Part 2: Deep dive on Palantir ($PLTR)

In order to read this deep dive writeup on Palantir (PLTR) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber, I appreciate your support.

Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +59% YTD), my daily activity (buys, sells, trims, adds plus hedges), my investment models and my daily webcasts.

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus you get my daily commentary and morning newsletter.

Company: Palantir

Ticker: (PLTR)

Website: Palantir.com

IPO date: September 30, 2020 (direct listing IPO)

IPO price: $10.00

Stock price when part 1 when out: $11.71

Outstanding shares: 2.118 billion

52 week high: $11.62 on August 05, 2022

52 week low: $5.84 on January 24, 2023

ATH: $45.00 on January 27, 2021

Market cap: $24.801 billion

Net cash/debt: +$2.566 billion

Enterprise value: $22.235 billion

Headquarters: Denver, Colorado, United States

Number of employees: 3,850

Average price target from analysts: $8.98

Next earnings call (Q2 2023): N/A

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Q1 2023 Earnings Call Presentation [click here]

May 2023 Letter To Shareholders [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1]

In case you missed part 1 of the Palantir deep dive writeup…

Below the paywall is part 2 of the Palantir (PLTR) writeup along with links to my investment portfolio, investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $200/year.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

Before I jump into the first section I want to give an update on my Palantir thoughts (and investment thesis) and why I don’t have a position yet. If you were watching PLTR this week you would have noticed that it was up another +16.5% from the close last Friday through the close today; PLTR is now up +43.6% in the past two weeks; and even more insane is that PLTR is up +87.5% from the lows on May 4th. I’ve been waiting for a pullback in PLTR but it just hasn’t happened.

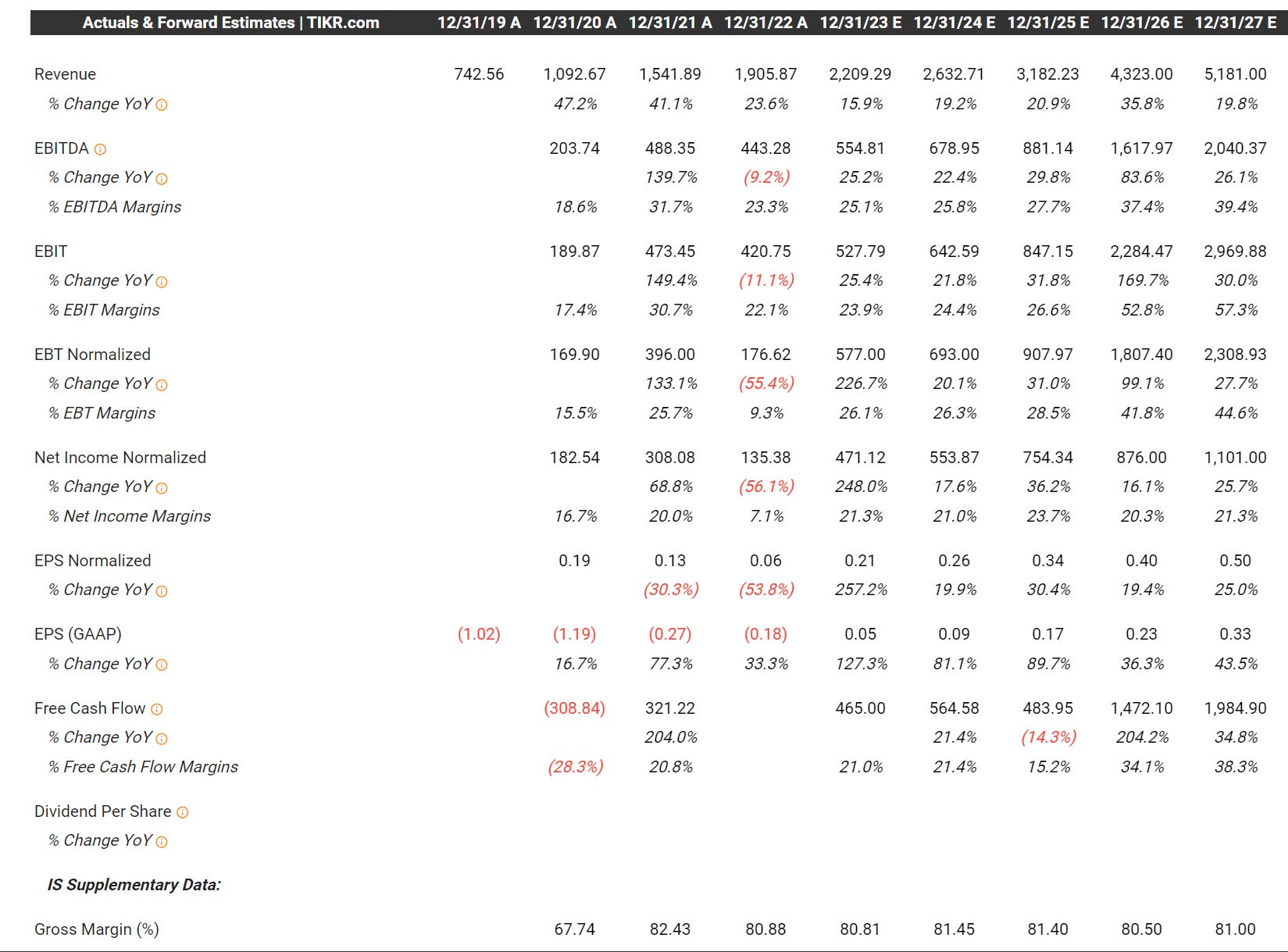

In my opinion PLTR is going up for no other reason than this AI hype that has taken over the markets. There was already alot of hype & hope coming into this week around AI but the blowout earnings from NVDA just made it that much more intense. It’s kind of crazy how many AI-related stocks were up 15% or more this week because of NVDA, even though they are not seen the same near-term impact to their revenues and earnings as NVDA is seeing because of the demand for their GPUs. I do think PLTR has the potential to be a winner in AI over the next 5-10 years but I’m not willing to chase the stock at these prices because the valuation is no longer reasonable and I just don’t see enough upside in the stock over the next 4-5 years compared to other companies that I follow or already own. PLTR was not a cheap stock a month ago and now the valuation is almost 90% higher even though analysts have not really changed their estimates for the next few years. Consensus is for $2.21 billion of revenues in 2023 and $5.18 billion of revenues in 2027 but even if you assume they can get to 21.5% net income margins in 2027 and throw a 30x multiple on the net income number and add back the cash it doesn’t provide an attractive CAGR from current prices.

Let me be clear, it’s certainly possible that PLTR continues to move higher on the AI hype but eventually valuation will matter and the company will need to justify the bigger valuation with better fundamentals and I’m not sure they can at which point the stock will come back to earth but that might not be for a while and perhaps they surprise us and start blowing out their quarterly earnings (which has not been standard practice for them up until now). With the AI hype and momentum surrounding these types of companies, I would not be surprised if PLTR rallied another 20-30% before finally pulling back but I’m not willing to chase it here because my investment models don’t justify it.

If you’re a trader or short term investor there’s a bunch of reasons (plus momentum) to own PLTR here but if you’re a long term investor I think you need to be cautious at these prices because there’s a lot of hype and hope priced into the current price (and valuation). Given NVDA’s blowout earnings report and their insane guidance for next quarter, the stock price jumping 25% was justified but PLTR is in a different boat — the stock is up 90% in the past month and nobody is expecting a massive upside beat to earnings anytime soon. PLTR has seen some huge multiple expansion without the fundamentals to back it up, maybe those fundamentals are coming in the future but they’re not here now. PLTR is now trading at 47.5x 2023 EV/EBITDA and 38.9x 2024 EV/EBITDA which are way too high given the current growth rates. Those multiples should probably be 30% lower unless PLTR ends up crushing the current estimates in which case this conversation is irrelevant the current multiples might be justified but even if that’s true it doesn’t mean there’s any meaningful upside in the near term based on anything other than hype & momentum around AI.

Valuation

I started talking valuations above but let’s dig a little deeper. Based on today’s closing price, PLTR has an enterprise value around $26.4 billion. Looking at the consensus estimates below, that means PLTR is trading at…

47.5x 2023 EV/EBITDA and 38.9x 2024 EV/EBITDA

56.1x 2023 EV/NET INCOME and 47.6x 2024 EV/NET INCOME

56.7x 2023 EV/FCF and 46.7x 2024 EV/NET INCOME

PLTR might be a great company and part of the AI revolution but the consensus estimates below simply don’t justify these multiples and valuations.

We’re almost into the 2nd half of 2023 when investors and analysts will start looking at 2024 numbers. If we look at 2024 net income, even if they beat that number by 20% and do $663M which would be 34% growth over 2023 (assuming they do $495M in 2023 which means a 5% beat to estimates), even if you give PLTR a 1.3x PEG ratio which means you’re applying a 44x multiple on $663M, that gives you $29.2B plus add back $3B of cash and you have $32.2B, divide that by 2.2B shares and you get $14.60 per share which is 7% above the current price which would be a very crappy ROI over the next 18 months. This is why I can’t buy PLTR at these prices for my investment portfolio however I’m still willing to own it in my trading portfolio because this AI craze is legit and just like we saw in 2020-2021, stocks can get very overhyped and overvalued in the short-term before it needs to adjust/correct for the actual fundamentals.

I really wish I had done my deep dive writeup 5-6 weeks ago when the stock was trading under $8.00 because I probably would have started a 2% position ahead of earnings.

I will say this… given the long-term potential of PLTR and their platforms for both government and commercial plus the AI-hype, I do expect the stock to trade with a premium multiple but 46.7x 2024 EV/NI is just too expensive for me unless I thought they’d beat the current 2024 consensus numbers by 40-50% and I don’t (at least not yet).

Investment Model

For the purposes of this investment model and trying to take a longer-term view, I wanted to make sure my 2027 revenue number was mostly inline with what the analysts are forecasting which is $5.18B but I ended up being a little more bullish/optimistic however even with my slightly higher numbers for both revenues and net income margins, when I apply a reasonable P/E multiple in 2025 and 2026… I’m simply not seeing much upside from current prices. With that said, if you want to value PLTR on FCF then you can build a better case for a higher stock price in 3-4 years however I just know if the market/investors will be willing to pay 45x FCF in 2025 or 41x FCF in 2026 even if FCF is growing that fast according to my model. I still think valuing companies on earnings (and net income) is most realistic. Focusing on FCF alone opens the door for disappointing returns over the next few years.

As you can see, SBC as a % of market cap has dropped to 2% which is much lower than it was a year ago or even back in December when the stock price was under $6. Dilution from SBC doesn’t look as bad as the stock price and market cap are increasing (assuming that SBC is increasing at a slower rate).

If you have any questions regarding this model please let me know.

Just like most of my investment models, I try to update them once a quarter as we get new data/guidance to work with but it’s very hard to predict where PLTR will be in 3-4 years for revenues and net income margins which is why these models are just a guide and other factors need to be considered.

Analysts

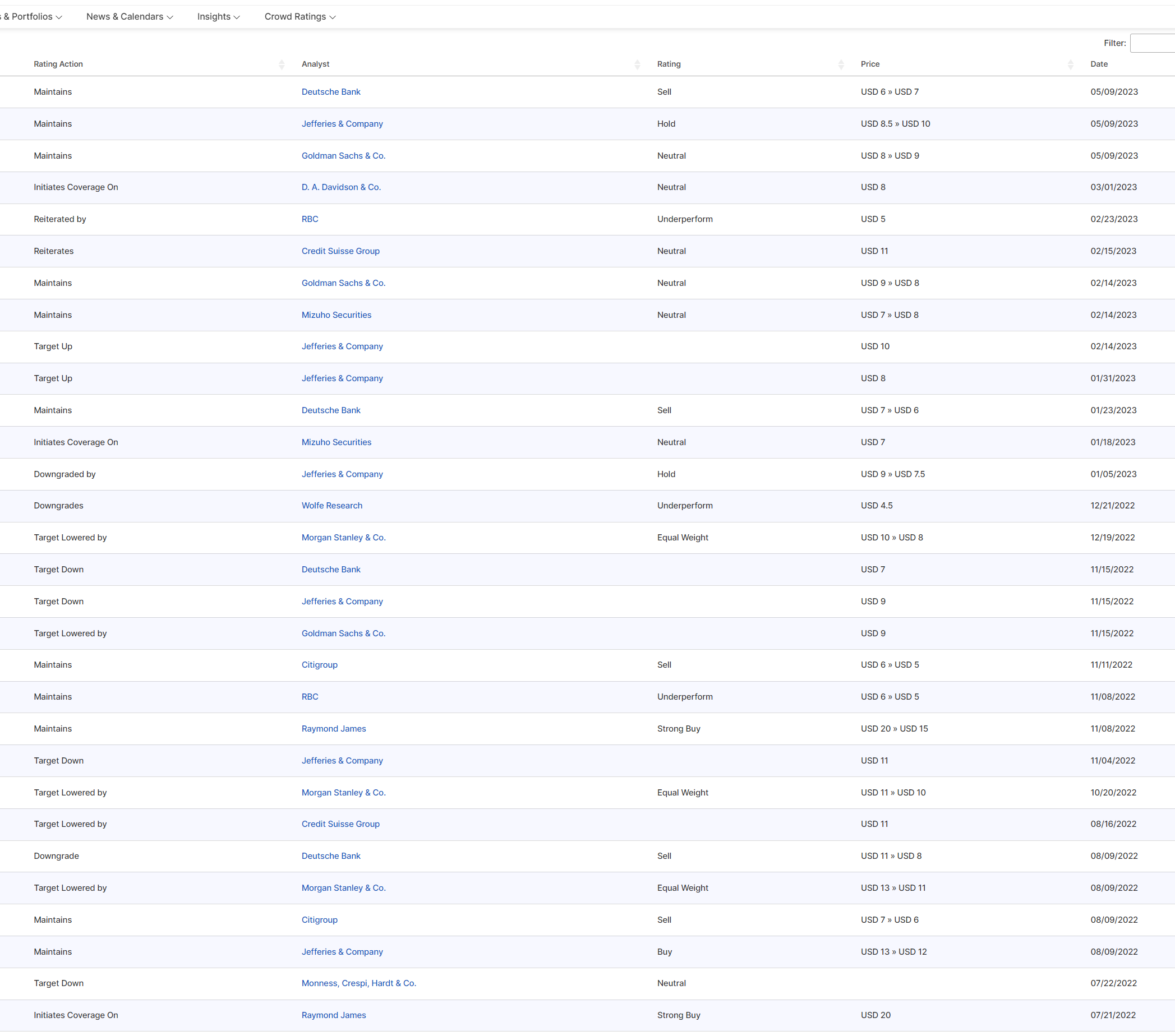

As far as I can tell (from several websites that I use), the average price target for PLTR is $8.98 which means if the stock price stays in the $12-14 range we could see a flurry of analysts raising their price targets but that’s not necessarily a good thing because if their current PT is $8-10 they might only raise it to $12-14 but then reiterate a hold or go from a buy to a hold. If the analysts are using the same numbers I was using above, there’s really no way they can justify a price target above $15 unless they’re also raising their 2023, 2024 and 2025 estimates. It’s kind of funny when you scroll down this list and go back to 2021 and see how many analysts had price targets in the $20s and $30s yet now those same analysts have price targets under $10.

Here’s what the analysts are saying…

May 23rd: Raymond James analyst Brian Gesuale removed Palantir from the firm's Analyst Current Favorites list while making no change to the firm's Strong Buy rating or $15 price target. The firm cites the recent appreciation and potential for non-core pressure on near-term trading for the removal from the ACF list.

May 9th: Deutsche Bank analyst Brad Zelnick raised the firm's price target on Palantir to $7 from $6 and keeps a Sell rating on the shares. The company reported Q1 results that were largely in line with revenue expectations and exceeded slightly on profitability when excluding the one-time revenue benefit, the analyst tells investors in a research note. However, the firm still believes Palantir is more a services company with reusable intellectual property versus a true software business and should therefore be valued accordingly.

May 9th: Jefferies analyst Brent Thill raised the firm's price target on Palantir to $10 from $8.50 and keeps a Hold rating on the shares post the Q1 results. Sentiment was too negative going into the print, and "better-than-feared" results led to the stock up 22% in after-hours, the analyst tells investors in a research note. The firm says record free cash flow in the quarter and positive GAAP operating income shows Palantir's continued commitment to profitability. However, despite the upbeat results and commentary, Jefferies believe investors will remain skeptical, given the continued slowdown in business fundamentals.

May 4th: Though shares of Palantir Technologies sold off post the Q4 results, the setup remains challenging with an "elevated" valuation versus peers and incremental commercial headwinds offsetting a more resilient government spending backdrop, Citi the analyst tells investors in a research note. With the company's fundamentals still under pressure, the firm expects limited upside to numbers in the quarter and updated outlook. It keeps a Sell rating on Palantir with a $5 price target.

March 27th: Last Tuesday, Space Systems Command, Los Angeles Air Force Base, announced that it awarded Palantir a three-month bridge extension, instead of a long-term renewal, on its Space Force data software services contract, which is Palantir's third-largest contract, William Blair analyst Louie DiPalma the analyst tells investors in a research note. And late Friday, Space Systems Command announced that it selected 17 other vendors along with Palantir for a five-year, $900M data analytics contract that builds upon the sole-sourced Palantir program, adds the analyst. The firm says there is risk that Palantir's growth for the program will be limited as the Space Force "splits the pie among the numerous vendors." Over the long term, there is the potential for the same type of migration off of the Palantir platform that took place with the Raven program and is taking place for the FDA's CDER program, contends Blair. The firm sees risk that Palantir's "premium 8.5-times sales multiple will compress as competition pressures revenue growth and profitability." It keeps an Underperform rating on the shares and sees downside to $4 and $5 in a "bear case scenario."

March 1st: DA Davidson initiated coverage of Palantir with a Neutral rating and $8 price target. The company possesses significant intellectual property, but its unique mission and focus may limit its opportunity and earnings visibility, the analyst tells investors in a research note. The firm added that the complex, service-intensive nature of the Palantir product makes it very expensive, thus limiting the company's addressable market. DA Davidson further notes that government deals also tend to be "more lumpy", limiting visibility.

Technicals

This first chart shows PLTR back to their IPO, just wild the stock got to $45+ and even with the recent surge in the stock price it’s still down 70% from the all-time high but creeping up on the VWAP from the ATH which is currently at $16.84

This next chart is more interesting because if I was going to trade PLTR this is how I would approach it. The next level of resistance is that previous high at 14.85, if PLTR can push through there you could buy the breakout but now we’re talking really overextended stock so it’s also possible that PLTR gets rejected at 14.85 setting up a possible short. TBH I’m not a big short guy so it’s not the play I’d hoping for or looking for.

What I would love to see is PLTR pullback to 11.63 which is not only the high from last summer but also where we’d hit the uptrend line from the Sept high through the October high through the February high. Not only would you have support from the previous highs and uptrend line but I’m thinking the 21/23d ema would also be around that area if this happened in the next couple weeks.

Unfortunately I don’t think PLTR is investable right now but it’s certainly tradable if you can get the right entry price and manage your risk appropriately.

Conclusion

I have lots of close friends that own PLTR so I’m definitely cheering for them and the company but given the 80-90% increase in the stock price over the past month it’s just gotten too expensive for me based on the valuation and current estimates for 2023 and 2024. If you were buying PLTR the past 6 months under $8 than I’d consider taking some profits at these prices because I think the upside is going to be limited from here however there’s clearly alot of hype and momentum in the AI stocks so nothing would surprise me. For the past 10 minutes I’m been debating whether I think the next 30% for PLTR is higher or lower and I honestly can’t come up with an answer. Neither move would shock me but I think 30% higher would be more likely from these two choices because a 30% drop would take PLTR below $10 and I just don’t see that happening given all the tailwinds provided by that NVDA earnings report.

I really like what PLTR is going and I think they’ll be one of the most important software/technology companies over the next decade so it’s disappointing that the fundamentals aren’t better and the valuation isn’t lower. If just one of these was different I’d consider a position but I’m not willing to pay 47x 2024 net income (estimates) with revenue and earnings growth in the 20-30% range. There are dozens of companies growing faster while trading at lower multiples so that’s where my capital is going.

Additional Sources

Management – https://investors.palantir.com/governance/executive-management

Board of Directors – https://investors.palantir.com/governance/board-of-directors

Ownership – https://www.sec.gov/Archives/edgar/data/1321655/000132165523000033/pltr-20230425.htm#i37de48c0bdc8476ba5d62418ce323d50_160 (page 43}

As a reminder, you can track my investment portfolio, my daily activity and join my daily webcasts through this spreadsheet [click here]. Please let me know if you have any questions.

Have a wonderful holiday weekend!!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.