Mini deep dive on SuperMicro Computer ($SMCI)

In order to read this mini deep dive on SuperMicro ($SMCI) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support.

Paid subscribers receive ~3 deep dives per month (7,000+ words) and ~3 mini deep dives per month (2,000+ words) plus access to my current investment portfolio (up +120% YTD), my investment models on current holdings and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up 120% YTD) and my trading portfolio (up +88% YTD) including lots of activity updates, charts, market opinions, macro analysis, earnings analysis, analyst upgrades/downgrades and much more.

Hardware Enabler Of The AI Revolution: Mini Deep Dive on SuperMicro Computer (SMCI)

Summary

Even though SuperMicro Computer is up more than 200% in 2023 it is still undervalued at less than 15x FY2024 earnings with 45-50% revenue & earnings growth

AI chip market is expected to increase 10x in the next 3-5 years (according to experts including CEOs of TSM, NVDA and NVDA, thus providing huge growth potential for Super Micro

SuperMicro is well-positioned to capitalize on this AI chip opportunity because of key partnerships with Nvidia ($NVDA) and AMD ($AMD)

As a paid subscriber you have access to the following:

My investment portfolio [click here]

My investment models [click here]

My daily webcasts [click here]

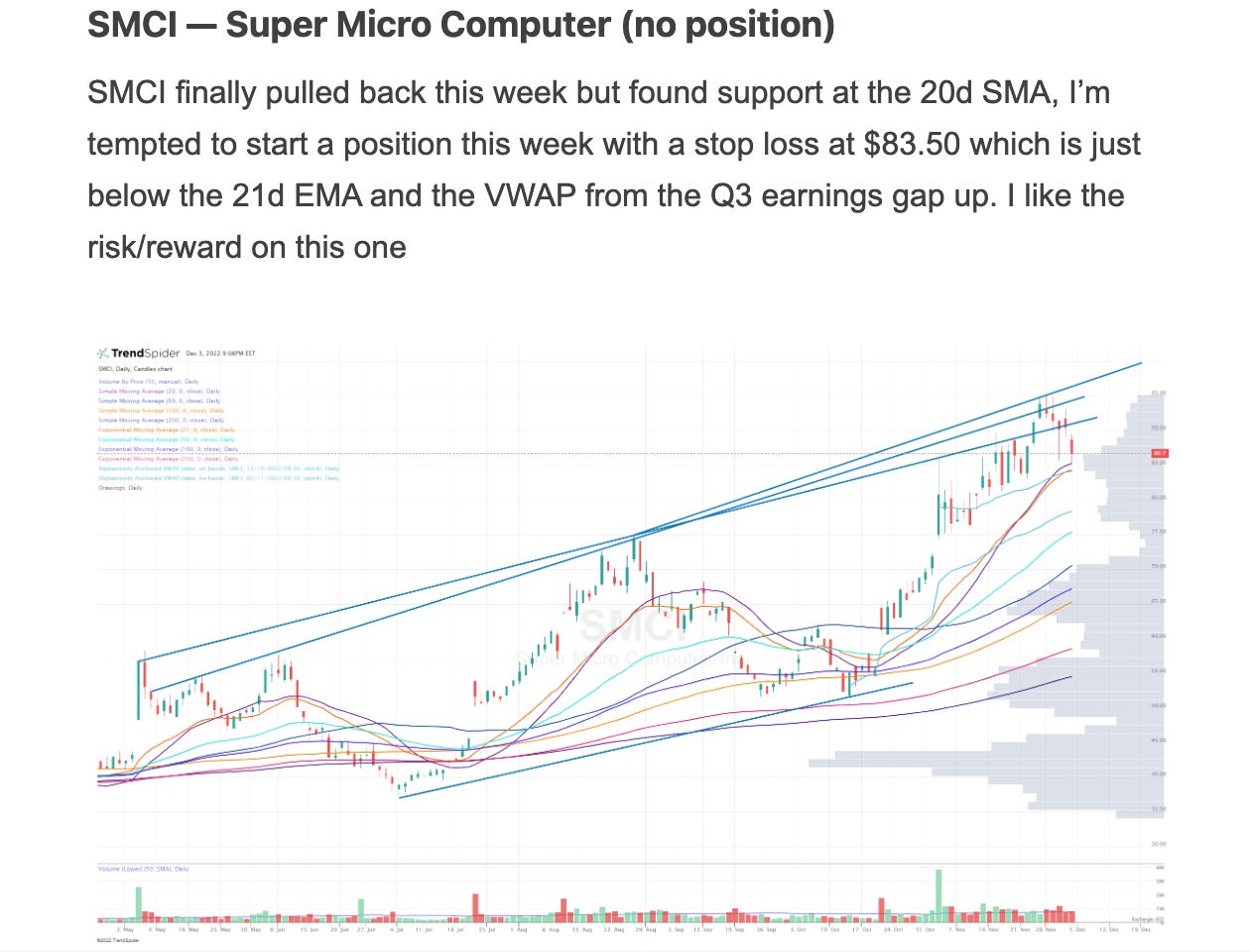

SuperMicro caught my attention back in December 2022 at around $83.50, before AI and Nvidia became hot topics, this was around the time that OpenAI launched ChatGPT.

I traded SuperMicro several times in late 2022 and early 2023 before starting a core position in my investment portfolio followed by a 7,000+ word deep dive on the company in June 2023 to share my research and investment thesis with my subscribers. The deep dive covered everything from the company's origins to its competitive advantages and most importantly the enormous opportunity ahead as data centers upgrade to AI chips for their own businesses as well as their customers. Through the first 9 months of 2023 the biggest buyers of AI chips have been Microsoft and Meta followed by Google, Amazon and Oracle.

Below I will go into the details about why I think SMCI is one of the most undervalued stocks I follow and because of this SMCI has become the second largest position in my portfolio, ahead of TransMedics (From Groundbreaking OCS To Sky-High Ambitions: Mini Deep Dive On TransMedics) and behind Celsius (CELH). I remain extremely optimistic about SuperMicro going into 2024 and will use pullbacks to increase my current position.

Investment Thesis

My investment thesis for SuperMicro is primarily based on the rapidly increasing demand for AI chips, especially from mega-cap tech companies like Meta, Microsoft, Google, and Amazon, which will only boost their investments in building out their AI infrastructures in the coming years.

The large tech, cloud, and software companies will need to buy a lot of AI chips over the next 3-5 years in order to power their LLMs (large language models) which are used for training & running their AI/ML models. Taiwan Semiconductor ($TSM), predicts that AI chip demand will grow 50% per year for the next 5+ years. Lisa Su, CEO of AMD projects the market for AI chips could reach $400+ billion in 2027 (up 10x from 2023) and Jensen Huang, CEO of Nvidia thinks AI chips will be a $1 trillion capex opportunity over the decade. All of these companies buying these critically important AI chips will need customized racks (and other components) to keep those chips at the right temperature and operating at peak efficiency which means better performance and less energy consumption i.e. lower operating costs. SMCI is one of the companies that makes this kind of hardware with their proprietary cooling technology.

Super Micro is a key beneficiary of this multi-hundred-billion (some estimate even a trillion dollar) AI race, being a critical enabler of advanced data center capabilities. In strategic partnership with leading chip manufacturers like Nvidia (H100) and AMD (MI300), SuperMicro allows big tech companies to integrate cutting-edge processing power into their data centers, which is crucial for the computationally intensive tasks that AI applications demand.

What I particularly like about SMCI, besides its strong ties with Nvidia and AMD, is its approach to providing customizable solutions and ongoing advancements in server technology, such as liquid cooling, which not only enhances the performance of AI systems by enabling higher operating speeds without overheating but also contributes to energy efficiency, an increasing concern in data center operations. These set SMCI apart from the crowded competition and provide a solid foundation for sustained growth.

In terms of growth, SMCI continues to beat estimates and raise guidance. When I did my deep dive back in June the company was projecting $9.5 billion to $10.5 billion of revenues for FY2024 (which ends June 2024) but in their most recent earnings report they raised FY2024 guidance to $10 billion to $11 billion. Personally I would not be surprised if we see $11.5 billion or even $12 billion when they report in June. Charles Liang, founder and CEO also outlined an ambitious goal of reaching $20 billion in revenues within the next 3-5 years which is one reason why they recently raised ~$525 million in a stock offering so they could expand their manufacturing capacity as well as accelerate their R&D efforts and get ahead of any inventory demand acceleration over the next few months which could happen thanks to the launch of AMD’s MI300 series AI chips.

Even though SuperMicro is showing rapid revenue growth they are still a lower margin hardware business so I’m not expecting any margin expansion however even if net income margins dipped from 9.5% in FY2023 to 9.0% in FY2024, if they’re growing revenues by ~55% we should still get 45-50% net income (or EPS) growth and this is why I think the stock is so overvalued because it currently trades at 15x FY2024 net income estimates. Despite the lower margins SuperMicro is still very profitable and should generate ~$1 billion of net income in FY2024.

I don’t expect SMCI to grow net income or EPS by 45-50% per year in perpetuity but even with that in mind the stock should be trading at 25-30x earnings and not 15x earnings, this is why I think SMCI has 50-100% upside over the next 6-12 months not to mention the current estimates for FY2025 and FY2026 are still too low.

Quarterly Update

SuperMicro reported its earnings (Q1 FY2024) just recently (November 1, 2023), beating both EPS and revenue expectations. EPS came at $3.43, surpassing estimates by $0.18. Revenue soared to $2.12 billion, marking a 14.45% year-over-year increase and exceeding forecasts by $57.20 million.

Management yet again raised its revenue guidance from a previous range of $9.5 billion to $10.5 billion to a new range of $10 billion to $11 billion, representing a 5.0% rise from the midpoint. I mentioned above that I think SuperMicro could potentially do $12 billion in FY2024 which would certainly catch investors and analysts by surprise forcing them to chase the stock higher.

The big highlight of these earnings was the growing demand for AI platforms, especially the NVIDIA HGX-H100 solutions, which drove significant revenue boosts for the company.

Additional optimism for investors came from the news that the company is expanding its liquid-cooling solutions in data centers and broadening its AI product range (including Intel Gaudi 2, AMD MI250 and MI300X platforms), further positioning Super Micro Computer favorably in the market. Management now expects over 50% of revenue to come from AI GPU and rack-scale solutions.

What I found especially bullish is the news about the significant expansion of the company's facilities to meet the growing demand. As part of its ongoing efforts to meet high-volume scale demands and enhance cost structures, the company is currently undertaking an expansion initiative in Malaysia. This expansion should have a significant impact on the company's total revenue capacity and help increase it beyond $20 billion.

Additionally, new buildings are being added close to the company's Silicon Valley headquarters, aimed to increase the current production capacity of 4000 racks per month. The company plans to complete a dedicated facility for manufacturing 100-kilowatt racks with liquid-cooling capabilities by March next year, which will increase the rack production capacity to 5000 pieces per month.

SuperMicro ended Q1 FY 2024 with a robust cash position of $543 million and $146 million in debt (notably, $144 million was paid down in this quarter), resulting in a net cash position of $397 million, a substantial increase from a net cash position of $150 million in the quarter prior. The company also generated a positive free cash flow of $268 million, a substantial improvement compared to the negative free cash flow of $17 million in Q4 FY 2023.

Update: To support the facility expansion, as well as to build up inventory and accelerate R&D efforts, Super Micro Computer announced a public offering on December 1, 2023. This offering would result in $524 million in gross proceeds. The stock price dipped after the news, but I believe it's a positive sign as it supports my argument about growing demand. I took this opportunity to add to my current position.

Growth Drivers

As mentioned earlier, the increasing adoption of AI across many sectors presents a huge opportunity for SMCI but there’s no guarantee that Nvidia and AMD will be the only US-based tech companies producing AI chips. It’s certainly possible the tech giants like Google, Microsoft, Meta, Apple, Amazon and even Tesla will eventually develop their own AI chips in which case I think SMCI still has an opportunity to work with many of them. SMCI will try to stay agnostic and build customized hardware for every AI chip company since they’ll all have similar needs.

If the CEO’s of Nvidia and AMD are correct and the AI chip market turns out to be worth $500 billion to $1 trillion over the next 5-10 years then there’s plenty of room for multiple winners but this is why I think SMCI is so attractive at current prices because they’ll get to work with all the winners and the stock at 15x FY2024 earnings is just too cheap.

I believe the company's strategic focus on AI chips and liquid-cooling technology, combined with its strong market position and continuous innovation, positions it to capitalize on this opportunity effectively and for the long term. As long as there is a demand for AI chips, SuperMicro will see demand for their products and services.

Valuation

As mentioned above, the current valuation of SMCI is one of the most compelling reasons to own the stock. Analysts are estimating $10.8 billion of revenues in FY2024 and $21.8 billion of revenues in FY2028. If they only hit these estimates (I think they’ll exceed them by a wide margin) it would mean 25% annualized growth and even if net income margins stayed at ~9.5% through FY2028 it would mean EPS growth would also be around ~25% per year so I simply don’t understand why the stock is trading at ~15x FY2024 earnings. I know that margins are on the thinner side but that’s mostly irrelevant when we’re trying to determine fair P/E multiples, that usually comes down to current and sustainable growth rates. It’s very reasonable to pay 25x earnings in 2023 if those earnings are expected to increase by 25% per year for the next few year. I know that SMCI doesn’t have the strongest moat like NVDA or AMD but trading at a PEG ratio under 0.5x is rare to see from such a high-quality, profitable company.

Below is my updated investment model for SMCI; I believe these numbers are reasonable and achievable.

The estimates in my model could turn out to be conservative if Lisa Su is correct and the market for AI chips reaches $400 billion in 2027; in this scenario I think SMCI would do $30+ billion in FY2028.

Conclusion

I’m obviously bullish on AI chips for the next 5+ years which is why I also own NVDA and AMD however I do think SMCI provides the most upside because of the current valuation and their ability to work with multiple AI chip companies. With that said I don’t think it’s too late to own all three of these companies but you’ll be owning them for different reasons. With AMD launching their MI300 chips in early 2024 it could provide an upside surprise to SMCI’s recent FY2024 guidance. With so many tech stocks looking overvalued right now after rallying over the past ~12 months, it’s surprising that SMCI could still look this cheap. Of course I wish they had better margins and a bigger moat ie competitive advantages but I believe both of these flaws are already priced in at 15x FY2024 earnings. As long as SMCI has a great relationship with NVDA and AMD then I’ll continue to stay bullish and add to my position on pullbacks.

Have a great week!!!

~Jonah

You can follow me on Twitter at @JonahLupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.