Part 2: Deep dive on Expedia ($EXPE)

In order to read this deep dive writeup on Expedia (EXPE) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber then I thank you for your support. Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +37.2% YTD), my daily activity, my investment models and my daily webcasts.

In addition to my newsletters and my podcast, I also run a Stocktwits room where I post about both of my portfolios/strategies plus you get my morning newsletter and my daily webcasts.

Company: Expedia Group

Ticker: (EXPE)

Website: Expedia.com and ExpediaGroup.com

IPO date: November 10, 1999 (first time)

IPO price: $14.00

Stock price at the time of writing: $93.54

Outstanding shares: 148.1M (142.6M Class A shares and 5.5M Class B shares)

52 week high: $178.02 on May 02, 2022

52 week low: $82.39 on December 22, 2022

ATH: $213.80 on February 16, 2022

Market cap: $13.853 billion

Net cash/debt: -$1.493B

Enterprise value: $15.346B billion

Headquarters: Seattle, Washington, United States

Number of employees: 16,500+

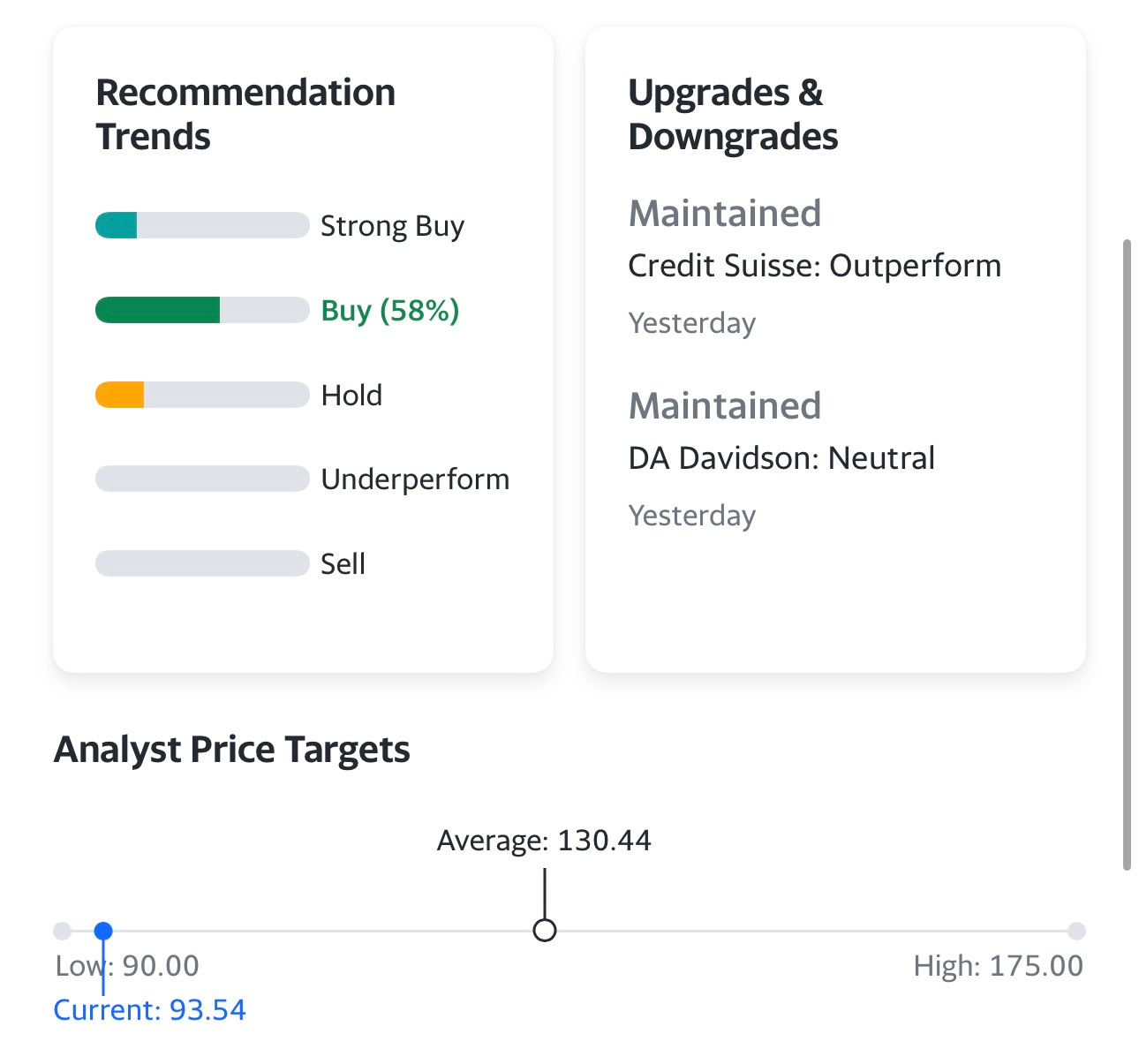

Average price target from analysts: $130.44 or 39.4% upside

Next earnings call (Q2 2023): TBD

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Investor Presentation June 2022 [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 2]

In case you missed part 1 of the EXPE writeup you can read it here..

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

As I mentioned in part 1 of this writeup, I do have a 1.5% position in EXPE and I’m willing to add on any pullbacks given the strong Q1 earnings report and the current valuation which is very compelling in my opinion.

EXPE was down 2.39% today but that’s probably because of ABNB’s disappointing report and concerns about slowing growth which BKNG and EXPE don’t seem to see. Even though I put all three of these companies into the same bucket I do like BKNG and EXPE more because they are asset light but also because they touch multiple aspects of the travel industry from transportation to accommodations and EXPE even owns VRBO which is a competitor to ABNB so you’re getting some exposure to the long-term stay market.

In my opinion ABNB was a bigger beneficiary of the late-stage-pandemic and post-pandemic surge in travel demand for two main reasons:

towards the end of the pandemic people wanted to stay in private homes/condos rather than hotels but now that the pandemic is behind us some of those people are coming back to the hotels because they typically have better amenities and better locations without the big cleaning fees

ABNB was a bigger beneficiary of the WFH (work from home) trend as companies were allowing their employees to work from home or anywhere but that’s starting to change and some companies are forcing their employees back to the offices either full time or part time but it means less people doing the WFH thing through ABNB

Valuation

I would not call EXPE a growth stock, it’s definitely more of a value stock — with low double digit to high single digit growth expected for this year and the next few years you’re not buying this company for the revenue growth… you’re buying it for the profits, free cash flow and buybacks that should happen over the next few years.

When I did part 1 of this writeup the enterprise value (EV) was around $15.3 billion so that’s what I use for this section however the stock is down 2-3% over the past few days so the EV is technically a little lower now which means valuation just got even more attractive.

Using that $15.3B enterprise value, EXPE is currently trading at:

5.5x 2023 EV/EBITDA and 4.9x 2023 EV/EBITDA

10.8x 2023 EV/NI and 8.9x 2024 EV/NI

6.5x 2023 EV/FCF and 5.8x 2023 EV/FCF

If you look at net income for the next two years (2023 and 2024) it’s expected to grow at 31.6% in 2023 and 21.2% in 2024 however the stock is only trading at 10.8x 2023 EV/NI which means EXPE is trading with a .34x PEG ratio which is insanely cheap. Lots of large cap tech companies are selling with PEG ratios above 1.0x and some are even trading with PEG ratios above 2.0 so EXPE looks dirt cheap compared to 90-95% of the companies in the S&P. It’s almost impossible to find any other companies growing earnings by 20-30% while trading at just 10x earnings/net income. This definitely makes EXPE a great risk/reward stock at these prices and even if we run into a recession I would expect EXPE to drop much less than BKNG and ABNB because EXPE is starting from a much lower P/E multiple.

BKNG is growing revenues slightly faster than EXPE but earnings slightly slower so let’s call that a wash — with that said BKNG currently trades at 19x EV/NI and if you stuck a 19x multiple on EXPE’s 2023 net income estimates of $1.411B then subtracted their debt and divided by 148.1M shares you’d get a $171 stock price which just proves how undervalued EXPE has gotten compared to BKNG.

Investment Model

The numbers in my investment model are pretty similar to what the analysts have, assuming EXPE can get to $17+ billion in revenues by 2027 with 14% net income margins… take those numbers and throw on a 13.5 P/E multiple plus the cash they’ll generate over the next 4 years (assuming they don’t do buybacks) and you get a $250 stock in 4 years which is 174% upside from today’s closing price. Obviously if revenues come in lower and/or net income margins come in lighter than it’s very possible EXPE doesn’t hit my price targets.

I still think EXPE can get to $250 per share by 2027 (it was a $218 stock just 15 months ago) but it’s more likely that EXPE uses all that FCF over the next 3-4 years to buyback 30-40% of the outstanding shares which means net income and EPS would come in much higher than current estimates but they’d obviously have less cash on the balance sheet as a result. Personally I love owning companies that do stock buybacks, these are usually some of the best performers over the long term. The only time I don’t like buybacks is if the company is able able to invest in their current business to increase revenues/earnings or they have the opportunity to make smart, strategic acquisitions. Just think back 11 years when Facebook bought Instagram for $1 billion, what if they had used that $1 billion to buyback stock instead of buying Instagram? The current market cap of Facebook/Meta would probably be 50% lower so acquisitions can add a ton of value over the long term if done correctly.

If these numbers are too small here’s the link to my EXPE investment model [click here]

Analysts

Overall the analysts are mostly bullish on EXPE with approximately 60% having buy or strong buy recommendations with the rest having neutral ratings and no sell ratings. Average price target is $127.92 which is ~40% higher than the current price.

Technicals

This top chart just shows what EXPE has done over the past year, since the all time high last February the stock is down 58% despite the fundamentals holding up well and the travel company CEO’s sounding optimistic about the industry and their own businesses but we know they can’t predict macro or a possible recession so that’s something we need to keep an eye on.

This bottom chart shows what EXPE has done since October, it’s current below most of the moving averages so a trader would tell you to wait until EXPE at least reclaims the 50d ema/sma or the 200d ema/sma but if you’re an investor an like EXPE at the current prices/valuation there’s no reason you can’t start buying here but my concern would be if EXPE can’t hold those recent lows at $89.00 so if the stock breaks below that level you might want to cut your losses and put the capital elsewhere. Even though I have a position right now doesn’t mean I’m going to ignore bad price action and fight the markets — my conviction is not higher enough to do that. Last year I was averaging down on stocks like CELH, SWAV, LNTH, MELI, UBER, CROX, FOUR, TMDX and several others which paid off for me but those were higher conviction positions. Since EXPE is already trading with .35x PEG ratio, if the stock dropped below $89 there’s a chance I’d just keep holding, at that point EXPE would be trading at 5x EBITDA which just seems too cheap to sell unless I thought there was an incoming recession in which case I don’t think EXPE would be worth holding.

Conclusion

I’ll continue holding EXPE for now and will add on pullbacks, at least through Q2 earnings because I expect the summer travel season to be a strong one which means EXPE should be in good shape especially at the current multiple/valuation. With inflation coming down and unemployment at 3.4% it doesn’t look like the recession is coming anytime soon which makes me think EXPE should hit their numbers for 2023 which should get us some multiple expansion on the stock. If EXPE really grows net income by 30% or more this year and 20% next year than there’s no way this stock could be trading at 10.8x 2023 net income estimates right now. We could/should see that multiple expand by at least 50% in the next 6-12 months which means the EXPE should be trading at $135+ in the next 6-12 months, possibly even higher if we avoid a recession.

Here’s a bonus thought: I actually think it would make some sense for UBER to buy EXPE and here are a few reasons why:

Dara (CEO of UBER) is the former CEO of Expedia so he knows the company/industry very well, if anyone was going to spearhead the acquisition of EXPE there’s nobody else better equipped to do so

UBER has already shown they want to get into the travel booking business with the recent launch of this service in the UK

EXPE is a cheap stock with a 13% FCF yield which means it would be an accretive acquisition for UBER

Transportation is a big part of traveling so combining these companies makes sense for the customer

If you combined these companies, they’d do $56-60B of revenues in 2024 with $6-7 billion of free cash flow, throw a 25x multiple on that (given FCF growth rates) and you have a $160+ billion company (not including their debt)

Additional Sources

Leadership [click here]

Ownership, page 47 [click here]

I’m sure I’ll discuss EXPE from time to time on my daily webcasts so hopefully you watch some of them.

Enjoy the rest of your week!!

As a reminder, you can track my investment portfolio and my activity as well as watch my daily webcasts through this spreadsheet [click here]

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.