Hey everyone,

Just wanted to share some news regarding my LARGE CAP DEEP DIVES newsletter…in the next week I’m going to merge my large cap deep dives newsletter into my small/mid cap deep dives newsletter and rename it as DEEP DIVES.

This year we’ve seen some big moves in large/mega caps… from META to NVDA to CRWD to ANET to SPOT to TSLA or UBER to PLTR to DKNG and many others.

Given these big moves I’m having a hard time finding compelling, undervalued large cap growth stocks whereas I see more interesting and exciting opportunities in small/mid caps so that’s going to be primary focus however I’m definitely leaving the door open for more large cap deep dives in 2024 if we get some pullbacks, IPOs or new catalysts ie AMD with their new MI300 AI chip (started a position in AMD this week).

For the most part I’m looking at companies with market caps between $1 billion and $20 billion that could have 100% or more upside over the next ~3 years.

As you may know, the Nasdaq 100 ($QQQ) is up +47% YTD whereas the Russell 2000 ($IWM) is only up +7% YTD, it’s very possible we see this rally continue into 2024 with better overall breadth which means the $1-20 billion companies might finally outperform compared to the $500+ billion companies ie Mag7 which is AAPL, MSFT, NVDA, AMZN, GOOG, META and TSLA.

I have a call with Substack next week to discuss the best/easiest way to migrate over my large cap deep dive subscribers, I’ll try to make it as seamless as possible for anyone who already paid for an annual plan. For instance if you signed up last March and did the annual plan for my large cap deep dives, you’ll get moved into the new DEEP DIVES newsletter (formerly small/mid caps) with access through March and maybe I throw on a free month for the inconvenience. If you’re currently a annual paid subscriber this large cap newsletter and you’re already a subscriber on the small/mid cap newsletter… in this scenario I’ll give you a prorated refund on the large cap newsletter.

Going forward my deep dives newsletter (no more small, mid, large) will consist of the following:

3-4 monthly deep dives (~8,000 words)

3-4 monthly mini deep dives (~8000 words)

access to my investment portfolio with daily activity, buys/sells, hedges, etc

access to my daily webcasts and all recordings

I hope this makes sense. If you have any questions just shoot me an email at jonah@luptoncapital.com

Here’s the mini deep dive on TransMedics ($TMDX) I sent to my small/mid cap subscribers this week.

My mini deep dive on SuperMicro ($SMCI) will be going out in the next few days.

Mini Deep Dive on TransMedics: From Groundbreaking OCS to Sky-High Ambitions:

Current stock price: $72.90

Market cap: $2.35 billion

Jonah’s current investment portfolio: https://docs.google.com/spreadsheets/d/1oqNvhyZH76EWdQPM7faTjqCthvskiNPNCOIEG295raE/edit#gid=0

Summary

TransMedics revolutionizes organ transplants with its patented OCS technology, fueling significant growth and industry leading position

Strategic aviation expansion and advanced OCS development creating competitive moat

TransMedics should be profitable inCY2024 followed by several years of high EPS growth

I covered TransMedics (TMDX) in my newsletter for the first time back in February 2021, when the stock was at $26 per share, and TransMedics had not yet launched its National OCS Program (NOP), which has been a game-changer for the company, completely transforming it ever since.

Several months ago (September 2023), after almost 2.5 years, I published a second deep-dive on TransMedics (7,000+ words) in my investment group, Fundamental Growth Investor, covering everything from the company's story and near-term/long-term catalysts to the recent acquisition of Summit Aviation and the 3-5 year price targets based on my investment model.

Today, TransMedics is one of my top 5 positions, and in this mini-writeup, I will provide an update after the recent quarter (Q3 2023) and explain why I am still bullish on the company.

Thesis

My investment thesis for TransMedics is centered around its innovative Organ Care System (OCS), a technology that has the potential to truly revolutionize organ transplantation. OCS technology represents a significant advancement over traditional static cold storage methods used for organ transplantation and a much superior alternative to other warm perfusion storage solutions, such as XVIVO and Organox.

This positions TransMedics as a leader in the field of organ transplants, with a significant first-mover advantage, particularly as they hold FDA approvals for heart, lung, and liver transplantation – the only FDA-approved device for multiple organs.

The critical demand for organ transplants, a space where supply and utilization are highly mismatched, highlights the need for such technology. OCS is well-positioned to bridge this gap, providing TransMedics with years of continuous growth.

The company is projected to reach substantial revenue growth, expecting to surpass $1 billion by 2030 from an estimated $228.9 million in 2023. I anticipate TransMedics to reach $1 billion in revenue earlier, maybe two years earlier, due to its increasing involvement in the growing number of transplants. In fact, TransMedics, with its OCS technology, is a primary enabler of increased donor utilization. The company, essentially, creates the market for itself.

Right now, TransMedics is unprofitable, but at this rate of growth, it should become adjusted EBITDA positive in 2024 before turning profitable on a net income basis in early 2025. I believe TransMedics could be profitable in 2025 however it will depend on hiring costs, R&D, S&M and additional expenses related to building out their aviation and logistics business.

The company’s strategic move into aviation, building its own fleet of small airplanes to transport donor organs, should only accelerate the growth in the coming years.

My thesis also acknowledges some potential risks, including the complexities involved in integrating an aviation division, the company’s indebtedness, shareholder dilution, operational readiness in meeting increasing demand, and a few others I cover extensively in my deep dive.

However, a combination of TransMedics' technological innovation, market leadership, growth potential, and competitive advantages make my thesis strong enough to justify a position in the top 5 in my investment portfolio.

I also put faith in Waleed Hassanein, TransMedics' founder and CEO, who not only has skin in the game but is also one of the most respected people in the field. He anticipates 10,000 transplants annually in five years' time, a significant increase from the 2,000 transplants scheduled for 2023. With a track record of beating and raising its projections, I am confident that TransMedics will successfully achieve that target.

Quarterly Update

Speaking about beating and raising, TransMedics delivered yet another outstanding and, to some extent, surprising quarter. EPS in Q3 2023 came at $0.07, beating estimates by $0.20, while revenue was $66.43 million, a whopping 158.65% year-over-year increase, surpassing expectations by $17.25 million.

The best part of this earnings is that TransMedics has significantly raised its 2023 outlook. Annual revenue guidance for 2023 increased to between $222 million and $230 million, representing 138% to 146% growth over 2022, from a prior range of $180 million and $190 million.

It is the main reason why the stock bounced back from its October lows when it reached its 52-week low at $36.42 per share, primarily due to investors' skepticism around the company's acquisition of Summit Aviation and its ability to successfully manage and operate an aviation fleet – something that is entirely out of TransMedics' scope and something that will significantly pressure gross margins from now on.

In the third quarter, TransMedics completed the acquisition of eight planes and outlined plans to expand its fleet to 15-20 by the second half of 2024. This quarter, the company initiated a limited launch of the transplant logistics service, resulting in $2.1 million from the new, transplant-related aviation and logistics offerings.

The NOP (National Organ Preservation) program continued to significantly contribute to revenue growth, and the company is on track to complete over 2000 NOP transplants in 2023.

On the not-so-bright side, the company has seen a considerable decrease in gross margin, from 70% in Q2 2023 to 61% in Q3 2023. This decrease is attributed to several factors, primarily due to transient inefficiencies – the old charter business is phasing out, while the new transplant business is just starting, with neither operating at full scale during the quarter. Once logistics is fully operational, the gross margin is expected to improve, though not to the previous level.

The acquisition-related costs and the purchase of eight jets influenced the increase in total operating expenses, dragged down net loss to $25.4 million from the $7.4 million loss in the same quarter of the previous year and $1 million in the prior quarter of 2023, and resulted in a significant decrease in free cash flow, from negative $7 million in Q2 2023 to negative $114 million in Q3 2023.

TransMedics still maintains a strong cash position, finishing the third quarter with $427.1 million. The company's significant investments in acquisitions and logistics infrastructure demonstrate a strategic effort to expand its service capabilities and infrastructure, which will eventually start to pay off.

Growth Drivers

TransMedics has a number of near and long-term growth drivers that will profoundly impact its revenue growth and profitability.

A key focus for the company is the expansion of its National OCS Program (NOP), which is essential for increasing the adoption and use of its Organ Care System (OCS) technology by transplant centers. Only a small percentage of US transplant centers currently utilize this technology on a constant basis, providing significant room for growth. Expanding the NOP is particularly important because it is expected to be a major source of volume and revenue for the company in the coming years.

To facilitate the National OCS Program further, the company is continuously improving its OCS technology. TransMedics is already working on next-generation OCS technology, which will bring innovations like cloud connectivity, automation, and remote control. This new technology, which includes new perfusion systems for hearts and lungs, is expected to enter clinical trials by 2025.

Another major catalyst for TransMedics is the development of its aviation operations. The company is now establishing its own air transportation fleet, which marks a strategic shift from relying on private jet brokers. The aim here is to control the entire logistics process from donor to recipient to directly manage all NOP transplant volume in the US by the second half of 2024.

This integration will help TransMedics manage transplant volumes more efficiently and overcome previous logistical challenges. Most importantly, it will further cement TransMedics' competitive advantage, making the competition at this stage almost obsolete.

Finally, TransMedics is looking to expand globally, particularly in Europe and Asia-Pacific markets. Despite being present in Europe for over a decade, the company has had a limited success rate there so far due to the way reimbursements work in these regions. I believe there is significant untapped potential, especially if reimbursement policies like those in the US are eventually adopted. TransMedics is currently developing materials and conducting clinical trials to facilitate this expansion. If successful, this will provide an additional boost to revenue, which is not projected in the current estimates.

Valuation

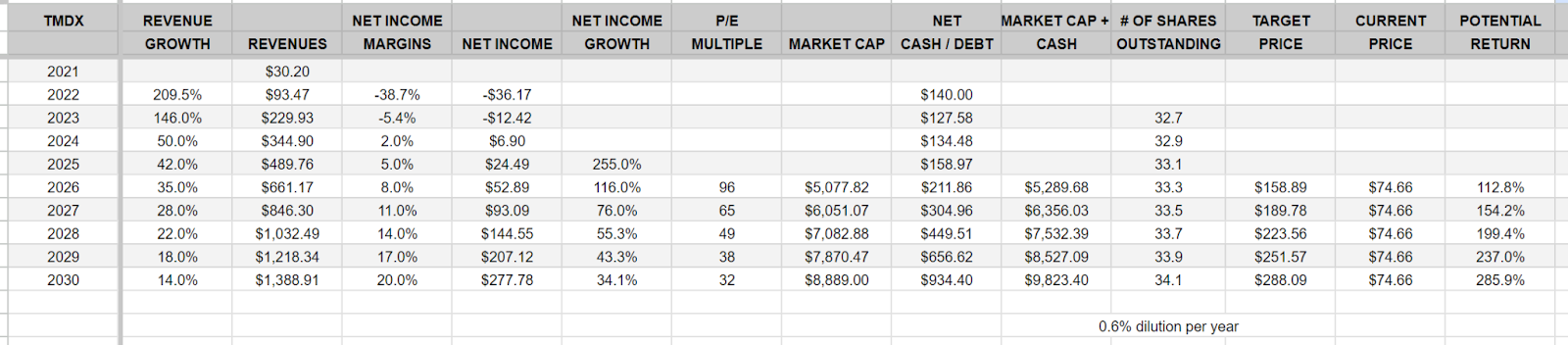

Now that TMDX is on the brink of profitability (would have been profitable in 2023 Q3 if they weren’t investing in the aviation & logistics business), the stock will trade at a premium multiple because EPS growth should be in the triple digits for the next 3-4 years as net income margins improve from -5% in 2023 to 8% in 2026 to 14% in 2028 and perhaps even 20% by end of decade. If you look at other more-mature medtech companies, most of them have net income margins north of 20% by the time revenue growth has slowed into the teens and I expect TMDX will be no different.

TMDX is very much a hypergrowth stock that is still investing in the business and building their moat, much different than Medtronic (MDT) or Intuitive Surgical (ISRG) which makes it a little harder to come up with a fair market valuation for TMDX since the next 5-6 years is less predictable. Below is my investment model going out to CY2030 with my estimates for revenues and net income margins which gets us to some rough price targets. Based on my investment model and estimates, I do believe TMDX has 100% or more upside over the next 2-3 years and 200% upside over the next 4-5 years.

Conclusion

TMDX is one of the largest positions in my investment portfolio because it has all the attributes of a long term winner assuming continued revenue growth (5x over the next 6 years) and expanding margins which leads to substantial EPS growth which is the most important ingredient when trying to find the best stock outperformers. TMDX has increased revenues almost 10x over the past few years but that’s just the tip of the iceberg now that heart, lungs and liver are all approved. We should see OCS Kidney approved in the next couple years which will be another catalyst for the stock. Just a couple months ago investors were giving up on TMDX because of their decision to push into aviation and logistics but after that incredible Q3 earnings reports those same investors are flocking back to the stock because they understand that strategic decision might cause some near-term margin compression but over the long-term it gives TMDX a dominant position and allows them to support their aggressive growth goals. If the CEO is correct and TMDX can go from ~2,000 OCS procedures in 2023 to ~10,000 OCS procedures, the only way that happens is with their own aviation fleet not to mention at some point we might see TMDX surgeons doing the actual procedures which just increases the TAM even further. Once I identify a potential multibagger and build out a large position, I rarely want to see that company get acquired because it puts a ceiling on the upside. However, I will mention it here because I do think there’s a 30-40% probability that TMDX gets acquired in the next 18-24 months. If it does happen I’m hoping it’s not until 2025 and the price is north of $150+ per share which still leaves 100% upside from the current price.

Have a great week,

~Jonah

Time passes by quickly, I can't believe we're already in late 2028!