Part 1: Deep dive on Expedia ($EXPE)

Part 1: Deep dive on Expedia ($EXPE)

In order to read this deep dive writeup on Expedia (EXPE) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber then I thank you for your support. Paid subscribers receive 3-4 deep dive writeups per month plus they get full access to my current investment portfolio (up +37.2% YTD), my daily activity, my investment models and my daily webcasts.

In addition to my newsletters and my podcast, I also run a Stocktwits room where I post about both of my portfolios/strategies plus you get my morning newsletter and my daily webcasts.

Company: Expedia Group

Ticker: (EXPE)

Website: Expedia.com and ExpediaGroup.com

IPO date: November 10, 1999 (first time)

IPO price: $14.00

Stock price at the time of writing: $93.54

Outstanding shares: 148.1M (142.6M Class A shares and 5.5M Class B shares)

52 week high: $178.02 on May 02, 2022

52 week low: $82.39 on December 22, 2022

ATH: $213.80 on February 16, 2022

Market cap: $13.853 billion

Net cash/debt: -$1.493B

Enterprise value: $15.346B billion

Headquarters: Seattle, Washington, United States

Number of employees: 16,500+

Average price target from analysts: $130.44 or 39.4% upside

Next earnings call (Q2 2023): TBD

Investor Relations [click here]

Q1 2023 Earnings Report [click here]

Q1 2023 Earnings Call Transcript [click here]

Investor Presentation June 2022 [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 2]

Part 2 should be out in the next couple days.

As a paid subscriber you have access to my…

Investment portfolio [click here]

Investment models [click here]

Daily webcasts [click here]

Introduction

Disclosure: I started a small position (1.0%) in EXPE on April 13th, 2023 at $91 and then added a few times over the past couple weeks so my cost basis is $90.40 and the position is currently at 1.5%

EXPE reported earnings this past week (Thursday, May 4th) and they were slightly better than expectations so the stock was up 4.9% yesterday although it was up as much as 9.6% before fading off the highs.

When I stared a position a few weeks ago EXPE was down 59% from the highs last March 2022 and I felt like it had just gotten too cheap especially when you look at their potential earnings and free cash flow for 2023. As you can see from the charts below (the top is linear scale and the bottom is log scale), the stock has been in a downtrend for the past year but might be on the verge of breaking out.

Let me be clear, I own EXPE right now because I think the valuation is extremely compelling and I love the FCF yield however if it looks like the US economy is going into a bad recession then EXPE is probably not a great stock to own however it’s still possible we could avoid any recession given that inflation is coming down, the FOMC is almost done with their rate hikes, corporate earnings are holding up well and the unemployment rate is still below 3.5%

…but, with that said, there are still some major concerns under the surface like the lag effects from 500+ bps of rate hikes, the credit tightening that will ensue from the recent bank failures, the inverted yield curve, the FOMC going too far, the potential landmine in commercial real estate (CRE) and some more but I’ll leave it there for now.

I have no idea if the US will be in a recession later this year or early next year, I still think it’s possible we don’t get one or if we do it’s shallow and short lived so perhaps EXPE is being valued like we’re getting a deeper recession which means there’s too much fear/pessimism being priced in.

EXPE is a travel industry company, competing with companies like BKNG and ABNB which are both great companies and lots of reasons to like them as well but I put together this chart comparing the valuations/multiples for each of them and it’s pretty clear the EXPE looks the most attractive. The FCF yield for EXPE is almost unheard of outside of energy and shipping which are both extremely cyclical industries so those companies tend to trade at much lower multiples.

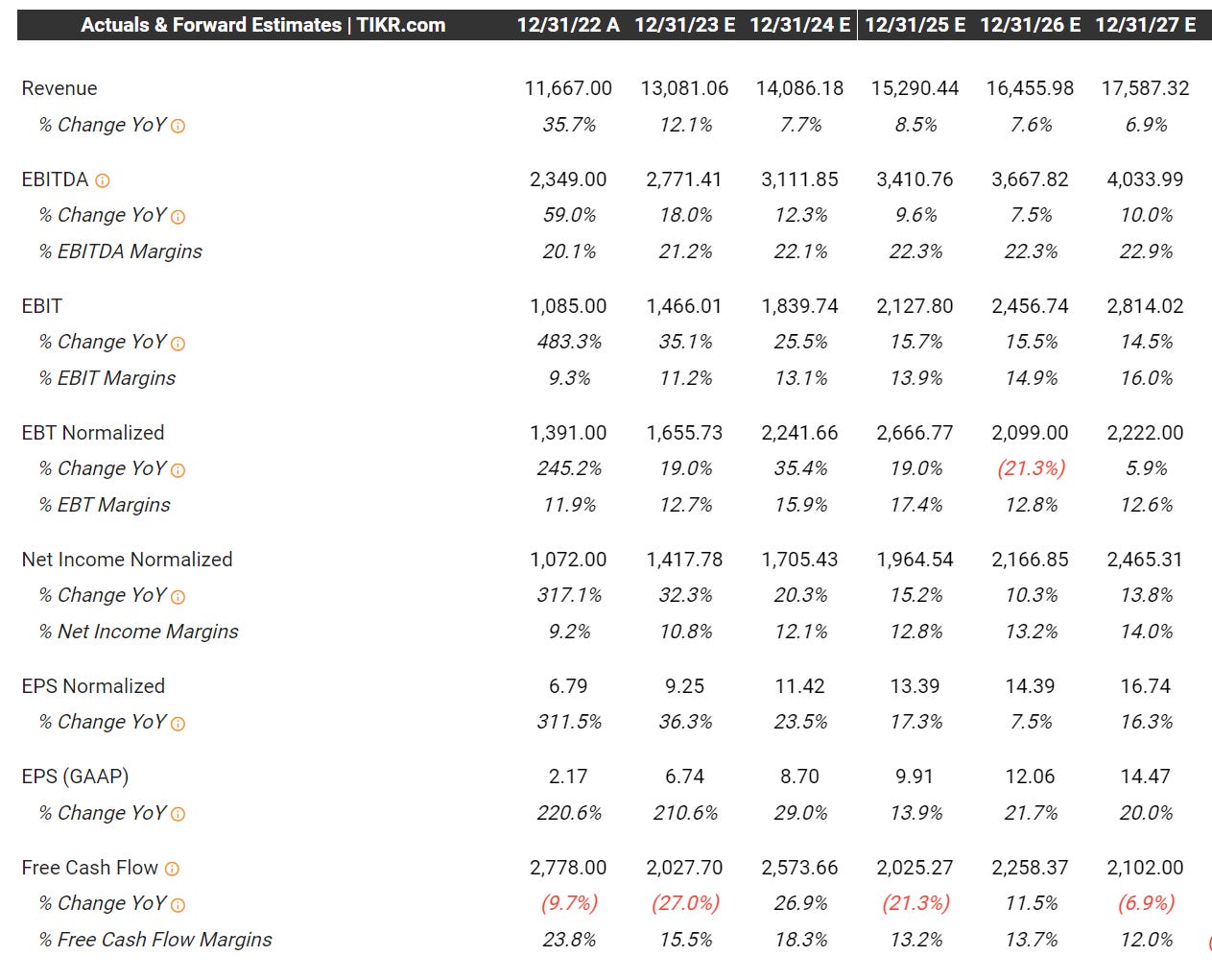

When you look at EXPE’s financials please keep in mind they are very lumpy whereas the majority of free cash flow comes in the first half of the year and the majority of earnings/EPS comes in the second half of the year. That’s why you should not base your valuation multiples on quarterly results but instead look at the full year estimates, for example EXPE did $2.9B of FCF in Q1 but they’ll probably have negative FCF the rest of the year but should generate at least $9 of EPS over the next 3 quarters which means the stock is trading at just 10.8x earnings, even when you include their debt.

As you can see from the consensus estimates below, nobody is expecting EXPE to be a hypergrowth company but they have double digit EPS growth and great margins which means they generate a ton of cash which should go towards buying back stock over the next few years.

EXPE should have $9-10 billion of net income from 2023 through 2027 which they could use to buyback 20-60% of the outstanding shares which would boost future EPS numbers. If they’re not buying back stock then it probably means they’re returning capital to shareholders through a quarterly dividend (which would also be fine although I prefer buybacks) or perhaps they’re doing acquisitions which might also make sense assuming they add growth to the top line while being accretive to earnings within a couple years.

Here’s the scenario that could play out over the next 3-4 years… right now EXPE has 148.1M shares outstanding but let’s assume they buyback 1/3 of them over the next 4 years and EXPE still does $2.465B of net income in 2027, well now you’re dividing that number by 112M shares (assuming 2.6% annual dilution from SBC — way too high but that’s a different discussion), which means that 2027 EPS number is $22 instead of $16, throw a 13x multiple on $22 and you have a $286 stock — sounds good to me!!!!

Here’s my current investment model for EXPE which I’ll continue to update quarterly [click here]

To be honest I’m not exactly sure why EXPE continues to trade at half the multiple of BKNG with similar margins and growth rates. It’s very possible they are both solid stocks to own for the next few years but given the current discount that EXPE is trading at I think it provides more upside for investors which is why I’d own EXPE over BKNG and/or ABNB but like I said earlier, if it looks like we’re going into a deep and prolonger recession than you’d probably be best to stay away from the travel stocks.

This is very speculative but given that EXPE is still down more than 55% from the highs last year (Feb 2022) and the current valuation, multiples and FCF yield are all extremely attractive I would not be surprised if we saw private equity come after EXPE at these prices. They could easily justify paying $125+ per share which is still a discount to BKNG’s current multiple which trades at 13.6x EV/EBITDA; if private equity paid $125 for EXPE it would only be 6.7x 2023 EV/EBITDA (not including their debt) — seems like a no brainer to me.

Company Background

Expedia was launched back in 1996 by Microsoft as one of its divisions. It marked the entry of Microsoft as the first major technology player into the online travel market, which was just getting started at that time.

Back in the day, reservations were held either by travel agencies or made directly with hotels, airlines, and car rental companies. The booking process was primarily made offline (by phone), which was time-consuming, inflexible, and inconvenient.

With the Internet becoming more available and adopted by the masses, the industry began moving online. Online travel agencies (OTAs) started to emerge. Travelocity (now owned by Expedia Group) became the first OTA ever. Expedia was launched just several months later.

At launch, Expedia allowed travelers to book air, car, and hotel reservations online and browse a library of in-depth multimedia travel guides. Purchasing travel online via a credit card at any time of the day, seven days a week, was quite disruptive back then and has changed the travel industry forever.

By the time when Microsoft spun off Expedia into a separate, public company, Expedia had 7 million registered users and was affiliated with more than 450 airlines and 40,000 hotels, becoming one of the most popular travel booking websites, alongside Travelocity and just launched Priceline (now Booking Holdings).

Expedia became a public company for the first time in 1999 before it was bought out entirely by IAC/InterActiveCorp (also owned Match Group) in 2003. The company stayed private for two years before IAC spun off its entire portfolio of travel businesses (including Expedia, Hotels.com, and Hotwire) into a new publicly traded company. Expedia stayed public ever since.

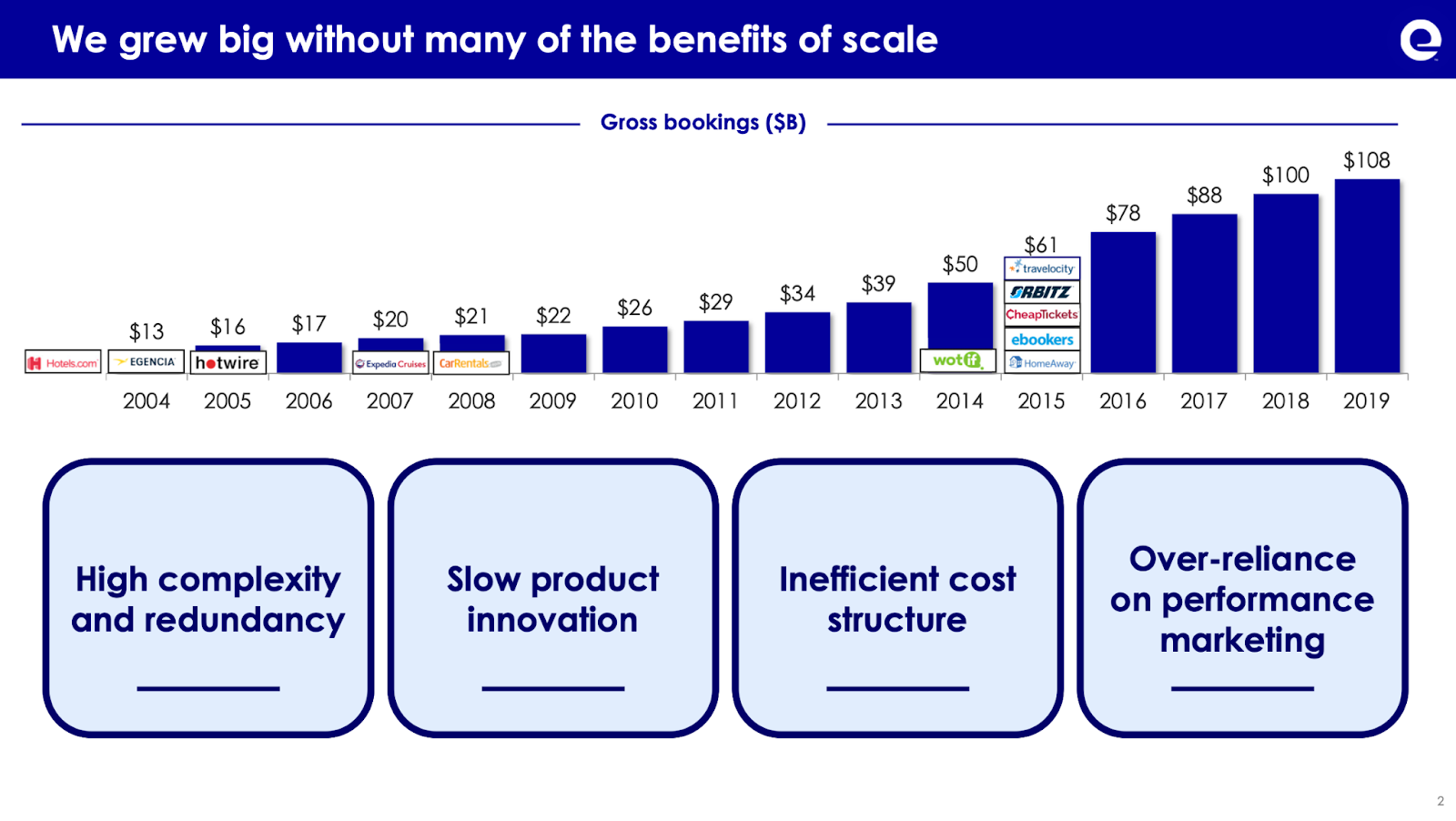

In the next 15 years, Expedia grew to become a holding company, which by the end of 2019, owned an entire portfolio of different travel brands, not just Expedia.com.

Throughout the years, Expedia Group acquired Hotels.com, Egencia, Hotwire, CarRentals, Wotif, Travelocity, Orbitz, CheapTickets, ebookers, HomeAway (now Vrbo), and a majority stake in trivago.com.

It made Expedia Group one of the three largest online travel companies in the world, competing for dominance with Booking Holdings and Trip.com. The company surpassed $100 billion in gross bookings in 2019, delivering $12.07 billion in revenue and $565 million in net income. It marked a decade of growing revenue, exceptional profitability, dividends, and buybacks.

And then the pandemic happened. Travel restrictions and lockdowns resulted in a steep decline in travel demand, dramatically impacting the company's revenue. Expedia ended 2020 delivering $5.19 billion in revenue (56.9% YoY decline) and generating $2.61 billion in net loss. Moreover, it forced the company to take additional debt, which reached almost $9 billion at some point (down to $6.3 billion as of Q4 2022).

Management had to take drastic measures such as cost-cutting and layoffs (almost 3000 jobs or about 12% of its workforce) to cope with the situation. From this point, an extensive transformation began in Expedia Group.

First, a new CEO was appointed. Barry Diller (in the picture on the right), a Chairman and Senior Executive of IAC and Expedia Group, who took over the day-to-day operations of Expedia back in 2019, was succeeded by another IAC/Expedia veteran, Peter Kern (in the picture on the left), who has been with the group since its spin-off from IAC.

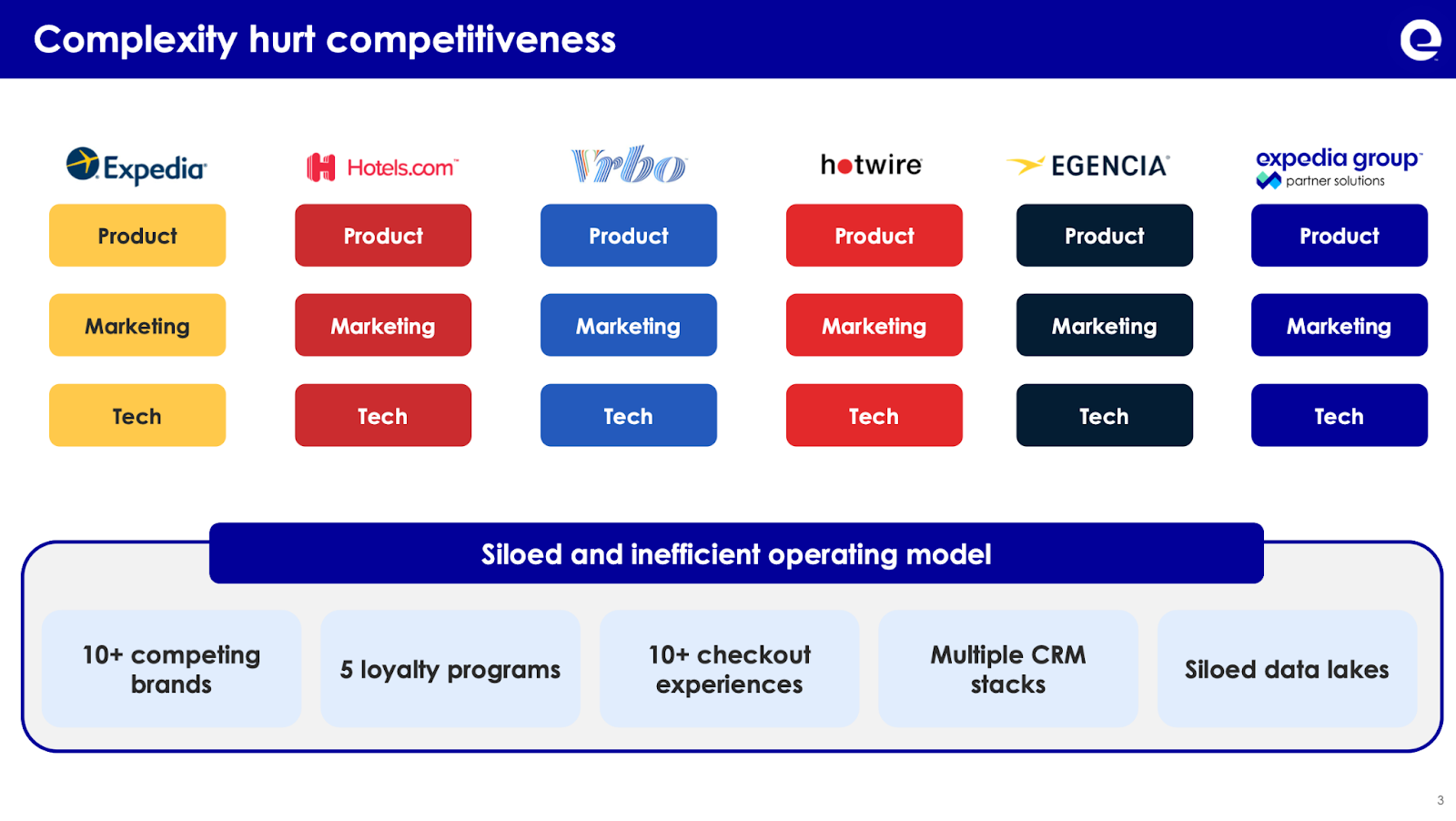

Upon his appointment, Kern immediately started to untangle the created throughout the years complexities and inefficiencies in pursuit of simplifying the business. Much of the company's prior strategy was based on all of its brands competing aggressively (including with each other) for a market share all around the world.

Kern orchestrated a shift to a platform operating model, which enabled the company to deliver more scalable services and operate much more efficiently. For example, the company now manages marketing investments holistically across the entire brand portfolio. It helps to optimize the marketing spend to achieve better returns and scale marketing capabilities more effectively.

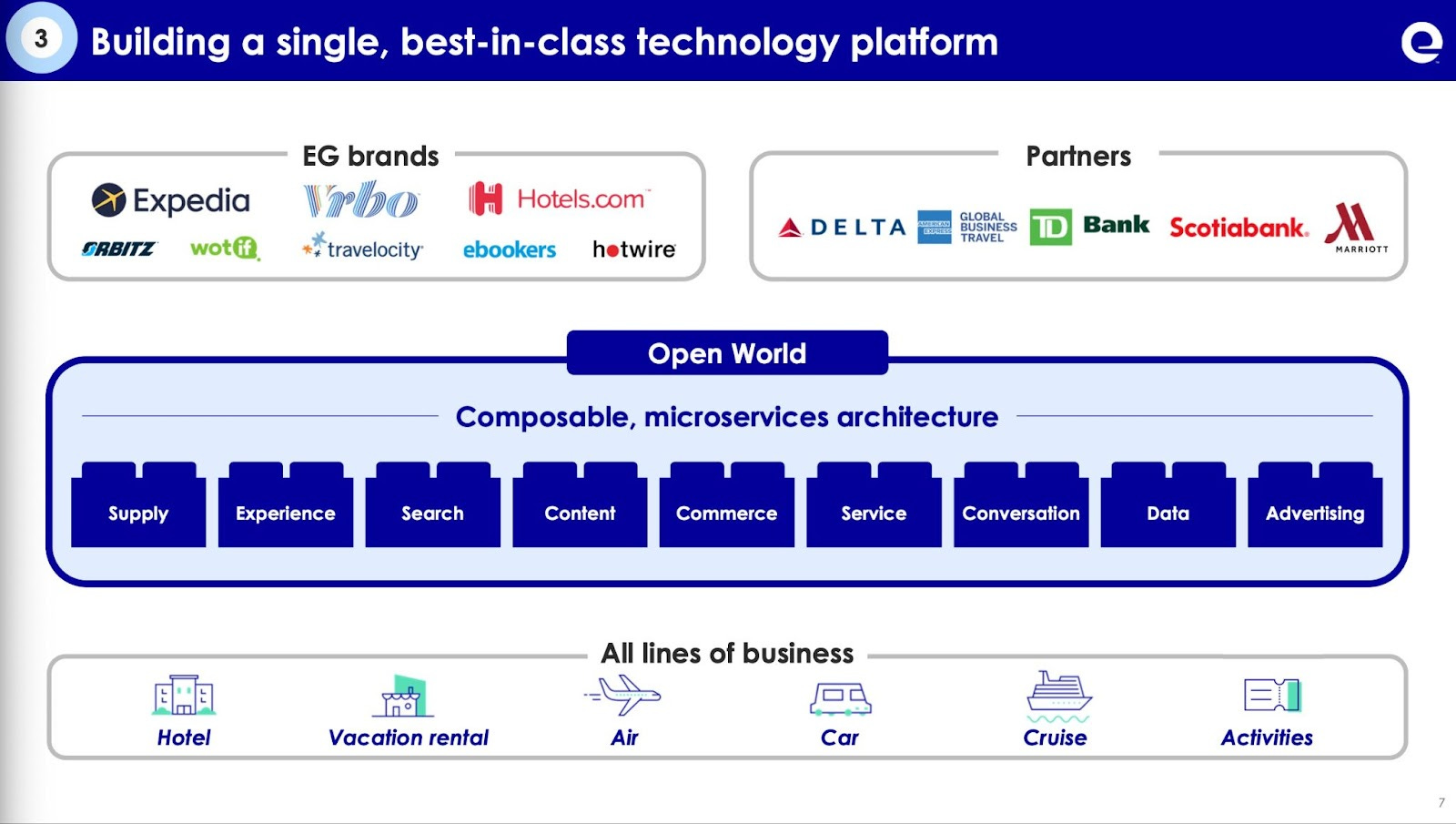

The company is also moving to a single tech platform, where all brands and geographies begin to ride on that same tech stack. Expedia.com and hotels.com have already completed the move, and Vrbo is on its way to completing it in 2023.

The new shared platform infrastructure helps build technical capabilities that support various travel products while using simpler, standard architecture and common applications and frameworks. All company's businesses now benefit from this shared platform infrastructure, including customer servicing and support, data centers, search capabilities, payment processing, and fraud operations. Ultimately, this move will result in faster product innovation, which will help create a better experience for travelers.

In addition, the company shut down or sold a number of businesses, including Egencia (which was sold to American Express that formed Amex GBT, a now publicly traded company under GBTG symbol, in which Expedia owns minority ownership and has a 10-year lodging supply agreement), as well as eliminated low-value partners, streamlined unprofitable channels (like email and coupons), reallocated spend away from non-core brands and much more.

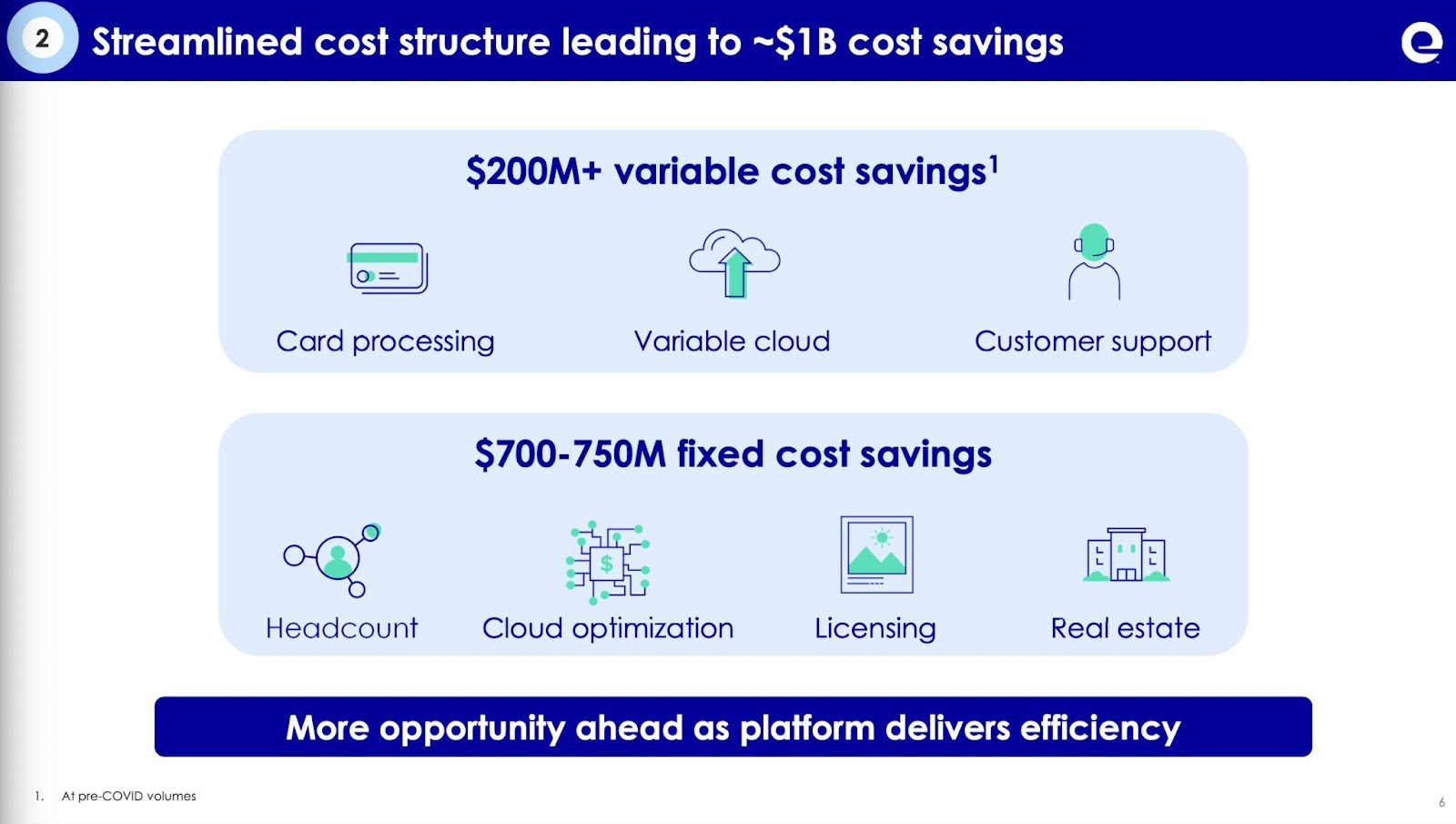

The efforts to streamline the organization did not stop there. The company also embarked on improving its cost structure, which already led to significant cost savings of approximately $1 billion (~$200 million of variable cost savings and a massive ~$750 million of fixed cost savings, including reducing headcount, optimizing cloud infrastructure, lowering licensing payments, and office consolidations.

Finally, Expedia began evolving its consumer retail strategy from being largely transactionally focused (acquiring customers through performance marketing channels like search engines) to building direct, longer-lasting relationships with its customers through customer loyalty and app adoption, a significant change that will provide the next leg for company's growth (more on this later in the writeup).

The 2020-2022 period was pivotal for Expedia Group. It returned to growth and profitability. With borders reopening and travel booming, the company reached an all-time high of $213 per share in February 2022. Since then, the stock has fallen more than 50% amid the recession concerns, but the company has become strong as ever.

Whether a recession is happening in 2023 or not, Expedia Group now has a clear path to accelerated growth and profitability, and after years of transformation, it is finally ready to become a truly global travel marketplace.

Opportunity

Trends

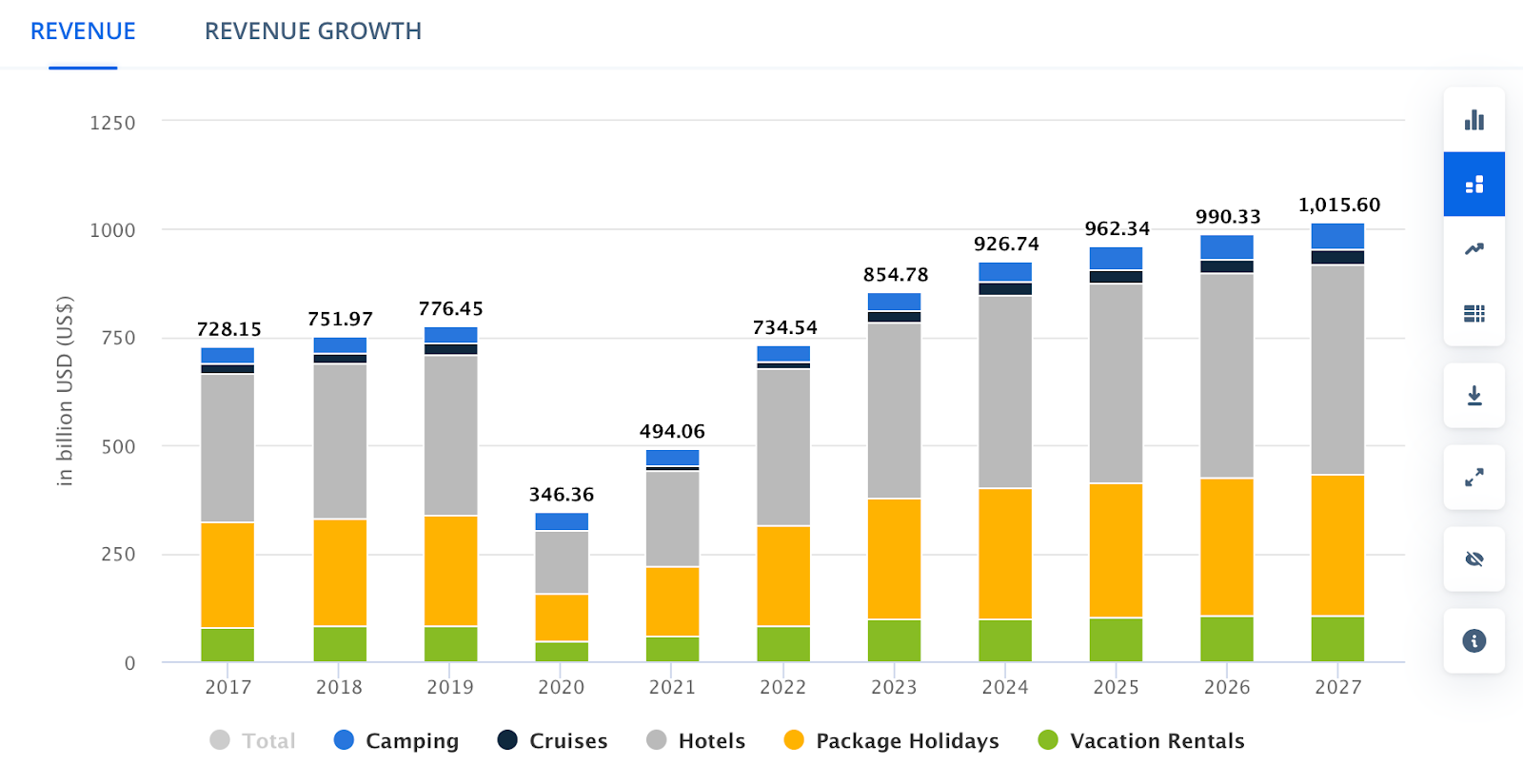

2022 was the year when the world officially opened back (with the exception of China, which expects to open its borders in Q1 2023). The industry has already seen strong travel demand, returning to almost pre-pandemic levels. According to Statista, revenue in the travel market in 2022 was $734 billion, a little shy of $776 billion in 2019.

Despite looming recession fears, the demand is only expected to increase in 2023 and beyond, reaching over $1 trillion in revenues by 2027, growing at a CAGR of 4.41% between 2023 and 2027.

After almost two years of being kept at home, more and more people are starting to see traveling as more of an essential spend than a discretionary one. Furthermore, some surveys suggest that frequent travelers have accumulated plenty of cash during the pandemic, which will be enough to spend on travel for several more years, even if the recession hits. Many industry experts expect 2023 to be the record season in many years.

Within the travel market, about 80% of total revenue will be generated online within the next five years. This long-playing trend of shifting consumer spending towards OTA's is gaining momentum. OTAs will only increase their share of the travel market in the coming years, with big players like Expedia Group getting a significant chunk of these revenues.

The rise of smartphones has boosted this shift immensely. According to various research, travelers spend, on average, 50% more if they book via the app. No wonder Expedia puts a lot of effort into app adoption going forward, as it will help make users more loyal to its brands and increase usage.

There are many other trends within the travel industry that will play in one way or another in favor of its further growth. For example, the digital nomads' movement has been growing exceptionally fast since working from home became a new norm. Only in the US, there is a minimum of 15 million people identifying themselves as digital nomads. This amount is close to 35 million people worldwide. These people are location-independent and constantly travel from one place to another, living predominantly in different vacation houses. This particular category spends a minimum of several billion dollars annually on travel.

TAM

Expedia operates in the subcategory of the travel market called online travel. Online travel is when people can plan their itinerary without relying on travel agents and do all bookings self-service via the Internet.

Online travel is projected to grow significantly in the coming years, not only in size but also as a percentage of the travel market's total revenue.

According to Statista, the global online travel market was approximately $474 billion in 2022, which is about 65% of the total travel market. By 2030, this market should surpass $1 trillion and reach over 80% of the travel market's total revenue.

Growth Drivers

Expedia Group is one of the world’s largest online travel companies, yet its gross bookings represent a small share of the total worldwide travel spending.

As of 2022, gross bookings on Expedia were $95 billion, or 20% of the online gross bookings and just 13% of the total gross bookings (both online and offline), highlighting the current size of the market opportunity and providing plenty of room for further growth.

The company is looking to grow through several channels:

B2B

Out of these $95 billion in gross bookings, $16 billion came from the B2B segment, which has seen tremendous growth in 2022 (74% YoY increase), far outpacing the growth of the Retail segment, which still accounts for the majority of revenue and Adjusted EBITDA.

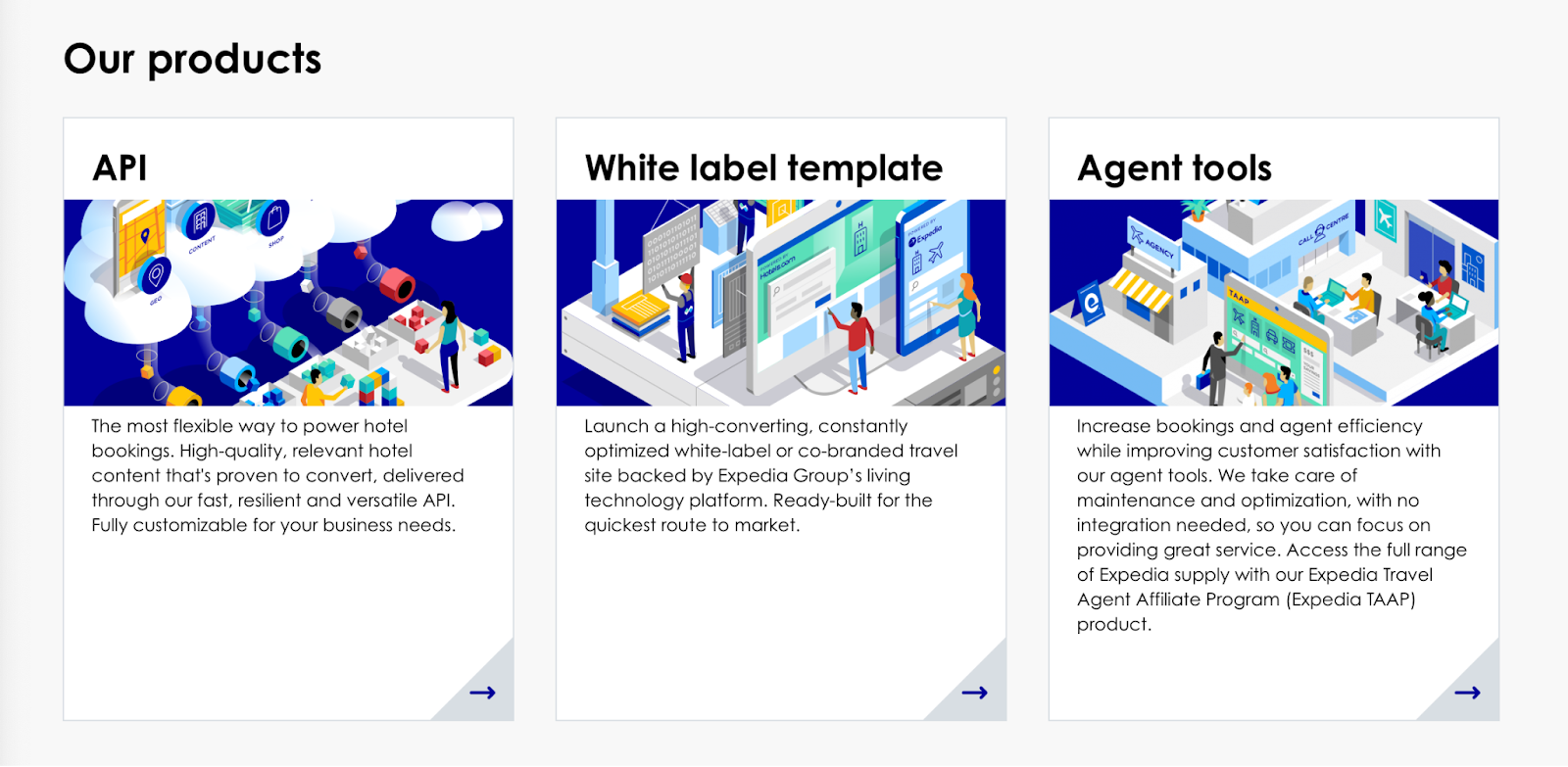

Expedia's B2B travel business is one of the largest in the world. It encompasses Expedia Partner Solutions (EPS), unlocking the power of Expedia Group for thousands of partners worldwide, including airlines, offline travel agents, online retailers, corporate travel management, financial institutions, and others. These businesses use EPS to provide competitive rates and availability, as well as quality content for travel supply worldwide to their customers.

Expedia offers a wide range of travel products and services available through Expedia's API (Rapid), customized white-label or co-branded ecommerce template offerings, and a powerful agent booking tool (Expedia Travel Affiliate Agent Program). Expedia also offers an “optimized distribution” product to help hotel suppliers distribute wholesale rates through authorized channels.

Unlike other B2B travel businesses, Expedia has three distinct differences: quality supply (more than 700,000 properties, flights from over 500 airlines, more than 175 car rental companies, and over 200,000 activities with high-quality images and descriptions), tailored customization (Expedia's travel technology products are precision-engineered to each customers' needs), and unparalleled travel expertise (a dedicated account manager for each customer to assist with the setup, answer all queries, and help grow further).

The company intends to continue to grow the B2B business by increasing the wallet share with existing customers, winning contracts with new customers, and introducing additional products and services.

With the return of travel into and out of China in 2023 and a robust pipeline of new partners around the world, management anticipates significant growth and a great 2023 for its B2B business.

There is a massive opportunity beyond 2023 to grow the B2B business, eventually offering a full range of flexible microservices.

Loyalty

In 2021, the company announced plans to unify and expand its existing loyalty programs into one global rewards platform called “One Key,” spanning all of the group's main brands.

It will be the broadest, most flexible travel loyalty program in the world. And for the first time, vacation home renters (Vrbo users) will get the benefits of a loyalty program too. One Key will also complement the loyalty programs of Expedia's many partners. No other travel loyalty program offers anything even close.

Expected to launch in 2023, One Key intends to help the company build a larger base of long-term high-value customers. With existing loyalty programs, the loyalty members drive two times the gross profit on repeat business over an 18-month period as compared to non-members.

When a loyalty member also uses the app, this drives the highest gross profit of all, and that group represents the fastest-growing customer cohort for the company in 2022.

The new loyalty program should unleash the next leg of growth for Expedia, driving more engagement, spending, and lifetime value.

“Because when you take care of customers and give them great experiences, they keep coming back. And that's how you win.” – from the Q4 2022 earnings report about the upcoming launch of the One Key loyalty program.

Core Brands

The company is making significant changes in the core brands' (Expedia, Hotels.com, and Vrbo) business, not only by moving all three to a unified technology platform that has a number of long-term benefits but also by putting the majority of the marketing efforts towards them, which should provide continuous growth in each of the brands.

Expedia is a leading full-service online travel brand in a wide range of countries around the world, offering a wide selection of travel products and services (similar to Booking.com). Hotels.com focuses on marketing lodging accommodations. And Vrbo operates an online marketplace for the alternative accommodations industry (similar to Airbnb).

International

International markets represent especially large opportunities for Expedia Group. In 2022, revenue derived outside of the US grew more than 50% YoY, and it is excluding China, which was closed for the entire 2022.

As a percentage of total revenue, the US still represents approximately 70% of total revenue (78% in 2021), providing plenty of room for international growth.

China could see a post-COVID rebound in travel as the Western countries had, providing an additional opportunity for Expedia, regardless of Trip.com being a dominant player in the Chinese market that will reap most of the benefits from the country's reopening.

Business Model

Expedia Group operates an asset-light business (does not own any inventory) with three distinct business models.

Business Models

Merchant

Under the merchant model, the company facilitates the booking of hotel rooms, alternative accommodations, airline seats, car rentals, and destination services from various travel suppliers. Expedia acts as the merchant of record for such bookings, meaning it buys rooms or air seats (usually in bulk for a lower price) from suppliers and then sells them to end users (usually with a markup). The majority of the merchant transactions relate to lodging bookings.

Agency

Under the agency model, Expedia facilitates travel bookings and acts as the agent in the transaction, passing reservations booked by the user to the relevant travel provider. For this, the company receives commissions from travel suppliers, usually from 20% to 25%. The majority of the agency bookings relate to air bookings.

Advertising

Finally, under the advertising model, Expedia offers travel and non-travel advertisers access to a potential source of incremental traffic and transactions through its various media and advertising offerings across several of its transaction-based websites, including trivago.

Merchant revenue accounted for 66% of total revenue in 2022, while agency and advertising for 26% and 8%, respectively.

Service Types

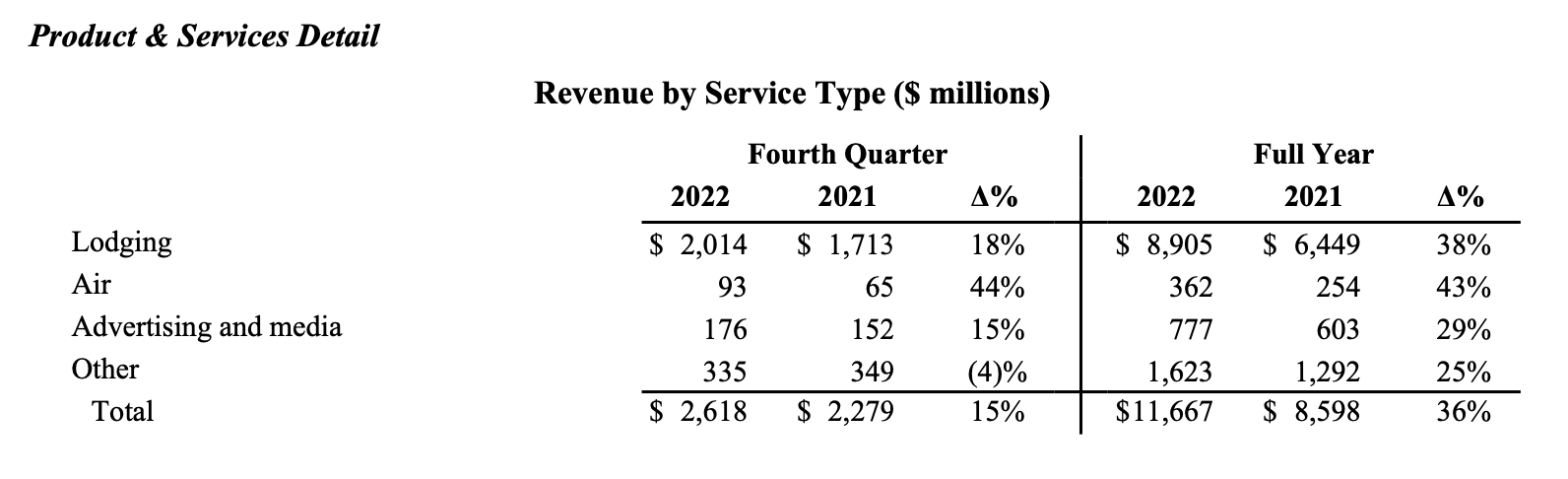

Lodging

As a percentage of total revenue in 2022, lodging (hotel and alternative accommodations) accounted for 76%, growing 38% YoY from $6.44 billion in 2021 to $8.9 billion in 2022.

The lodging business has seen significant growth in the past several years, driven by industry trends, a mix shift to Vrbo (which carries a higher ADR than hotels and has accounted for a higher percentage of room nights), and high ADR geographies.

The shift to alternative accommodations has accelerated since the pandemic, but hotel reservations (stand-alone and package bookings) still account for the majority of lodging revenue.

Vrbo has transitioned from a listings-based classified advertising model to an online transactional model and generates revenue through host subscription-based listing (an annual subscription that costs $499) or pay-per-booking listing model (3% payment processing and 5% commission fee), as well fees for guests (vary from 6% to 15%).

Air

The air segment has also seen a surge in pent-up demand. However, throughout the entirety of 2022, airlines have been operating at reduced capacity due to staffing shortages (especially pilots), supply chain disruptions, and elevated fuel costs. As a result, airfares increased across the board. Despite improved air bookings in 2022, air business continues to lag lodging bookings and remains below 2019 levels. It accounted for just 3% of total revenue in 2022.

Advertising

The advertising business (comprises primarily of revenue generated by trivago from sending referrals to online travel companies and travel service providers and Expedia Group Media Solutions, which is responsible for generating advertising revenue on all of Expedia's brands) represented 7% of the total revenue in 2022. The growth of 29% YoY in 2022 was mostly due to growth in Expedia Group Media Solutions, while trivago has seen continuous revenue pressure since most online travel agencies (including Expedia) have reduced marketing spend on trivago.

Other

The other revenue (car rental, insurance, destination services, and cruise) has also seen growth in 2022, increasing 25% YoY. This growth was primarily attributable to growth in fee revenue related to the corporate travel business (Egencia) prior to its sale to Amex. Going forward, other revenue will decrease substantially compared to the previous years.

Gross Margin

The costs primarily consist of customer services and fees related to customer bookings, including fees to air ticket fulfillment vendors, credit card processing (including merchants fees, fraud, and chargebacks), and other costs (including data center and cloud costs).

Though the costs have increased in 2022 (primarily due to higher merchant fees, cloud costs, and customer service costs), they grew at a much slower rate than revenue, reflecting Expedia's divestitures and ongoing efficiencies primarily across the customer support operations.

Expedia recorded the highest gross profit in its history in 2022, with the highest gross margin (85.80%) ever. In Q1 2023, the gross margin remained strong at 84.47%.

Operating Expenses

Expedia's OpEx is still high (~75% of total revenue) due to high SG&A expenses. The marketing costs increased significantly in 2022. As the company still heavily relies on traffic from search engines, and the competition for this traffic is intense and growing, it had to continuously spend to remain at the top of search results.

With the change in the strategy (towards loyalty and app adoption that will drive more direct traffic and higher conversions), the operating expenses should improve going forward.

Profitability

Expedia is back to being profitable on both adjusted EBITDA and Net Income basis. In 2022, the company drove record EBITDA at over $2.3 billion and an EBITDA margin of over 20%. Net income came at $352 million, a significant improvement from $15 million in 2021 and a net loss of a whopping $2.72 billion in 2020.

In Q1 2023, the company delivered $185 million in adjusted EBITDA but posted a net loss of $145 million due to seasonally higher S&M expenses.

Analysts covering Expedia expect the company to only accelerate its earnings in the coming years, delivering around $1 billion in net income in 2023.

Expedia has a strong balance sheet with $5.85 billion in cash and cash equivalents and an undrawn revolving line of credit of $2.5 billion (ample liquidity of $8.4 billion).

There is also a hefty debt of $6.24 billion (with a leverage ratio of 2.7x), but it is long-term, and the majority of it is due after 2025. The company is actively working on reducing the debt from quarter to quarter (the debt went down from $8.8 billion as of the end of 2021).

The current liquidity, combined with robust free cash flow ($2.8 billion as of the end of 2022, up approximately $1.2 billion or over 70% versus 2019 and $2.9 billion in Q1 2023), will not only help support growth and profitability but also maximize the return on capital to shareholders. The company accelerated share buybacks in the second half of 2022 and repurchased nearly 6 million shares (worth $600 million) so far. Management plans to continue to buy back the stock opportunistically in 2023 (approximately 12.1 million shares remain under the existing authorization for future repurchases).

Expedia also has a history of paying dividends. Payouts were paused because of the pandemic, but the company may resume paying them soon.

After several difficult years and a transformation along the way, Expedia is finally ready to capitalize on the hard work. Its business model is well-diversified and proven to accelerate profitability regardless of if the economic downturn happens or not.

Competitive Advantages

Competition

Expedia faces rapidly evolving and intensifying competition across all segments where it operates. Because Expedia currently generates most of its revenue from hotel reservations, the main competitors are two other industry juggernauts, Booking Holdings and Trip.com. While Trip makes most of its revenue in China (and is generally more active in Asian markets) and Booking is more used in Europe, Expedia tries to operate and compete in all markets simultaneously, though currently, it is more present in the US.

Expedia also competes with certain hotel chains that have been focusing on driving direct bookings on their own websites and mobile applications (Hilton and Marriott are great examples) by advertising lower rates than those available on third-party websites as well as incentives such as loyalty programs, increased or exclusive product availability, and complimentary benefits (like free WiFi).

In between these large players and hotel chains is a vast number of online and offline travel companies that target leisure and corporate travelers, including travel agencies (both online and offline), tour operators, travel supplier (hotels, airlines, and rental car companies) direct websites and their call centers, consolidators and wholesalers of travel products and services, large online portals and search websites (Google is the largest with its Google Travel and Google Flights products), certain travel metasearch websites (Kayak, TripAdvisor, Skyscanner, and many others), mobile travel applications, social media websites, as well as traditional consumer ecommerce and group buying websites.

Additionally, in recent years, with the purchase of Vrbo, Expedia began actively moving into the alternative accommodations market (which is an alternative to hotel rooms that is becoming more and more popular around the world), where Airbnb currently dominates the market, and because it has certain competitive advantages, it is extremely hard to compete with it.

B2B is also getting a bigger piece of Expedia's business, and while Expedia is one of the best (if not the best) players in the global B2B travel space, the company is facing increasing competition from travel consolidators and wholesalers of travel products, other OTAs with B2B offerings, and other technology and content providers.

Competitive Advantages

Travel (in all of its niches) is such a competitive market that requires competing companies to stand out in order to win over the constantly increasing competition. However, it is increasingly hard to build a competitive advantage in this space for any company because travel has been generally commoditized, with price being the only differentiation for many consumers. So it leaves companies with only one option: build a strong brand and loyal customer base around it.

Brand

Being one of the first and oldest OTAs, Expedia has built one of the most recognized and trusted brands in the travel industry. There is probably no person that has ever booked a trip online and never heard about Expedia.

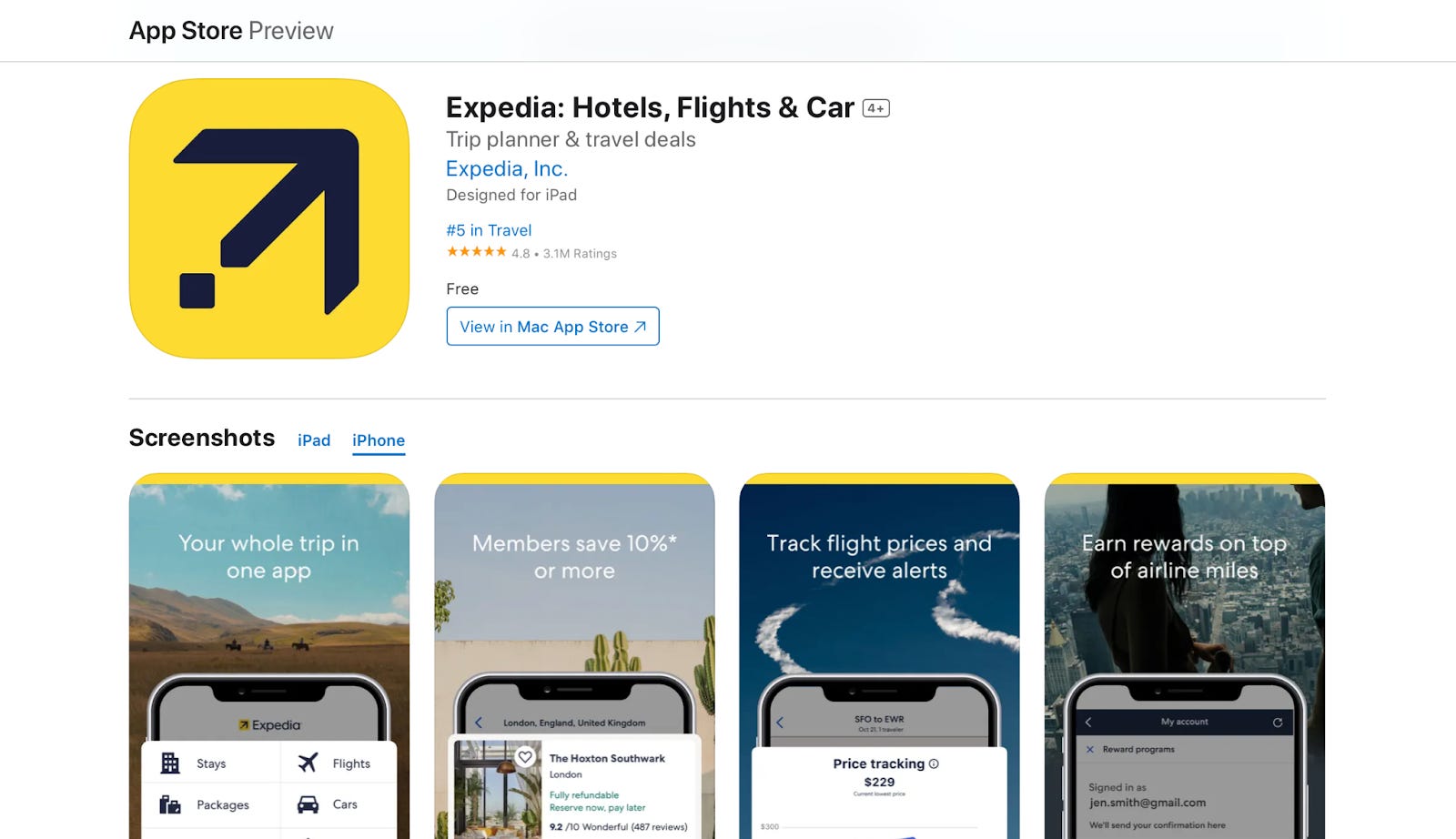

Expedia is by far the best travel app in the US App Store based on the rating. With a rating of 4.8 / 5 based on 3.1 million ratings, it surpasses Booking's 4.8 / 5 based on only 823k ratings.

Furthermore, Expedia is the most popular travel booking app in the US App Store (excluding alternative accommodations). Interestingly, Vrbo is the most popular alternative accommodations app in the US. It is not only higher than Airbnb in the App Store travel category, but it also has more ratings (1.3 million compared to 595k, respectively).

While Expedia and Vrbo are dominating in the US, the situation is different in other markets outside of the US. In most cases, Booking and Airbnb will dominate their respective niches.

Nevertheless, the reputation that Expedia has been building for more than 25 years is undoubtedly helping the company generate strong word of mouth that converts into new users.

Pricing

The brand reputation also helps the company to negotiate competitive pricing with suppliers and provide added value to travelers.

Thanks to its strategic partnerships and collaborations with hotels, airlines, and other service providers, Expedia most often offers better prices vs. booking directly. The price is certainly better if a user books a travel package (hotel and air flights).

Optionality

The best part of Expedia is that it contains several businesses in one. It is not only an OTA in its classic representation but also provides alternative accommodations through Vrbo (perhaps, the fastest-growing and most fascinating part of Expedia's business overall), and it has an advertising arm through trivago and its own solutions.

This optionality helps the company retain a competitive advantage over even the largest OTAs.

Risks

Recessionary environment

If the recession occurs anytime soon, it will undoubtedly hurt travel bookings, leading to a substantial decrease in revenues.

Demand

The consumer demand for travel will most likely peak in 2023 after the pandemic boom, especially for the retail segment.

Inflation

A substantial increase in living expenses leaves less available budgets for discretionary spending like travel.

Competition

Covered extensively in the Competitive Advantages section.

Dependence on suppliers

An essential component of Expedia's business success depends on its ability to maintain and expand relationships with travel suppliers (most of the revenue is derived from these relationships). Travel suppliers now have better negotiating power than they had several years ago.

Indebtedness

Covered in detail in the Business Model section.

Control

Barry Diller has 100% of Expedia Group’s outstanding Class B common stock, representing approximately 27% of the total voting power. He is also Chairman of the Board of Directors and Senior Executive at Expedia while acting in the same role at IAC/InterActiveCorp. It could create a potential conflict of interest.

Additional Sources

Leadership – https://www.expediagroup.com/who-we-are/leadership/default.aspx

Ownership – https://www.sec.gov/Archives/edgar/data/1324424/000132442423000018/expe-20230421.htm#i6a21162b82534b6486ec490a6406414e_97 [page 47]

Enjoy the rest of your weekend!!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.