Part 1: Deep dive on Deckers ($DECK)

In order to read this entire deep dive on Deckers ($DECK) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (+97% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio and trading portfolio (fwiw, my trading portfolio is up +68% YTD with a much different strategy than my investment portfolio)

Here are my other newsletters…

Company: Deckers Outdoor

Ticker: (DECK)

Website: Deckers.com

IPO date: October 1993 (traditional IPO)

IPO price: $15.00

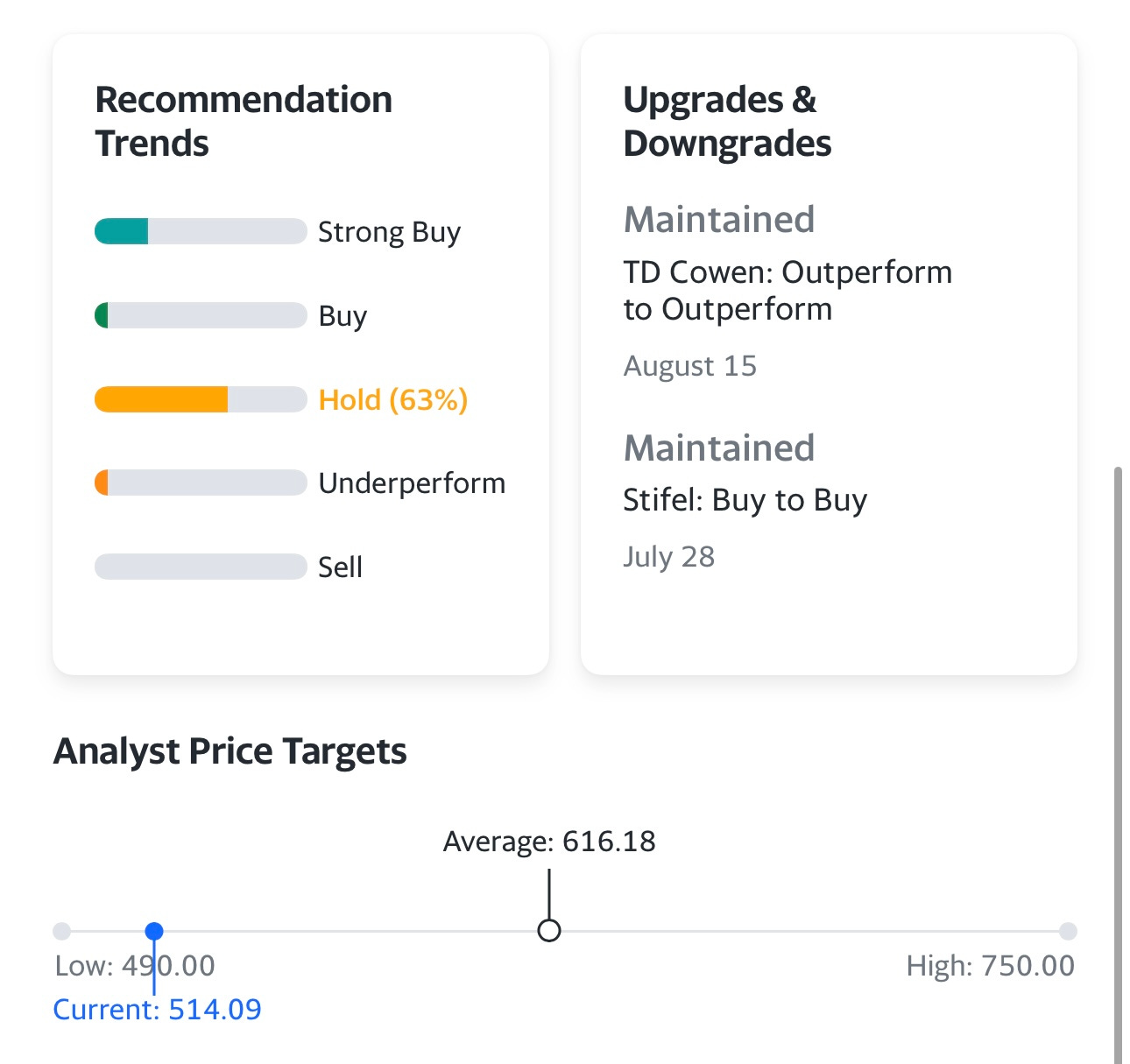

Current stock price: $514.09

Outstanding shares: 26.13 million

52 week high: $568.47 on August 08, 2023

52 week low: $298.61 on September 30, 2022

ATH: $568.47 on August 08, 2023

Market cap: $13.435 billion

Net cash/debt: +$786 million (net cash)

Enterprise value: $12.549 billion

Headquarters: Goleta, California, United States

Number of employees: 4,200+

Average price target from analysts: $616.18

Investor Relations: https://ir.deckers.com/

Q1 FY 2024 Earnings Report: https://ir.deckers.com/news-events/press-releases/press-release/2023/DECKERS-BRANDS-REPORTS-FIRST-QUARTER-FISCAL-2024-FINANCIAL-RESULTS/default.aspx

June 2023 Presentation: https://s25.q4cdn.com/376120126/files/doc_presentations/Deckers-Brands-Presentation-Baird-Conference-June-2023.pdf

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1, 2]

Below the paywall is the Deckers ($DECK) deep dive along with links to my investment portfolio (up +97% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here]

My investment models [click here]

My daily webcasts [click here]

Introduction

I don’t currently have a position in DECK however if the markets start acting better and it looks like we’re going to get a Q4 rally then DECK is one of the 8-10 stocks I’ll consider adding to my portfolio along with ELF, ONON, CROX, AXON, PLTR, SDGR, NVDA, META, TSLA and several others.

As you can see from this chart DECK has been a massive winner over the past 10 years, in fact the stock is up 750% since September 2013.

My favorite brand inside of DECK, is by far, Hoka which is their high-performance sneaker for running, gym workouts, leisure or really anything. I have 5 pairs of Hoka’s and overall they’re probably my favorite sneakers because they have the best cushion in the sole — even better than On Running — just look at the image above and it’s very clear how thick those soles are which really helps the knees, ankles, etc.

When investors talk about the best acquisitions of all time the top 3 are usually:

Facebook buying Instagram

Google buying YouTube

eBay buying PayPal

All three of these deals created a ton of shareholder value (in absolute dollars) but DECK buying Hoka for $1.5 million back in 2012 has a better ROI than all of them combined but obviously the numbers are much smaller with DECK/HOKA so it never gets talked about. It’s hard to know exactly what Instagram and YouTube would be worth as separate companies but Hoka should do $2.0+ billion of revenues over the next 12 months so it’s probably worth $7-8 billion which is a ~5,000x return on their original purchase price. I wish DECK would spin off Hoka into a separate company because that brand is way more exciting to me than their other brands like Ugg and Teva which don’t have the kind of growth that Hoka does.

As you can see below the estimates for DECK have been rising steadily over the past 3 years — back in late 2020 the analysts thought DECK would do less than $3 billion of revenues in FY2024 and now they’re on track to do $4+ billion.

My biggest concern with DECK (and Hoka)… is slowing growth which means the P/E multiple is unlikely to expand much from here unless DECK finds a way to re-accelerate growth or maybe the multiple expands if the markets are going higher and the 10Y yield is dropping (ie rising tide lifts all boats)

If you look back 15 years, DECK was growing ~50% per year but now that growth has slowed down to ~10%. This is why DECK would be my third choice in the footwear category after ONON and CROX because ONON is growing faster than DECK, while CROX has similar growth to DECK but CROX is trading at a much cheaper P/E multiple. If DECK only grows revenues by ~10% over the next 4-5 years there’s a chance the stock doubles during that time frame but I think CROX has more upside because the stock is cheaper and they have better margins (DECK with 19% EBITDA margins vs CROX with 29% EBITDA margins) which means more FCF which means bigger stock buybacks.

DECK could have $1+ billion of net cash in the next 2 quarters so we could/should see some buybacks unless they are planning to do acquisitions which I’d probably (if I was a shareholder) given their phenomenal track record with the Hoka acquisition.

DECK is not expensive at 22.7x FY2024 earnings (GAAP) but also not cheap with earnings growth expected to be around 15% over the next few years which means the stock is trading at a 1.5x PEG ratio. Fwiw, Nike ($NKE) trades at 25.6x FY2024 earnings (GAAP) with a similar expected earnings growth rate over the next few years so it’s trading at a slightly higher PEG ratio but obviously has a much stronger brand. For another comparison, ONON trades at 45x FY2024 GAAP earnings but they’re also growing earnings by 50-60% so their PEG ratio is below 1.0x which is one reason I’d own ONON before I’d own DECK or NKE.

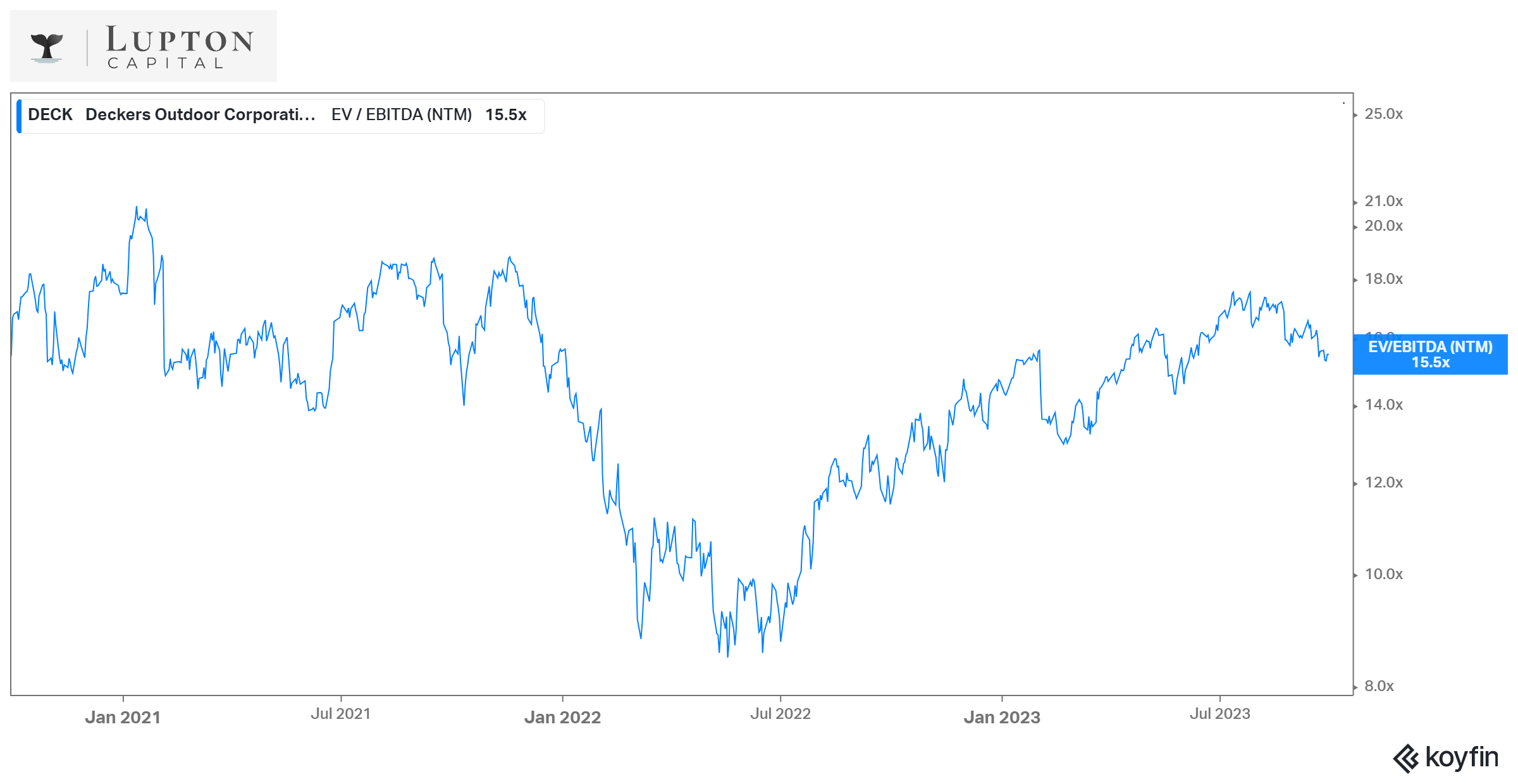

As you can see from the charts below, DECK’s valuation has dipped since the July highs but it’s still much higher than last summer when the stock bottomed out at ~$213 which means it’s up more than 100% since the May 2022 lows. These multiples are fair given the expected growth rates, I could argue that CROX and ONON are cheap given their fundamentals but I can’t make the same argument for DECK which is fully valued at current prices.

TBH, Nike ($NKE) should consider buying DECK because it would get them Hoka plus a few more brands. They could pay a 25% premium for DECK which is $642 per share or 28.4x FY2024 GAAP earnings but that’s before you account for their ~$1 billion of cash — if you include the cash they could pay a 25% premium but now that’s only 25.6x FY2025 GAAP earnings which is almost exactly where NKE’s P/E multiple is right now so the deal would not be dilutive to earnings. NKE executives should be concerned about these emerging brands like Hoka and On Running because they do pose a threat to Nike’s sneaker business.

When I look around my gym I’d say at least 40-50% of the members are now wearing Hoka or On Running whereas that number was probably under 10% a couple years ago. Just like Celsius and Ghost are taking market share from Red Bull and Monster… On Running and Hoka are taking market share from Nike, UnderArmour, Reebok, New Balance and Adidas. I know that Nike has a great selection of sneakers but they should be nervous about the cult following that Hoka and On Running have created.

I’ve never met anyone that owns a pair of Hoka sneakers and doesn’t love them. Most people that try Hoka will never switch to anything else so Hoka is definitely creating some lifelong customers but it’s the other brands inside of DECK I’d be worried about as a shareholder, they’re holding the stock back.

Another concern I have is what happens to footwear sales in a possible recession considering Hoka is the crown jewel with most sneakers selling at a higher price point — if the consumer is pulling back on discretionary spending does it mean they’re less likely to go buy another pair of $150+ Hoka’s? I think the answer is yes but I could be wrong.

Along those same lines, now that student loan payments are coming back (the moratorium is over), if consumers in their 20s, 30s and 40s are once again making $500-1000 monthly student loan payments, does that mean they have less money to buy a new pair of pricey sneakers? I think the answer is yes but I could be wrong.

Hope you enjoy this deep dive on Deckers, please let me know if I missed anything important. Part 2 should be out in the next couple days.

Company Background

The beginnings of Deckers Outdoor take place back in the early 1970s when Doug Otto, driven by a passion for surfing and an entrepreneurial dream, identified a gap in the market for high-quality sandals tailored for surfers.

Taking flip-flops as a foundation, Otto created an entirely new kind of footwear, which he called Deckers. His vision was to make both comfortable and stylish sandals that cater to the lifestyle of surfers, a goal that Otto not only achieved successfully but also made a part of Deckers Brands' philosophy for decades ahead.

The first Deckers flip-flops took the surfing community by storm, paving the way for the company that would become the owner of several iconic brands later and the business that would generate billions of dollars in revenue per year.

However, the road to this success was long and bumpy. Deckers' sandals and other beachwear products never got traction outside the surfing community. It took the company more than ten years before the pivotal moment finally happened: in 1985, a river guide, Mark Thatcher, brought Deckers' boss his Teva sandal concept.

Thatcher noticed that while traditional flip-flops were lightweight and dried quickly, they frequently slipped off his feet when he stepped in mud or water during his raft trips. He came up with the idea to add a nylon strap around the back of his heel to keep the shoes in place. Soon, other river guides and passengers started asking Thatcher to make a pair for them with his simple yet innovative invention.

He quickly realized that he could build a business out of this and shortly launched Teva, making sandals with the backstrap. The sales in the first years were challenging until Teva became a part of Deckers.

Deckers first patented Teva's universal strapping system, which would later become the backbone of the modern sport sandal category. Then, having already established relationships with key retailers, Deckers brought Teva to nationwide outdoor stores such as REI, EMS, and L.L. Bean, as well as department stores such as Nordstrom.

The popularity of the original Teva sandal skyrocketed in the next several years, becoming Deckers' most-sold product. By 1991, outdoor sports sandals conquered the entire US and became a cultural phenomenon. The sandals were so popular that people even started to wear them with socks in much cooler weather. Teva's sandal line grew to over 30 different styles, ranging from $30 to $80 per pair.

On the wave of such resounding success, Otto decided to take Deckers public. By the time the company filed for an IPO in 1993, it had several brands under its umbrella, including Sensi, a manufacturer of casual-wear beach and spa sandals, and Simple Shoes, a manufacturer of casual street shoes.

Deckers went public in October 1993 at $15 per share. That year, the company achieved almost $58 million in sales and posted earnings of $6.3 million for the first time in its history. With raised capital on the public market, Deckers continued its strategy of acquiring other promising brands in an attempt to diversify its business and offerings.

In 1995, Deckers made, perhaps, the most quintessential purchase in its history: the company acquired UGG, an Australian brand famous for its sheepskin boots. Sheepskin boots became popular among surfers in Australia in the 1960s. A surfer by the name of Brian Smith brought a pair of his sheepskin boots to the US and soon realized that sheepskin footwear was not available there. Together with his friend, they created UGG in 1978.

Like early Deckers' flip-flops and Teva's sandals, UGG boots remained a niche product for over a decade until Deckers acquired the company (for $14.6 million, which is equivalent in purchasing power to about $30 million in 2023) and re-positioned it as a luxury sheepskin brand sold through high-end retailers.

By the early 2000s, UGGs' popularity expanded beyond southern Orange County. Sales were growing double-digit quarter in and quarter out. But the real breakthrough came in 2003 after UGG boots were featured on Oprah Winfrey's show as part of "Oprah's Favorite Things." It not only led to an unprecedented surge in sales but also gave the brand worldwide fame, paving the way for it to become a cult brand and "one of the greatest success stories within the consumer category" ever since.

Otto retired from the company in 2008, leaving it in great financial shape and position for future growth and profitability. Deckers continued to grow and surpassed $1 billion in total sales in 2010. The company remained to execute its strategy of acquiring other brands, adding MOZO Shoes in 2010, a brand that produced footwear for the culinary industry, Sanuk in 2011, another surfer-oriented brand producing sidewalker surfers, sandals, shoes, yoga slings, and flip flops, and HOKA One One in 2013, a sportswear brand producing running shoes.

The latter acquisition has become the second-most important one in the company's history and may one day turn out to be the best one ever. HOKA One One was founded in 2009 in France by two ex-Salomon (a famous French sports equipment manufacturing company) employees. As runners themselves, Nicolas Mermoud and Jean-Luc Diard experienced a problem running downhill: they wanted to run much faster than existing running shoes allowed them. So, they designed their own shoe, which had an oversized outsole providing more cushion than any other running shoes at the time.

The brand's initial success was largely due to the invention of its proprietary sole, which provides better shock absorption and a more stable stride. In addition, it helps to reduce exhaustion among runners during long-distance races. HOKA's shoes' comfort and performance are still unmatched, even by brands like On, which offers highly similar products and has also seen massive success in recent years.

Under Deckers' management, HOKA became one of the fastest-growing sports footwear brands in the world, proving that the running shoe market is not limited to just giants like Asics, Adidas, and Nike. In recent years, HOKA also became the primary growth driver for Deckers, accounting for 39% of its total sales as of FY 2023.

Today, Deckers is a global leader in designing, marketing and distributing innovative footwear, apparel, and accessories developed for both everyday casual lifestyle use and high-performance activities. Its differentiated portfolio of brands, which includes UGG, HOKA, Teva, Sanuk, and Koolaburra (Deckers acquired Koolaburra in 2015 and positioned it as a value-oriented alternative to the UGG brand), is unmatched by any other company in the industry.

Going forward, the company's primary focus is building global consumer-obsessed brands for long-term success and taking this business to $5-6 billion in sales over the coming years while potentially bringing more brands under its umbrella and putting them through its well-established growth playbook.

Opportunity

Deckers operates across the fashion and casual lifestyle, performance, running, and outdoor segments – all part of the activewear market.

Trends

This market is driven by several trends, including the increasing awareness about health and wellness, digital transformation, the move from wholesale to DTC, the growing awareness of environmental impact, the rise of omnichannel retail, product innovation, and the general shift in fashion to sportswear.

Below are the key trends that will profoundly impact the market's continued growth and Deckers' in particular.

Health and wellness awareness

Increasingly, more people globally understand that movement is the key to being physically and mentally healthy. Whether it is indoor or outdoor, shoes are the foundation, paving the way for the continuous growth of the footwear segment and being the key enabler of healthy and active living.

Other segments are also net beneficiaries of this global trend. The apparel category, in general, is twice as large as footwear, according to Fortune Business Insights.

Moreover, the apparel category is projected to dominate the market further due to the rising popularity of the utilization of sports apparel for fitness and day-to-day wearing.

Product innovation

Today, shoes for active movements must be both comfortable and performance-enhanced. The latter is becoming critical for many consumers, explaining the explosive growth of such brands as On and HOKA.

More and more consumers seek more advanced shoes than they used to buy previously from brands like Nike or Adidas, with superior cushioning, enhanced grip, and support that facilitates a range of movements being the standard product features.

Fashion shift to sportswear

The focus on health and wellness, together with product innovation and generally changing lifestyle patterns (like being constantly on the move), have paved the way for a fundamental shift in fashion toward sportswear.

Sportswear has transitioned from being just part of gyms and sports fields to becoming a staple in people's daily wear wardrobes. There is even a special name for this in the fashion industry – athleisure.

Increasingly, more people are looking for comfortable shoes for traveling to and back from work or t-shirts that are breathable and quickly drying during summers and thermal resistant during winters.

Digital transformation

Traditionally, activewear products have been primarily sold in physical stores. Retail remains the main growth driver for any brand, but online sales are multiplying.

More and more companies in the industry are observing a meaningful shift in how consumers shop for products and make purchasing decisions, evidenced by decreases in retail store activity as consumers increasingly migrate to online shopping.

While many brands follow an omnichannel strategy, which allows consumers to start the buying journey in-store and finish it online, the more advanced the websites/apps and user experience become, the faster this transition will happen.

The move to DTC

Many brands in recent years have been moving away from traditional wholesale distribution channels (which involve selling products to retailers who then sell them to end consumers, resulting in lower margins and less control over brand presentation and customer experience) to Direct-to-Consumer (DTC).

A broader change in retail and consumer behavior drives this trend as brands seek to build more direct engagement between them and consumers. DTC allows brands to control every aspect of the consumer experience, as well as make their businesses more profitable by cutting the middleman.

Technology advancements here play a critical role in this move. DTC allows to generate a lot of data, which is absolutely vital for any brand today. With the help of this data, the brands not only can sell more effectively but also create better products, enhance customer experience, and increase loyalty.

DTC also allows brands to integrate sustainability into their business practices, one of the most critical aspects of every modern brand that wants to win customers at large. By controlling the supply chain processes, brands can guarantee ethical production practices and sourcing of sustainable materials.

The move to DTC is a fundamental shift in the industry and will only accelerate in the coming years.

Total Addressable Market (TAM)

According to Allied Market Research, the global activewear market size was valued at $425.5 billion in 2022. It is projected to reach $771.8 billion by 2032, growing at a CAGR of 6.2% from 2023 to 2032.

North America dominated the activewear market in 2022 and is expected to continue to dominate in the next ten years minimum.

This market is primarily dominated by several large companies, including Nike, Adidas, Asics, Columbia Sportswear, lululemon, and a few others.

Deckers' market share today is just around 0.85% (based on $3.62 billion in revenue in FY 2023), providing enough room for growth, given the market's overall size, which keeps growing further.

Growth Drivers

Deckers had three consecutive years of double-digit revenue growth, delivering a CAGR of 19% during this period.

While all analysts covering the company expect revenue growth to slow down in the coming years, Deckers still has plenty of growth opportunities ahead.

The long-term strategic vision remains focused on building HOKA into a multibillion-dollar major player in the performance athletic space across categories and geographies, growing the UGG brand by connecting with consumers through elevated experiences and a segmented product offering, expanding the DTC business through consumer acquisition and retention, and driving international growth through strategic investments.

HOKA

HOKA remains the primary growth opportunity for Deckers despite the expected decrease in revenue growth in FY 2024 and possibly beyond.

In FY 2023, HOKA generated $1.413 billion compared to $891.6 million, representing a 58.5% YoY increase. In Q1 FY 2024, the sales continued to be strong, increasing 27% YoY and generating $420 million, a quarterly record and the first time the brand eclipsed $400 million in a single quarter.

Direct-to-consumer (DTC) was the primary growth driver in the latest quarter, increasing 63% versus last year and accounting for approximately two-thirds of total brand growth. This exceptional DTC demand resulted in an improved gross margin as HOKA maintained high levels of full-price selling. Deckers continues to benefit from shifting a more significant proportion of HOKA's revenue mix to DTC.

DTC is actually the major growth driver for HOKA in the future. It is predominantly e-commerce today, so the major opportunity is in retail expansion. The company wants to expand HOKA's retail presence in the key markets to increase brand awareness and customer engagement. Retail is a critical piece of HOKA's growth because it creates an unparalleled experience and helps to showcase the broad range of different products the brand has to offer, leading to improved adoption.

This strategy is starting to pay off already, with brand awareness rapidly increasing, up 20% in FY 2023 over the prior year. More and more customers (especially the 18 to 34-year-old cohort, which remains the key target) are switching from traditional apparel/shoe brands like Nike and Adidas and choosing HOKA as the better alternative. This is especially true in international markets, where sneaker and sandal styles see increased adoption.

As to wholesale, HOKA continues to drive growth and expand its presence in existing distribution points, maintaining high levels of full-price sell-through (the period during which the products were sold for their full price). It remains one of the fastest-turning brands within the majority of the wholesale partners.

HOKA is also growing shelf space through differentiated products. The expansion and increased adoption of products beyond the brand's heritage running styles is another growth driver for HOKA.

As of Q1 FY 2024, HOKA offers over a hundred products across footwear and clothing categories for men, women, and kids. Entering the kids' market provides an avenue to further expose the brand to parents and younger athletes over the long term.

HOKA's products are sorted by activity: road running, trail running, hiking & walking, race, train & gym, and lifestyle. Within each activity, the brand has several franchises.

The company continues to update existing franchises with new, better, and more innovative products, as well as launching new exciting franchises.

A great example of franchise development is the new Mach X collection, where the team has innovated upon the original Mach collection and introduced the snappier and more competitive version.

It is an incremental addition to the already stellar footwear portfolio, led by the brand's most popular styles, Clifton and Bondi. These two franchises continue to be the frontrunners, with the Clifton 9 being received exceptionally well globally and requiring more inventory from the company due to very high demand.

This approach to launching and developing franchises allows HOKA to broaden the reach of potential customers while maintaining its position as the leader in the performance athletic space.

The results are encouraging: among DTC purchases in the US and EMEA, multi-category purchases increased 79% and 127% YoY, respectively. Across both wholesale and DTC channels, HOKA more than doubled revenue on trail and hike products.

HOKA is the company's brightest spot right now, and management puts much hope on its continued growth.

UGG

Unlike HOKA, UGG sales have been much weaker, decreasing 2.7% in FY 2023 compared to FY 2022, with a further decline of 6% YoY in Q1 FY 2024. The primary reason for this decline is the US interest in the brand is slowing down, and because the US represents 68% of total sales, this is particularly substantial for UGG, yet the brand is still expected to increase low single-digits in FY 2024.

However, the brand has been growing internationally across multiple regions and in both wholesale and DTC channels. In particular, the EMEA region and China, which benefited from lower demand from lockdowns during FY 2023, drove above-average growth. In Europe, online search interest in UGG products increased 60% YoY, with outsized strength in the UK and France.

These regions experience success in attracting consumers with more transitional styles, such as Ultra Mini, Tasman, and Classic Mini, increasing the adoption of these key global franchises year-round. This success is primarily due to a more focused approach to product marketing.

UGG also sells other categories of products, including clothing, accessories, and home products. The brand is quite popular among parents, having various products for kids starting at an infant age.

In recent years, UGG has launched several transitional franchises / category extensions with greater year-round wearing occasions. This allows it to bring customers in-store during the spring and summer seasons when UGG products historically had lower sales. Among such products are sneakers, clogs, and sandals for the beach.

Moving forward, UGG is focused on driving more business to DTC, launching new category extensions, and expanding on international markets while trying to revive interest in the US.

This iconic fashion lifestyle brand remains Deckers' leading brand, accounting for 53% of total sales, and despite short-term shrinking sales, it should perform well in the long term.

Moving to DTC

DTC is always a priority among any brand as it not only provides higher margins but also allows building direct relationships with each customer.

Furthermore, the company gains a lot of first-party data from DTC, creating an even stronger flywheel going forward in the marketplace as the brands expand globally.

Deckers plans to expand the DTC business for each brand through consumer acquisition and retention. This strategy has already been in play for several quarters with some solid recent results. In the long term, management wants to get the entire company to 50% DTC.

Own retail stores will play a significant part of this strategy, which enable Deckers to expose consumers to a more curated selection of products, directly impact the consumers’ experience with all of its brands, and sell the products at retail prices, which provide higher gross margins vs. wholesale.

As of Q1 FY 2024, the company had 164 global retail stores, including 81 concept stores and 83 outlet stores, 52 of which were located in the United States and 112 worldwide. These stores are predominantly UGG brand concept stores and UGG brand outlet stores, with just 18 being HOKA brand retail stores. Deckers plans to open more HOKA brand retail stores in the coming future.

The company has a lot of pop-up stores all around the world. It uses pop-ups to inform the management of the potential locations for permanent stores. This strategy is broadly used for growing HOKA retail store presence.

International expansion

International business currently accounts for about 32% of total sales, increasing 15.8% YoY in the recent quarter.

Deckers continues to drive international expansion through strategic investments, which include various initiatives specific to each market. For example, in China, the company is experiencing a very strong hiking business, so it has doubled down on this product category in each of its brands that sell hiking products.

New products

Deckers is actively taking steps to diversify and expand its product offerings by creating more year-round styles because its business, in general, is seasonal, with the highest percentage of UGG and Koolaburra net sales occurring in Q3 and Q4 and the highest percentage of Teva and Sanuk net sales occurring Q1 and Q2. Only HOKA's sales occur evenly throughout the year, reflecting the brand's year-round product offerings. Deckers wants to replicate HOKA's strategy with all of its brands.

Additionally, the company does category expansions. A great example is how HOKA moved beyond just running shoes to trail, hiking, and even casual lifestyle shoes like sneakers. The latter actually presents the biggest opportunity in the footwear category since it is the largest market within it. It is where the real money is. UGG has just recently launched a sneakers product line, while Teva has had it for some time.

Category expansions are vital in driving more sales among existing customers and attracting totally new customers, especially younger ones. In wholesale channels, it also helps to get more shelf space, thus driving more awareness. Awareness is the key to continuous growth for both a well-established brand like UGG and an emerging one like HOKA.

Business Model

Deckers operates a classical transaction-based business model, where the company derives all of its revenues from selling the products through wholesale (60%), including domestic and international retailers and international distributors, and DTC (40%), including e-commerce and own retail stores. Wholesale sales are slowly decreasing, giving way to more DTC sales as a percentage of total sales.

The United States remains the primary market for Deckers, accounting for 68% of total sales, but international sales are growing much faster and gradually eating up the share of total sales.

Deckers has six reportable operating segments, including five strategic business units responsible for the worldwide operations of the wholesale divisions of its brands (UGG, HOKA, Teva, Sanuk, and Other brands) and separate DTC business.

The UGG brand is sold globally, including in the US, Canada, Europe, Asia-Pacific, and Latin America. The brand's products are primarily sold through fashion lifestyle retailers (like Urban Outfitters), domestic higher-end department stores (like Nordstrom, Dillard’s, and Macy’s), streetwear and sports style retailers (like Footlocker and Journey’s), and various online retailers (like Amazon, Zappos, and Zalando).

The HOKA brand is also sold globally, including in the US, Canada, Europe, Asia-Pacific, and Latin America. Deckers sells HOKA brand footwear primarily through full-service US specialty retailers (like Fleet Feet and Road Runner Sports), outdoor retailers (like REI), select online retailers (like Zappos), other strategic partners (like DICK’s Sporting Goods and Running Warehouse in the US, Intersport and Sport 2000 in Europe, and Xebio Group and Himaraya in Japan), streetwear and sports style retailers (like Footlocker), and higher-end department stores (Nordstrom).

The Teva brand is present in the US, Canada, Europe, Asia-Pacific, and Latin America. The company sells Teva brand footwear primarily through outdoor retailers (like REI), fashion lifestyle retailers (like Urban Outfitters), other strategic partners (like DICK’s Sporting Goods in the US, and United Arrows and ABC Mart in Japan), large national retail chains (Famous Footwear and DSW), higher-end department stores (Nordstrom), and online retailers (Amazon and Zappos).

The Sanuk brand is primarily sold in the US, while Other Brands (mostly the Koolaburra brand) is sold in the US and Canada.

Gross Margin

Deckers has above industry average gross margins, with a blended gross margin of around 51%, compared to other players, including Skechers – 49%, Nike – 43.5%, Adidas – 47.5%, PUMA – 46%, Asics – 49.6%, Under Armour – 44.8%, On – 56%, and Crocs – 52.3%).

Unlike most of its competitors, Deckers was able to constantly improve the gross margin throughout the past ten years, from 47.7% in FY 2014 to 50.3% in FY 2023, though the highest gross margin of 54% has been recorded in FY 2021.

In Q1 FY 2024, the gross margin improved by more than 300 basis points due to lower freight costs, a greater mix of HOKA brand revenue, and an increased mix of DTC business.

Management expects further improvements, with a 52% gross margin anticipated in FY 2024. The more the company will move its business to DTC, the more the gross margin will improve.

Financial Snapshot

The company's financial year ends in March

Based on Q1 FY 2024

Revenue

Actual:

FY 2023 – $3.62 billion (+15.1% YoY)

Q1 FY 2024 – 675.8 million (+10% YoY)

Estimates:

FY 2024 – $4.01 billion (+10% YoY)

Operating Expenses

FY 2023 – 32.3% of net sales

Q1 FY 2024 – 40.79% of net sales

Year-over-year, operating expenses as a percentage of net sales have been gradually going down, from 38% of net sales in FY 2017 to 32.3% in FY 2023, indicating the flexibility of the company's operating model and some operating leverage it possesses.

The company continues to reinvest in key areas of the business in support of its growth targets, which include strategic marketing (specifically intended to amplify HOKA awareness in leading international markets), supply chain footprint to match the growing scale of the entire organization, enhanced e-commerce capabilities, and talent across the organization.

Stock-based compensation (SBC)

FY 2023 – 0.74% of total revenue and 0.19% of the market cap

Q1 FY 2024 – 1.03% of total revenue and 0.05% of the market cap

In the past ten years, the shares outstanding decreased by almost 25% (due to stock repurchasing), while the stock price appreciated over 700%.

Stock repurchasing

Deckers continuously repurchases stock, buying out 52,000 shares for a total of $25.5 million in Q1 FY 2024. The company has approximately $1.33 billion remaining under its stock repurchase authorization.

Net Income

Actual:

FY 2023 – $516.8 million (+14.35% YoY), representing a 14.25% net profit margin

Q1 FY 2024 – $63.6 million (+41.7% YoY), representing a 9.4% net profit margin

Estimates:

FY 2024 – $592 million (+14.6% YoY)

Starting from FY 2018 (after a tough FY 2017), earnings have been steadily accelerating, with expected further growth in the next several years at around 15% CAGR.

Balance Sheet

As of Q1 FY 2024, Deckers had $1.04 billion in cash on hand compared to a cash balance of $695.2 million a year ago. The company has no outstanding debt.

Cash Flow

The company generated $456.4 million in free cash flow (FCF) in FY 2023 (+276% YoY) and $94.5 million in Q1 FY 2024. Analysts expect $568 million in FCF in FY 2024 (+24.5%).

Deckers is expected to continue generating extensive amounts of free cash flow in the long term, which will allow the company to heavily reinvest back in its businesses (possible acquisitions) and continue executing the stock repurchasing program, which will positively impact the stock price.

Manufacturing & Supply Chain

Deckers outsources the production of all of its brands' products to independent manufacturers primarily located in Asia.

The company has a buying office in Hong Kong and on-site supervisory offices in China and Vietnam, helping it to successfully link all independent manufacturers.

Deckers is a highly ESG-driven company, and this applies to manufacturing and materials sourcing. More products are now made from recycled materials.

For example, the UGG brand’s Classic Mini Regenerate and Tasman Regenerate are crafted with raw materials from ranches that practice regenerative agriculture. UGG also offers a consumer-facing repair service, UGGrenew, to extend the life of Classic Boots. The HOKA brand continues to focus on integrating more environmentally preferred materials in its footwear and apparel collections. Teva continues to work with TerraCycle to give well-worn Teva sandals new life as downcycled materials. The Sanuk brand’s Veg Out Collection features 100% plant-based sneakers crafted using plant-based and recycled materials.

Competitive Advantages

Competition

Deckers operates in a highly fragmented and extremely competitive market of footwear, apparel, and accessories. The rise of outsourced manufacturing and e-commerce has made it easier for new companies to enter these markets; hence, the competition is only increasing.

The company competes with wholesalers and direct retailers of sports footwear, apparel, and accessories and other apparel sellers that do not specialize in the sports segment and sell more fashion and lifestyle products.

Alongside main competitors are Nike, Adidas, Puma, Under Armour, Lululemon, Jordan, New Balance, Reebok, Columbia Sportswear, and Asics. These are the largest companies in the sports segment, with Nike holding the biggest market share and making almost 50 times more in sales than HOKA.

Traditionally, brands like Nike and Adidas have dominated the footwear market. However, the changing consumer preferences, characterized by a demand for more advanced and specialized footwear, have led to a decline in their absolute dominance. They must adapt to the new landscape where more innovative brands like HOKA, On, and Brooks are increasingly winning more customers.

UGG, on the other side, primarily competes with companies that offer footwear and apparel for cold weather, including EMU Australia (which offers similar quality sheepskin boots at comparable prices), Bearpaw (another similar brand that offers sheepskin footwear), Koolaburra (despite being owned by Deckers, it offers more affordable alternatives to UGG boots), North Face (which offers alternative winter boots and footwear), and many others.

Competitive Advantages

One of the distinctive characteristics of Deckers is that it has a diverse portfolio of strong and recognizable brands, each with its unique identity and target audience. Its differentiated brands have been able to create lasting consumer connections for so many years, maintaining the quality and authenticity of its products – the primary reason why millions of consumers around the world keep buying them.

Deckers has also been able to innovate while quickly adapting to continuously changing market trends. Its unique ability to introduce exciting innovation into both fashion and performance products has been its primary competitive advantage. For example, innovation is a big part of the HOKA brand. This helps win new customers and eat the market share of giants like Nike and Adidas.

Risks

The footwear, apparel, and accessories markets are subject to rapidly changing consumer preferences and fashion trends, which may result in less demand for specific products and brands. For example, the Sanduk brand saw significant declines in sales in the past several years due to the brand's primary focus on casual footwear, which has become less popular in recent years.

The current demand for products that Deckers' brands offer is wicker across the board due to slowing discretionary spending everywhere.

The competition remains one of the biggest risks for Deckers despite slowly eating the market share in key markets. Deckers has already experienced how giants like Nike can introduce similar products, win back the market share, and take away its customers.

UGG's sales and demand in the US are shrinking.

Wholesale partners (which account for 60% of total sales) choose to receive products later into the year instead of a front loaded preference the company saw in the last couple of years.

Supply chain disruptions of any kind significantly affect companies like Deckers.

100% of manufacturing facilities that produce all Deckers products are located outside the US, predominantly in China.

Additional Sources

Management – https://ir.deckers.com/governance/management/default.aspx

Board of Directors – https://ir.deckers.com/governance/directors/default.aspx

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/910521/000091052123000025/deck-20230724.htm (page 71)

Enjoy the rest of your weekend.

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.