Part 1: Deep dive on DraftKings ($DKNG)

In order to read this entire deep dive on DraftKings (DKNG) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (~100% YTD and ~1,000% over the past 3 years), investment models and daily webcasts.

I also run a Stocktwits rooms where I post 25+ times per day including my daily activity, market commentary, quarterly earnings analysis, analyst upgrades/downgrades, options trades, daily webcasts and much more… this is also where I chat with subscribers throughout the day.

Here are my other newsletters…

Company: DraftKings

Ticker: (DKNG)

Website: DraftKings.com

IPO date: April 24, 2020 (through SPAC)

IPO price: $20.49

Current stock price: $31.74

Outstanding shares: 463.9 million

52 week high: $32.45 on July 28, 2023

52 week low: $10.69 on December 28, 2022

ATH: $74.38 on March 22, 2021

Market cap: $14.724 billion

Net cash/debt: -$206.4 million (net debt)

Enterprise value: $14.931 billion

Headquarters: Boston, Massachusetts, United States

Number of employees: 4,200+

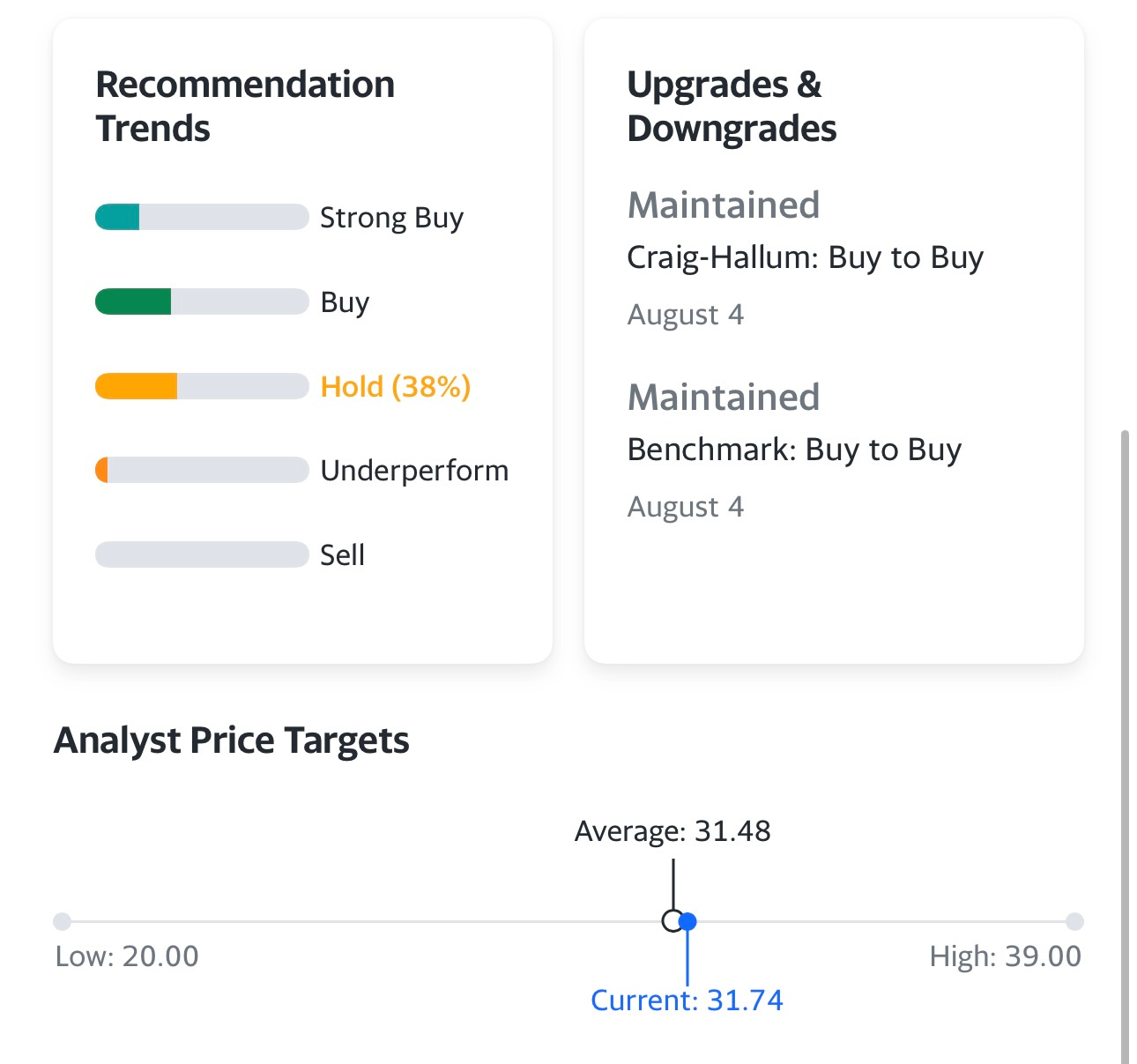

Average price target from analysts: $31.48

Investor Relations [click here]

Q2 2023 Earnings Report [click here]

Q2 2023 Earnings Webcast [click here]

Q2 2023 Earnings Presentation [click here]

Moffett Nathanson Technology Conference [click here]

18th Annual Needham Technology Conference [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

Below the paywall is part 1 of the DraftKings deep dive along with links to my investment portfolio (up ~100% YTD), daily activity, investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here] new link for August/September

My investment models [click here] new link for August/September

My daily webcasts [click here] new link for August/September

Before going through this deep dive I would suggest watching this CNBC interview with the CEO of DKNG after they reported earnings last week…

Introduction

Disclosure: I currently have a 6.5% position in DKNG in my trading portfolio which I started pre-market last Thursday as soon as I saw DKNG’s Q2 results and then I added to the position after it faded off the highs and bounced just above the 20d ema. I have a stop loss on these shares at $29.56 which is just below the 23d ema and last week’s low (see chart below). I don’t have a position in my investment portfolio which is much larger than my trading portfolio.

I was very bearish on DKNG last year and even shorted the stock multiple times, mostly because the losses and SBC were absolutely horrendous plus it seemed like competition in the sports betting market was getting more competitive because not only was DraftKings fighting for market share and customers against FanDuel but then MGM and Barstool Sports decided to launch their own services. You can see how much the “outstanding shares” has increased over the past few years. This is partly from SBC (stock based compensation) to employees but also from secondary stock offerings to raise capital in order to cover the losses. Hopefully we continue to see SBC as a % of market cap (aka dilution) come down, last year around this time it was at 5-6% because the stock was trading at $10-15 but now that the stock has rallied 200% the dilution number has actually come down to 3% which is still bad but looking a little better than last year.

Another reason I stayed away from DKNG last year is because I was worried they’d have to spend an absurd amount of money to acquire customers — for the most part I think that was correct and not owning the stock was a good move because DKNG dropped 87% from the highs of 2021 to the lows of 2022. Just look at those losses in 2020 through 2022, over $3.7 billion and that doesn’t even include all the new stock that was created/issued. DKNG was an absolute mess the past couple years but they’d really started to turn the corner over the past 6 months which was evident in last week’s Q2 earnings report with much better than expected guidance for Q3 and full year.

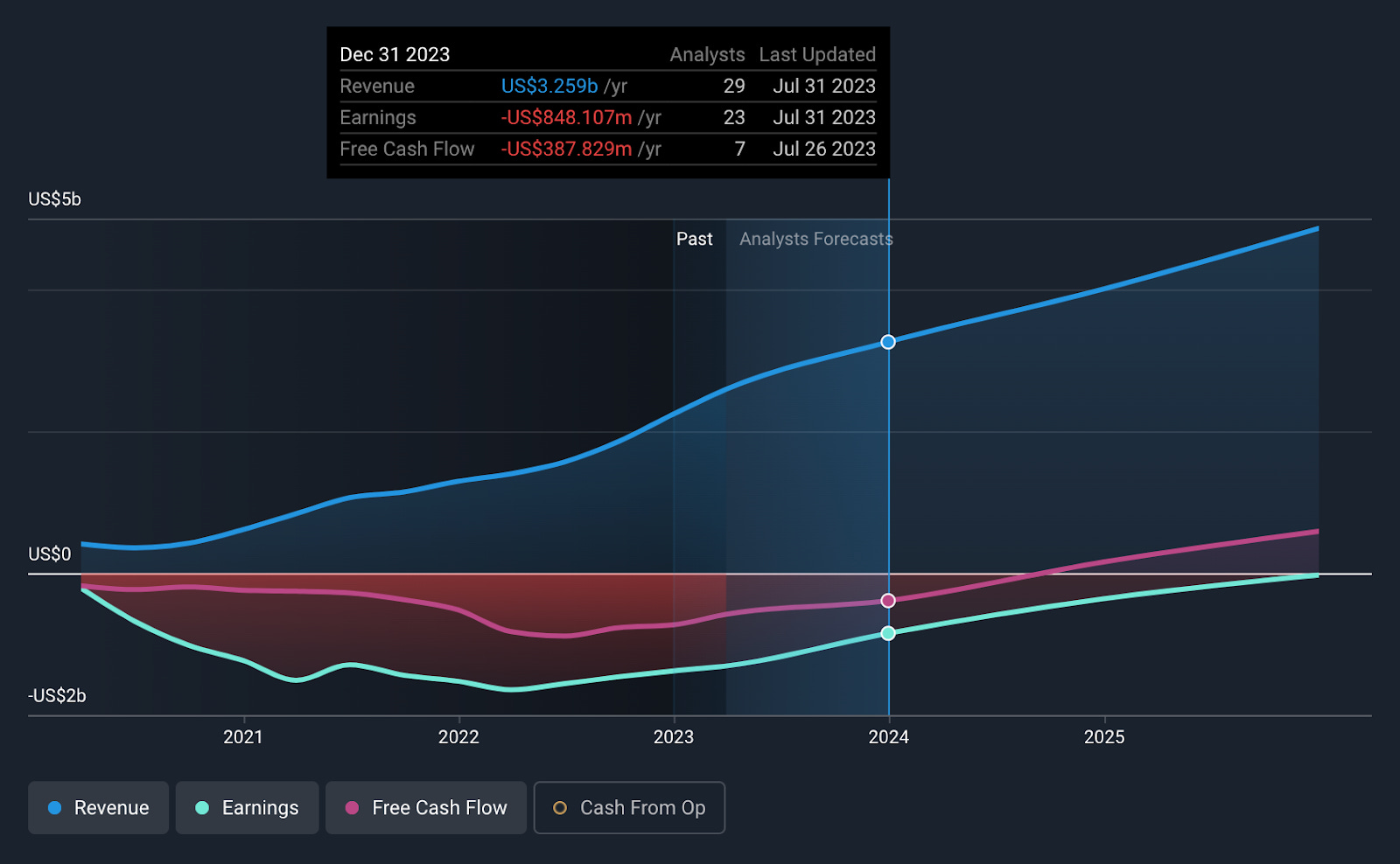

Last May, DKNG was probably oversold at ~$10 but the fundamentals were not pretty, the company was losing a ton of money and the path to profitability was very murky. Fast forward 15+ months and things have certainly gotten much better in terms of financials & fundamentals. SBC is still too high (starting with the executives/founders) but DKNG continues to report very impressive revenue growth (up 88% YoY in Q2) and now they’re forecasting positive EBITDA in Q4 but not for the full year however it looks like DKNG could do $200M+ of EBITDA next year (2024) and then be non-GAAP profitable in 2025 and GAAP profitable in 2026. These are all massive improvements from a year ago when it looks like non-GAAP profitability might not happen until 2027 so kudos to the management team for getting more fiscally responsible which included cost cutting, layoffs and more efficient marketing campaigns. As you can see from the chart below the revenue estimates (from the analysts) continue to move higher. Several years ago analysts were looking for ~$3.0 billion of revenues in 2026 but now they’re looking for almost $6 billion, that’s incredible and is a testament to how well DKNG is executing but also how faster the industry is growing thanks to more states legalizing sports betting (mostly because they want the tax revenue).

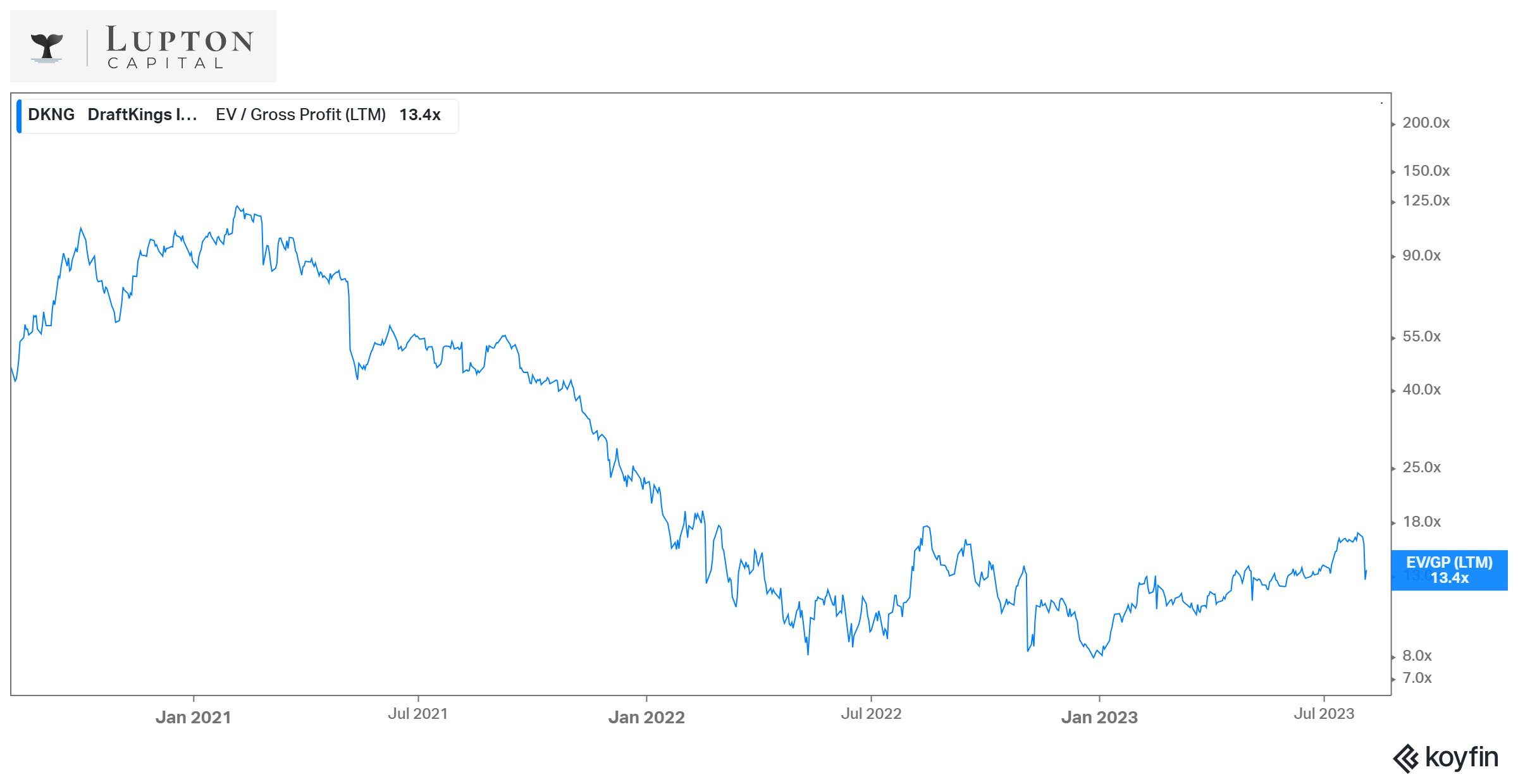

On top of the fundamentals improving and the path to profitability looking more clear, DKNG’s valuation is somewhat compelling at current prices with the stock trading at 4.1x NTM EV/SALES and 13.4x LTM EV/GP, both are higher than where they were a year go but down 90% from where they were in early 2021.

This introduction probably sounds bullish so you might be wondering why I don’t own the stock yet in my investment portfolio. There are several reasons why so I’ll list them out…

DKNG is already up 178% ytd and I’d rather not chase it, especially if the markets might pullback another 5-10% which would probably take DKNG down even more.

10Y treasury yields are back to November 2022 levels (~4.1%) which isn’t good for unprofitable growth stocks

SBC and executive compensation is still very high which becomes very dilutive, the number of shares outstanding has more than doubled since the company came public via SPAC

DKNG is still losing money and even though those losses look better than they did a year ago it’s still possible DKNG does another capital raise, they do have $1.1B of cash but they also have $1.25B of long-term debt and I’m sure they’d love to get it paid off. If this happens it would either be straight equity or it would be convertible debt. I do think there’s a 50% chance it happens in the next 6 months and with the stock up ~180% YTD and Q2 earnings now behind them it’s not a bad time to do it. If DKNG did an offering and the stock dropped ~10%, I’d definitely consider starting a position.

My ideal entry price would be the 50d ema/sma at $27.50 to $28.00 but I don’t think it happens without a broad market pullback and a dilution event. DKNG should hold up well in a market pullback because that was a better than expected Q2 earnings report and their guidance/outlook keeps them on track to be EBITDA+ next year. One of the unknowns with DKNG is how well their business would perform in a recession with increasing unemployment especially from their younger demographic.

I’ll go deeper into my investment model in part 2 of this deep dive but here’s a sneak peek, DKNG could have tremendous upside over the next 3-5 years if they can hit my estimates which I think are reasonable. Any stock that might have 200% upside over the next 4-5 years is one that’s worth keeping on the watchlist.

Hope you enjoy this deep dive on DKNG and learn something new about the comapny.

Company Background

The initial idea of DraftKings came about in 2011 when Jason Robins (current CEO, owns approximately 1.18% of the company worth ~$171 million and 90% of total voting power), Matthew Kalish (currently a President of DraftKings North America, owns around 0.7% worth ~$102 million), and Paul Liberman (currently President of Global Technology and Product, owns approximately 0.8% worth ~$118 million) were still working at VistaPrint, one of the largest e-commerce companies that produce physical and digital marketing products for small businesses.

The trio shared a common passion for fantasy sports, which they had already been playing together for several years. Fantasy sports is a type of online game where participants assemble virtual teams composed of real professional sports players. Then, their virtual teams compete with each other based on the statistical performance of selected professional sports players in real-life games. The best teams get prizes, including cash.

Back then, virtual teams were picked before the start of the season. Once you have chosen your team, you cannot change it. "We gathered together to discuss fantasy sports every week. One day, we raised the question, what if you can do fantasy sports daily? Picking the team on a draft is the most popular part of fantasy sports. Allowing users to pick the team or players daily or weekly will make fantasy sports more engaging." [edited] – recalled Matthew Kalish on ARK Investment's FIY Podcast.

With that idea, Kalish, Robins, and Liberman started developing a platform for daily fantasy sports. The first iteration of DraftKings was launched in early 2012, just before Major League Baseball’s opening day. It was a one-on-one competition with a prize pool of just $100. But just a year later, the company had awarded a whopping $50 million in prizes.

From a totally new product (which later made every fantasy sports provider switch to daily fantasy sports) and just a few thousand daily users, DraftKings grew to become the second-largest DFS provider (after FanDuel), with over 10 million users by 2015. That year marked the beginning of a continuous rivalry between now two largest players in the industry.

Interestingly, both companies went under fire in 2017 due to the ongoing argument over whether daily fantasy sports contests should be classified as gambling. While DraftKings and other DFS operators maintained their position that it was a game of skill rather than chance, the debate continued to gain momentum. After many lost lawsuits, canceled deals, banned transactions by several banks, and even withdrawal of services from several states, DraftKings and FanDuel decided to join forces and merge into one company to move forward together rather than compete with each other. However, the Federal Trade Commission immediately blocked the deal in the face of violating antitrust laws (the combined company would have controlled about 90% of the total market), and both companies had to call off the merger and go separate ways.

That same year, gambling in the US changed forever. The US had a federal ban on sports betting in nearly every state (except Nevada, Oregon, Montana, and Delaware) since 1992. New Jersey was the first state to file a case to the Supreme Court to overrule that ban to legalize online betting.

The ban on betting was struck down by the US Supreme Court in May 2018, granting each state the freedom to determine its own stance on whether or not betting is suitable for its residents. In almost 30 years, New Jersey became the first state to legalize online betting, as well as iGaming (online casino and poker).

DraftKings was vigorously preparing for this moment, and in August 2018, the company took the first bet in New Jersey, becoming the first online sportsbook outside Nevada. That was the beginning of a new chapter for DraftKings, transforming the company from just a DFS provider to the only vertically integrated pure-play sports betting and online gaming company in the US today.

Revenues have followed. In the year of the start of betting legalization, the company generated $226 million in revenue, a 17.95% increase compared to 2017. But next year, revenue soared to $323 million, marking an impressive growth of 43% from 2018.

2020 was a unique year for DraftKings in many ways. The pandemic has hit the sports industry significantly with the widespread cancellation of live sports in the US, including March Madness and the NBA finals. Yet the company managed to grow its revenue by 90% to reach an impressive $614.5 million. That same year, DraftKings became a public company.

Management chose a SPAC route, merging with a special purpose acquisition company, Diamond Eagle Acquisition, formed by entertainment veterans Jeff Sagansky (ex-CBS Entertainment) and Harry Sloan (ex-MGM). The deal was valued at around $3 billion, and the combined company (SBTech, a provider of interactive sports betting solutions and services, was also a part of the deal) received around $500 million in cash.

DraftKings began its trading on April 24, 2020. The stock opened at $20.49 (+100% from the NAV price of the SPAC). At the time of the IPO, DraftKings offered mobile and online sports betting in Indiana, New Jersey, Pennsylvania, and West Virginia, and sports betting at retail locations in Iowa, Mississippi, New Jersey, and New York.

On March 22, 2021, the stock price hit an all-time high of $74.38 per share, and despite a phenomenal 2021 when the company generated almost $1.3 billion in revenue (a mind-blowing 110% YoY increase compared to 2020), it plummeted to nearly $10 in 2022.

The primary reason for such a dramatic fall is that DraftKings continued to increasingly lose money. From a net loss of $76.2 million in 2018 to $142.7 million in 2019 to $1.23 billion in 2020 to $1.52 billion in 2021, the company was moving farther away from becoming profitable at the time when 'growth at all cost' is no longer a narrative among investors and the cost of capital increased substantially.

Like many other growth companies, DraftKings had to change its course and adjust its business model to balance growth and profitability. Management became more aware of efficiency and preserving capital. According to the founders, they found at least $100 million in efficiencies in 2022, especially on the vendor side. The company continues to seek ways to make it more efficient, from buying certain games to negotiating specific market access rates to rethinking the entire payment ecosystem all the way down to the snack vendor in the corporate office.

The real profitability is still far away from the company (not earlier than 2026) despite planning to break even in 2023 and become profitable in 2024 (on an adjusted EBITDA basis). But it is already a massive step for a company like DraftKings that is still on the stage of aggressive market capturing where it has to spend heavily to acquire (and educate along the way) as many players as possible before it sees any conversion into profitability. And some initial signs of a long-term sustainable business model capable of generating significant profits on the scale are already here.

For example, in Q1 2023, the company that requires massive budgets on promotion managed to acquire 57% more first-time players YoY while spending 27% less on the acquisition. DraftKings showed that it can effectively and quickly switch from expensive local marketing to cheap national marketing while still growing the number of users.

DraftKings seems to have passed the inflection point and is now making the necessary steps to capture its massive opportunity while doing it more efficiently and effectively. In the long term, DraftKings can transform from a sports betting operator to an 'everything sports' juggernaut, offering fans a complete experience of following sports: from placing bets and reading latest sports news to making DFS picks and trading sports NFTs to buying sports merchandise and tickets for sporting events.

Opportunity

Trends

DraftKings operates within the Casinos and Gaming industry, with a particular focus on sports. This industry is driven by several big trends, including the growth of the popularity of watching sports, the legalization of sports betting and iGaming and its growth in popularity, and increased fan engagement.

The growth of the popularity of watching sports

Sports are a major form of entertainment in the United States. Every year, millions of Americans tune in to watch various sports via television and online platforms or by attending live events.

According to Statista, 65.5 million people in the US (>20% of the population) watched digital live sports content at least once per month in 2022. This figure is projected to rise to over 90 million by 2025 (~30% of the population).

Sports events hold the top spots year in and year out in most-watched primetime telecasts in the US. It is not just the Super Bowl telecast that usually garners the highest viewership numbers (the 2023 edition of the Super Bowl was watched by an average of 115 million viewers across both NBC and its streaming platforms). Other sports events and programs attract tens of millions of viewers.

The increasing popularity of streaming services is the primary factor behind the rising number of sports enthusiasts watching games. According to Nielsen Fan Insights, a significant percentage of sports fans in 2022, including 76% of NFL fans and 89% of soccer fans, have watched sports on streaming or online platforms, either regularly or occasionally.

Just five years ago, this was hard to imagine. The variety of sports events was highly limited to the TV broadcasting selection, capping the number of games available to watch.

With more sports events moving to streaming platforms now, more games are becoming available, which in turn attract more viewers and increase the popularity of sports in general.

Thus, for example, NFL’s Thursday Night Football (viewed by an average of 16.7 million viewers during the 2022 NFL season) became exclusive to Amazon Prime Video in 2022, while Apple will exclusively stream all MLS soccer matches starting the 2023 season. These two deals on sports rights indicate a shift that has been developing as digital platforms continue to gain more influence in the sports industry.

Apple actually did something even more significant than just buying the rights to stream MLS for ten years. The company almost single-handedly brought one of the most popular athletes in the world and one of the greatest-ever soccer players, Lionel Messi, to play in MLS for Inter Miami. This deal is unprecedented in the world of sports and may change it forever. According to The Athletic, Apple and Messi have a revenue-sharing arrangement on the number of new subscribers that Apple TV will add after his arrival to MLS. And Apple is expected to add millions of new subscribers.

Some initial results are already seen: MLS recorded the most viewed matches ever on the week between July 19-26, 2023, when Messi had a debut match and scored the winning goal in compensated time before scoring two more goals and making one assist in the second match.

The arrival of Messi to MLS is a major boost for soccer, which historically had low popularity among Americans despite various European superstars that came to play in MLS previously, from David Beckham to Zlatan Ibrahimovic. With the upcoming FIFA World Cup 2026, which will be held in the US, Canada, and Mexico, soccer should gain more popularity in the coming years, attracting millions of new viewers and further boosting the popularity of watching sports that will positively impact DraftKings.

The growth of the popularity of sports betting

Watching sports goes hand in hand with sports betting. There is a direct link between placing a bet and watching a game. It makes the experience more exciting and entertaining. Furthermore, a fundamental psychology principle plays out here: people pay more attention to something that involves their money.

Data backs it up: for example, two-thirds of mobile gamblers in 2022 watched the NFL game when they placed a bet on it.

Technological advancements are another key contributor to the rise of sports betting in recent years. Betting has become more accessible and convenient than ever before – no more visits to retail shops. With just a few taps on the phone, anyone can place a bet on their favorite team at any time.

In recent times, sports betting has evolved into a popular social activity where individuals place bets with their peers, engage in discussions about their picks, and share their tips, strategies, and opinions. This has come from fantasy sports, where the social aspect is an integral part of the overall experience.

Finally, the sports betting platforms themselves contribute a lot to this growth by offering constant promotions and bonuses (from free bets to deposit bonuses) to attract new customers and keep existing ones engaged.

Increased fan engagement

More and more fans are getting increasingly involved with their favorite teams and players. In one of its reports, Deloitte identified four types of fans (based on their motivations and attitudes): casual fans, avid fans, super fans, and fanatics. The latter two are the most engaged and comprise almost 30% of all US sports fans.

Super fans (make up around 20%) watch sports frequently and consume additional content such as podcasts or video blogs related to sports, while fanatics (make up around 10%) watch sports regularly and participate in activities such as fantasy sports and betting. The number of fanatics is growing the fastest among all four types, positively impacting DraftKings.

This particular group of fans tends to follow and interact with their favorite teams or players on social media, use various apps to access sports content or information, participate in online forums or communities to discuss sports and use podcasts or video blogs to listen to or watch sports analysis or commentary.

Total Addressable Market (TAM)

DraftKings operates in three segments: daily fantasy sports, online sports betting, and iGaming.

Fantasy sports remain highly popular in the US even after online betting legalization. There are over 60 million active players in this region. This market is expected to reach $9.84 billion in 2023 and could potentially increase to $85 billion in the next ten years, growing at around 24% per year.

The online sports betting market has experienced the biggest growth among these three since 2018, when it was first legalized. An increasing number of sports enthusiasts are turning to digital platforms to place bets on their favorite sports events and teams.

According to Statista, the online sports betting market will reach $7.62 billion in 2023, an increase of 35.82% from $5.61 billion in 2022. This market is further expected to almost double by 2027, reaching nearly $14.5 billion (CAGR 2023-2027 of 17.32%).

DraftKings also operates in the iGaming (online casinos) market, which is projected to reach $6.29 billion in 2023 and grow at approximately 12% CAGR in the next five years to almost $10 billion.

Cumulatively, DraftKings' total addressable market today is north of $24 billion. While it is already one of the market leaders, the company expects to generate $3.25 billion in 2023, representing just 13.5% of the total opportunity and leaving plenty of room for further growth.

Growth Drivers

There is an extensive list of growth drivers that should have a long-lasting impact on DraftKings, leading to a considerable increase in revenue from $2.24 billion in 2022 to over $6.4 billion in 2027 (representing a CAGR of 23% over the next five years) while resulting in long-term profitability and earnings growth for the company.

Below are the key growth drivers:

Expansion to new states

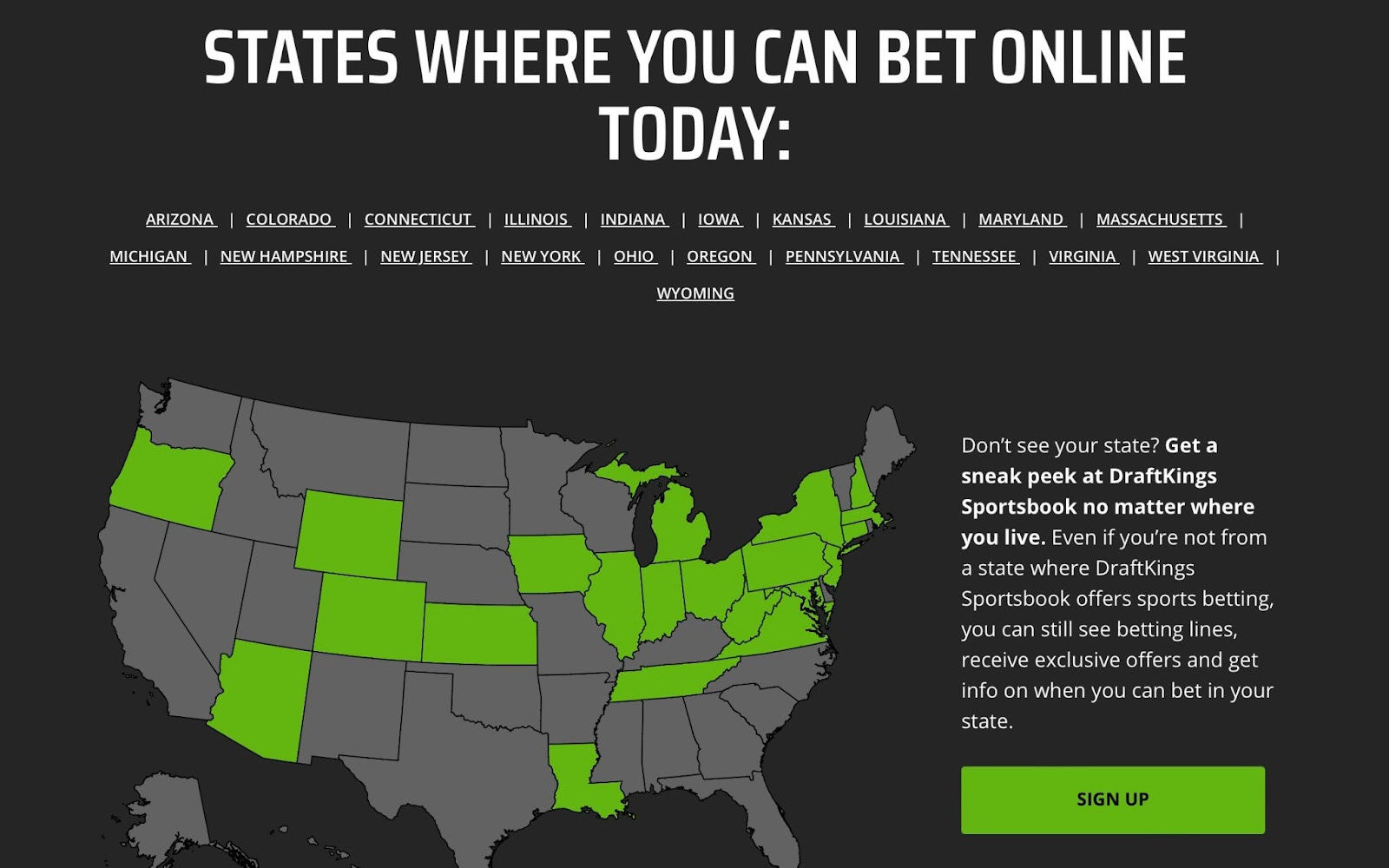

DraftKings' growth prospects highly depend on the legalization of online sports betting and iGaming in additional jurisdictions. Following New Jersey in 2018, other states began legalizing betting. As of July 2023, sports betting is legal in 37 states (out of 50), but only 28 states allow placing bets online.

There is a strong pipeline of states considering legalizing online betting. This topic is rising on the agenda in more and more states (12 states that represent an additional 24% of the US population have pending bills for online betting legalization, while 5 states that represent an approximately 14% of the US population have either introduced legislation to legalize iGaming or introduced a bill that may result in an iGaming referendum during an upcoming election), and DraftKings management believes it will be able to reach 65% of the US population for online betting and 30% for iGaming in the next few years.

Growth within current states

DraftKings is currently accepting bets in 21 states, with Ohio and Massachusetts launching in Q1 2023.

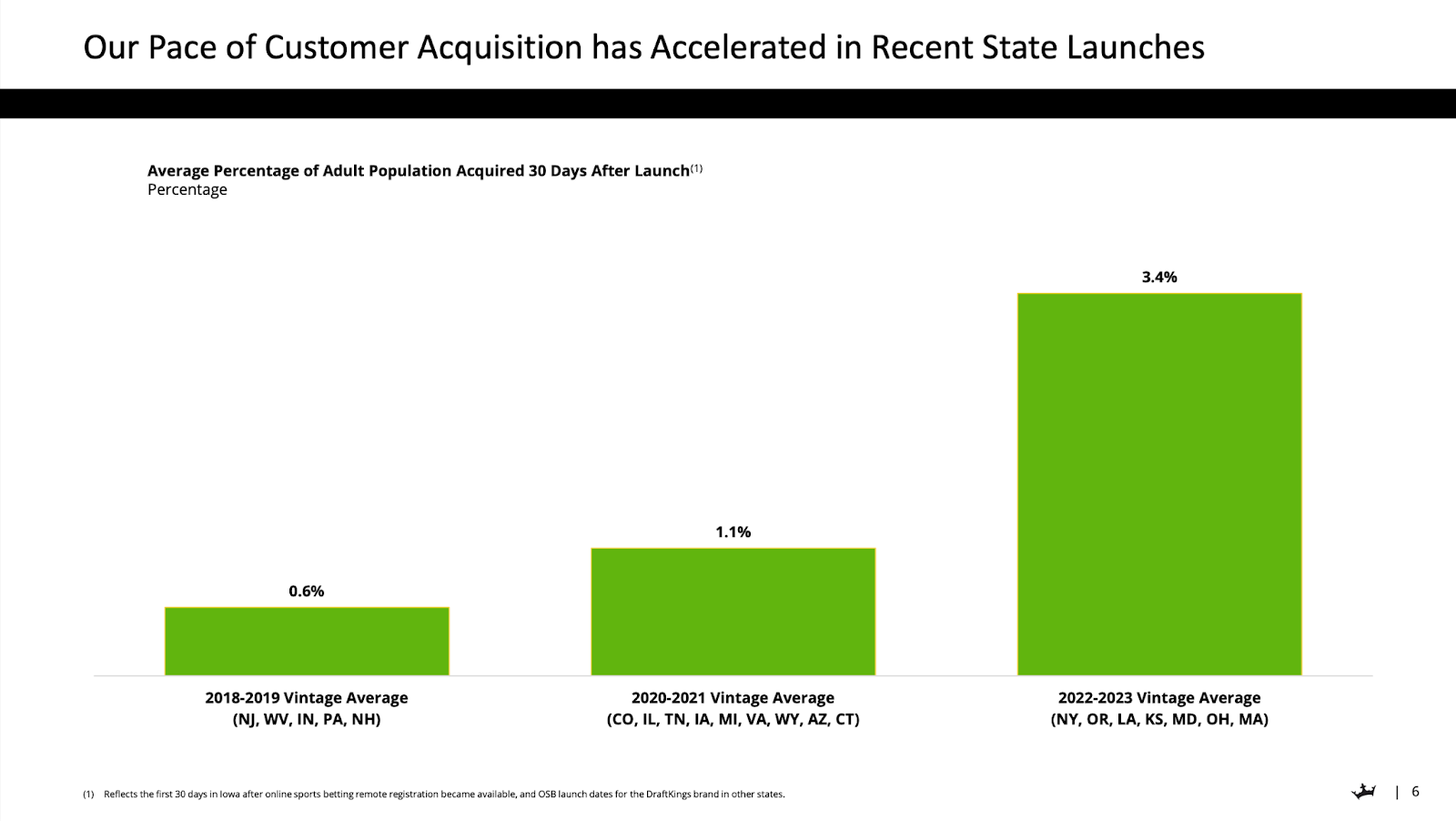

The company has been highly successful at executing its State Launch playbook lately. With every new state, DraftKings is able to capture more users than in previous vintages, resulting in massive per-customer efficiencies, which have profound implications for future profitability.

To illustrate, early 2023 launches in Ohio (January 2023) and Massachusetts (March 2023) have already led to attracting 7% and 6% of these states' total adult populations onto its platform.

DraftKings is also successfully growing older vintages. In each of its 2018-2019 and 2020-2021 state vintages, handle increased >25% YoY, unique customers increased >10% YoY, and revenue grew >80% in the first quarter of 2023 compared to the same quarter a year ago, while the company spent less on marketing.

This is due to the highly effective retaining strategies. The company continuously introduces new sports to bet on and new bet types designed to increase players' activity on the app.

DraftKings currently offers 18 sports to bet on, and its bets range from traditional bets on the outcome of games to more unique sports wagering opportunities tailored for more engaged users. Most recently, the company introduced live same-game parlays (multiple bets within the same game) for MLB. More sports will follow.

DraftKings has always been investing in new product offerings, as well as improving marketing, merchandising, operational efficiency, and delivering a great user experience. Most recent advancements in AI/ML should greatly help retain customers by personalizing their experience and reduce fixed costs from the customer support perspective.

iGaming

With the acquisition of Golden Nuggets in May 2022, DraftKings has greatly improved its ability to capitalize on the iGaming opportunity. Golden Nugget's established brand allowed the company to broaden its reach into new customer segments and enhance the combined company's iGaming product offering through its vertically integrated platform.

As a result, according to management's estimates, DraftKings' iGaming offering has achieved the #1 GGR share (gross gaming revenue, a measure of all the money generated by player losses in a certain time period) among all operators in the US at 26% in the first quarter of 2023.

The expansion of iGaming is going at a much slower pace than online sports betting, currently limiting the potential for DraftKings. Many states are concerned that the proliferation of online and mobile gaming may lead to the decline of land-based casinos, resulting in job losses. Additionally, there is concern that the increased availability and convenience of gaming options may lead to a rise in addiction.

But the growth of iGaming in states that allow online casinos already is mind-boggling. This will eventually lead to more states opening for iGaming, and DraftKings is actively preparing for this moment.

The company is moving from licensing games from third-party vendors to creating games in-house. This move will help the company increase iGaming margins long-term, build more stickiness, and create a differentiator aspect.

DraftKings already has a number of exclusive games that became best-selling (played the most). One example is Rocket, a game played with a rising rocket where the player must cash-out by exiting the rocket before it stops rising.

Rocket also provides a chance to win a jackpot. The company is working on its exclusive jackpot technology that aims to help increase wallet share and retention. DraftKings Jackpot products now live in three states across more than 100 slots and table games.

Horse racing

DraftKings has recently entered the horse racing market, valued at $400 billion in 2022 and expected to double by 2030.

DK Horse app offers wagering on races from hundreds of domestic and international tracks, including all three Triple Crown races. The app is currently available in 15 states with more states planned to launch later in 2023.

DraftKings has partnered with Churchill Downs, an industry leader with a deep-rooted history in horse racing (the home of the Kentucky Derby and the Kentucky Oaks). Together, they plan to deliver an innovative, mobile customer experience not available elsewhere. DK Horse will also allow customers to stream videos of races within their account.

Web3

In August 2022, DraftKings launched its first NFT game, Reignmakers, in partnership with Polygon. Despite being present in the NFT market since 2021 (DraftKings Marketplace offers curated initial sports NFT drops and allows owners of these NFTs to list them for sale to other Marketplace customers), the company made an important pivot during 2022 from digital collectibles to utility-based NFTs that play into DraftKings' gameplay platform.

Reignmakers is different from Fantasy Sports. It combines daily fantasy sports with Web3/NFT space, day trading, and collecting traditional sports cards. Users collect athletes and then build roasters using those NFTs. If you have specific athletes in your collection, you can utilize them. Otherwise, they are not available for use, unlike in fantasy sports.

With an NFT-driven game, a user can constantly buy/sell/trade his NFTs to improve the collection and use the skill to build the best team to compete for real prizes.

So far, DraftKings made exclusive deals with the NFL, UFC, and PGA and is looking to expand to other sports.

While the NFT market is going through a bear cycle right now, the company continues to pour investments in this space. In management’s words: “Reignmakers is our biggest bet among everything we do, but it provides the biggest possible opportunity.”

Consolidation

This industry will see massive consolidation during this decade, eventually leaving just several players that will take most of the market share. A lot of future growth for DraftKings will come from acquisitions or partnerships in some cases (like the one with Churchill Downs).

International

DraftKings can potentially expand to international markets. The feasible options are emerging markets (like Mexico, for example, where regulation of online gambling began in 2016) rather than long-time established markets in Europe, where betting has been legal for decades.

Business Model

DraftKings' business model is centered around three key product offerings: online sports betting, online casino (iGaming), and daily fantasy sports (DFS). Additionally, the company offers DraftKings Marketplace, retail sportsbook, media and other consumer product offerings, but their share of revenue is currently insignificant.

Users can access the key product offerings via the company's website or mobile apps (iOS and Android). DraftKings' Sportsbook and Casino app is currently placed higher than any other betting app (including FanDuel) on both the App Store and Google Play, though FanDuel has twice as many ratings and reviews as DraftKings.

DraftKings' daily fantasy sports app is currently placed in 40th place in the Sports category in the App Store and 45th place in Google Play, far below ESPN Fantasy Sports, NFL Fantasy Sports, and Yahoo Fantasy.

Revenue Streams

DraftKings earns revenue by taking a percentage cut, commonly referred to as a hold rate, from all of its offerings.

In online sports betting, DraftKings first determines the odds for various sports events (usually, the odds are similar among most bookmakers). These odds have a built-in theoretical margin and are set in such a way that the bookmaker actually does not care if the player wins or loses the bet; it makes money on both sides of a game and then simply collects the hold.

For the online casino, DraftKings uses the same model as land-based casinos that set odds that favor the house, meaning that the casino will always win (hence the phrase 'the house always wins').

Finally, with daily fantasy sports (DFS), a peer-to-peer product offering where contestants compete against one another for prizes, DraftKings simply collects the difference between entry fees paid by the players and the amount it pays out to players as prizes.

The company allocates a portion of gross revenue from each of its offerings to new and existing user incentives and promotions, including loyalty programs, free plays, deposit bonuses, discounts, rebates, or other rewards and incentives. These incentives and promotions are generally used to acquire new users, reactivate prior users, and increase the monetization of current active users.

DraftKings' hold rate is currently at the industry average of close to 8%. In Q1 2023, the company posted a hold rate in the mid-8s, signaling that the company can increase the hold rate long-term, supported by the introduction of in-house same-game parlay capabilities.

Gross Margin

DraftKings' casino and DFS businesses are already profitable due to their pretty straightforward revenue model and less marketing spend needed/done by the company.

Sportsbook, on the other hand, is still unprofitable, while it is DraftKings' most important segment. It is also the lowest-margin business out of the three.

Promotions are one of the largest factors that impact the gross margin rate for the online betting segment in any given period, and sportsbooks currently require a lot of marketing spend. There are also other elements that affect the gross margin, like taxes and costs paid to various vendors that sit within DraftKings' platform.

Combining three segments together, DraftKings has a gross margin of approximately 34% (down from 78% in 2018 when the business primarily consisted of DFS to 67.8% in 2019 to 43.6% in 2020 to 38.72% in 2021). The gross margin may vary from quarter to quarter due to seasonality (for example, in Q4 2022, the gross margin was 43.2%, while in Q3 2022, it was just 25.75%).

Sportsbook gross margin should eventually increase as states mature (enter the second, third, and fourth year of operation). Starting the second year, the company would begin decreasing its promotional efforts, gradually increasing its hold rate towards the end of the third year, which would lead to an increased gross margin and contribution profit as a result.

DraftKings' gross margin is projected to gradually increase in the next five years to over 50%.

Operating Expenses

Operating expenses remain exceeding the total revenue (on a yearly basis). However, the last several quarters have demonstrated that the company is finally starting to show operating leverage. In Q4 2022, total operating expenses as a percentage of total revenue were 70.1%, while in Q1 2023, they were 82.8%.

As states mature, the company should spend less and less on marketing, leading to operating income.

Profitability

The company is on track to turn adjusted EBITDA positive in 2024. The current analysts' consensus for adjusted EBITDA in 2024 is $176 million, which is projected to grow to over $1 billion by 2026.

In 2026, analysts expect the company to become profitable on a GAAP basis, delivering a net income of over $420 million.

Elevated stock-based compensation is a current drag on profitability. In 2022, the company paid $578.8 million in SBC, a whopping 25.8% of total revenue and almost 4% of the market cap. High SBC continued in Q1 2023, in which the company paid out $117.4 million, representing almost 16% of the total revenue.

Since going public in 2020, the company increased the number of shares outstanding by almost 50%, while the stock price appreciated by 80%.

Balance Sheet

The company finished Q1 2023 with $1.1 billion of cash and now plans to end the year with more than $800 million of cash before its expected inflection to generate positive adjusted EBITDA for the full year 2024.

There is a long-term debt of $1.25 billion on its balance sheet. In March 2021, DraftKings issued zero-coupon convertible senior notes in an aggregate principal amount of $1.265 billion with a mature date in 2028.

The company also has a revolving line of credit of up to $125 million, which matures at the end of 2024. As of Q1 2023, the company has not used it.

Cash Flow

DraftKings currently heavily burns cash to fuel its growth. However, starting in 2024, the company should be able to transform some of its EBITDA (~$100-$125 million) into free cash flow.

By 2027, the company is expected to reach $1 billion in FCF, with an FCF margin of more than 15%.

*

Once DraftKings takes marketing expenses and SBC under control, its business will not only start generating a lot of cash but also become highly profitable on the scale. In the longer term, DraftKings is a cash machine capable of not only buying back all of its issued shares for SBC along the way but also paying dividends.

Competitive Advantages

Competition

At the micro level, DraftKings operates in the entertainment and gaming industries and, first and foremost, competes with other forms of entertainment, such as television, movies, video games, and in-person casinos. The competition with other forms of entertainment is primarily for the discretionary time and income of the users. There are countless options vying for their attention and wallets, and spending on betting or gambling at casinos is not always a high priority for the majority.

At the micro level, DraftKings faces competition from a range of providers of online gaming and entertainment. This includes various fantasy sports apps (like ESPN Fantasy Sports, NFL Fantasy Football, PrizePicks, Yahoo Fantasy, and others) and countless online casinos (some of which may operate illegally).

DraftKings stands out in the online gaming and entertainment industry by providing a diverse range of products through a single platform. When considering all of DraftKings' offerings, FanDuel is its primary rival.

FanDuel was founded two years prior to DraftKings and also began as a fantasy sports provider. In May 2018, Paddy Power Betfair (now Flutter, which also owns a portfolio of brands, including Sky Betting & Gaming, Sportsbet, PokerStars, Paddy Power, Betfair, and others) purchased a controlling stake (and later increased its stake to 95%) in the company and swiftly launched FanDuel Sportsbook.

Since then, FanDuel has operated in all currently legalized states and holds the market-leading position in most of these states, ahead of DraftKings. FanDuel's overall market share today is around 50%, but it was much larger earlier this year: DraftKings managed to increase its share from 31% in March to 37% in June.

Some reports claim that Fanatics is making moves into the scene with its pending acquisition of PointsBet, the Australia-based operator with an existing business in 12 states in the US. Earlier this summer, DraftKings submitted the proposal to acquire PointsBet, but a week later announced that it is no longer pursuing the acquisition. While Fanatics is undoubtedly a strong competitor on paper (with its massive user base of 80+ million), it will take years and extensive spending for the company to reach a low double-digit share of the market.

DraftKings and FanDuel will most likely eventually dominate the entire industry, consolidating most, if not all, smaller competitors, and collectively hold up to 90% of the market share.

Competitive Advantages

To dominate the industry, DraftKings must continuously work on developing competitive advantages that will not only protect the company from new entrants but will also allow it to compete successfully with FanDuel.

Below are some potential competitive advantages that the company possesses at this stage. These competitive advantages may develop over time, and some may transform into a real moat.

Technology

DraftKings' core product offerings are built on top of an integrated, proprietary account management technology. This technology provides users with access to their account history across all DraftKings-branded products and a uniform identity verification system, which is critical to enabling seamless navigation from DFS audience to Sportsbook and iGaming product offerings.

Thus, the company created a powerful cross-selling mechanism that allows it to successfully cross-sell various of its products. Someone who starts playing DFS could end up betting on his favorite team, or someone who already places bets on sports events may try playing one or two sports-themed casino-type games.

Recently, DraftKings has begun investing in creating its in-house, proprietary games, new betting mechanics, and other things that enhance user experience and make it exclusive to DraftKings only.

Brand

DraftKings uses copyright, trademark, trade dress, domain name, and patents to protect its product offerings and other intellectual property. DraftKings name, in particular, is its biggest asset, as it is already a household name known nationwide among fantasy sports players.

DraftKings has built a trusted and recognized brand associated with integrity, innovation, and customer satisfaction. This strong brand has played a significant role in the company's ability to attract and keep a substantial user base, which is particularly important in the fiercely competitive online gaming industry. When it comes to playing on money, users will select only those platforms that they can trust and are recognized by others.

DraftKings also managed to strategically position its brand by partnering with major sports leagues and media entities, including the NFL, UFC, PGA, MLB, ESPN, Amazon, and others. For example, DraftKings' partnerships with ESPN and Amazon (Thursday Night Football on Prime Video) allow it to advertise its product offerings across these platforms and integrate them into their media players.

DraftKings is known not only for its popularity among users but also for its ability to attract and retain talent. Being a leader in the online gaming industry, DraftKings' highly skilled workforce helps the company innovate and provide top-notch products and services, enhancing the brand's reputation even further.

Stickiness

DraftKings has built an easy-to-use app that combines excellent customer support, a highly personalized data-driven experience (from special promotions to exclusive bets like betting on eSports, based on past play history and location), and a robust customer loyalty program (designed to reward users for their continued patronage through bonus bets, cashback offers, and exclusive promotions).

These all help to keep players around and grow their engagement level over time, making the app very sticky.

Risks

Discretionary spending

DraftKings operates in the discretionary segment. In the event of a recession, inflation, rising living costs, declining consumer confidence, and other unfavorable economic conditions, the spending on gambling will be the first to be cut by the majority of users.

Marketing expenses

Since DraftKings operates in a fiercely competitive industry, where it not only competes with small emerging players but also with deep-pocketed FanDuel, the company must continually and aggressively spend on marketing activities, including various promotions.

Right now, the company spends too much on marketing (>50% of total revenue and >60% of total operating expenses) with no signs of slowing down, which could potentially limit its profitability (move profitability away from the current target of 2026).

Legalization

Although many states have yet to legalize online betting and iGaming, the legalization of these activities is not guaranteed or could be limited, making operating in some jurisdictions unattractive. State budgets have been boosted by government funding, and the need for additional revenue from gambling taxes is no longer a top priority for many of these states. Legalization in new states is critical for DraftKings' growth and profitability projections.

SBC

Stock-based compensation in this company has been under control in recent years. Not only does it dilute existing shareholders, but it also limits the company's profitability prospects. There are no signs that SBC will decrease anytime soon.

Profitability

As a result of the elevated SBC and marketing expenses, DraftKings remains unprofitable, and though it expects to turn adjusted EBITDA positive in 2024, the real profitability (GAAP) is years away. Currently, the company is heavily losing money ($1.23 billion in 2020, $1.52 billion in 2021, $1.37 billion in 2022, and projected $856 million in 2023).

Seasonality

DraftKings' business significantly depends on sporting events and seasons. This can result in short-term volatility in betting win margins and user engagement, thus impacting revenues.

Insider selling

There has been high insider selling since March 2023. DraftKings' CEO alone sold half of his entire stake in the company worth over $250 million.

Additional capital

Defending and capturing market share requires a significant amount of capital. Even with over $1 billion in cash and soon-coming positive FCF, the company may require raising additional money at some point to sustain its growth (including through acquisitions), adding to an already large enough long-term debt of $1.25 billion.

Voting power

The company's CEO, Jason Robins, holds 90% of total voting power, which limits anyone's (including large shareholders or the members of the board of directors) ability to influence any outcomes.

Additional Sources

Management – https://www.draftkings.com/about/who-we-are/

Board of Directors – https://draftkings.gcs-web.com/governance/board-of-directors

Ownership – https://www.sec.gov/Archives/edgar/data/1883685/000110465923036644/tm239801d2_def14a.htm#tSOOC (page 19, note: CEO sold half of its shares after this filling)

Have a great week!!!!

Don’t forget about my daily webcasts. I typically cover my investment portfolio for the first 15-20 minutes and then my trading portfolio for the second 15-20 minutes. You can also ask questions through the chat feature.

Part 2 should be out in the next couple days, I’m still trying to decide on my next large cap deep dive, some of the companies I’m considering are FSLR, DECK, ZG, CHWY, GRAB, ZS, WDAY, NOW, WOLF, LULU, ULTA, BX, KKR, APO, ISRG, SYK, BKNG, PAYC, LYV, ADSK, ADBE, ANET or CSU. Feel free to let me know if you have specific interest in any of these companies.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.