Part 1: Deep dive on Palantir ($PLTR)

In order to read this deep dive writeup on Palantir (PLTR) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber, I appreciate your support.

Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +54% YTD), my daily activity (buys, sells, trims, adds plus hedges), my investment models and my daily webcasts.

I’m also thinking about starting a private Twitter account for all my paid subscribers so we can interact in a more conversational format, share investment/trading ideas, discuss my recent writeups, etc.

In addition to my newsletters, I also run a Stocktwits room where I post about both of my portfolios/strategies (investment portfolio & trading portfolio) plus you get my daily commentary and morning newsletter.

Company: Palantir

Ticker: (PLTR)

Website: Palantir.com

IPO date: September 30, 2020 (direct listing IPO)

IPO price: $10.00

Current stock price: $11.71

Outstanding shares: 2.118 billion

52 week high: $11.62 on August 05, 2022

52 week low: $5.84 on January 24, 2023

ATH: $45.00 on January 27, 2021

Market cap: $24.801 billion

Net cash/debt: +$2.566 billion

Enterprise value: $22.235 billion

Headquarters: Denver, Colorado, United States

Number of employees: 3,850

Average price target from analysts: $8.98

Next earnings call (Q2 2023): N/A

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Q1 2023 Earnings Call Presentation [click here]

May 2023 Letter To Shareholders [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1]

Part 2 should be out in the next couple days.

Below the paywall is the full writeup on Palantir (PLTR) along with links to my investment portfolio, investment models and daily webcasts.

I hope you consider becoming a paid subscriber for just $20/month or $180/year (ie $15/month).

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

Introduction

Disclosure: I do not currently have any position in PLTR. I did start a position in my trading portfolio on 5/15 but sold it on 5/18 to lock in a 21.6% gain. I did own PLTR a couple years ago shortly after the IPO, if I remember correct I started a position around $12 and sold it around $28 but never got back into it and never did a writeup on the company until now.

Several weeks ago I decided it was finally time to do a writeup on PLTR because there are many things I like about the company not to mention it’s been a very popular stock with retail investors over the past 2-3 years. Knowing that PLTR was reporting earnings on May 8th I decided to wait until after earnings to send out the writeup just in case the stock tanked on earnings and presented a better buying opportunity for investors.

Unfortunately (or fortunately if you owned the stock in earnings), PLTR has done nothing but go up since earnings. As you can see from the chart below, PLTR is up 51.3% since they reported Q1 earnings just a couple weeks ago.

I do think it was a solid earnings report and the company is clearly most focused on profitability than they ever have been before but there’s no way that report was good enough to justify a 50% move in the stock. I think investors now believe that PLTR is another way to play the AI revolution that has been the hottest trend/conversation for the past few months amongst investors.

Over the past couple months I have been considering a position in PLTR because I felt the valuation was finally getting reasonable and they had a decent chance at beating current estimates over the next few years which includes better margins but there’s no way I’m chasing the stock at these prices in my investment portfolio. Now, my trading portfolio is a different story which I’ll get into more in part 1 (technicals section) but I’m more than happy to trade PLTR off the technicals but I can’t get excited about the current valuation after the recent move which means the stock is now trading at 40x 2024 EV/NI (net income). The only way I could justify buying PLTR at $11.79 per share is if I thought they’d do $700M+ of net income next year which means the stock would only be trading at 30x 2024 EV/NI right now and $700M next year on top of ~$480 this year would be 45% NI growth so paying 30x 2024 EV/NI would give me ~50% upside over the next 18 months. Unfortunately I don’t have confidence they can do $700M+ of net income this year so I’ll sit on the sidelines for now and wait for a pullback in the stock price. If the indexes/markets start to selloff over the next few months and I get a chance to buy PLTR under $10 then I’d probably do it. I do think there’s a decent chance that PLTR doubles from here over the next 3 years but they’ll need to get to $4.3B+ of revenues in 2026 with 28-30% FCF margins.

One of the main reasons I’ve stayed away from PLTR the past 18 months (in addition to slowing revenues) is the SBC situation aka stock based compensation. It’s certainly gotten better in recent quarters compared to the first 18 months after the IPO but as you can see from the chart below, the dilution since the IPO is horrendous. Technically the company does have enough cash to buyback 10% of the float but that’s a slap in the face to shareholders that would prefer to see PLTR use that cash to invest in future growth prospects. I’m sure I could think of a few companies that have grown their share count faster than PLTR over the past 2.5 years but PLTR is still at the top of the list (and not a good list to be on).

I’m definitely no Palantir expert compared to many of the retail investors that have owned the stock since the IPO, rode it up to $45 and then back down to ~$6 before the recent rally back to ~$12. There are entire podcasts, twitter accounts and online communities dedicated to Palantir shareholders where members share all sorts of news, updates, analysis, etc on the company. Outside of Tesla, Berkshire, Costco, Apple, Nvidia, Sofi and a few others, I’m not sure there’s a more passionate, diehard shareholder base (amongst retail investors) than Palantir (or at least that’s the way it looks to me). Even though some of those diehard Palantir shareholders can provide alot of great information on the company, products, growth strategy, etc… they are extremely biased and have ignored many red flags over the past couple years like slowing growth, excessive dilution and frothy valuation but maybe things are starting to change and a possible investment thesis is emerging — but I still think the stock needs to pullback and consolidate in the $10.50 range where I’d consider a started position with the expectation of averaging down into a bigger position under $10.00 because I do think PLTR will be one of the largest and most important global software/analytics companies over the next 10+ years.

I’m going to have more thoughts/comments on PLTR in part 2 of this writeup which should be out in the next day or two. Now that earnings season is almost over I should have more free time during the day to catch up on writing and researching.

If you have any strong opinions on Palantir (good or bad) please feel free to share them with me.

Company Background

Palantir was founded back in 2003 by a group of people led by a Silicon Valley legend, Peter Thiel, who was one of the original co-founders of PayPal. The idea for Palantir came about right after PayPal was sold to eBay in 2002. On the back of 9/11, Thiel wanted to use the fraud recognition software specially designed for PayPal to combat terrorist attacks.

In 2004, Thiel (who owns nearly 8% of the company and still serves as a Chairman of the Board) hired Joe Lonsdale and Stephen Cohen (who owns about 1.4% of the company and serves as President and Secretary), two Stanford computer science graduates, and one of the PayPal engineers, Nathan Gettings, to create a minimum viable product. Thiel fully funded Palantir at its early stage.

However, in the very beginning, no one was taking Palantir seriously, neither outside investors nor potential customers. The team was struggling to make any progress until the company was joined by Alex Karp (who still acts as a CEO and owns approximately 4% of the company).

Karp changed everything for Palantir. While he did not have any technical background (he studied philosophy at the University of Frankfurt), Karp was able to understand Palantir's complex technology right away and pitch it to some angel investors from Europe he knew from his days working in asset management.

But investors from the US were still not taking Palantir seriously. After a while, some connections helped to get an introduction to the In-Q-Tel venture fund, the CIA’s venture arm, which ended up investing just a bit more than $2 million in the company in 2005.

CIA was not just the first outside investor but the first and only Palantir's customer for more than three years before other government organizations (like Homeland Security, the FBI, the Center for Disease Control, and the Air Force, among other at least ten organizations) also started to use its software.

For many years Palantir was secretive about what they were doing. The public knew it was helping intelligence and law enforcement organizations analyze massive data sets to help combat terrorism and crime. Palantir was turning massive lakes of siloed information into visualized maps, histograms, and charts to help detect abnormal objects or behaviors.

But in 2010, the company made a decision to go after the commercial market and open up more for the public. JPMorgan became Palantir's first commercial customer, implementing its software to help battle the bank’s fraud problems.

Since then, the company has expanded into other industries to help various organizations quickly implement solutions to the most challenging problems they face, from anti-money laundering and solving complex supply chains to enabling connectivity across the health data ecosystem and improving network stability, visibility, and reliability.

Palantir has even built entirely new platforms like Skywise (in collaboration with Airbus), which has become the central operating system of the airline industry.

Karp kept saying that Palantir won't go public as it would make "running a company like ours very difficult." However, in 2020, amid the roaring market, Palantir filed for an IPO.

Most analysts have been quite skeptical about the company and its valuation, questioning whether Palantir is more of a government consulting firm focused primarily on defense rather than a true software company.

The valuation was indeed high. Palantir became public in September 2020 through a direct listing (it did not raise any money but allowed existing investors to sell the shares to the public) with a reference price of $7.25 per share. Shares began trading at $10, bringing the valuation to over $21 billion.

The market appetite for high-growth software companies skyrocketed Palantir's shares by almost 300% during the pandemic. At an all-time high level, when the stock price reached $39 per share, the company was at 33 times forward-looking revenue, which was two times more than the average multiple in the SaaS industry.

Even with the uplift after strong Q1 2023 earnings, the company is still trading below the IPO price, down 80%+ from the all-time high. The primary reason is that the company has been unprofitable for almost 20 years. It is also shareholder unfriendly, having been diluting its shareholders with continuously elevated stock-based compensation.

But in Q4 2022, Palantir seemed to reach an inflection point. It was the first-ever quarter in the company's history with a GAAP net income of almost $31 million. Though this profit came from a non-cash gain from its Japan joint venture (the company was still unprofitable at the operating level), it was a massive step for the company, which it confirmed again in Q1 2023, but this time with the GAAP operating income.

It is yet early to say if Palantir has started a new chapter in its history and that the GAAP profitability will be durable long-term, though it expects to deliver net income in every quarter in 2023, but what is certain is that management has finally heard the shareholders, changing its focus to slower but profitable growth (instead of growth at all cost) and continued management of its stock-based compensation (though it is still increasingly high).

With all of its controversies and increasing competition, Palantir still has one distinct advantage: it has built a name for itself in the government sector, where it has cemented itself as a go-to company for analyzing big data. This should not only attract new government contracts but also help the company win more businesses in the future.

Opportunity

Trends

There are several trends in favor of Palantir, some of which are secular (big data), while others are more short-term (war).

The big data trend has been around for a while. The vast amounts of structured and unstructured data generated from various sources require analyzing and extracting insights from this data. It has become increasingly important for all organizations, whether they are public, private, or non-profit.

The volume of data continues to grow exponentially. This data also comes in various formats, including text, images, videos, and sensor data, making it harder to manage and analyze it. To help cope with this task, more and more companies are doubling down on AI and ML.

Big data and machine learning actually go hand in hand. ML filters vast datasets to help discover patterns, make predictions and automate processes. AI further enables organizations to extract valuable insights from unstructured data sources like text, images, and videos. Combining AI and ML allows organizations to gain deeper and more accurate insights from their data.

Like any commercial organization, governments also generate data, actually vast amounts of it, and this data is most often siloed. Governments, more than ever, require effective data analysis and decision-making.

Their systematic failures to provide for the public, including fractured healthcare systems, erosions of data privacy, strained criminal justice systems, and outmoded ways of fighting wars, will continue to require both the public and private sectors to transform themselves through implementing new software solutions like the one provided by Palantir.

Right now, Western governments, especially the US, are heavily involved in the ongoing war between Russia and Ukraine. Palantir, which supplies Ukraine with its software, benefits from government support immensely, though Karp has been very cautious about it.

The elevated geopolitical tension between the US and China (and possible war in Taiwan) may bring even more demand from the government for Palantir's solutions in the short to mid-term.

Total Addressable Market (TAM)

Palantir's market opportunity is substantial, with or without ongoing wars. The company estimates its total addressable market to be approximately $119 billion across both the government and commercial sectors.

The government sector, including government agencies in the United States, its allies, and other countries abroad whose values align with liberal democracies, is estimated to be worth $63 billion a year (domestic is $26 billion and international is $37 billion).

In 2018, Palantir won a lawsuit against the US Army, forcing the federal government to consider commercially available software before attempting to build its own custom-made software. This has transformed how the US military purchases software for its soldiers and service members.

The court's ruling affected not only the military but also the entire US government. Now, software like Palantir can be funded through either information technology, operational, or other government budgets – a significant factor that enables Palantir to capture an even greater share of its government TAM.

Thus, the revenue from the US Army increased significantly since Palantir's victory in court. In ten years, from 2008 to 2018, the company generated $51.9 million in revenue. In less than two years since the ruling, the company almost tripled its revenue from these accounts.

The estimate for the commercial sector is $56 billion annually. But Palantir constantly expands its platform into new product categories, creating new use cases and increasing its potential customer base. Based on the data from International Data Corporation, the global spending on these product categories is more than $150 billion per year.

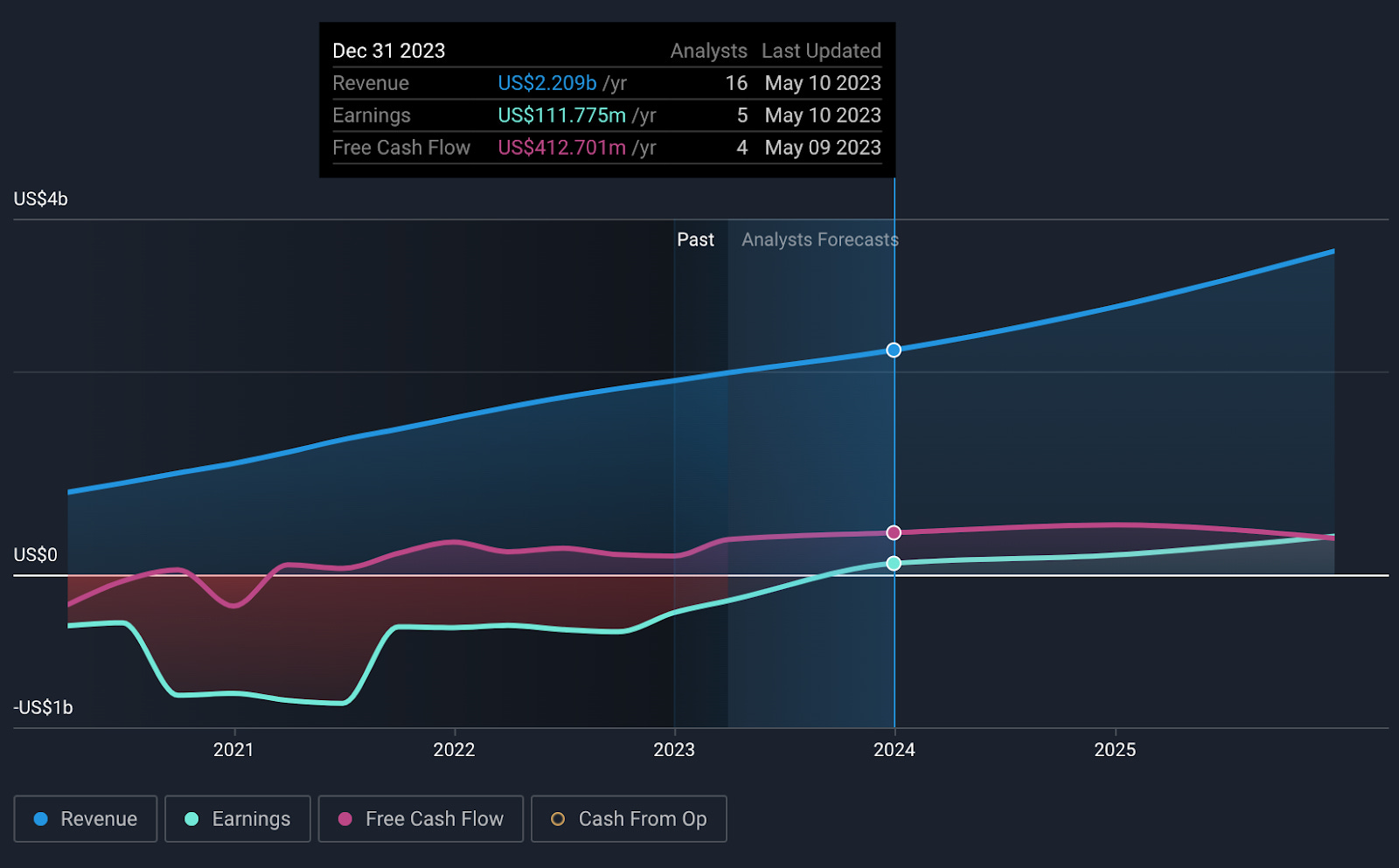

As of 2022, with $1.9 billion in revenue, Palantir has penetrated less than 2% of the total opportunity, providing the company with a concrete runway for at least the next decade.

Growth Drivers

Palantir's growth strategy for both commercial and government business segments in the United States and abroad is based on continuous expansion into the commercial sector, increasing usage with existing customers (especially with government customers), expanding internationally, growing the number of partnerships, and ultimately becoming the industry standard.

Below are the primary growth drivers:

Commercial sector

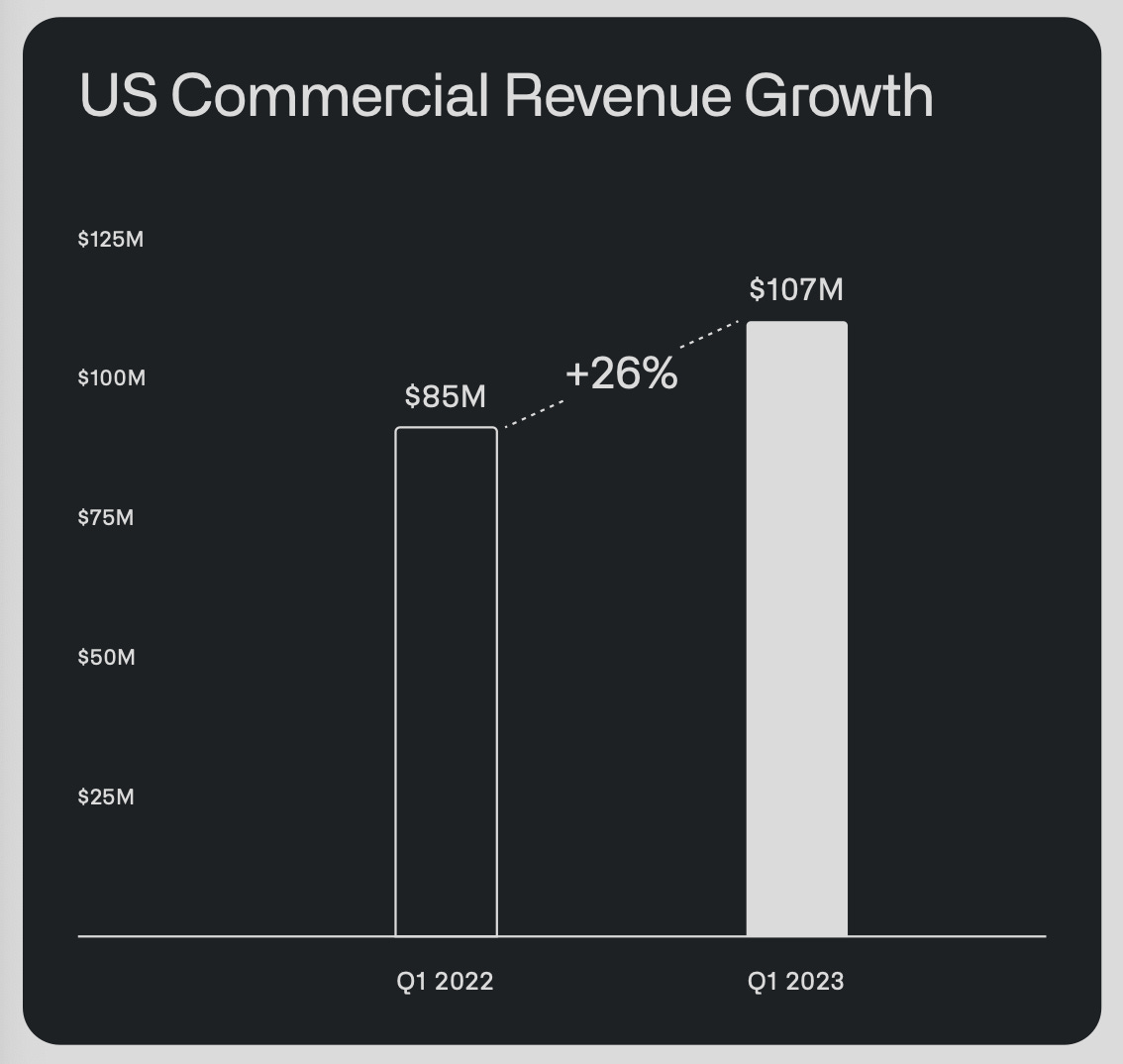

The growth in the commercial sector is absolutely crucial for the company. The commercial sector, especially the US one, has been the primary driver for Palantir's top-line growth in recent quarters, surpassing the $100 million revenue threshold in Q1 2023 for the first time in the company's history.

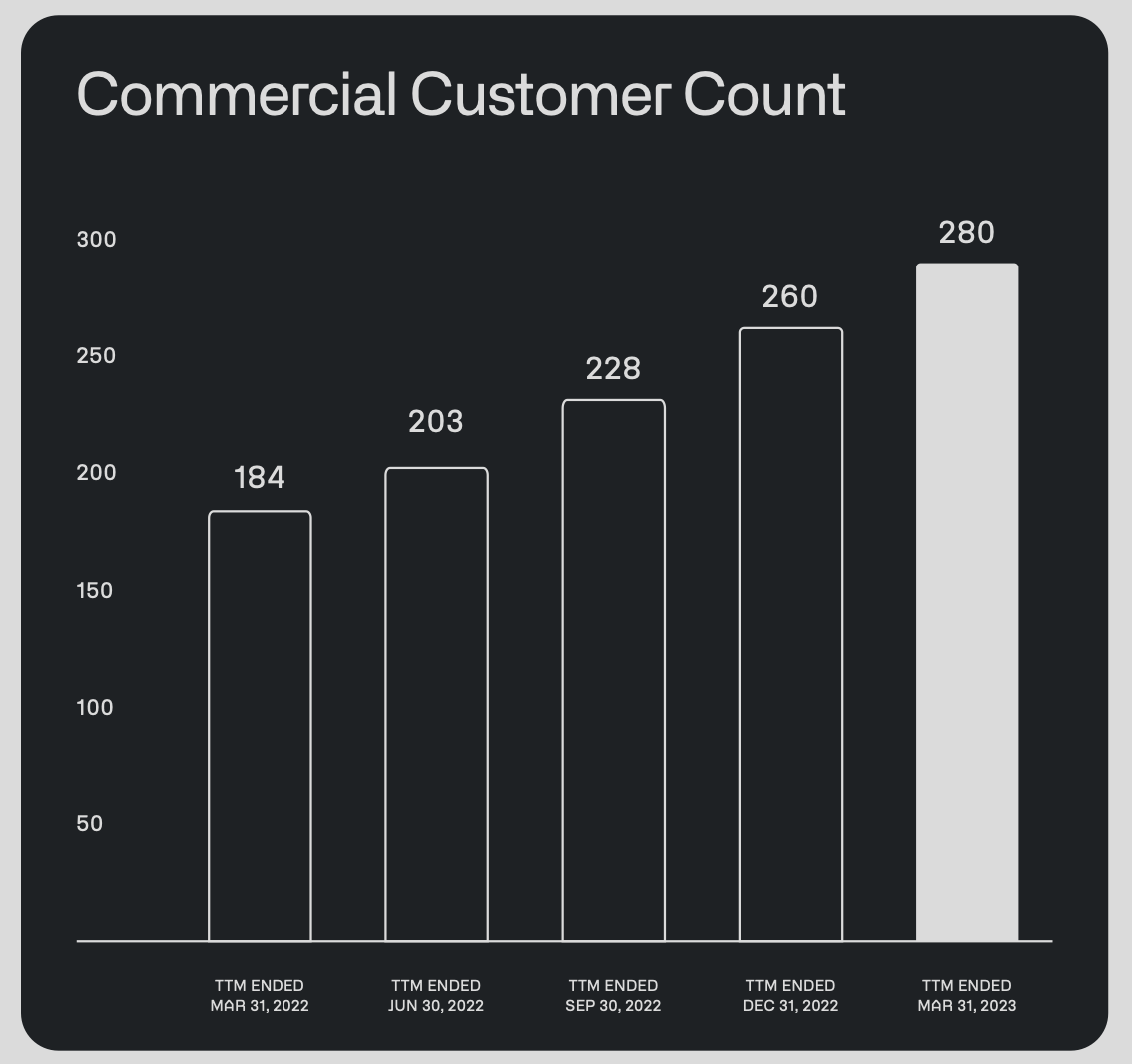

In Q1 2023, the company signed 20 new commercial customers making it 280 commercial customers in total, of which 155 are from the US, a seven-fold increase in customer count over just two years.

The US commercial continues to become a larger and larger part of Palantir's overall business. At this pace of growth, the commercial revenue will soon reach the same level as the government revenue. As of Q1 2023, 56% of the revenue came from government customers, while 44% came from commercial customers.

It is still a tiny number of customers compared to the potential 6,000 customers with more than $500 million in annual revenue worldwide. Most of the company's current customers are blue-chip companies, and Palantir has not only the opportunity to grow within this category, but it is yet to expand to a massive mid-market/SMB market.

Palantir now targets companies from 60 industries, from health care and supply chain to manufacturing and energy to automotive and utility.

For example, the number of deals closed in health care more than doubled in 2022. The company servers four of the largest hospital systems, which together represent nearly 10% of the entire hospital system in the US.

Increase usage with existing customers

Palantir has tremendous opportunities with existing customers to expand their usage of its platform.

For example, revenue from the top 20 customers continues to expand. In Q1 2023, the average trailing 12-month revenue per top 20 customer grew to $51 million, representing 14% YoY growth.

Some recent examples of how customers expand their usage:

Hertz is now using Foundry to more efficiently manage and operate its fleet of nearly 500,000 vehicles;

Jacobs Engineering doubled down on its partnership with Palantir to reduce cost and improve performance across plants;

The largest health system in the US signed an expansion agreement for continued acceleration of the hospital operations efforts;

SOMPO Holdings, which uses Foundry to help improve security, health, and well-being through digital transformation, has signed a $50 million five-year expansion agreement.

As of the end of 2022, the company expects to generate revenue under its existing customer contracts for an additional 2.8 years on a dollar-weighted average contract duration basis.

The company's contracts with its customers are usually long-term oriented, often lasting multiple years. Palantir has already been awarded certain contracts by government and commercial customers. Under these contracts, the company is entitled (but not guaranteed because many of these contracts are subject to termination for convenience provisions) to receive $3.7 billion ($2 billion from commercial customers and $1.7 billion from government customers) as of February 2023.

Palantir AIP

AIP represents the single biggest expansion opportunity for the company. It enables enterprises across the commercial and government sectors to leverage the power of large language models on their own privately held datasets.

By allowing customers to access and utilize AI capabilities, Palantir aims to increase the adoption of its software as well as create new revenue opportunities through licensing and subscriptions. The more organizations adopt AIP (as part of increased spending on AI), the larger this revenue will become over time. Potentially, all of Palantir's customers will be users of AIP by default.

“We're already seeing unprecedented demand for AIP, and we are reorganizing our efforts aggressively to capitalize on the interest.” – management comments.

The company has already had hundreds of conversations with potential customers about deploying the AI and is currently negotiating terms and pricing. AIP's first iteration will be available to select customers in May 2023.

Ultimately, management believes that artificial intelligence, including large language models, will prove transformational for its business and enterprises in the government and commercial context.

Partnerships

Partnerships also play a vital role in Palantir's growth, especially with public cloud services. The company has been strengthening its relationships with various ISVs (integrated service vendors), which can resell Palantir's software to thousands of customers without Palantir's direct involvement.

One particular partnership (with Microsoft) looks especially promising. Palantir Foundry will be available through the Azure Marketplace for seamless purchasing and invoicing. Customers can use their existing Microsoft Azure Consumption Commitment (MACC) to purchase a license and cover other costs.

Business Model

Palantir operates a highly scalable, software-as-a-service business model with 80%+ gross margins.

Revenue streams

The company generates revenue from selling subscriptions to access its software in its hosted environment along with ongoing O&M services (Palantir Cloud), software subscriptions in the customers’ environments with ongoing O&M services (On-Premises Software), and professional services.

Palantir Cloud

Palantir offers subscriptions to its cloud service that grant customers the right to access its software in a hosted environment controlled by Palantir. Subscriptions to the cloud service are sold together with operations and maintenance (O&M) services, which include critical updates and support as well as maintenance services required to operate the software. Palantir Cloud is primarily used by commercial customers.

On-Premises Software

Customers can also use Palantir's software either on their internal hardware infrastructure or on their own cloud instance. On-premises is also available through subscriptions and comes with stand-ready O&M services.

Professional services

The company offers professional services to support the customers’ use of the software. These services include on-demand user support, user-interface configuration, training, and ongoing ontology and data modeling support. Professional services are contracted separately but typically coterminous with Palantir Cloud or On-Premises Software subscriptions.

Gross Margin

The costs of running Palantir's platform are insignificant and include salaries, stock-based compensation, benefits for personnel involved in performing O&M and professional services, as well some other direct costs.

As a result, Palantir has solid gross margins comparable to the best SaaS companies. Adjusted gross margin, which excludes stock-based compensation expense, was 81% in the latest quarter. The GAAP gross margin came at a robust 79.50%.

Operating Expenses

Total operating expenses have been constantly improving, from 111.69% of total revenue in Q1 2021 to 87.69% in Q1 2022 to 78.72% in Q1 2023.

As a result, for the first time in its history, Palantir was able to deliver an operating income of $4.1 million in Q1 2023.

The company continues to manage expense growth by optimizing operations in G&A, capturing cloud efficiencies, and focusing its headcount investments in key strategic areas.

Profitability

Palantir plans to become profitable on a GAAP basis for the full year in 2023, posting two consecutive quarters of GAAP profitability, including a $17 million net profit in Q1 2023. Management expects to be GAAP profitable in each quarter this year.

While management does not provide specific numbers, analysts that cover Palantir expect the company to deliver more than $100 million in earnings in 2023, a tremendous increase from a net loss of $373.7 million in 2022. The earnings should accelerate from this point significantly.

Stock-based compensation remains high and is expected to trend up through the remainder of the year. As a percentage of total revenue, SBC was a hefty 22%, and 0.55% as a percentage of its market cap. Palantir remains a serious diluter.

Since going public, shares outstanding increased by 21.7% while the stock price has appreciated only by 3.5%.

Balance Sheet

Palantir has an exceptionally strong balance sheet with no long-term debt. The company ended the first quarter of 2023 with $2.9 billion in cash, cash equivalents, and short-term US treasury bills.

Furthermore, the company retains access to additional liquidity of up to $950 million through its $500 million revolving credit facility and $450 million delayed-draw term-loan facility, both of which remain entirely undrawn.

Cash Flow

To add to the strong liquidity position, Palantir has generated $189 million and $187 million in adjusted free cash flow and cash from operations, respectively, each representing a margin of 36%.

The company has been FCF-positive since the first quarter of 2021 and expects to only increase its FCF in the coming years.

*

Palantir has been losing money for basically its entire history until recently. If management sustains its ability to grow revenue while keeping stock-based compensation under control, Palantir will become a highly profitable company in the long term with attractive margins. Maybe then the company will be able to buy back the shares for all of the dilution it has already done and will continue doing.

Competitive Advantages

Competition

The big data landscape in which Palantir operates is massive and continuously widening. The company faces competition in both government and commercial sectors, less in the former and stiff in the latter.

Throughout the past decade, Palantir has established itself as a go-to company for any government-related organization. Palantir essentially became the default software supplier of big data analytics for governments, making it especially hard for any other company to compete with it.

Yet, the company faces competition in the government sector from some established players and some niche ones. Among established companies are traditional IT consultancies like Booz Allen and Accenture, which lose Palantir on the technology front; big data companies like IBM, which lose on price; and various defense contractors like Booz Allen, Raytheon, SAIC, and others, which can't compete on price, technology, and end-user experience.

Some smaller companies like Semantica AI, which offers an AI-based enterprise intelligence platform for governments, simply lack the resources (including connections with governments) to compete with Palantir on a big scale.

In the government sector, Palantir pretty much owns the niche. A different picture is in the commercial one. It is much more competitive with a wide variety of various solutions from companies like Alteryx, Cognizant, and Tableau, among others, making it hard for Palantir to win over customers. It explains why 13 years after the launch of the commercial business, the company has only 280 commercial customers.

But the company's success in the government sector, alongside some other competitive advantages, puts Palantir in a good position to continue driving new commercial customers as well as expanding relationships with existing ones.

Competitive Advantages

When it comes to competition in this space, companies generally compete on the best products, most professional services, and best-in-class customer experience. Reputation also plays a vital role when customers choose their vendors.

Palantir has built a number of competitive advantages around these, some of which are becoming stronger and stronger the more the company grows and attracts customers.

Technology

In its core sector of intelligence and defense, Palantir has built the best-in-class platform. Gotham is out of reach of competitors, and it has not only a technological edge over them but is also more cost-effective.

The superior technology pairs with Palantir's forward-deployed engineers, which assist its customers in identifying new use cases, modernizing their data architectures, and achieving success with data-driven initiatives. Once the deployment work is complete, these engineers help train customers until they are ready to use the products independently.

Switching costs

The very same forward-deployed engineers help customers build new applications on top of Palantir's platforms, further increasing switching costs.

Arguably, Gotham became the default operating system for big data at many US government entities, cementing its role and securing years of contracts.

Over time, the company can become an operating system for many other organizations, including commercial ones, like it already did for the aviation sector with Airbus.

High barriers to entry

The niche in which Palantir operates has exceptionally high barriers to entry. It requires not only a superior product, excellent service, and the best customer experience but also an impeccable reputation and connections on the government level.

Risks

Growth

Revenue growth peaked in the first quarter of 2020 and has since been on a steady decline. The growth may further slow down if the company cannot renew some key government contracts (the company extracts most of the revenue from these customers).

Profitability

Though the company expects to become GAAP profitable in 2023 and accelerate from there, the revenue growth slowdown could dramatically impact future profitability.

Commercial sector execution risk

More and more large companies are tightening their budgets amid the macroeconomic environment. Palantir has already seen a decline in the commercial part of the business in the past several quarters, indicating a weak interest from customers in Palantir's software and long-term, pricey contracts.

Dependence on US government contracts

A significant portion of revenue is derived from contracts with US government entities. A decline in the government budgets, changes in spending or budgetary priorities, or delays in contract awards will significantly impact Palantir's revenue and profitability.

Customer concentration

The company derives a significant portion of its revenue from existing customers that expand their relationships with it. The top three customers together accounted for 17% of total revenue in 2022. Palantir gets increasingly dependent on key customers.

Customer contracts

Customer contracts may be terminated by the customers at any time for their convenience.

Reputation and social acceptance

Palantir is a very ethically controversial company that has been involved in several scandals. For example, the company works closely with ICE, which oversees immigration. Some sources claim that ICE has used Palantir's software to conduct raids on immigrants, including forcefully separating parents from their children.

Stock-based compensation

Covered in detail in the Business Model section.

Competition

Covered in detail in the Competitive Advantages section.

AI

Generative AI tools may end up displacing or disrupting many of Palantir’s tools and features.

Control

The company is controlled by Peter Thiel, Alex Karp, and Stephen Cohen through a Founder Voting agreement, which means if they sell shares, they will still have control over the company.

Additional Sources

Management – https://investors.palantir.com/governance/executive-management

Board of Directors – https://investors.palantir.com/governance/board-of-directors

Ownership – https://www.sec.gov/Archives/edgar/data/1321655/000132165523000033/pltr-20230425.htm#i37de48c0bdc8476ba5d62418ce323d50_160 (page 43}

Have a great week!!!

As a reminder, you can track my investment portfolio, my daily activity as well as join me on my daily webcasts through this spreadsheet [click here]

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.