Part 1: Deep dive on Live Nation ($LYV)

In order to read this entire deep dive on Live Nation ($LYV) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (up +94.2% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio (up 94.2% YTD) and my trading portfolio (up +69.5% YTD) throughout the day including lots of charts, market opinions, macro analysis, earnings analysis, and much more.

Here are my other newsletters…

Company: Live Nation Entertainment

Ticker: (LYV)

Website: LiveNation.com

IPO date: December 2005

IPO price: $10.85

Current stock price: $79.95

Outstanding shares: 228.1 million

52 week high: $101.74 on July 28, 2023

52 week low: $64.25 on March 24, 2023

ATH: $126.79 on February 25, 2022

Market cap: $18.2 billion

Net cash/debt: $1.3 billion (net debt)

Enterprise value: $19.5 billion

Headquarters: Beverly Hills, California, United States

Number of employees: 12,800+

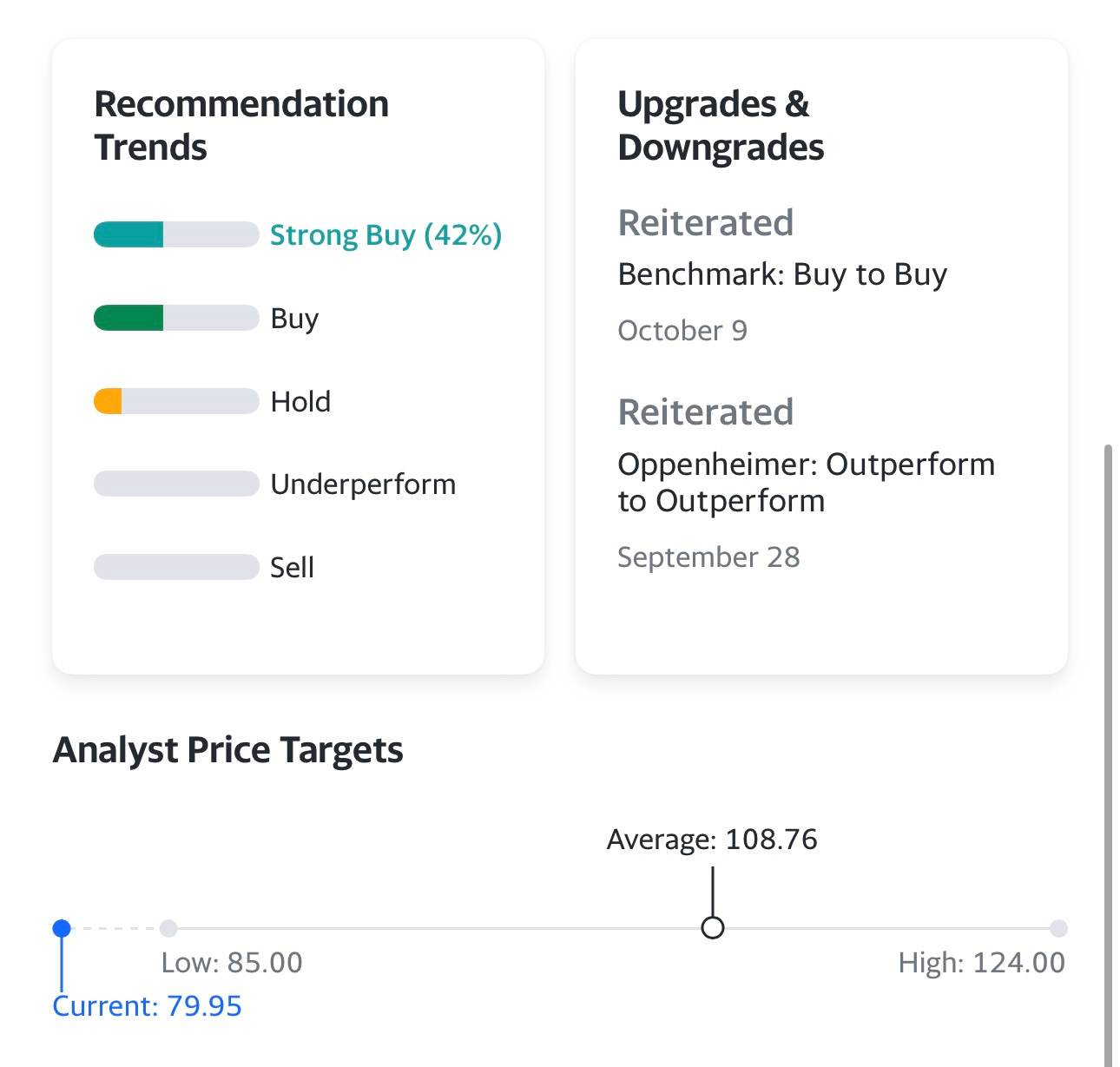

Average price target from analysts: $108.76 or 36% above current price

Investor Relations: https://investors.livenationentertainment.com

Q2 2023 Earnings Report: https://d1io3yog0oux5.cloudfront.net/_19a4ef8dcbafbc8831d0b9748379b404/livenationentertainment/db/670/6275/earnings_release_pdf/LYV+2Q23+ER+Final+V2+.pdf

Q2 2023 Trended Results: https://d1io3yog0oux5.cloudfront.net/_19a4ef8dcbafbc8831d0b9748379b404/livenationentertainment/db/670/6275/trended_results_grid_pdf/2Q23+LNE+Trended+Results+Grid.pdf

Q2 2023 Earnings Transcript: https://d1io3yog0oux5.cloudfront.net/_19a4ef8dcbafbc8831d0b9748379b404/livenationentertainment/db/670/6275/transcript/2Q23+LNE+Live+Call+Transcript.pdf

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

Below the paywall is the Live Nation ($LYV) deep dive along with links to my investment portfolio (up +94.2% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here] — new link for October

My investment models [click here]

My daily webcasts [click here] — new link for October

Introduction

I do not have a position in LYV, in fact I’ve never owned it in my investment portfolio however I have owned it a couple times in my trading portfolio. LYV actually looks interesting at current prices if, and only if, it can stay above the 200d sma with 78.69 as the floor. I believe the big unfilled gap in May was from Q1 earnings and the big move lower in August was because of growing concerns that the DOJ investigation could turn into a lawsuit. This is a definitely a risk over the next 3-6 months with some media outlets speculating that a DOJ lawsuit could come before year end, [click here] for more info.

I didn’t realize how large and influential LYV was until I met someone at my gym that worked for the company and they starting breaking down all of the different businesses that LYV is involved with from managing/promoting hundreds of the biggest musicians/comedians/DJs to owning/managing the venues to handling ticket sales through Ticketmaster.

As it turns out the new MGM Music Hall near Fenway Park in Boston is a joint venture between Live Nation and Fenway Sports Group

In addition to that, the Leader Bank Pavilion (which is just down the street from me) is also owned and operated by Live Nation. This is what LYV does all over the world, they build their own venues or they make equity investments into existing venues.

I like LYV’s business model, I like the diversified mix of revenues, I like their expansion strategy outside of the US, I like that they’ve pushed harder into the venue-ownership business… however I just don’t love the valuation or the tepid growth estimates over the next several years… my best guess is that LYV stock outperforms the broad markets like SPX (S&P 500) but not by a huge margin.

Right now LYV is trading at 48x 2024 EPS estimates which is quite expensive for a company that is only expected to grow revenues next year by 7.7% but here’s where it gets interesting — EPS is expected to grow 63% next year followed by three more years of ~43% EPS growth which makes the current P/E multiple a little more palatable. Revenue growth is expected to be in the high single digits for the next 4-5 years but profit margins are expected to expand from 1% in 2023 to 4.5% in 2027 which is why the EPS growth looks so much better than the revenue growth.

Looking out over the next ~4 years (from 2023 through 2027), LYV is expected to grow net income (NI) by 55% per year and EPS by 48% per year, however I’m guessing the stock performance will be closer to the revenue growth numbers than the NI or EPS growth numbers because you’re not going to see much multiple expansion with LYV already trading at 75x 2023 EPS and 48x 2024 EPS.

If, LYV was trading at 20x 2024 EPS with expected EPS growth of ~48% through 2027 then I’d be very excited about owning LYV for the potential upside because then we could get some multiple expansion.

With all that said, it might be better to look at FCF instead of EPS, in which case LYV is trading at 17.5x 2023 FCF and 16.0x 2023 FCF which seem reasonable with FCF expected to grow by 13.3% per year through 2027 during which time LYV should generate $6-7 billion of FCF which could be used for a variety of activities including paying down debt, stock buybacks or making new investments into venues with an emphasis on international expansion.

Here are the estimate trends for LYV over the past few years; what’s interesting is that back in 2020 (during the pandemic) the analysts were only looking for ~$14 billion of revenues in 2023 but now it looks like that number will actually be north of $20 billion.

I like companies that are growing revenues by at least 30% per year like Celsius (CELH), Elf Beauty (ELF), TransMedics (TMDX, On Running (ONON) and NuBank (NU) and there’s probably no shot of LYV ever getting back to this kind of growth so any bullish thesis will need to revolve around margin expansion and compounding FCF growth at ~15% per year then using that cash to make the company and balance sheet stronger.

I do worry that LYV could be impacted by a bad recession because it probably means less people spending big money to attend live events, however I still think it’s possible the US avoids a recession in 2024 if the FOMC is done hiking rates, the 10Y yield starts to drop and the labor markets remain strong.

If the DOJ does come after Live Nation and Ticketmaster it’s possible they hit the company with a fine and/or try to breakup the company which probably means a spinoff of Ticketmaster into a separate publicly traded company which could actually be good for shareholders if it unlocks value and gives Live Nation an influx of cash. The worst scenario would probably be a DOJ lawsuit that not only results in a big fine but forces Ticketmaster to lower some of their fees thus impacting revenues & earnings. I’m not a lawyer so I have no idea where this DOJ case might go but it’s something that shareholders should be paying attention to.

In these deep dives I like to speculate about possible M&A deals as either an acquirer or as the company being acquired… in this case I think LYV should go after Madison Square Garden Entertainment aka MSGE which owns and operates 70+ music & entertainment venues including Madison Square Garden, the Beacon Theatre, Radio City Music Hall and dozens of the biggest nightclubs in the country. Recently the Dolan Family split up their company into several pieces which includes MSGE (mentioned above), Madison Square Garden Sports (MSGS) which owns the Knicks/Rangers and finally Sphere Entertainment (SPHR) which owns MSG Networks and the new Sphere in Las Vegas. Other acquisitions that could make sense would be ticketing platforms like SeatGeek, StubHub, Eventbrite, etc that LYV could combine with Ticketmaster however I’m not sure if the DOJ and FTC would like that.

Hope you enjoy this deep dive and learn something new about Live Nation.

Company Background

Live Nation was founded back in 1996 as SFX Entertainment by American businessman and media mogul Robert F. X. Sillerman.

SFX Entertainment was initially a part of his other company, SFX Broadcasting, which owned approximately 70 radio stations at that time. Sillerman sold SFX Broadcasting for $2.1 billion in 1998 but kept two small concert promoters and combined them into SFX Entertainment.

Sillerman's original idea was to consolidate concert promoters into a national entity in order to combat the overwhelming influence of Ticketmaster, which was already the largest ticket sales and distribution company in the US back then. In just four years since the launch, SFX Entertainment grew from a small US amphitheater company (amphitheaters were the easiest way for promoters to enter) into the largest live entertainment promoter.

On the wave of this resounding success, Sillerman sold SFX Entertainment to Clear Channel (iHeartMedia today) for $4.4 billion in 2000. SFX Entertainment (renamed to Live Nation later) was under Clear Channel's management for just several years and, following a corporate restructuring, spun off into a separate, publicly traded company in 2005. Live Nation has been public ever since.

Until 2010, Live Nation was predominantly a concert promoter. Promoters are those who arrange live music events and tours for artists, including events marketing, ticket selling, renting venues, and arranging for local production services (such as stages and equipment).

Promoters primarily earn revenue from the sale of tickets, and the promoter only makes money if enough tickets are sold to cover the guarantee. Different guaranteed payment formulas are used, which may include fixed guarantees and/or a percentage of ticket sales or event profits. These guarantees help promoters protect themselves against unprofitable events.

Back then, the ticketing side was handled mainly by Ticketmaster, which took most of the profits, leaving pennies for promoters like Live Nation. So, the only way to make money for promoters was sponsorship/advertising – offering advertising or promoting a brand, product, or service in a live music event or tour.

Live Nation CEO, Michael Rapino, really wanted to take a bigger piece of the ticketing business by creating its own ticketing system, which would also serve as a critical tool for marketing concerts.

He began by developing LiveNation.com into an entertainment portal, including ticket sales. He then tried to renegotiate an agreement with Ticketmaster, which was due for renewal in late 2008. Unfortunately, the negotiations led to a break up in early 2009 after ten years of partnership.

However, less than two months after the end of this partnership, the two companies announced a surprising merger to "build a better artist-to-fan direct distribution platform at the time when too many tickets go unsold and too many fans are frustrated with their ticket-buying experiences."

The merger was finally approved in the US only a year later, in January 2010. Ticketmaster had to sell Paciolan, the self-ticketing company it owned, and license its software to Anschutz Entertainment Group (AEG), allowing the latter to compete "head-to-head" with Ticketmaster. Additionally, Live Nation received a 10-year court order (which was further extended for five years) banning retaliation against venues that accept competing ticket contracts.

Since the merger, Live Nation has invested over $1 billion to improve the Ticketmaster system. Since 2010, the company built an entirely new, modern computing architecture, developed digital ticketing to eliminate fraud, created the Verified Fan service to get tickets to fans instead of ticket scalpers using bots, and invested millions in anti-BOT technology.

Today, Ticketmaster's performance in large on sales is the best in the industry (despite occasional slips like with Taylor Swift in 2022), it has the best marketing capabilities of any ticketing system, and it is by far the leader in preventing fraud and getting tickets into the hands of real fans vs. scalpers.

The merger of Ticketmaster was the first step in Live Nation's diversification strategy. The company began vertical expansion by becoming a venue operator. First, Live Nation started leasing (and later buying or operating) Amphitheaters, which are generally outdoor venues with 5,000 to 30,000 seats, used primarily in the summer and ideal for concert events.

Over time, the company added Clubs (indoor venues that are built primarily for music events and typically have a capacity of less than 1,000), Theaters (indoor venues that are built primarily for music events and typically have a capacity of between 1,000 and 6,500), Restaurants & Music Halls (indoor venues that offer customers an integrated live music, entertainment, and dining experience), Arenas (indoor venues that are used as multi-purpose facilities, often housing local sports teams, and typically have between 5,000 and 20,000 seats), Festival Sites (outdoor locations mainly used in the summer season to stage large single-day or multi-day concert events featuring several artists on multiple stages and can range from 10,000 to over 100,000 fans per day), and Stadiums (multi-purpose facilities, often housing local sports teams, and typically have 30,000 or more seats) to list of venues that it owns, leases, or operates.

As of the end of 2022, Live Nation owned, leased, operated, had exclusive booking rights for or had an equity interest over which it had a significant influence in 238 venues in the US and 100 venues globally.

Live Nation had pretty stable growth in the past decade, growing on average at 10%+ CAGR from 2010 to 2019. Going into 2020, the company had high hopes, with prominent artists planning tours and a record number of music festivals scheduled. The pandemic hit hard on Live Nation, putting a halt on essentially all concerts and sporting events worldwide. As a result, the revenues plunged in 2020, seeing an 84% fall compared to 2019. The stock lost more than 50% of its value in March 2020.

However, the company had seen such a speedy rebound that by December 2020, the stock returned to the pre-pandemic level and continued its further growth, hitting its all-time high (at that time) in early 2021. This growth was due to the rapid return of music events and the desire of millions of people to get out of their homes to socialize with others.

After just $1.8 billion in revenue in 2020, Live Nation delivered $6.26 billion in 2021 and $16.68 billion in 2022 (44.5% increase over pre-pandemic 2019). The company anticipates generating $20.19 billion in 2023, approximately a 21% increase compared to 2022, and continuing its growth in 2024 and beyond, though the growth is expected to slow down to mid-single digits.

Yet, it is not a pent-up demand; instead, it is a new cyclical growth for many years ahead. People are increasingly prioritizing experiences over goods, especially after COVID. Combined with other secular trends, Live Nation is well-positioned for continued growth and improved profitability, further cementing its position as the largest live entertainment company in the world, which annually issues over 500 million tickets, promotes more than 35,000 events, partners with over 1,000 sponsors, and manages the careers of 500+ artists.

Opportunity

Live Nation operates in several segments within the live entertainment business: live music events, music venue operations, management and other services to artists and athletes, ticketing services, and sponsorship and advertising sales.

The live music events segment includes concert promotion and music events/tours production. The music venue operations segment includes renting out venues for specific events on specific dates, as well as additional services such as concessions, parking, security, and ticket scanning at the gate. Artists/athletes management includes various services to manage their careers. Ticketing services generally refer to the sale of tickets primarily through online and mobile channels, as well as through phone, outlet, and box offices. Finally, sponsorship and advertising involve the sale of international, national, regional, and local advertising and promotional programs to a variety of companies to advertise or promote their brand, product, or service through venue naming rights, onsite venue signage, online advertisements, and exclusive partner rights in various categories such as credit card, beverage, travel, and telecommunications.

Trends

Music distribution change

Over the past few decades, the music industry has undergone a monumental shift. In the past, physical album sales dominated the industry, and artists relied heavily on them as a primary source of revenue. However, with the advent of digital streaming services like Spotify, the music distribution landscape has changed forever.

One of the most noticeable changes brought by this digital revolution is the changed revenue model for artists. The royalty payments from streaming services are often just a drop in the bucket compared to what artists made from physical album sales in the 1990s and 2000s. As a result, live performances have become a crucial source of income for musicians of all types. Today, around 90% of their earnings come from touring. This shift has led to an increased desire among artists to perform live, resulting in more extensive tours covering various countries and cities.

The evolution doesn't stop at the way fans now consume music. There's a noticeable trend in the release strategy of music. Instead of dropping full-length albums, like it was done in the past, a growing number of artists are now favoring the release of singles. Drake was the first major artist to successfully adopt this strategy, resulting in an industry-wide shift.

The approach of releasing singles aligns well with streaming platforms' consumption patterns. This allows for increased engagement with audiences and higher visibility in algorithm-driven playlists.

This and many other music streaming advancements have ripple effects on the concert and promotional segments. The enhanced global distribution of streaming services has broadened the horizon for artist discovery. A remarkable 61% of respondents in a recent survey done by Oppenheimer & Co. acknowledged that streaming platforms influence their desire to attend live music events, underscoring a symbiotic relationship between digital music consumption and live concert attendance.

This shows that streaming services today are less distribution channels and more tools for artist promotion and audience engagement. Artists can tap into a larger and more diverse audience base and promote live concerts more successfully.

Social media importance

Social media has had just as much impact on the music industry as streaming. In its essence, social media allowed the globalization of the artist. Artists now have a powerful channel to grow and engage with their followers, something that was not possible ~15 years ago.

Through social platforms like Instagram, Twitter, or TikTok, artists can share snippets of their lives, creative processes, and upcoming events. This organic interaction helps in not only creating a loyal fan base anywhere in the world but also in gathering invaluable data about where these fans are geographically located. Artists can then use these insights to plan tours based on the locations of their fanbases, ensuring better attendance and a more satisfying experience.

Additionally, the buzz created online before a concert or a tour significantly impacts the anticipation and attendance. Shares, likes, and comments on social media can help boost ticket sales and improve the overall success of live events.

Social media has also unlocked direct access to the artists. Artists can use social media as they use music streaming services to drop new singles or snippets of upcoming releases and reap millions of views just within hours.

Artists going global

The growth of social media and music streaming services enabled the artists' discovery at a global scale. Anyone today can learn about an upcoming artist from Colombia or India. Previously, these artists were only popular in their local markets, with some rare examples. Social media has changed it completely.

This enables an incredible pipeline of artists from other countries to perform on the biggest stage in the world – the US. And more and more local artists today are becoming world sensations.

Additionally, as artists can now go global faster and easier, increasingly more international markets want to become just like New York or Boston, hosting U2's and Beyonce’s of the world. This enables a tremendous growth of the live entertainment industry internationally.

Live entertainment growth

Live entertainment has seen significant growth in the last decade, with attendance growing at a 10% CAGR during this period. And there are no signs of it slowing down.

This category is difficult to disrupt. Replicating the live show is challenging, even with technologies such as AR/VR. While they promise a totally unique experience, they are unlikely to match the experience of physically attending the live show anytime soon, if ever.

Many feared the new generation would prefer video games over live concerts, but it is not playing out either. Music remains as important today as it was in previous decades. And with social media and music streaming services, music has become more accessible than ever and maybe even more popular, further helping the industry's growth.

And consumers really love live events. 67% of respondents said live concerts had been one of their life's most memorable events. With social media, 70% of consumers said they would go to the show just for a photo and video from the live concert.

Live concerts remain the second experience after traveling in many industry surveys, outpacing live sports, dining out, and various amusement parks.

This industry is also pretty recession-proof, with some exceptions, like the 2008 crisis and the COVID-19 pandemic. All current economic indicators for services are trending well as US consumption for services continues progressing towards its pre-COVID level.

According to Oppenheimer's estimates, live concerts will remain on a growth trajectory for the next several years at a minimum.

Total Addressable Market (TAM)

According to Live Nation's management, the live music market in 2022 was $12 billion in the US alone (where most of the live events took place). Market analysts expect the industry to continue growing (at about 5.3% CAGR) in the coming years to reach approximately $16 billion by 2028.

Live Nation has played a critical role in this market's rapid growth in the past decade. In 2005, it was just $3 billion. To fuel this growth, Live Nation has invested billions of dollars in funding artists globally – $9 billion in 2022 alone.

As of Q2 2023, Live Nation had approximately a 70% market share in the live music (concerts) segment. However, this does not include ticketing and sponsorship/advertising, which are multi-billion segments on their own and also growing in mid-single digits year over year.

Growth Drivers

Live Nation had two incredible years of triple-digit revenue growth following the 84% collapse in 2020.

Analysts covering the company expect the revenue growth to decelerate starting in 2024 and be in the high single-digits going forward.

Live Nation's show pipeline (which is up double-digits) for 2024 assures the strong consumer appetite for concerts despite some macro difficulties. The company is seeing continued growth in the show count, which should lead to continued growth in attendance.

The company expects a record number of fans in 2023 (over 117 million tickets were sold as of Q2 2023). Over the next several years, the goal is to grow to over 175 million.

Growing attendance is the company's top priority as it will accelerate the Adjusted Operating Income (AOI) levels with increasing per-fan profitability onsite, increasing sponsorship, and increasing ticketing business.

Oppenheimer's recent survey indicates that 89% of respondents plan to attend a concert in 2024, with 83% planning to spend the same amount or more on tickets, which in 63% of cases is under $300, an amount that is less sensitive to macro weakness.

However, growth in shows and the number of fans attending them is one of many growth opportunities for the company. Below are the key growth drivers for the next ten years.

Pricing of tickets in the primary market

The primary ticketing market is generally mispriced to the low end. The tickets then enter the secondary market, where they can be sold much higher, sometimes five to ten times higher.

Regulators currently discuss this issue, but regardless of the outcome, there is certainly a growth opportunity in increasing the price of tickets in the primary market.

Upgrading experience

Live Nation's primary goal is to maximize attendance, which requires offering the kind of consumer experience that will build lifetime fans. Better experience equals more tickets sold.

Current music venues are pretty generic and not built for premium hospitality, unlike sports venues, for example. But more and more consumers want that premium hospitality in music concerts as they get in sports events. When people have one time in a life opportunity to see Beyonce or Taylor Swift, no matter what income group they are, they are willing to spend to have the best experience.

Michael Rapino, Live Nations' CEO, believes it is the biggest growth opportunity for the company. Live Nation can upgrade or upsell the current, already massive base of fans. And the company is currently in the first inning of doing this. Right now, 99% of Live Nations’ business is general admission, and only 1% is VIP, providing so much room for development here.

The company is now actively working on its venues and venues for festivals to see how it can upgrade the experience. And this is not about a complementary cocktail but about truly making a unique experience, like providing backstage access or getting an artist's signature.

Growing venues business

Live Nation has been in the venue business since its inception. During the COVID year, the management started to alter its venue strategy. Under the new Venue Nation strategy, the company created a dedicated development team and made incredible progress since then.

Traditionally, developers were in charge of venues, and more of them have prioritized live venues over movie theaters in recent years.

But Live Nation's management realized the value of its content and decided to operate its own venues, cutting out the middleman, which offers the best return on capital for the company and long-term growth opportunities.

However, the US was always packed with venues. In recent years, many sports venues have been launched throughout the entire country. These venues can easily be transformed into live concert venues.

The company found one location, in Austin, where there was no arena. Management spent $350 million to build an arena that has everything, from boxes and premium seats to advertising/sponsorship spots and arena name/title. It was a rare find and a lucky one. There will not be that many such opportunities within the US.

So, the real opportunity is in international markets. Most large cities in Europe and Latin America have beautiful soccer arenas but no venues for live events, or those venues are extremely old. So, Live Nation enters these cities and, in most cases, builds new arenas for live events and, in some cases, upgrades the old ones.

Latin America, Asia, and more European cities (the company already owns Ziggo Dome in Amsterdam, 3Arena in Ireland, Royal Arena in Copenhagen, and one arena in Lisbon) are the highest priority for the Venue Nation strategy.

Live Nation has been very successful in Asia, particularly in Japan and South Korea. In South Korea, Live Nation ended up being a promoter of BTS, the most popular Korean music band known worldwide.

In 2022, the company won many bids for arenas because of its unique approach: Live Nation not only builds the arenas but also fills them with events, something that most developers can't do.

Currently, there are 75 arenas in the company’s pipeline, which will take several years to build or modernize. These venues are supported by a strong balance sheet and will provide better margins and control over the entire process in the long term. Own venues enable the company to grow sponsorship and onsite spending.

Live Nation will become the largest live events venue owner in the next decade, further cementing its position as the world's number one live entertainment company.

International growth

International growth will come not only by launching and operating new venues. Since Live Nation, at its core, is a promoter, its primary business remains working with artists.

For 50 years, Western artists mainly played in the US and Europe as it was expensive to move around with large crews and instruments. Now, this is changing: artists are moving beyond the US and Europe and charge the same as they will in the primary markets as the demand is there.

For instance, in 2022, Live Nation put 10 concerts in Argentina (amid considerable inflation happening in the country). All shows were sold out. The best part is that economics were similar to if, let's say, Coldplay would give 10 concerts in Detroit. Just a few years ago, going international was not economically viable for most artists. But today, Live Nation can make the same money in other markets as it can make domestically.

As a result, international acts doubled representation in the company's top 50 tours over the last five years, with more acts touring globally and visiting 42% more countries.

Live Nation is using an incredibly successful playbook for expansion to new markets: first, it comes as a promoter, then it sets up a festival in the new city, brings Ticketmaster as a ticketing provider, and attracts sponsors for this festival.

For instance, in Brazil, Live Nation launched Rock In Rio, a recurring music festival that now also takes place in Lisbon, Madrid, and Las Vegas. The launch of this festival was wildly successful, so now Live Nation has a great touring business in the country, continuously bringing international artists there. The company established the local office in Brazil and just launched the sponsorship business and the full ticketing service there.

Latin America is indeed on fire. This region is up about 35% YoY so far in 2023, with roughly 10 million fans already. But this is just a tiny piece of a massive opportunity in the region, where music traditionally has been popular among all demographics. Live Nation is currently actively expanding in this region, following its playbook in one city after another.

Sponsorship growth

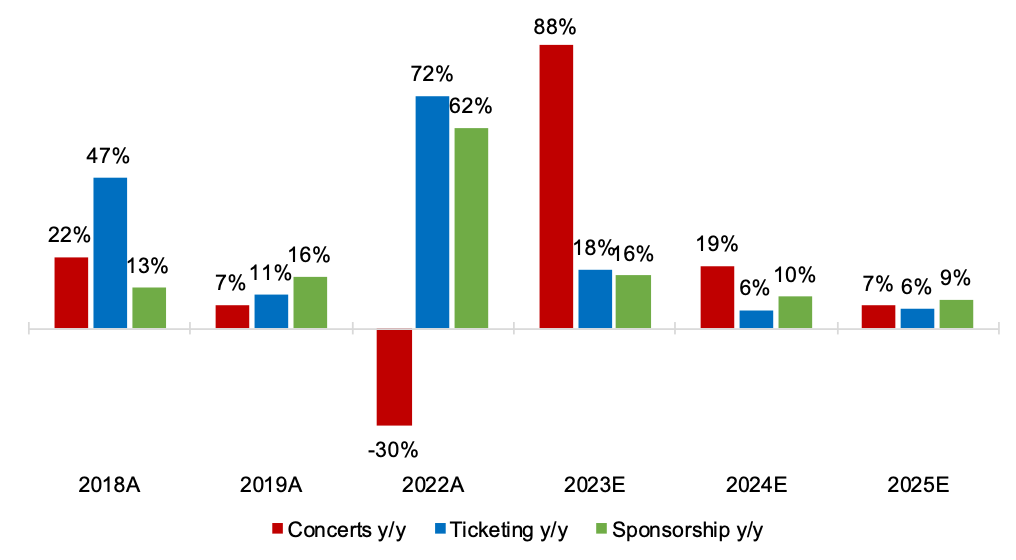

Live Nation's global footprint is one of the world’s largest music advertising networks. Despite the macro environment and tough advertising market, the company has not seen a slowdown in this business. This segment continues to grow, showing a 25% increase in H1 2023 compared to the same period last year.

The company has over 90% of the expected revenue for the year already booked, driven by many large multi-asset, multi-million dollar sponsors (100+ brands) that have long-term agreements with Live Nation and keep buying more ads. In total, the company works with over 1,000 different sponsor brands from literally every category. Among sponsors are Diageo and Chateau St. Michelle, Salesforce and Gildan, and many other well-known brands.

More and more brands shift some of their dollars from other categories to the event space, where they can get direct consumer interaction they can't get elsewhere. So, this segment continues to grow without any signs of slowing down, and as soon as most primary markets exit the pre-recession stage, it could find another substantial growth leg. Analysts covering the company expect this segment to grow the most past 2024.

Sponsorship business also supports higher FCF conversion. It carries 61% AOI margins, and segment AOI is up 88% compared to 2019, translating to improving FCF/AOI conversion (~61% in 2023 vs. 53% in 2019).

Business Model

Live Nation has a pretty diversified business model with three reportable segments: Concerts, Ticketing, and Sponsorship & Advertising.

The Concerts segment predominantly involves the promotion of live music events in company-owned or operated venues and in rented third-party venues, as well as the operation and management of these venues, the production of music festivals across the world, the creation of associated content, and services related to the management and support of artists.

The company generates the majority of its total revenue from this segment. In 2022, 80.9% of total revenue ($13.5 billion) came from Concerts. In H1 2023, the share remained pretty unchanged (about 79% of total revenue).

The Concerts segment of the company operates throughout the year, but it experiences a surge in revenue during the second and third quarters. This increase in revenue is primarily due to the seasonal nature of the shows that take place at outdoor amphitheaters and festivals, which are more frequent from May through October. These outdoor shows and festivals attract a large audience and provide a unique experience for attendees. As a result, the company primarily focuses on maximizing its revenue during this period by scheduling popular artists and promoting events through various channels.

As a promoter, Live Nation earns revenue largely from the sale of tickets. This revenue is determined by several factors, such as the number of events held, the volume of tickets sold, and the price of the tickets. The more events the company holds, the higher the revenue. Similarly, if the volume of ticket sales is high, the revenue generated will also be high. Moreover, ticket prices play a crucial role in determining revenue, as higher-priced tickets generate more revenue per ticket sold.

As a venue operator, Live Nation generates revenue primarily from selling concessions, parking, premium seating, rental income, and ticket rebates or service charges earned on tickets sold through its internal ticketing operations or by third parties under ticketing agreements.

The Concerts segment still operates at a loss (even at its peak, though the loss has been significantly lowered, from $111.8 million in H1 2022 to just $5.9 million in H1 2023), but it is an integral part of Live Nation's business. The other two segments provide the company with operating income.

The Ticketing segment is primarily an agency business operated by Live Nation that sells event tickets on behalf of its clients and retains a portion of the service charge as its fee. Live Nation sells tickets for its own events and also for third-party clients across multiple live event categories (beyond just music), providing ticketing services for leading arenas, stadiums, amphitheaters, music clubs, concert promoters, professional sports franchises and leagues, college sports teams, performing arts venues, museums, and theaters.

The Ticketing business generated $2.2 billion, or 13.4% of the total revenue during 2022. While the company sold more than 500 million tickets, it only received fees for approximately 281 million.

Live Nation (Ticketmaster) does not set ticket prices, does not decide how many tickets go on sale and when they go on sale, and does not set service fees. Artists and their teams determine pricing and distribution strategies, and while Ticketmaster provides support for these decisions, Live Nation does not use algorithms to set prices. In most cases, venues set service and ticketing fees, and most of those fees go to the venue, not to Ticketmaster. For years, the portion of the service fee that Ticketmaster retains has been falling, and the venues' share has been increasing.

Live Nation also offers ticket resale services (secondary ticketing) through its integrated inventory platform, league/team platforms, and other platforms internationally.

Ticketing revenue increased 31% to $1.4 billion during the first half of 2023, primarily due to higher primary and secondary sales volumes and upward pricing momentum due to higher demand and artist mix. Ticketing also achieved a 33.1% operating margin in the first half of 2023, compared to 31.6% in the first half of 2022.

Finally, the Sponsorship & Advertising segment employs a sales force that creates and maintains relationships with various sponsors and allows them to reach customers through concerts, festivals, venues, and ticketing assets, including advertising on Live Nation's websites. Many of the company's venues have naming rights sponsorship programs, too.

This segment generated $968.1 million, or 5.8% of the total revenue during 2022. In the first half of 2023, the revenue from the Sponsorship & Advertising segment increased 25% to $473 million, primarily due to new venue sponsorships and increased activity in international markets. Sponsorship & Advertising operating profit was $251 million, representing a 53.2% operating margin, down from 60.1% in the first half of 2022.

Gross Margin

Live Nation's gross margin has been pretty stable in the past several years at ~26%, with a slight spike in 2021 (~31%).

The company may see some minor margin expansion in the coming years as it continues to increase the per-fan profitability across all of the different venue types, including in third-party buildings where the margin is generally lower. Additionally, the company tries to drive down the average operating cost per fan, which also positively impacts the gross margin. But in the near term, the gross margin will still remain at a ~26% level.

Live Nation traditionally sees gross margin lower in the second half of the year due to more costs associated with contract renewal cycles and other factors.

Financial Snapshot

Based on Q2 2023

Revenue

Actual:

2022 – $16.68 billion (+166.1% YoY)

Q2 2023 – $5.63 billion (+26.98% YoY)

Estimates:

2023 – $20.19 billion (+21.1% YoY)

2024 – $21.73 billion (+7.6% YoY)

Operating Expenses

2022 – 21.5% of total revenue

Q2 2023 – 19.3% of total revenue

Total operating expenses as a percentage of total revenue have returned back to historical levels after elevated operating expenses during the COVID year and its aftermath in 2021.

In fact, in 2022, the company saw the lowest operating expenses as a percentage of total revenue in its history (21.5%).

Stock-based compensation (SBC)

2022 – 0.66% of total revenue and 0.55% of the market cap

H1 2023 – 0.63% of total revenue and 0.27% of the market cap

Since going public, Live Nation increased its shares outstanding by 260%, while its stock price has appreciated by 383%. Most of this came after a merger with Ticketmaster in 2010. In the past ten years, the company increased shares outstanding only by 15.5%, while the stock price grew by 343%.

Profitability

The company returned to GAAP profitability in 2022 after two years of net losses occurred due to the pandemic. The company generated $296 million in net income in 2022, compared to a loss of $650.9 million in 2021, a loss of $1.72 billion in 2020, and a net income of $69.9 million in 2019.

Analysts expect a significant acceleration (>30% CAGR) of positive earnings in the next five years. The company is forecasted to reach $1 billion in net income by the end of 2027.

Balance Sheet

As of Q2 2023, Live Nation had $7.1 billion in cash and cash equivalents, including $1.4 billion in ticketing client cash and $2.3 billion in free cash.

The company's current long-term debt is $8.77 billion, including $6.55 billion in long-term debt, $1.65 billion in long-term operating lease liabilities, and $562 million in other long-term liabilities.

Approximately 87% of this debt is at a fixed rate, with an average cost of debt of 4.7%

Cash Flow

Live Nation generated $966 million in free cash flow (FCF) in 2022 and $406 million in the first half of 2023. The company will exceed $1 billion in FCF by the end of 2023.

Free cash flow is then projected to grow at ~9% CAGR in the next several years. However, as a percentage of AOI, it will decline 68.7% in 2022 to ~60% for the next several years.

Competitive Advantages

Competition

Although Live Nation (and its subsidiary Ticketmaster) is often accused of having a monopolistic share of the market, the reality is that the company operates in a competitive environment. There are several players in the market that are trying to grab a share of the live entertainment and ticketing industry away from Live Nation/Ticketmaster.

Today, the competition for every ticketing contract that goes out to bid is intense like never before. Companies like SeatGeek (especially), AEG’s AXS, and Eventbrite are taking away many contracts that Ticketmaster previously had or winning new over Live Nation/Ticketmaster.

While Live Nation may have the number one position in the primary ticketing market, it has been losing its share in the secondary ticketing market to StubHub and Vivid Seats — and more competitors are also emerging for primary ticketing contracts, especially SeatGeek.

The competition is also significant in the Concerts segment, with competitors like The Madison Square Garden Company (engages in live sports and entertainment businesses, owning and operating a portfolio of venues, sports teams, and entertainment productions), AEG (a sports and live entertainment company with a network of over 120 clubs, theaters, arenas, and stadiums), and C3 Presents (an event company that creates and produces large-scale live events, including music festivals and concerts).

Competitive Advantages

The merger of Live Nation and Ticketmaster resulted in the formation of an industry giant that wields significant influence over various aspects of the live entertainment industry, such as ticket sales, promotions, and venue operations. Due to their size, they are able to negotiate favorable terms with venues, artists, and other stakeholders.

Over the years, these two companies have worked together to create the largest network of venues, promoters, and artists in the industry. This network allows them to provide a diverse range of events and tickets to live entertainment fans, making them a popular platform for many.

Live Nation/Ticketmaster has successfully obtained exclusive contracts with many venues and artists, forcing consumers to use their platforms to gain access to tickets for highly sought-after events. These exclusive arrangements effectively create a barrier to entry for competition, resulting in a significant boost to Live Nation/Ticketmaster's overall market share. No wonder the United States Department of Justice is trying to break these two companies.

Live Nation was built for artists in the first place. The company has the best-in-class operation. Pre-planning here is the key. When an artist comes to Live Nation, data and depth in expertise come into place. Live Nation has all this information to understand how many concerts to play, where, and how much to charge in each city – all to help the artist make the most money and have the best return on investment. Mapping the global plan based on real data is one of the company's strongest competitive advantages.

Selling tickets is the most critical part of a successful tour, and while Ticketmaster may not be the best platform out there, Live Nation has been investing billions in making the Ticketmaster ecosystem the most advanced in the industry.

Despite a lot of controversy surrounding the company, increasingly more artists are choosing Live Nation to work with. The company, first and foremost, ensures the artist is safe on tour and then provides everything else needed. As of the end of 2022, Live Nation globally had over 90 managers providing services to more than 410 artists.

Risks

Live shows business is cyclical. After record years (2022 and 2023) for live shows with the world's most successful artists touring, the growth in coming years will significantly decelerate. Revenue is expected to grow only in high mid-single digits starting in 2024.

The problem with a large number of bots constantly trying to crash into Live Nation's verified fan system and getting tickets for resale on the secondary ticketing market;

The potential lawsuit by the Department of Justice that could breakup Live Nation and Ticketmaster due to alleged anticompetitive conduct, including high fees, extended contracts with artists, and retaliation against venues;

The company is highly affected by broader market and economic conditions, including fluctuations in consumer spending on entertainment, the state of the global economy, and potential impacts from unforeseen events like pandemics or wars;

Increased competition in the ticketing business;

In the secondary ticketing market, the company has restrictions on its business that are not faced by competitors, imposed as a result of agreements entered into with the Federal Trade Commission, the Attorneys General of several individual states, and various international governing bodies.

A large amount of debt, which exceeds the cash reserves.

Additional Sources

Management – https://www.livenationentertainment.com/leadership/

Board of Directors – https://investors.livenationentertainment.com/corporate-governance/board-of-directors

Ownership – https://www.sec.gov/Archives/edgar/data/1335258/000133525823000046/lyv-20230426.htm#if93576b595fd48de92ca94f57609c685_73 (page 21)

Have a great week.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.

Great writeup, thanks for sharing. Any thoughts on CTS Eventim? I'm surprised that CTS wasn't mentioned in concert or ticketing competition sections. Thanks