Part 2: Deep dive on Deckers ($DECK)

In order to read this entire deep dive on Deckers ($DECK) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (+93% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio and trading portfolio (fwiw, my trading portfolio is up +67% YTD with a much different strategy than my investment portfolio)

Here are my other newsletters…

Company: Deckers Outdoor

Ticker: (DECK)

Website: Deckers.com

IPO date: October 1993 (traditional IPO)

IPO price: $15.00

Current stock price: $514.09

Outstanding shares: 26.13 million

52 week high: $568.47 on August 08, 2023

52 week low: $298.61 on September 30, 2022

ATH: $568.47 on August 08, 2023

Market cap: $13.435 billion

Net cash/debt: +$786 million (net cash)

Enterprise value: $12.549 billion

Headquarters: Goleta, California, United States

Number of employees: 4,200+

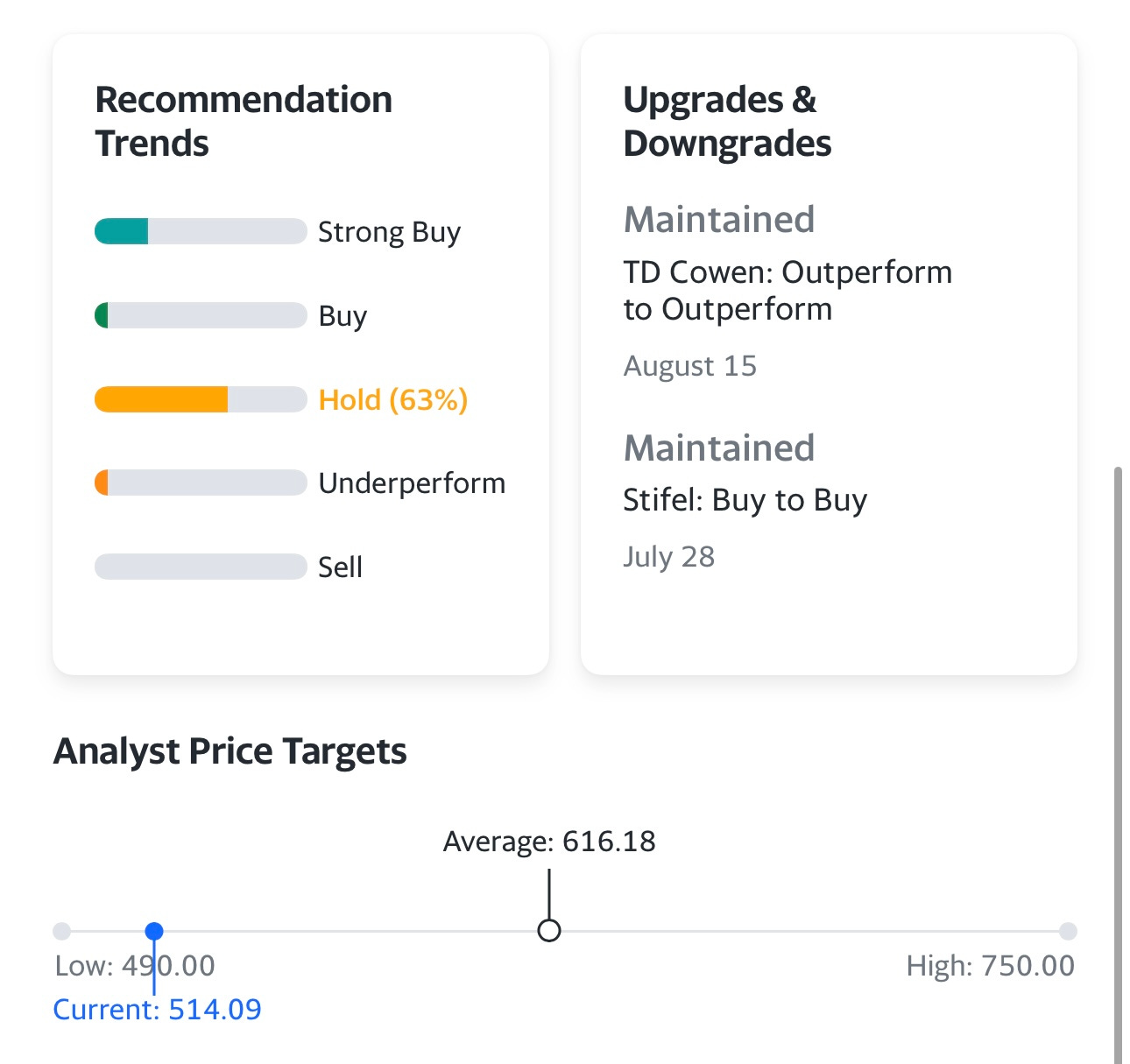

Average price target from analysts: $616.18

Investor Relations: https://ir.deckers.com/

Q1 FY 2024 Earnings Report: https://ir.deckers.com/news-events/press-releases/press-release/2023/DECKERS-BRANDS-REPORTS-FIRST-QUARTER-FISCAL-2024-FINANCIAL-RESULTS/default.aspx

June 2023 Presentation: https://s25.q4cdn.com/376120126/files/doc_presentations/Deckers-Brands-Presentation-Baird-Conference-June-2023.pdf

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

Here is part 1 of the Deckers ($DECK) deep dive…

Below the paywall is the Deckers ($DECK) deep dive along with links to my investment portfolio (up +93% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here] — new link for October

My investment models [click here]

My daily webcasts [click here] — new link for October

Introduction

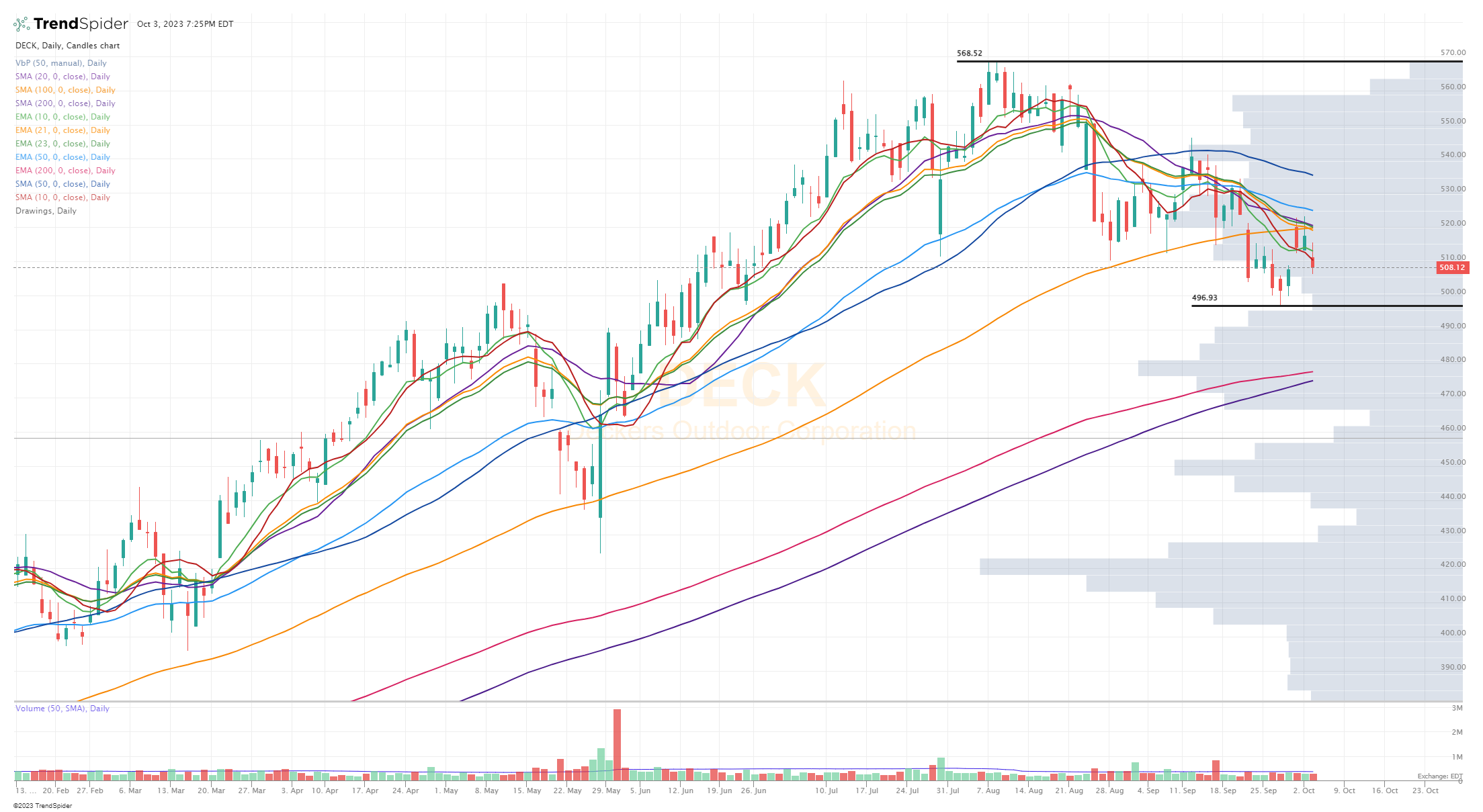

I still don’t have a position in DECK even though the stock continues to pullback. I’d consider a position closer to the 200d sma (~6% lower) at ~$475 with a stop loss below the 200d sma just in case that does not hold. I’m already having a very good year and I don’t want to risk big losses on new positions in Q4. With that said I did start a new position in ONON (On Running) yesterday at $26.00 because 25.50 has been support multiple times on pullbacks; I’ll keep the position as long as it stays above 25.00

You can follow all of this activity on my investment portfolio spreadsheet and/or watch my daily webcasts when I cover all of my daily activity.

Valuation

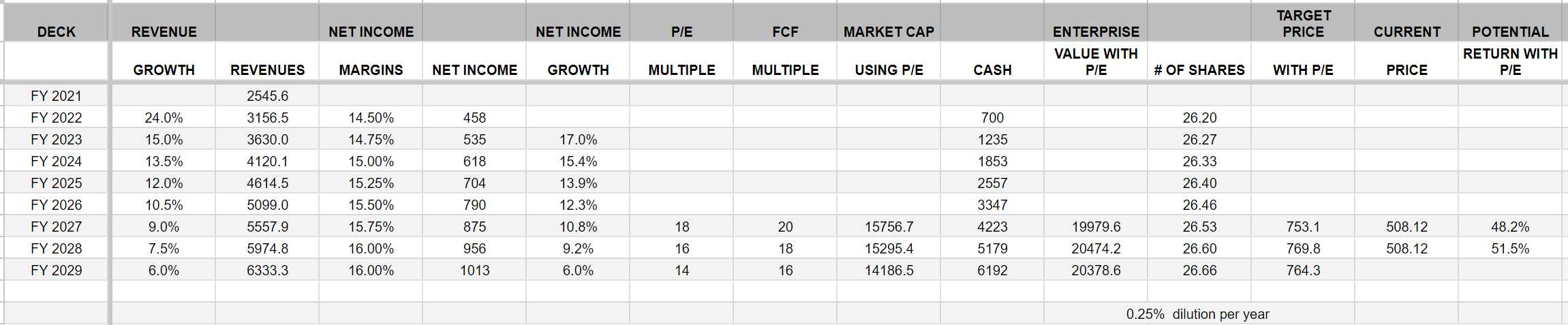

Like I stated in the part 1’s introduction, DECK is not expensive but it’s also not cheap given that growth is expected to slow down over the next 4-5 years and margins are not expected to expand which means earnings growth will be close to revenue growth which means revenue growth in the single digits also means earnings growth in the single digits so you can’t expect the stock to trade a premium P/E multiple like ONON does but that’s because they’re growing at 40%.

DECK has pulled back slightly the past 2 days since I sent out part 1 of this deep dive, with the stock closing today at $508.12 it means the current enterprise value is right around $12.5 billion so we’ll use that for the multiples below. DECK is now trading at…

3.1x FY2024 EV/SALES and 2.8x FY2025 EV/SALES

15.9x FY2024 EV/EBITDA and 13.8x FY2025 EV/SALES

21.1x FY2024 EV/NET INCOME and 18.6x EV/NET INCOME

If you look at FY2024 and FY2025 estimates for revenue and earnings growth, I’d say DECK is fairly valued at 21.1x FY2024 net income, that’s already a 1.5x PEG ratio which is probably on the higher end. Fwiw, CROX trades at 9.5x CY2024 net income although their revenue and earnings growth is expected to be slightly slower next year but that still means CROX trades at a 50% discount to DECK but the PEG ratios are similar. ONON now trades at 34.8x CY2024 net income but they’re expected to grow net income next year by 49% over CY2023 so the stock is trading with a PEG ratio below 1.0x which makes it the most attractive in my opinion.

In order for DECK to be “cheap” in my mind, the NTM P/E multiple would need to be under 15x, maybe even closer to 12x but I don’t think that’s going to happen anytime soon so you need to decide what multiple you’re willing to pay for DECK is top/bottom line growth is in the high single digits for the next few years.

Investment Model

My estimates below are slightly above the current consensus estimates but that’s because I think Hoka is likely to keep surprising to the upside as they continue to take market share in the footwear industry. Of course you could apply a bigger P/E multiple in FY2027 and FY2028 to get a higher price target but I try to be realistic in this models, unfortunately I just don’t see enough upside over the long-term to have a position however that doesn’t mean you can’t own it from time to time when the markets are doing well, technicals look good and fundamentals remain solid. I try to only own stocks that have 100% or more upside over the next 3-4 years and I think DECK would have to beat the current estimates by ~20% to make that happen which is certainly possible, just like it’s possible the stock could trade at 20x net income in FY2028 instead of 16x. DECK has similar growth rates to NKE but trades at a slightly lower multiple so it’s possible it would hold up better in any corrections however NKE has the bigger brand with a stronger long-term shareholder base.

Analysts

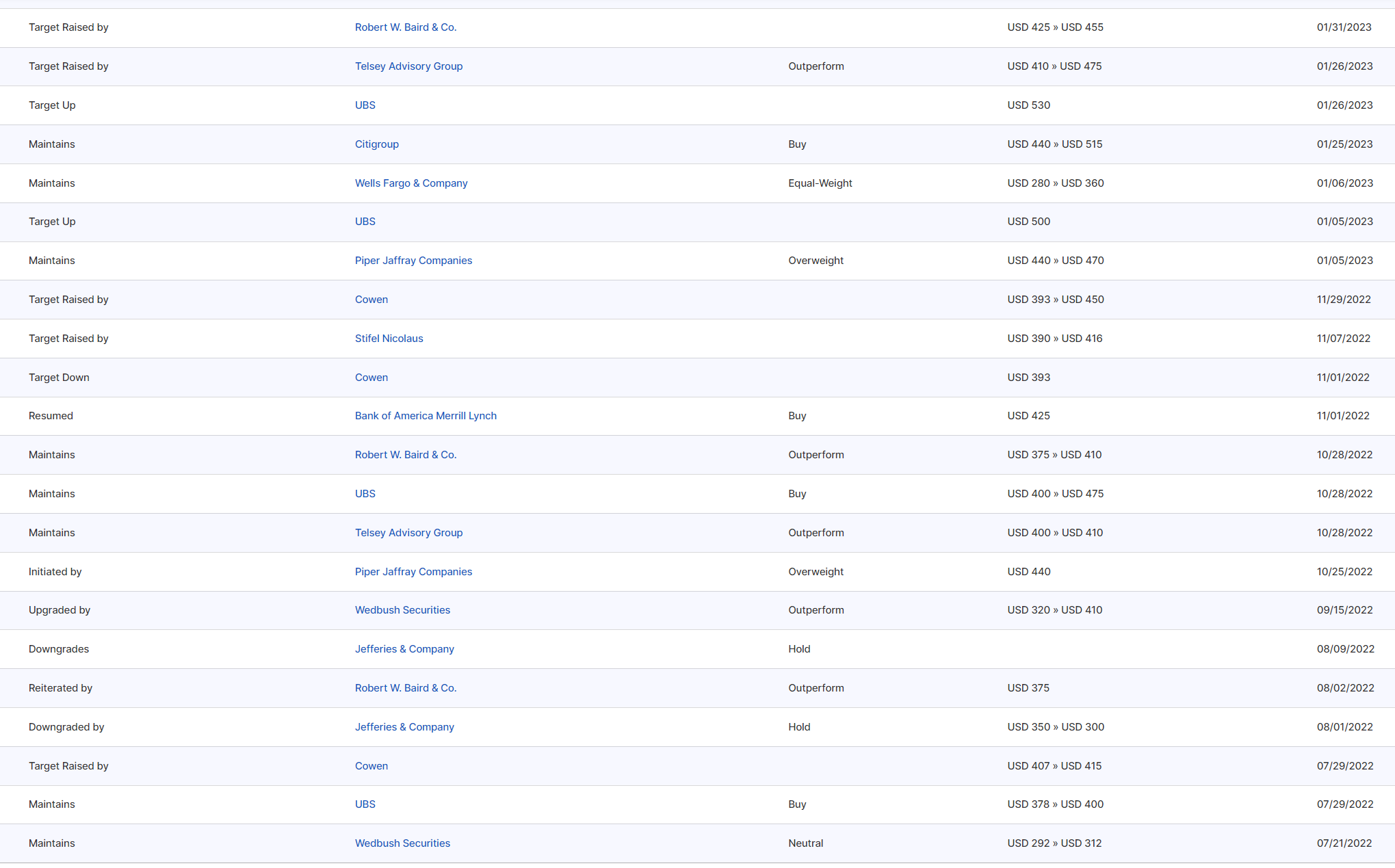

There’s ~12 analysts that cover DECK and most of them have buy/overweight ratings that range from $585 to $715 with an average price target of $585 to $615 depending on whether you want to include the analysts that have not updated their ratings in 6+ months.

Here’s what the analysts are saying:

August 15th: TD Cowen analyst John Kernan raised the firm's price target on Deckers Outdoor to $618 from $564 and keeps an Outperform rating on the shares. The firm believes Deckers deserves a higher multiple on durability of growth and sector leading financial returns as HOKA in-bound data and checks suggest upside to consensus expectations into year end

July 28th: Stifel analyst Jim Duffy raised the firm's price target on Deckers Outdoor to $600 from $550 and keeps a Buy rating on the shares after fiscal Q1 results exceeded expectations and the company's increase to its fiscal year revenue and mid-point EPS guidance exceeded the upside to Q1 consensus. With nearly 90% of the annual earnings power still ahead in Q2-Q3, "we are unsurprised that estimates move only modestly higher," said the firm, which is raising its own estimates.

July 28th: BTIG analyst Janine Stichter raised the firm's price target on Deckers Outdoor to $640 from $613 and keeps a Buy rating on the shares. The company reported another strong quarter and a raise to its annual outlook against a challenging backdrop, and while Deckers is not entirely immune to the broader environment, the investments in brand and DTC are paying dividends

July 28th: UBS raised the firm's price target on Deckers Outdoor to $720 from $715 and keeps a Buy rating on the shares. Hoka's exceptional momentum with consumers continues and think this will lead to strong FY24 sales growth and stock-driving earnings beats

July 28th: Baird analyst Jonathan Komp raised the firm's price target on Deckers Outdoor to $620 from $575 and keeps an Outperform rating on the shares. The firm its Q1 results confirmed many positives of the Decker's story, including healthy overall HOKA growth, global DTC strength, encouraging margin expansion, and an upward bias to F2024E EPS.

July 26th: Wedbush analyst Tom Nikic raised the firm's price target on Deckers Outdoor to $614 from $505 and keeps an Outperform rating on the shares. The firm continues to believe that Deckers Outdoor is one of the strongest names fundamentally in its coverage, with the Hoka brand continuing to exhibit strong momentum, UGG resonating with consumers, margin tailwinds this year, and conservative guidance. That said, Wedbush thinks the stock may take a "pause" in its upward momentum, as the share price tends to exhibit seasonality, and this seasonality is about to turn less favorable.

July 24th: Piper Sandler analyst Abbie Zvejnieks raised the firm's price target on Deckers Outdoor to $595 from $535 and keeps an Overweight rating on the shares. The analyst says Hoka demand has remained strong while investors are valuing controlled distribution. The firm believes Deckers will deliver a "beat and raise" this quarter as Hoka guidance was likely "exceedingly conservative." PIper's checks point to continued brand momentum and demand as well as low promotional levels.

July 21st: UBS raised the firm's price target on Deckers Outdoor to $715 from $610 and keeps a Buy rating on the shares. The firm's channel checks suggest Deckers' Hoka brand maintained robust revenue momentum during Q1, which should drive a 2c EPS beat for Q1, but conversations with investors suggest the market already expects a beat and raise, the analyst says in a research note.

July 21st: Citi analyst Paul Lejuez raised the firm's price target on Deckers Outdoor to $665 from $515 and keeps a Buy rating on the shares. The analyst expects a solid sales and earnings beat when Deckers reports fiscal Q1 on July 27. The firm expects a beat from better sales in Hoka direct-to-consumer and slightly stronger gross margin. The Q1 earnings are likely to further crystalize the global growth opportunity still ahead for Hoka, which will be a net positive, the analyst tells investors in a research note.

Technicals

DECK does look semi interesting on the charts, as I mentioned in the intro I’d be interested at the 200d ema/sma but not where the stock is now. I want to test the 200d moving averages and see if it holds plus I can put my stop loss just below the 200d so I can minimize my losses if it slices through. If the 200d does not hold up I could see DECK testing the May low at $424 which is -16% below today’s closing price. If I was more bullish on DECK I’d consider starting a position at current prices then average down into the 200d but that’s not the case.

If you’re someone that likes to buy stocks with strong fundamentals and strong technicals I think there are better options out there but if you really like DECK and want to have a position I’d wait until the stock reclaims the 50d ema and/or 50d sma which puts it back into an uptrend.

Conclusion

DECK is a great company and I love Hoka but it’s just hard to be super bullish on a company/stock with slowing growth that still trades at 21x FY2024 earnings, that multiple doesn’t leave any wiggle room to the downside which means if revenues slow down faster than expected, perhaps from a recession, then that multiple goes from 21x to 13x and the stock drops 30-40% from current prices.

I still think DECK should consider spinning off Hoka to unlock value because that part of the business would trade at a higher multiple (closer to ONON) and then DECK could use the cash generated from the spinoff to do a big stock buyback and/or begin paying a dividend and/or do more acquisitions. If they spun Hoka off at a $7.5 billion valuation, over the next 2 years sold 40-49% of the shares and kept a majority stake they could use that $3+ billion for a $1+ billion buyback, a 3% dividend and then spend $500 million to $1 billion to buy some emerging brands like they did with Hoka almost 10 years ago (although bargains like that probably don’t exist anymore) and Crocs had to pay $2.5 billion for HeyDude which is starting to look expensive as growth at HeyDude slows down faster than expected.

Like I said in part 1 of my deep dive, I honestly think Hoka makes the best sneakers for running, walking, and most gym activities but DECK gives me a few other brands that have me less excited as a potential shareholder although Ugg does have a relatively loyal customer base and has proven by now they’re more than just a fad.

I also have to wonder if Nike (NKE) would ever acquire DECK to get their hands on Hoka or maybe Nike would just buy Hoka off of DECK for $7-8 billion which would dump a ton of cash into DECK’s bank account and create quite an interesting scenario. If that happened I’d like to see DECK go after Sketchers (SKX) although that might be closer to a merger but SKX only trades at 8.6x NTM EV/EBITDA while DECK trades at 15.8x NTM EV/EBITDA so they could pay a 30% premium and it wouldn’t be dilutive to FY2024 or FY2025 earnings depending on how much stock was used in the deal.

Additional Sources

Management – https://ir.deckers.com/governance/management/default.aspx

Board of Directors – https://ir.deckers.com/governance/directors/default.aspx

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/910521/000091052123000025/deck-20230724.htm (page 71)

Enjoy the rest of your week.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.