Deep dive on Chewy ($CHWY)

In order to read this entire deep dive on Chewy ($CHWY) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (+94% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about both of my portfolios (trading and investment) throughout the day including my market commentary, stock charts, earnings analysis, analyst upgrades/downgrade and much more… this is also where I chat with subscribers and answer questions.

Here are my other newsletters…

Company: Chewy

Ticker: (CHWY)

Website: Chewy.com

IPO date: June 14, 2019 (traditional IPO)

IPO price: $22.00

Current stock price: $25.76

Outstanding shares: 427.4 million (dual-class)

52 week high: $52.88 on February 03, 2023

52 week low: $27.77 on August 17, 2023

ATH: $120.00 on February 16, 2021

Market cap: $11.09 billion

Net cash/debt: +$275 million

Enterprise value: $10.825 billion

Headquarters: Boston, MA, and Plantation, FL, United States

Number of employees: ~19,400+

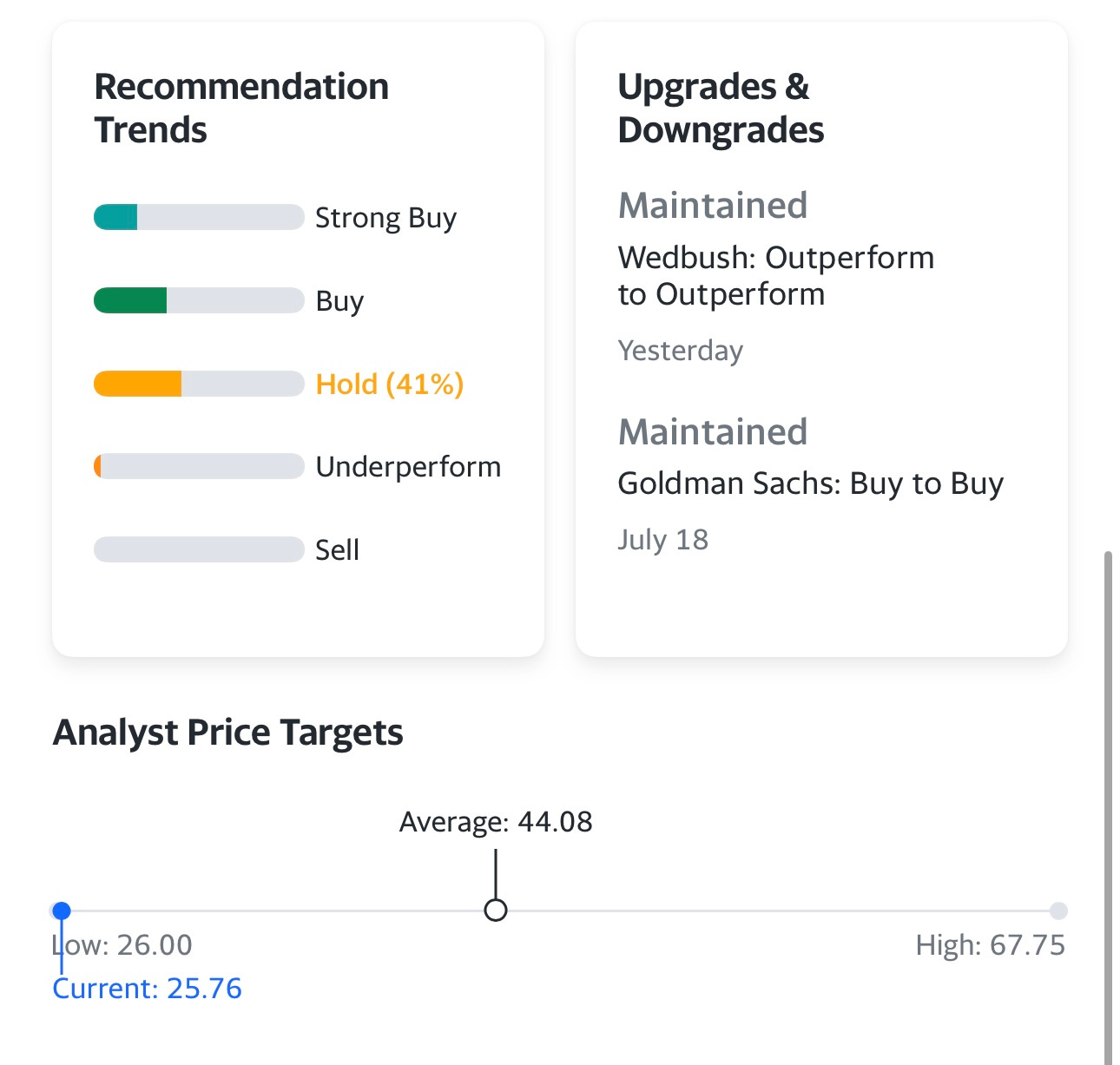

Average price target from analysts: $39.75 (STA) to $44.08 (Yahoo)

Investor Relations: https://investor.chewy.com

Q1 2023 Earnings Report: https://investor.chewy.com/news-and-events/news/news-details/2023/Chewy-Announces-First-Quarter-2023-Financial-Results/default.aspx

Q1 2023 Letter to Shareholders: https://s23.q4cdn.com/610444331/files/doc_financials/2023/q1/Q1-2023-Shareholder-Letter-FINAL.pdf

Outline

Introduction

Company Background

Opportunity

Business Model

Competitive Advantages

Risks

Valuation

Investment Model

Analysts

Technicals

Conclusion

Additional Sources

Below the paywall is the CHWY deep dive along with links to my investment portfolio (up +94% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here] new link for August/September

My investment models [click here] new link for August/September

My daily webcasts [click here] new link for August/September

Introduction

Disclosure: I do not have a position in CHWY and I have no plans to start one in the near term. CHWY does report earnings this week so I’ll be watching closely because there are things I like about the company however the stock’s performance over the next 3-4 years will come down to two things of which I don’t have enough conviction or clarity… growth and margins

CHWY might be the ultimate example of a great company that is loved by customers but not necessarily a great stock to own because the business model is flawed and by that I mean their margins are razor thin so it’s been hard for them to generate any significant profits and now that growth is slowing it might continue to be a disappointing stock for shareholders. With that in mind, CHWY is approaching the all-time lows since the 2019 IPO and with the stock down 78.5% from the 2021 highs, the expectations have never been lower.

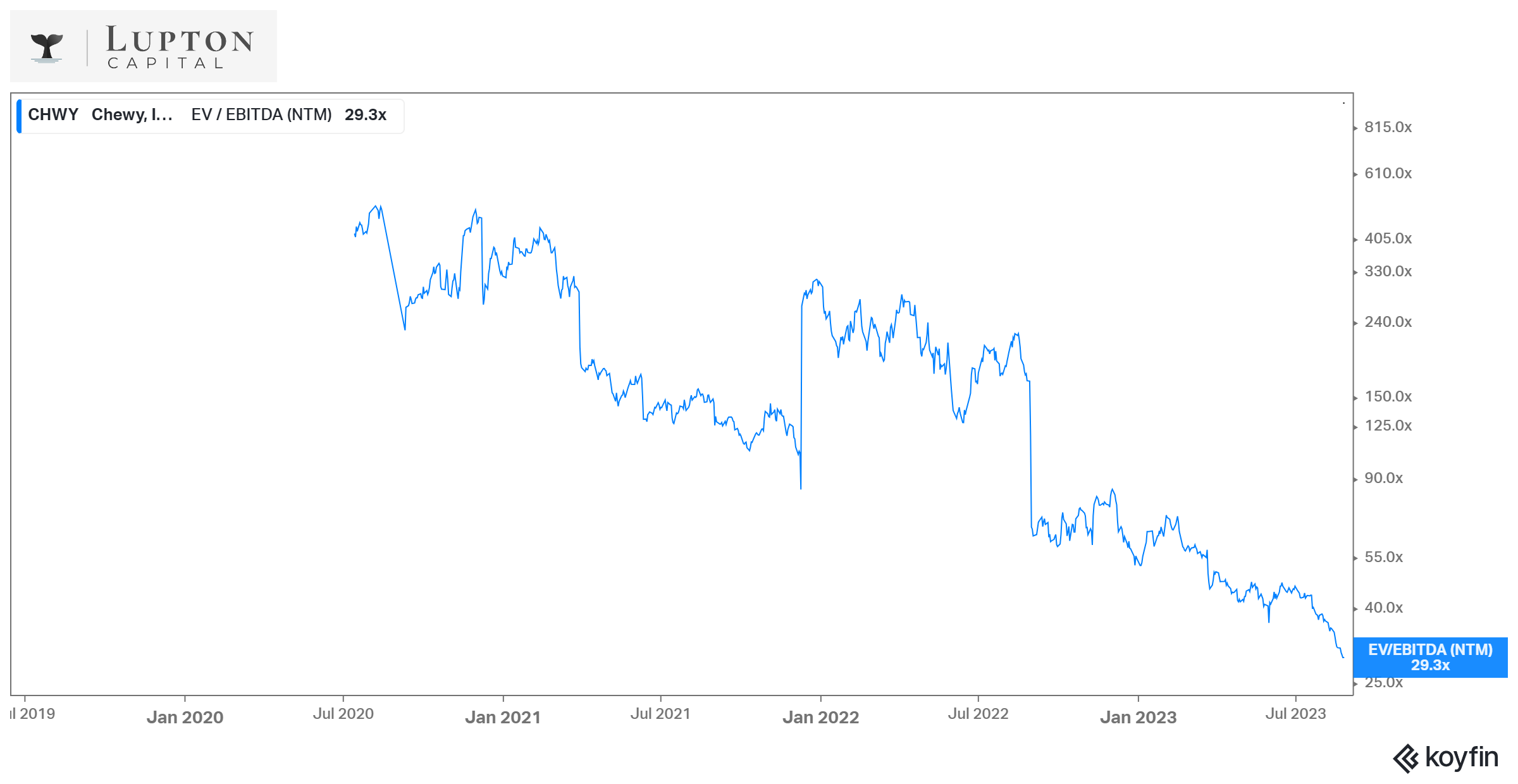

CHWY has also never been cheaper in terms of EV/GP, EV/EBITDA and EV/SALES however multiples are lower because the growth has never been slower. During the pandemic CHWY was growing at 40-50% and now they’re only growing at 10-15% so the stock has gotten re-rated by investors and rightfully so.

CHWY has a very loyal customer base but it’s proving to be hard and expensive to keep growing that customer base; on top of that shipping heavy products (like bags of pet food) to customers really chews into their margins.

Fwiw, I live in high-rise building in downtown Boston so of course our package room is always packed with Amazon boxes but the second most popular brand/box I see is definitely CHWY. When you’re living in the city it’s way more convenient to order from CHWY as opposed to driving to the nearest PetSmart or Petco (or taking an Uber) to the nearest pet store plus the CVS down the street is a ripoff and nobody wants to carry 40-pound bags of dog food down the street.

CHWY has done a nice job scaling to $10 billion in revenues but now that growth is slowing down they’re expanding into new categories like pet healthcare/meds and pet insurance as well as starting their international expansion however there’s no guarantee they’ll be successful in other countries and in the meantime it could cost alot of upfront capital to build out the infrastructure and being acquiring customers.

CHWY’s story is pretty wild because it launched in 2011 then got acquired by PetSmart for $3.35 billion, then PetSmart got acquired for $8.7 billion then the private equity group that bought PetSmart spun out Chewy into a new publicly traded company.

At the 2021 highs, CHWY was valued just shy of $50 billion which would have been a reasonable valuation if revenue growth had stayed at 47% but obviously that didn’t happen. Many other tech, cloud and ecommerce stocks are also down 60-90% over the past two years for the same reasons… growth slowed and the multiples got compressed.

I put CHWY in the same bucket with SE and CPNG, they’ve turned into mature ecommerce companies with slowing growth and low margins but they still have a chance to be good stocks if they can grow at 10-20% while expanding net income margins by 1-2% per year. If growth is below 10% per year, margins don’t expand by at least 1% per year and SBC stays high at ~2% per year then these stocks will all disappoint. Each of them is trading near the all time lows because the fundamentals have continued to deteriorate but now the valuations are finally realistic given future estimates and I think they each have 100% upside over the next 3-5 years which is decent but not good enough for me to own them yet.

If I ever get a dog, there’s a 100% chance I’ll be a CHWY customer.

CHWY reports earnings this week and I’m not sure what to expect but the stock was up ~21.5% after their last earnings report — however the stock has given back all of those gains over the past 3 months and it’s now trading 12.6% below where it was trading at their last report so maybe sentiment has gotten too negative once again and CHWY could have another big move to the upside. I’m actually tempted to buy a few call options for this reason.

With CHWY trading near it’s all time low, I wonder if AMZN would ever want to acquire them? Nobody does logistics better than AMZN and they might have the ability to improve margins faster than CHWY could on their own.

Company Background

The initial idea of Chewy came to Ryan Cohen in 2011 when he was standing in a local pet store and discussing the dietary needs of his toy poodle, Tylee. Looking to start a new business (online jewelry), he came to the realization that the pet supplies market held immense potential, especially online.

Cohen was not spooked by the infamous story of pets.com, which went bust in 2000 with a roar. On the contrary, he saw an opportunity: in 2011, Americans spent more than $50 billion on pet products, according to the American Pet Products Association, while online penetration was just a couple of percent.

E-commerce was just getting started back then, and selling pet products online presented a tremendous opportunity. Cohen shared this idea with his long-time friend, Michael Day, and in June 2011, MrChewy (the company's initial name before it was changed to just Chewy) was born. The newly-created company aimed to revolutionize the pet supplies market by offering a vast range of products at competitive prices with the convenience of online shopping.

However, back in 2011, everyone was quite skeptical about this idea. It took two years and over 100 "no's" from investors for Cohen and Day to finally raise the first outside capital ($15 million from Volition Capital) to help further develop and grow their platform.

What investors from Volition Capital saw in Chewy was its unique approach, which eventually brought the company to enormous success: Chewy is now the second-largest online retailer (after Amazon) of pet food and other pet-related products in the US, with more than 20 million customers.

From the company's early days, Cohen and Day recognized the emotional bond between pets and their owners. They believed buying food and pet-related products for furry friends should have a different customer experience. So Chewy aimed to create the best shopping experience, from user-friendly website design to personalized product recommendations and efficient delivery services.

This customer-centric approach not only led to winning millions of customers along the way (many of whom changed their way of shopping for pet products forever) but also to exponential sales growth. From 2011 to 2017, the company grew its net sales from just $2 million to over $2 billion, 50%+ of which came from Chewy's Autoship program.

The Autoship program is a subscription-based service that allows customers to schedule regular deliveries of pet products, ensuring that they never run out of essentials like pet food, treats, or medications. Customers could set a flexible frequency for automatic shipments instead of manually placing an order each time. Subscriptions could be canceled anytime, and Chewy notifies customers before each shipment so that last-minute changes can be made, including skipping the delivery if enough supplies are on hand.

Buying pet food is essential and habitual, so making this process automatic was one of the most impactful decisions ever made by the company. Today, Autoship accounts for over 75% of all sales, providing Chewy with predictable and recurring revenue while having an army of loyal, repeat customers.

By 2017, Chewy was capturing half of all online pet food sales in the US. The founders started considering an IPO when the acquisition offers came first from Petco and then PetSmart, two of the biggest names in pet retail.

Both deals were lucrative, each with its benefits for Chewy. Eventually, Cohen and Day chose PetSmart's deal, which came all-cash and allowed Chewy to operate as a separate entity. In May 2017, the deal was finalized for an impressive $3.35 billion, making it the largest e-commerce business acquisition at the time.

After the acquisition, Chewy continued its growth trajectory. In 2018, the company generated $3.53 billion in sales, growing almost 70% YoY. That same year, Chewy began diversifying from just selling products to offering services. The first ever service was an online pharmacy, providing prescription medications in collaboration with veterinarians.

A year later, the company filed for an IPO after all. Chewy's shares began trading on the NYSE on June 14, 2019, at $22 per share, above the expected range of $19-$21. The stock soared to $41 on the first day of its trading before closing at $34.99 (+60%). The company raised $1 billion from the stock sale at a more than $15 billion valuation. Following the IPO, PetSmart retained 70% of the company’s common stock and held approximately 77% voting power. Today, PetSmart remains the largest Chewy shareholder with a 72.8% stake.

Becoming public marked a new chapter in Chewy's history. Both founders left the company a year prior, and a new CEO, Sumit Singh (who now owns approximately 0.2% of the company worth $37 million), was appointed to lead the company further. Singh had extensive experience working in public companies, previously holding various roles at Amazon and Dell.

In his first year as a CEO, Chewy generated $4.84 billion in revenue, continuing its solid growth trajectory, although the pace was much slower (37% YoY) than in the previous three years. And then the pandemic happened.

2020 saw a significant surge in the adoption of pets all around the world and in the US particularly, with 11 million new pets added in the country. At the same time, consumers increasingly turned to online shopping, including for pet-related products, with many consumers buying online for the first time.

As a result, Chewy's net sales soared to $7.14 billion in 2020 (47% YoY), and its stock skyrocketed to its all-time high of $120 on February 16, 2021, growing almost 5x from the pandemic lows.

But the trend of "pandemic pets" started to slowly vanish. While the company continued to prove its reputation as a vigorous top-line YoY grower, the actual growth was slowing down year after year. The stock price has followed, dropping more than 70% from its peak.

The decline in revenue growth was inevitable since the company would have reached a plateau in the number of active customers at some point anyway. However, the biggest concern among investors was/is how the company translates its growth into profits. Chewy had/still has a hard time generating meaningful earnings despite doing billions in revenue. The company became GAAP profitable only in 2022, posting $49.2 million in net income.

While most analysts covering Chewy expect the company to post negative earnings in 2023, Chewy is still in its early days of realizing the economies of scale needed to produce substantial long-term profits. Furthermore, the company is firing on cylinders to enter new niches within the pet industry, further cementing its dominant position and creating new ways to cross-sell to its massive base of more than 20 million active customers. Chewy may no longer be a growth business, but it is a fantastic company that will gradually compound earnings for many years ahead.

Opportunity

Chewy operates in a large and growing industry in the US, consisting of pet food and treats, pet supplies and medications, other pet health products, and pet services.

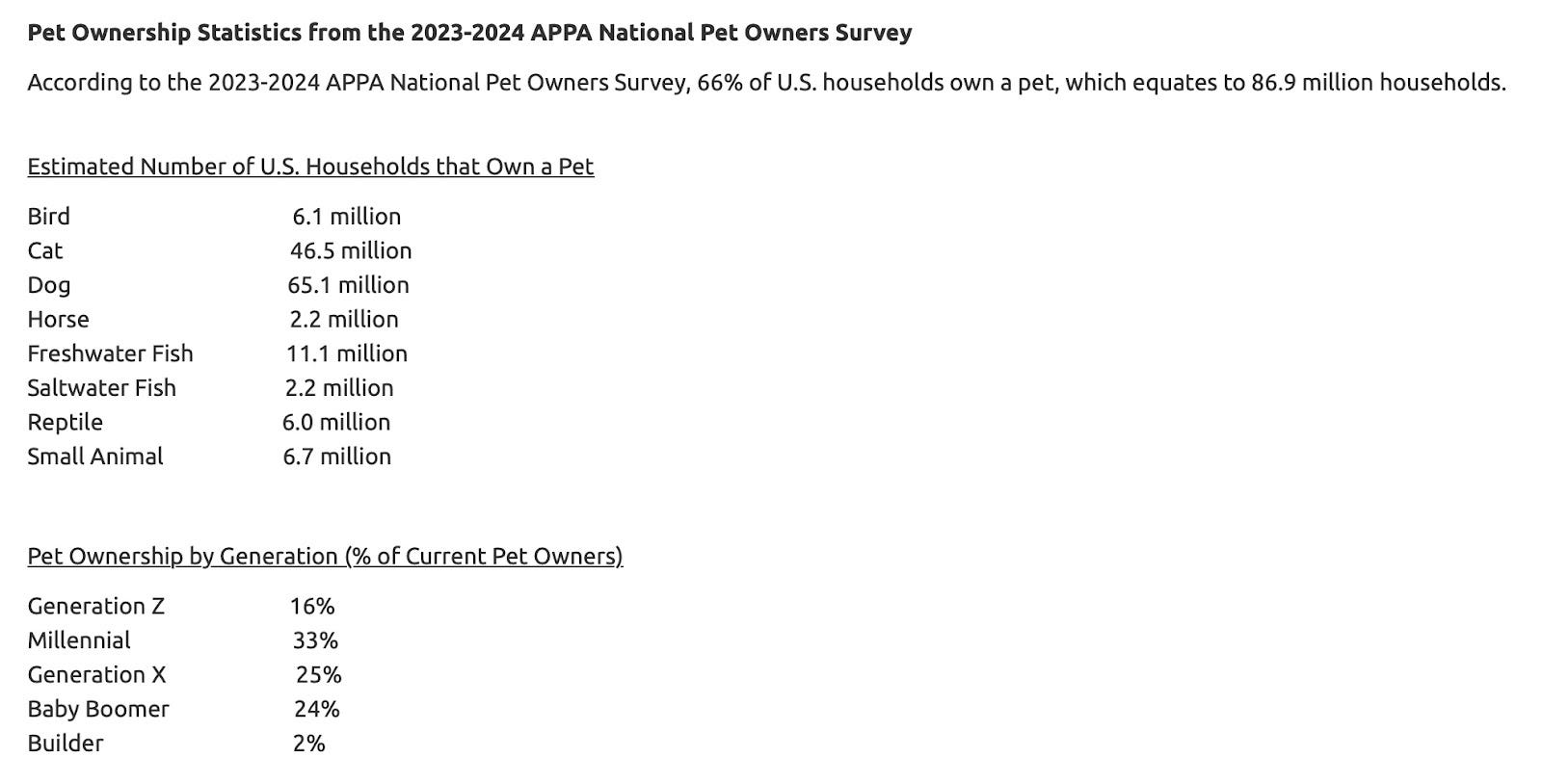

The US is among the top countries in the world with the highest percentage of pet ownership. In fact, it is the number one country in the world with dogs per capita (65.1 million US households own a dog). It also has the largest pet dog population of any other country.

The latest pet ownership statistics (according to the American Pet Products Association) show that approximately 66% of all US households own a pet, with Millenials (the largest demographic group in the country with the highest spending power and adoption of online shopping/services) leading the way.

Besides high and growing pet ownership, this industry has a number of other ongoing trends that profoundly benefit Chewy.

"Pet humanization"

Over the past few years, there has been a considerable change in how pet owners view and treat their pets. This shift in perspective is commonly referred to as "pet humanization." It involves recognizing pets as important members of the family.

Many pet owners now provide the same level of care and attention to their pets that they would give to their loved ones. According to Packaged Facts, a staggering 94% of dog or cat owners view their pets as family members. Furthermore, 90% of dog owners, 87% of cat owners, and 85% of other pet owners agree that pets are central to their home life.

As pets are now considered part of the family, there is a growing demand for the best possible care and quality products and services. An impressive 89% of pet owners actively seek products to improve their pets' health and wellness and are willing to spend more on premium goods and services.

The trend of pet humanization has also led to an increase in customized pet products. Understanding that each pet is unique, having its own set of dietary needs and preferences, pet parents are increasingly seeking tailored solutions. According to the same research by Packaged Facts, 61% of pet owners are willing to pay more for food customized for their pet's dietary requirements. One-size-fits-all products are increasingly replaced by personalized offerings catering to individual pet needs.

Pet humanization echoes the deepening bond between humans and their pets, indicating that this trend is not going anywhere. As pets continue to be a significant part of their owners' lives, the demand for pet products and services will only grow.

Shift to buying pet products online

Historically, pet owners bought food and other pet products in brick-and-mortar stores. Companies like PetSmart and PetCo were the go-to places for pet owners. However, in recent years, purchasing pet goods and services online has gained immense popularity among consumers. And this is not just a mere trend (the pandemic effect). This is a gradual shift in the behavior and preferences of millions of consumers.

The data confirms this: according to Packaged Facts, the share of online shopping in US retail pet product sales skyrocketed from 16% in 2017 to approximately 38% in 2022 (32% CAGR), with over $21 billion of pet food and treats bought online by almost half of all pet-owning households in the country.

Packaged Facts further estimates that the e-commerce channel will increase to 48% of total retail pet product sales by 2026, while the number of households will be far above 50% as more and more consumers seek out the convenience of home delivery and subscription-based purchasing.

Subscription-based purchasing

Chewy's Autoship program took the pet industry by storm. The subscription-based model, which guarantees regular, scheduled deliveries of various pet products, has been gaining massive adoption in recent years.

According to Packaged Facts, 58% of pet owners utilized subscription-based purchasing in 2022, including a range of products, from pet food and treats to essentials like litter and medications.

By opting for a subscription-based purchasing plan, consumers can eliminate the hassle of manually reordering products that require regular replenishment, such as pet food or medications. With subscriptions, consumers know their supplies are always on hand and won't run out unexpectedly.

Subscriptions are especially popular among younger, more affluent age groups. Millennials and Gen Zers, who are increasingly adopting pets, show a strong adoption of subscription models, with a whopping 71% adoption rate.

With its appeal of being convenient and automated, subscription-based purchasing in the pet industry will only grow going forward, fostering loyalty, reducing customer churn, and increasing average spending.

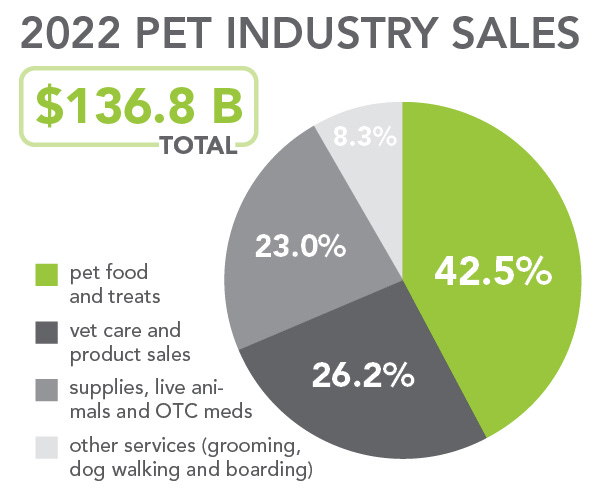

Total Addressable Market (TAM)

According to Packaged Facts, spending on pet products in the US grew from $82 billion in 2016 to an estimated $138 billion in 2022, representing a 9.1% CAGR.

Spending in 2022 grew by 10.8% compared to 2021, with pet foods and treats being the highest spend category (approximately $58 billion) and increasing the most (16.2% YoY).

On average, each household in the US spent around $1,032 in 2022 on pet food, treats, supplies, and medicine.

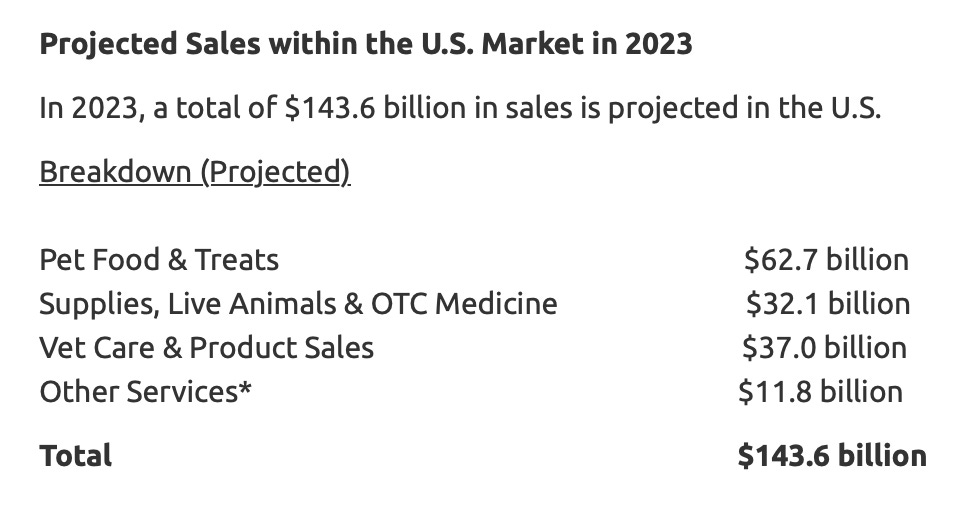

Packaged Facts further projects this market to grow at a CAGR of over 6.9% from 2022 to 2026, with retail pet food and treats projected to grow at a CAGR of over 6.5% over that period. In 2023, the US pet industry is expected to grow by almost 5% and reach approximately $143.6 billion.

Chewy keeps expanding its TAM, moving from offering primarily food and treats to also offering pet supplies and OTC medicine, as well as health services like pet insurance and telehealth.

The opportunity for Chewy remains significant: the company generated $10 billion in 2022, just 7% of the size of the total pet market.

Growth Drivers

Chewy is one of the rare companies with that many growth opportunities, both existing and new. The new opportunities have the potential to increase Chewy's addressable market by at least 30%, helping the company continuously grow its revenue and earnings for years ahead.

Existing customers

Chewy has a base of 20.4 million active customers (who made at least one purchase within the preceding 364-day period). While the number of active users has stayed pretty flat (a slight decline of 1% YoY in Q1 2023) for the past 12 months, the net sales per active customer (NSPAC) have been steadily and continuously growing, indicating that existing customers are spending more with the company by placing larger orders.

Net sales per active customer were $372 in 2020, $430 in 2021 (+15.6%), and $495 in 2022 (+15.1%). In Q1 2023, this figure increased further to $512 (+15% YoY).

Consistent NSPAC growth is driven by strong and ongoing customer engagement in programs like Autoship and expansion in cross-category purchases, which are the primary drivers of average spending growth.

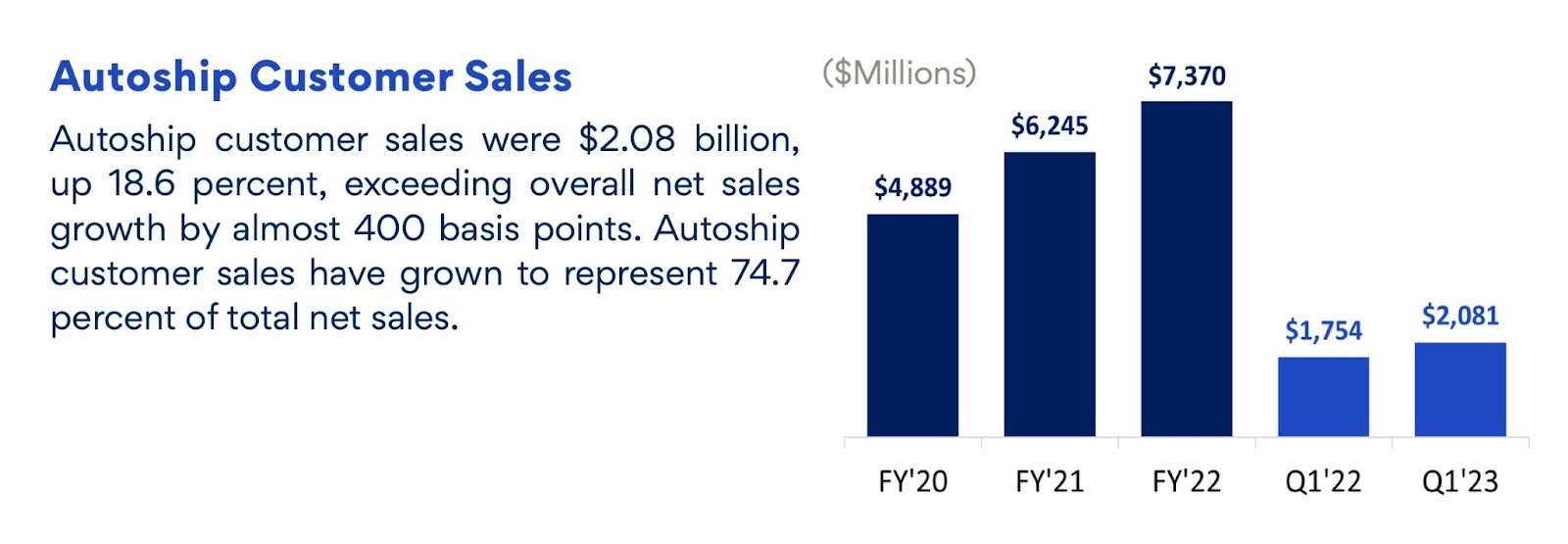

The Autoship program shows solid numbers, driving recurring and predictable revenue and long-term customer loyalty for Chewy. Autoship customer sales have been on a constant rise, expanding from $4.88 billion in 2020 to $6.24 billion in 2021 (+27.7%) to $7.37 billion in 2020 (+18%). In Q1 2023, Autoship customer sales grew 18.6% compared to Q1 2022, accounting now for almost 75% of all net sales (up from 68.4% in 2020, 70.2% in 2021, and 73% in 2022).

Chewy expects to continue to expand the share of customers’ wallets, especially those who have been with the company for more than one year. Oldest cohorts historically have been spending more as they discover over time the wide range of products and services and the value proposition Chewy provides.

Private-label products

In response to many unmet needs by branded products and the opportunity to pursue less competitive categories like hard goods, Chewy launched its first private-level brand, Frisco, back in 2016, selling various hard goods, from carriers and leashes to litter and toys. It was followed by the launch of two more brands, American Journey and Tylee’s, selling consumables like pet food and treats.

Most recently, in 2022, Chewy launched Vibeful, the company's first private brand in the pet wellness category, featuring products ranging from multivitamins to hip and joint supplements.

Growing the penetration of its private-label brands (from the current mid-single digit) is an important part of Chewy's strategy as it helps not only increase customer stickiness but also improve gross margins, which have been historically low primarily because of the cost of products of other suppliers.

Health services

Chewy aims to provide a one-stop shop for all pet owners' needs, not only for food and treats. The company began expanding to the healthcare segment (which represents 1/3 of the entire pet industry in the US today) in 2018 by launching Chewy Pharmacy, a full-service online pharmacy for pet owners to shop for prescription medications. By 2023, it far surpassed others and became the largest online pet pharmacy in the US.

In 2020, the company launched “Connect with a Vet,” a telehealth service allowing pet parents to connect directly with licensed veterinarians. Since 2022, this feature is complimentary to all registered customers.

That same year, Chewy also added a compounding pharmacy, allowing customers to order compounding medications in the form of customized, pharmaceutical-grade, prescription medications that meet their pets’ unique needs.

In 2021, the company launched Practice Hub, a complete e-commerce solution for veterinarians that can integrate Chewy with their existing management software to manage pre-approved prescriptions and enable practices to earn revenue with Chewy while it handles all inventory, fulfillment, shipping, and customer service. Chewy now works with over 1,000 veterinary practices.

Finally, in 2022, Chewy entered the pet insurance market with the CarePlus product suite of Insurance and Wellness plans. This is an entirely new opportunity for Chewy, which can help the company accelerate revenue growth and increase gross margins.

CarePlus plans are available across a wide spectrum of coverage options and price points. Chewy now works with the two best-in-class providers, Lemonade and Trupanion, allowing it to meet the needs of a broader range of pet parents.

The company currently drives broader awareness and education around its insurance product offerings, but the opportunity is significant since it is an underpenetrated and highly profitable category.

Today, fewer than 5% of Chewy customers buy all pet healthcare products from Chewy. Management is looking to make healthcare 30% of Chewy's business in the near future, providing long-term growth for the company.

International expansion

So far, Chewy has been operating in the US only. Putting together its US business on a steady trajectory of growth and profitability, Chewy seems finally ready for an international expansion.

When the company announced its plans to go international, many analysts expected it to go to Europe. But the cost and time to expand to that market is incredibly high, so the most logical step was to go across the border – to Canada.

Canada is clearly a much smaller market with lower internet penetration in the pet category. According to the Canadian Animal Health Institute and GlobalData, approximately 60% of Canadian households own at least one dog or pet. Canada had 15.3 million households in 2021, spending an average of $800 per household on their pets. It translates into approximately $7.2 billion opportunity. With that, only about 23% is currently made online, making the current opportunity for Chewy at around $1.65 billion.

Chewy's management believes that the Canadian market will grow to $12-$15 billion in the next five years, with significant online expansion.

"As we assessed which geography would be most suitable for our expansion plans, we honed in on Canada's large and growing market, where we see a path to achieving market share and profitability akin to our US business. Canada has a healthy and increasing e-commerce penetration where we can offer a differentiated value proposition relative to existing players in the market and build the same level of trust with Canadian pet parents that those in the US have come to associate with the Chewy brand." – from Q1 2023 earnings call.

Chewy expects to launch in the Greater Toronto area, the largest metropolitan area in Canada, in Q3 2023 before taking a gradual and responsible approach to expanding to other areas.

While the market size is ten times smaller than that of the US, Canada still provides a meaningful opportunity for Chewy, especially having undergone a multi-year transition of its tech stack into the cloud. The company can now leverage its platform to be reliably deployed in Canada without meaningful incremental investment.

"We do not anticipate this market requiring material CapEx investment through at least 2024. More broadly, on a company-wide level, we do not expect our investments in Canada to deviate us from our projected long-term profitability, cost or CapEx targets." – from Q1 2023 earnings call.

Business Model

Chewy operates an asset-heavy business model characterized by a high inventory of pet products and low gross margins.

To ensure that it has a wide variety of products readily available to ship to customers as soon as the orders are placed and to deliver them as fast as possible, Chewy must maintain a substantial inventory of pet products across its 17 fulfillment centers. The company hosts more than 3,500 carefully selected brands on its platform, offering more than 110,000 products and services.

Additionally, to attract and retain customers in a highly competitive market where the company primarily competes with Amazon (more about it later), Chewy must offer products at competitive, often discounted prices, further limiting already thin gross margins.

Revenue Streams

Chewy primarily generates revenue from selling pet products on its platform. The company sells pet food and treats from both third-party brands and its private-label brands, various pet supply products (such as toys, supplements, grooming products, beds, bowls, and many others), and pet pharmacy products (medications, health supplements, and other pharmacy-related products).

The company provides two options to buy pet products: regular purchase (for full price) and purchase through the Autoship program (with a 5% discount).

In an attempt to increase the customers' average spending, Chewy also launched various pet parent products, which include personalized gifts (like mugs, blankets, memorials, and many others), home goods (wall decor, doormats, picture frames, and many others), and even clothing and accessories.

Most recently, Chewy began actively diversifying its offerings with pet services like telehealth and pet insurance. While the former is now free (chat is free for everyone, video calls are free for Autoship customers and certain CarePlus holders, but $19.99 per 20-minute video call for others), the latter is growing to a significant part of Chewy's business. Chewy's insurance plans start from $20 per month.

In 2022, Chewy introduced a beta version of sponsored ads, which are dedicated product placements on its website. These ads promote specific products from select vendors with precise targeting, providing enhanced user experience and allowing the company to tap into a high-margin ad business.

Management segments the company's revenue into three categories: Consumables, Hardgoods, and Other.

Consumables are the main contributor to net sales and their growth, while Hardgoods category has been shrinking quarter in and quarter out and being replaced by the Other category, which includes healthcare products. The company is making a push with the Hardgoods category (which offers higher gross margins), launching and marketing its private-label brands, but it is still early to see any meaningful results.

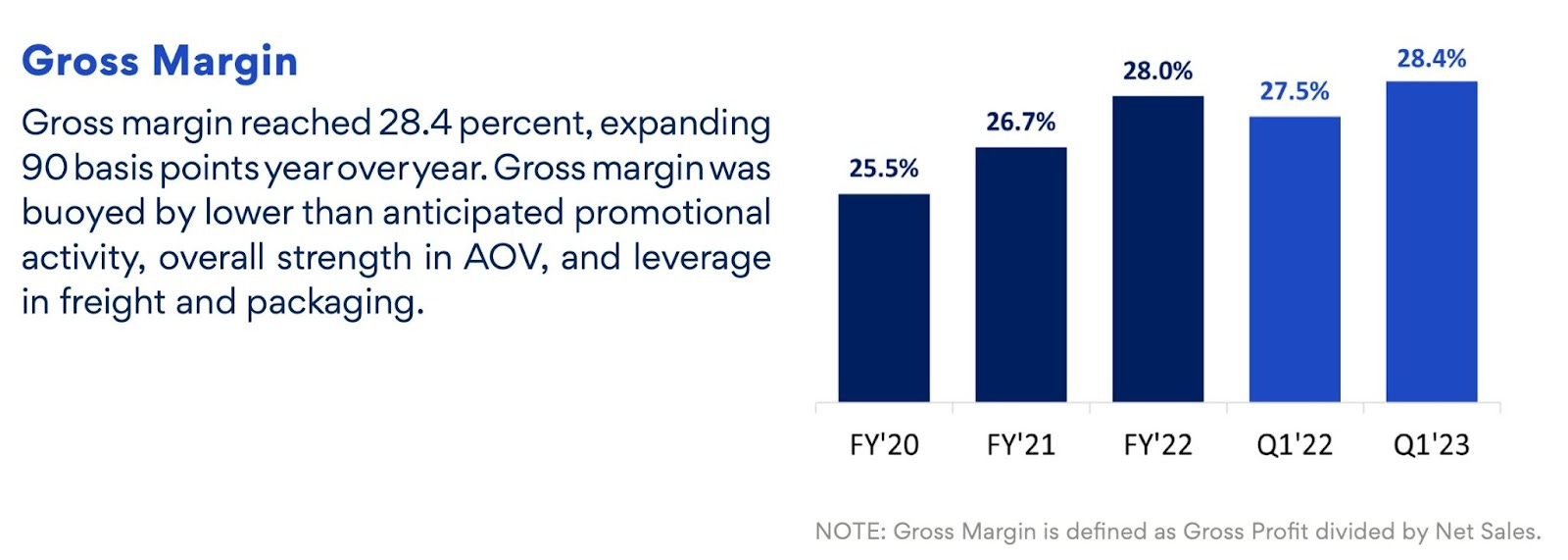

Gross Margin

Chewy began by selling third-party brand products, which have always been a low-margin business. Over the past few years, the company has broadened its range of products/services (including its private-label brands) to boost its gross margins.

As a result, the total gross margin has seen a steady increase from 17.4% in 2016 to 20.23% in 2018 to 25.5% in 2020 to 28% in 2022. The company further increased it to 28.4% in Q1 2023, exceeding analysts' expectations. This push was buoyed by lower than anticipated promotional activity, overall strength in average spending, and better than expected leverage at the freight and packaging level.

But no matter how hard the company tries to manage costs and negotiate deals with third-party brands, being an online retailer in the pet category, there is a limit to how high the gross margin can go. Most likely, Chewy will hit the ceiling at around 35% eventually.

Operating Expenses

Chewy spends around 27% of total revenue on selling, general, and administrative expenses, which have been more or less consistent for the past eight years.

Operating expenses are also growing pretty much in line with the revenue growth, showing that the company has little operational leverage.

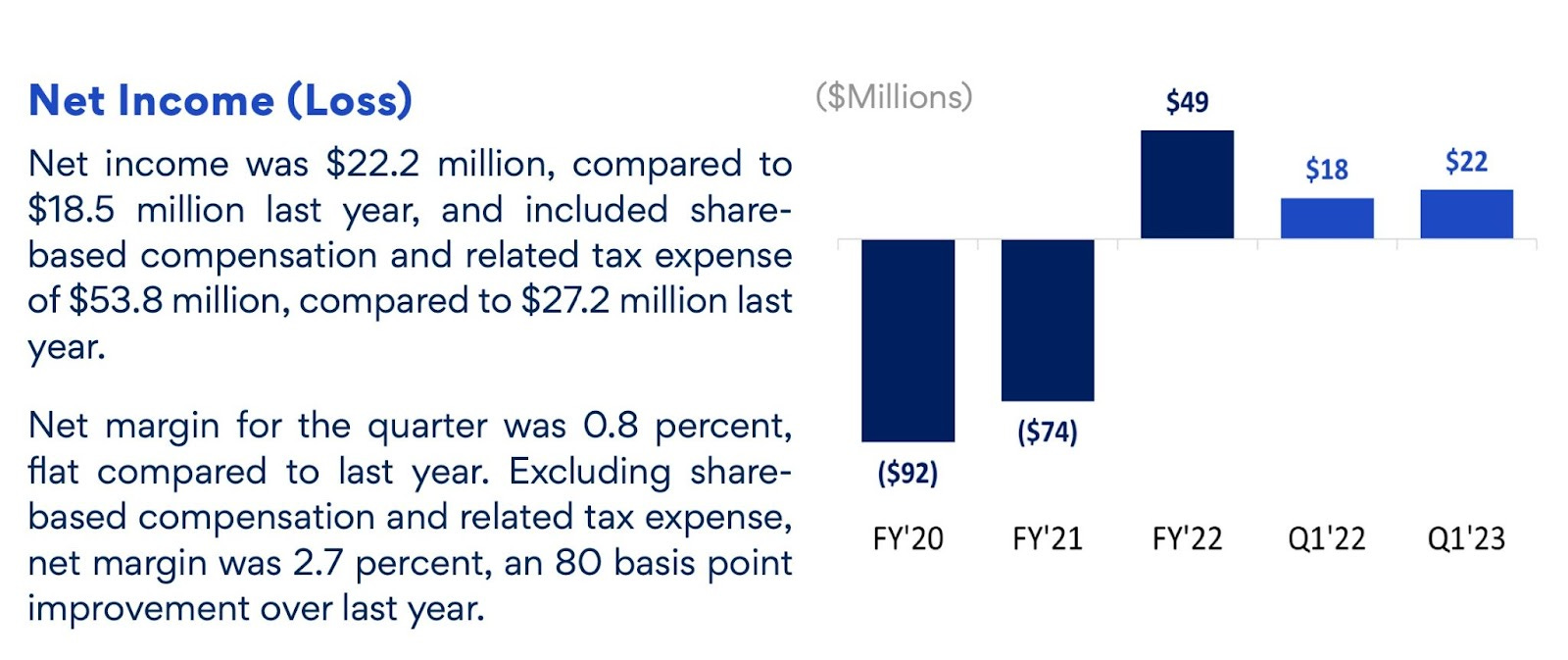

Profitability

Chewy historically had a problem converting its revenue into profits, primarily due to the high costs of goods and operating expenses.

The company finally succeeded in posting positive earnings in 2022, delivering $49 million in net income for the first time since its inception.

The start of 2023 continued this trend, with the company reporting $22 million in net income in Q1 2023.

However, most analysts expect the company to end the year in negative territory, posting losses but minor.

With the move to more high gross margin offerings and further increasing operational efficiency, Chewy can significantly boost its bottom line in the coming years.

Analysts expect the company to return to positive earnings in 2024 and grow from there at a rapid pace.

Stock-based compensation (SBC) accounts for 1.74% of total revenue and 0.4% of the market cap, which seems reasonable, though it exceeds the operating income by several times.

Since going public in 2019, Chewy has increased the number of shares outstanding by a moderate 7.23%, while the stock is now below the IPO price by almost 20%.

Balance Sheet

Chewy has an exceptional balance sheet with approximately $803 million in cash, cash equivalents, and marketable securities, and no debt.

While all its competitors are heavily leveraged, paying interest fees quarterly, Chewy is actually making additional income from interest payments ($9.29 million in 2022 and $8 million in Q1 2023 alone).

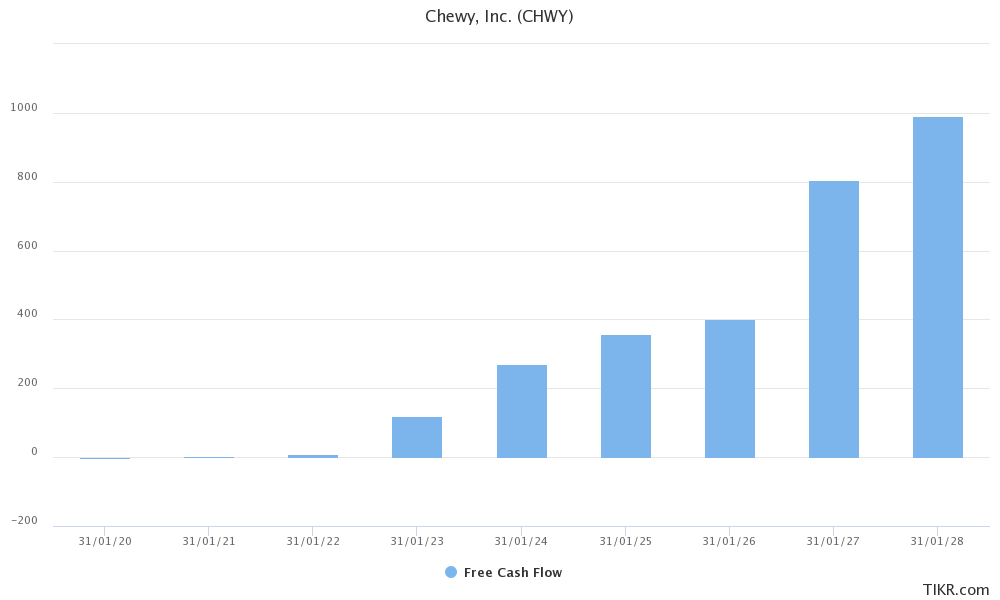

Cash Flow

The company made astonishing progress in generating cash lately. Its free cash flow soared from $9 million in 2021 to $119 million in 2022. FCF accelerated even more in Q1 2023 and reached $127 million, more than in the whole of 2022.

FCF is projected to skyrocket to almost $1 billion by 2027, providing Chewy plenty of cash to further invest in growth opportunities and possibly make share buybacks.

Competitive Advantages

Competition

The pet industry is a highly competitive market with a vast number of channels through which customers can purchase pet products and services, both online (pure-play e-commerce stores and large e-commerce platforms like Amazon) and offline (pet specialty stores, mass merchandisers/discount stores/supercenters, food stores, wholesale clubs, farm/feed stores, independent pet channel, dollar stores, drug stores, natural food, and veterinary).

Chewy operates solely online and, therefore, primarily competes with other e-commerce platforms. Amazon, perhaps, is its largest and main competitor. Amazon tops the online part of the pet market with a 46% share, followed by Chewy with 35% and Walmart with 8%. The remaining market share is divided among other players, including Petsmart (~2%) and PetCo (~1.2%).

In recent years, Amazon has been increasingly focusing on the pet category, including launching its private-label brand, Wag. Amazon still loses money on each sale of pet food on its platform but keeps prices low in order not to lose its market share, greatly hurting Chewy, which cannot afford to lose money as Amazon. Furthermore, Amazon offers Subscribe & Save discounts and a 5% cashback/discount with Amazon Credit Card, creating additional competitive pressure.

Chewy also competes with veterinarians in pet medications and other health products category. Veterinarians have a competitive advantage over Chewy as many pet owners will find it more convenient to purchase prescription medications directly from their veterinarians during an office visit.

Competitive Advantages

Chewy is undoubtedly a pure-play leader in the online pet industry, which not only rapidly eats away the share of brick-and-mortar stores but also slowly catches up with Amazon.

There are several competitive strengths that make Chewy different from other competitors (including Amazon), from commitment to customer service as the core of the brand to the largest selection of high-quality pet food, treats, and supplies to Autoship subscription to offering competitive prices and so on.

When it comes to competitive advantages, it boils down to brand and technology.

Brand

Chewy has successfully built a strong brand that associates with the pet industry. Suffice it to say Chewy became a household name in the US.

The success of the Chewy brand is attributable to its reputation for reliability and exceptional customer service. The latter is at the core of what the company does. The Internet is full of amazing stories where Chewy employees went the extra mile to ensure customers would be delighted and even surprised by small touches like handwritten notes or sent flowers on the pet's death day.

This level of customer service not only builds an army of loyal customers who will likely stick with the brand for as long as they are pet parents but also brings more and more new customers who quickly turn to loyal ones. This is hard to replicate for anyone, even for Amazon.

So, a strong brand attracts loyalty, and loyalty allows to pass price increases onto customers, showing a substantial pricing power.

Technology

Chewy's advanced technology platform stands as a cornerstone of its competitive edge in the online pet market. On the scale, it enables growing sales volume and increasing the number of active customers while cutting down on overall costs. So, as Chewy processes more transactions, the cost per transaction reduces, leading to better operational efficiency and long-term profitability.

This technology also allows Chewy to automate many planning and fulfillment processes. This allowed the company to build reliable automated shipments, further streamlining operations, reducing errors, and increasing efficiency. Recently, the company has put into operation the fourth automated fulfillment center.

“Our growing network of automated FCs, accompanied by our supply chain transformation, is improving margin efficiency and we believe will contribute to scaling SG&A over the long term.” – from Q1 2023 earnings call.

Chewy's technology also empowers its customer service, providing employees with real-time customer data and advanced tools. Not even Amazon has similar capabilities.

Furthermore, from its inception, Chewy's founders wanted to build an exceptional shopping experience for pet products online. With intuitive navigation, detailed product descriptions and photos, customer reviews, and personalized recommendations – Chewy has the most frictionless and easy-to-use experience you will find among all competitors, including Amazon (in some features).

Resilience

There are not too many industries that, even in times of economic downturns, can remain resilient. The pet category, especially the pet health segment, has proved its defensiveness over time. Moreover, this particular industry has significantly outperformed others in troubled times.

For example, during the 2008-2010 recession, while overall consumer spending in the US declined, pet spending increased by 12%, according to the American Pet Products Association. In 2010 alone, spending in the US on entertainment decreased by 7.0%, food by 3.8%, housing by 2.0%, and apparel and services by 1.4%, while spending on pets increased by 6.2%.

More recently, due to high inflation and economic uncertainty, 68% of consumers have been cutting back on household expenses in the last 12 months. But only 15% of consumers cut back on pet care, proving yet again how resilient this industry is.

Risks

Growth sustainability

Chewy is no longer a growth company. The growth rate has been steadily declining in the past several years. While the company will still grow at a 12-15% rate per year in the near term, the growth will most likely hit a plateau at some point.

Gross margin expansion

Selling third-party products, many of which are bulky and heavy (like pet food and litter), will always stay a low-margin business. The only way to expand the gross margin is to increase the share of products with higher gross margins (like private-label brands) and offer more services with higher margins (like pet insurance).

However, no matter how hard Chewy grows the percentage of these as of the total net sales, the company will still hit the gross margin expansion ceiling at some point.

Profitability

After finally turning profitable in 2022, the company is projected to end 2023 with losses again, though minor. It is still unclear when the company will be able to return to profitability and how quickly earnings will grow from there.

Amazon

Amazon will remain the biggest risk for Chewy. Competing with Amazon is hard and capital-intensive. More information about the competition is in the Competitive Advantages section.

Ownership

PetSmart (affiliates of BC Partners) still owns the majority stake in Chewy (72.8%) and holds the total voting power. There are seven board members representing BC Partners. Not only the direction of the business is set by this group of people, but also, if BC Partners chooses to sell any of its stake in Chewy, it will have significant pressure on the stock price.

Valuation

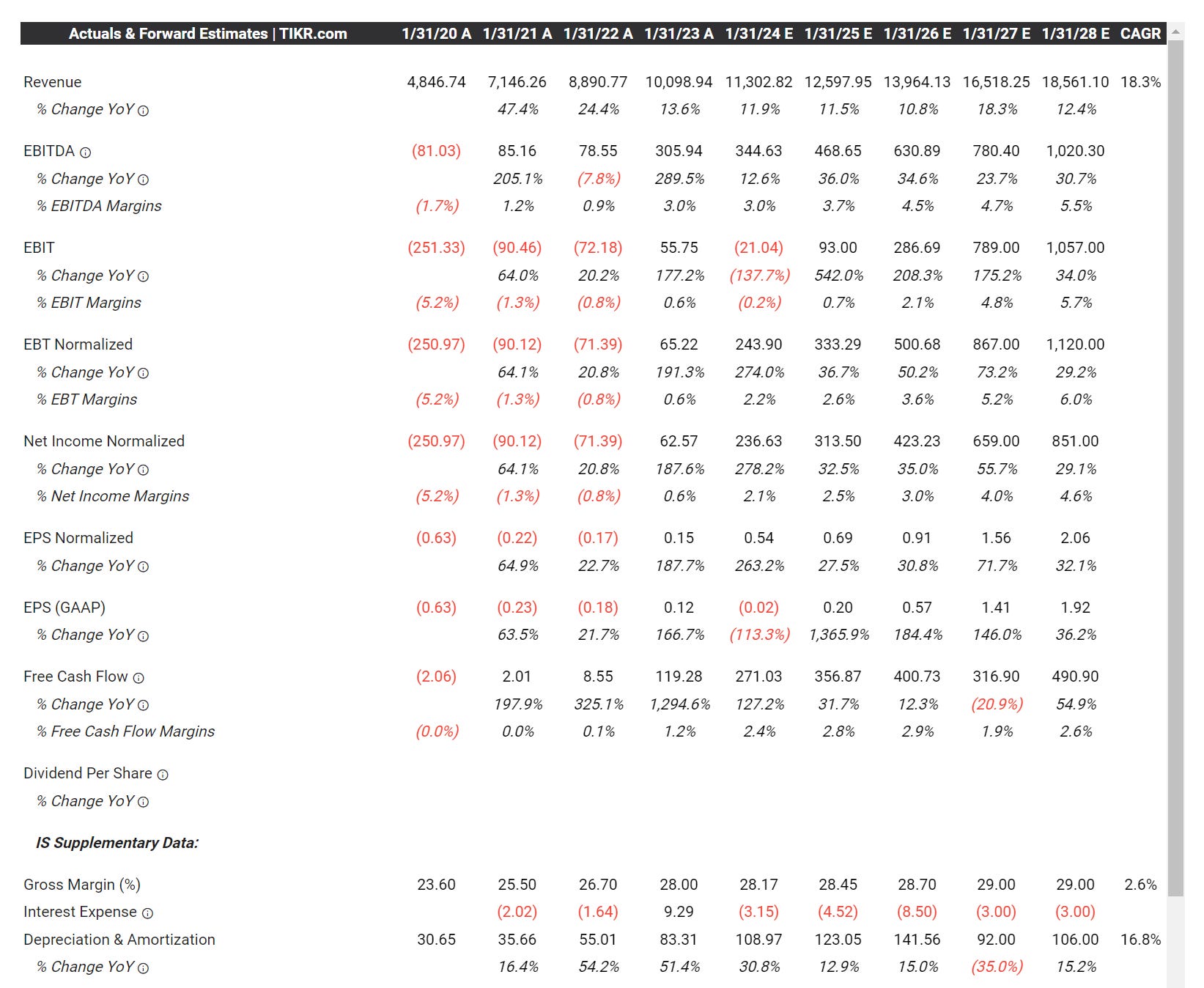

Besides the slowing growth and low margins, the first thing that stands out to me in these analyst estimates is the spike in FY2027 growth expectations, perhaps that’s when the analysts believe CHWY will start to see meaningful growth from their international expansion plans.

CHWY’s valuation has gotten more attractive in recent months, it now reflects a company with a sizable revenue base but slowing growth and razor thin margins.

Using the current $10.8 billion enterprise value and the consensus estimates below, CHWY is now trading at…

0.95x FY2024 EV/SALES and 0.85x FY2025 EV/SALES

31.3x FY2024 EV/EBITDA and 23.0x FY2025 EV/EBITDA

45.6x FY2024 EV/NET INCOME and 34.4x FY2025 EV/NET INCOME

39.8x FY2024 EV/FCF and 30.2x FY2025 EV/FCF

Looking at all these multiples and the respective growth rates for FY2024 and FY2025, I’d say CHWY is fairly valued. If CHWY is expected to grow net income by ~35% per year for the next few years then the stock trading at 34.4x FY2025 net income is fair so you’re unlikely to see any meaningful multiple expansion unless they company can report better than expected revenues and earnings.

Investment Model

My estimates are slightly more conservative on revenues (I don’t have them spiking by 18% in FY2027) however I’m slightly more bullish on net income margins, I think they can reach 6% by FY2028 however this might not be the case if they are spending lots of money on international expansion in which case it might help grow the top line but could hurt the bottom line.

As you can see from my model, if CHWY hits my estimates than I do think the stock has more than 100% upside over the next 3-5 years assuming investors are willing to pay 36x earnings in FY2027 and 30x earnings in FY2028

fwiw, my investment models for CHWY and CPNG look very similar with revenue growth in the low double digits for the next few years and net income margins expanding from 1-2% to 5-6% over the next few years. CPNG is a more diversified company and closer to a combination of AMZN, NFLX, DASH but the company is based on South Korea and a finite number of potential customers. I believe the US population is 10x bigger so I’d probably favor CHWY for that reason alone but CPNG is a very cool company and very focused on keeping the customer happy.

Analysts

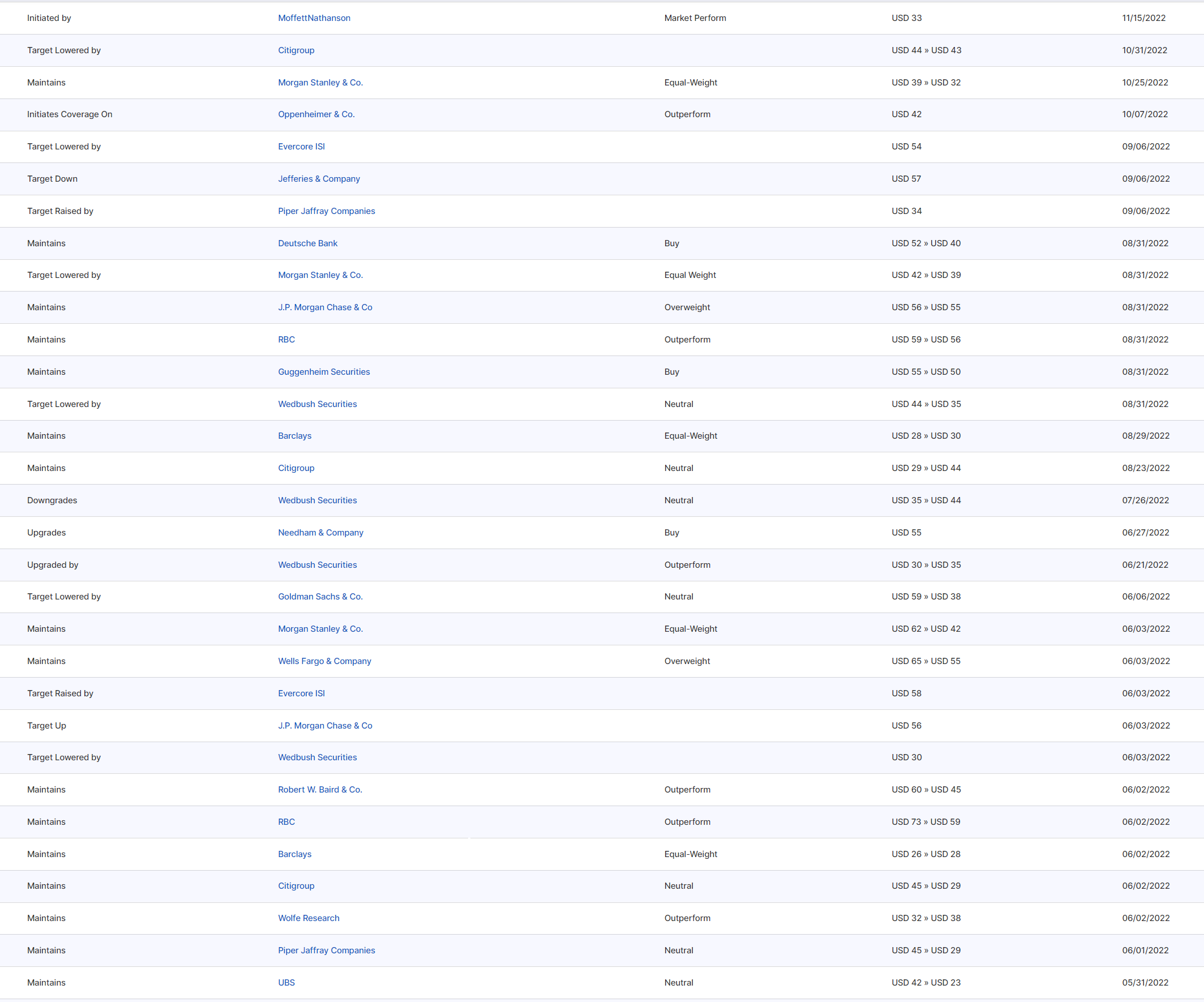

If you scroll back to 2021 you’ll see many of these analysts had price targets in the $80-100 range but as the growth has slowed and the stock price has fallen those same analysts now have price targets in the $30-50 range however most of them kept their buy ratings the whole way down.

Here’s what the analysts have been saying:

April 25th: Wedbush analyst Seth Basham lowered the firm's price target on Chewy to $31 from $45 and keeps an Outperform rating on the shares. The firm sees modest downside risk to Q2 results and guidance when the company reports earnings on August 30, but thinks this is largely factored into buyside expectations, the analyst tells investors in a research note. Wedbush says competitor read-throughs and industry data points lean negative, but feels that Chewy's relative lack of exposure to discretionary products and price-competitive offering that is helping it gain market share limits downside risk.

July 17th: Goldman Sachs analyst Eric Sheridan upgraded Chewy to Buy from Neutral with a price target of $50, up from $39. The analyst sees a more positive risk/reward skew at current levels and is increasingly more positive on Chewy's ability to maintain 10%-plus sales growth from 2023 to 2027. Chewy has the potential for steady margin expansion over the next five years as it scales private label and healthcare segments at high margins.

June 1st: Goldman Sachs analyst Eric Sheridan raised the firm's price target on Chewy to $42 from $41 but keeps a Neutral rating on the shares after its Q1 results. The company noted continued strength in overall customer spending on its earnings call and despite being given ample opportunity to call out any macro weakness or spin down in spending behavior, its management continued a theme of seeing their buyer remaining resilient, the analyst tells investors in a research note. The firm adds however that it sees a balanced risk/reward on Chewy shares from current levels.

June 1st: Roth MKM analyst David Bellinger keeps a Buy rating on Chewy with an unchanged $52 price target while reiterating the firm's Top Pick call on the stock. The company reported a "very clean" Q1 as net active customers improved sequentially from Q4, with management indicating attrition levels are now steadying. The firm sees "material upside" in Chewy shares from here as customer counts improve in coming quarters and with international expansion likely not being as disruptive as some thought.

June 1st: Deutsche Bank analyst Lee Horowitz raised the firm's price target on Chewy to $37 from $35 and keeps a Hold rating on the shares. Chewy reported Q1 results well ahead of expectations, with active customers growing modestly versus expectations of a decline, revenue ahead * Chewy reported 1Q results well ahead of expectations, with active customers growing modestly versus expectations of a decline, and and a meaningful adjusted EBITDA beat given gross margin that was buoyed by a less intense discounting environment, the analyst tells investors in a research note.'

June 1st: UBS analyst Michael Lasser raised the firm's price target on Chewy to $26 from $24 and keeps a Sell rating on the shares. Chewy's Q1 results signal that its execution is improving, but the company's inability to generate new customer growth is "worrisome,"

June 1st: Gordon Haskett analyst Greg Sommer upgraded Chewy to Buy from Hold with a $40 price target. The company reported a strong Q1 print with EBITDA upside and its guidance provide more visibility, the analyst tells investors in a research note. The firm says the 35% pullback in the shares since its early February initiation has created a more compelling entry point.

June 1st: Barclays raised the firm's price target on Chewy to $35 from $33 and keeps an Equal Weight rating on the shares. The company's broad-based beat and solid Q2 guidance "should be well received," the analyst tells investors in a research note. Chewy's raised fiscal year guide still implies a softer seocnd half, which may prove conservative, says the firm. It thinks the shares will head higher near term.

May 3rd: Raymond James upgraded Chewy to Outperform from Market Perform with a $36 price target after assuming coverage of the name. The drag on Active Customer growth from the churn of "COVID cohorts" is lessening, and the firm sees a positive inflection in 2H23, the analyst tells investors in a research note. The firm sees trends improving q/q and views Chewy as having multiple levers to drive growth and better margins over the long-term.

April 20th: Guggenheim lowered the firm's price target on Chewy to $45 from $50 and keeps a Buy rating on the shares. The firm is updating its detailed market share analysis given the recent release of Euromonitor's 2022 Pet Care Industry data and reducing its out-year market share assumptions for Chewy, which leads to its lower target.

April 19th: Argus initiated coverage of Chewy with a Hold rating. Over the past four years, the company's revenue has increased nearly 200% to $10B and its gross margin has expanded by 800 basis points to 28%, but Chewy will likely face earnings pressure in the near term from a post-pandemic decline in online ordering, substantial investment spending, and weaker economic conditions, the analyst tells investors in a research note. Argus sees FY24 EPS down 80% at 2c per share before renewed growth in FY25 to 13c per share.

April 11th: JMP Securities analyst Nicholas Jones initiated coverage of Chewy with an Outperform rating and $50 price target. The company's "dominant position" within pet-related retail and services positions it well to capture a "highly impassioned audience that is increasingly humanizing their pets," the analyst tells investors in a research note. The believes this consumer behavior should continue to increase the premiumization of pets, driving consumers to allocate more discretionary spend to those pets longer term. In addition, Chewy's auto-ship subscription model adds more predictability into future revenue than typically seen in an e-commerce marketplace.

March 23rd: Evercore ISI lowered the firm's price target on Chewy to $53 from $55 and keeps an Outperform rating on the shares. Chewy posted a mostly beat and mixed EPS results, the analyst tells investors. Its Q4 revenue, EBITDA, and Gross Margin were above the street consensus, however its active customers saw the steepest decline on record and its outlook was mixed, the firm says. While Chewy had solid margin expansions, reported international expansion, and its gross adds remained resilient, its net adds trend remain "very weak" and its margin guide also disappointed, the firm argued. Evercore ISI came away from this quarter "largely neutral."

March 23rd: Deutsche Bank analyst Lee Horowitz downgraded Chewy to Hold from Buy with a price target of $35, down from $41. Users returned to declines in the Q4, with Chewy seeing users decline by 120,000 in the quarter, the analyst tells investors in a research note. The company's outlook for 2023 suggests that while users will flip positive this year, the magnitude of that user growth is "likely tepid at best," says the firm. It believes investors need confidence in the company's user growth trajectory to justify stock upside, and believes "that is in short supply for Chewy at the moment." Deutsche awaits signs of more sustainable user growth and a return toward margin expansion before growing more constructive on the shares again.

March 23rd: Barclays analyst Trevor Young lowered the firm's price target on Chewy to $33 from $35 and keeps an Equal Weight rating on the shares post the Q4 results. The analyst says the declines in active customers raises questions "as headwinds should have been abating." Chewy's fiscal 2023 margin outlook is softer than expected and while its international expansion is moving to the forefront, details are still light, the analyst tells investors in a research note.

Technicals

As you can see from this first chart which goes all the way back to the 2019 IPO, CHWY is now trading below the IPO price despite revenues being up 133% since FY2020. If you were looking to trade CHWY or start a position, perhaps it’s worth a shot as it gets closer to the 52-week low and all-time low although you’d probably want to use a stop loss in case it slices through. Even if CHWY doesn’t report a beat & raise this week, I don’t think the stock is going much lower from here, I’d expect buyers to step in at the all time low unless CHWY reports a big miss and lowers guidance in which case I’d stay away.

The technicals for CHWY are horrible, the stock is down ~40% over the past couple months but sentiment can’t get much worse so it’s possible we’re getting closer a price where the stock becomes attractive enough to start a long-term position. If you’re a trader this is not a stock to waste your time with but if you’re an investor CWHY is definitely interesting in the low $20s.

Additional Sources

Management – https://investor.chewy.com/governance/executive-management/default.aspx

Board of Directors – https://investor.chewy.com/governance/board-of-directors/default.aspx

Ownership – https://www.sec.gov/ix?doc=/Archives/edgar/data/0001766502/000114036123028028/ny20006317x2_def14a.htm#tS1 (page 25)

Conclusion

I like CHWY as a company and like their expansion into new pet-adjacent categories given their large and loyal customer base but I’m worried about growth and margins plus expanding into international markets is never easy or cheap.

I’m also worried that the private equity firm that acquired PetSmart (which included CHWY) still has a very large position in CHWY and will need to sell down that position over time in order to return capital to their limited partners and/or make new investments. This could be a headwind for the stock.

I’m not interested in CHWY at $25.76 before they report earnings this week but it’s possible I’d get more interested if CHWY dropped below $20 in the coming weeks/months or reported some strong numbers and raised guidance which might give me hope that growth isn’t slowing as fast as feared. I certainly don’t expect CHWY to accelerate growth in a big way so for me I think margins are more important, if CHWY get expand net income margins by more than 1% per year then I think the stock could have more upside over the next few years than my investment model currently shows.

If you like CHWY and use their products want to own the stock for the next 3-5 years, I do think you can start averaging into a position, but whether you wait until after this upcoming earnings report is your decision.

Enjoy the rest of your weekend!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.