the firm's price target on Sea Limited to $92 from $87 and keeps a Buy rating on the shares post the Q4 results. The analyst expects Sea's EBITDA to "surge" to $3.3B by fiscal 2025 as margins expand at Shopee and SeaMoney. EBITDA increases by consensus would be a key catalyst for the stock, the analyst tells investors in a research note.

March 7th: Jefferies analyst Thomas Chong raised the firm's price target on Sea Limited to $115 from $104 and keeps a Buy rating on the shares. The firm said that Q4 revenue and earnings were head of consensus estimates and the firm's estimates. Jefferies added that improvement in take-rates and cost optimization drives fundamentals in the future.

Technicals

If you’ve been an SE shareholder the past two years; this chart has probably given you nightmares but hopefully the damage is in the past and now we move forward with a stock price and valuation that makes more sense given the current/expected fundamentals. SE is current stuck inside a large volume shelf with lots of overhead resistance so it will be a fight to get back to $90+ that will require a good Q2 earnings report and positive outlook/guidance. If Q2 disappoints it’s very possible SE revisits the recent lows in the $40s but there will always be those investors willing to overlook short term headwinds thus focusing on where this stock could be in 3-5 years. The question I’m still asking myself if whether I care more about revenue growth or profit margins.

FWIW, the 200w SMA is 125% higher from here which is where I think the stock can get to over the next 2-3 years. If SE goes from $61 (current price) to $135 (200w) over the next 2.5 years that would be a 37.5% CAGR which is just fine for me.

My goal is a 38% CAGR over the next 7 years which would 10x my portfolio again.

Conclusion

SE is definitely not the same company it was in 2020 when the stock was one of the best performers in the market. Back then investors were very undisciplined about valuations and didn’t spend enough time thinking about what would happens to multiples if/when growth started to slow down. This happened the most aggressively across cloud/ecommerce stocks (especially the unprofitable ones) with many of them dropping 70-90% but now some of them are starting to look attractive assuming growth has stabilized and margins still have room for improvement.

I have investment models for 8-10 ecommerce companies and SE (at current prices) remains one of the more attractive stocks in this group. CHWY is on my watchlist now, it’s down 70% from the ATH and could double from here over the next 3-4 years but their profit margins are truly “paper thin” which is what scares me. SHOP is way too expensive for me. W (Wayfair) is a mess in my opinion, they sell low quality products from too much suppliers and the customer experience is horrible. I can’t think of another publicly traded company that has pissed off more former customers than W (including me). CPNG is another one to watch but that’s also a margin story now with slowing growth. There are lots of smaller ecommerce companies like EBAY, OSTK (down 76% from ATH), BIGC (down 95% from ATH) but I don’t follow any of them close enough to have an opinion.

I keep wondering if BIGC could be an acquisition target, they are still losing money but expected to be profitable next year. BIGC currently trades at 2.3x 2024 EV/SALES versus SHOP at 10x 2024 EV/SALES.

Please pay attention to my investment portfolio spreadsheet over the next few weeks because there’s no guarantee I hold SE into Q2 earnings. I don’t like the stock reaction to Q1 earnings and companies that disappoint in Q1 are more likely to disappoint in Q2. Even if I’m bullish on SE over the next few years doesn’t mean I need to hold into earnings with no profit cushion. I’m also worried the markets will pullback during Q2 earnings season because so many stocks have run up the past 3-6 months and now valuations look stretched compared to where their fundamentals are. This isn’t necessarily true for SE but it’s true for many large components of the SPY and QQQ; if they pullback then everything is likely to pullback as well.

Here’s a webcast I did this morning with some of my thoughts going into Q2 earnings season plus a weekly recap of my portfolios… https://us06web.zoom.us/rec/share/a_7TR5FQJjaKSqASVjrsI0T18PkPo_lTbk7nPVHlhRFO629SXAUE1uI32koKC-IN.ioqMD9MWhNdJ-lOH

Let me know if you have any questions.

Additional Sources

Corporate Governance – https://www.sea.com/investor/corporategovernance

Ownership (note dual-class structure)

Have a great week!!!!

Don’t forget about my daily webcasts to follow along with my investment portfolio and/or trading portfolio. I typically cover my investment portfolio for the first 15-20 minutes and then my trading portfolio for the second 15-20 minutes. You can also ask questions through the chat feature.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.