Part 2: Deep dive on Axon ($AXON)

In order to read this entire deep dive on Axon ($AXON) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (+104% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio and trading portfolio (fwiw, my trading portfolio is up +70% YTD with a much different strategy than my investment portfolio)

Here are my other newsletters…

Company: AXON, formerly known as Taser

Ticker: (AXON)

Website: Axon.com

IPO date: June 2001 (traditional IPO)

IPO price: $13.00 ($0.52 stock split adjusted)

Current stock price: $214.71

Outstanding shares: 74.76 million

52 week high: $229.95 on May 03, 2023

52 week low: $109.31 on September 23, 2022

ATH: $229.95 on May 03, 2023

Market cap: $16.052 billion

Net cash/debt: +$417 million

Enterprise value: $15.635 billion

Headquarters: Scottsdale, Arizona, United States

Number of employees: 2,800+

Average price target from analysts: $235.82

Investor Relations: https://investor.axon.com/home

Q2 2023 Earnings Report [click here]

Q2 2023 Webcast [click here]

Q2 2023 Shareholder Letter [click here]

August 2023 Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1 and 2]

Here is part 1 of the AXON deep dive in case you missed it…

Below the paywall is the Axon ($AXON) deep dive along with links to my investment portfolio (up +104% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here]

My investment models [click here]

My daily webcasts [click here]

Valuation

As I stated in part 1 of this deep dive, I really like AXON as a company, platform, management team, proven execution, market penetration, etc but my biggest issue is the valuation — if AXON’s market cap was 50% lower I’d already have a position but I’m worried the $15+ billion market cap just doesn’t leave enough upside for shareholders over the next 3-5 years, not unless they crush the estimates you see below, and by crush I meant at least 50% higher otherwise the current P/E multiple will need to contract faster than the combination of revenue and earnings growth can support it.

Today (Sept 13th), AXON closed at 209.86 which means the current enterprise value is around $15.2 billion. Using this enterprise value, it means AXON is currently trading at…

9.9x 2023 EV/SALES and 8.4x 2024 EV/SALES

49.3x 2023 EV/EBITDA and 38.2x 2024 EV/EBITDA

56.5x 2023 EV/NET INCOME and 51.7x 2024 EV/NET INCOME

87.8x 2023 EV/FCF and 57.3x 2024 EV/FCF

These are rich multiples for a company with the growth rates you see below. I’m willing to pay 50x EBITDA but only if they’re growing EBITDA by 50-60% for the next few years. EBITDA growth in the 30% range does not justify this multiple.

Same goes for the net income or earnings multiples, paying 56x earnings is fine if earnings growth is growing at 50% or better for the next few years like it will be for companies like CELH, TMDX, etc but AXON is not expected to have that kind of earnings growth so paying 51.7x next years net income number could get you in trouble.

However, if you think AXON will do $400M of net income next year, now we’re looking at 49% net income growth in which case the current multiple would be justified. I’m not willing to make this bet. Plus they’d need to put up that level of earnings growth for a few years to rationalize paying that P/E multiple right now.

Investment Model

Unfortunately we don’t have any analyst estimates past 2025 so I had to make up my own numbers. I do think it’s possible that AXON can hit these numbers but it won’t be easy and even if they do it might only get the stock to return 100% over the next 4-5 years which is decent but I think there’s much better opportunities in the market where 200% upside over the next 4-5 years is possible.

If AXON fails to hit my estimates below, the stock will most likely return less than a 10% CAGR over the next 4-5 years unless you’re trading it and you time the exits and entries perfectly.

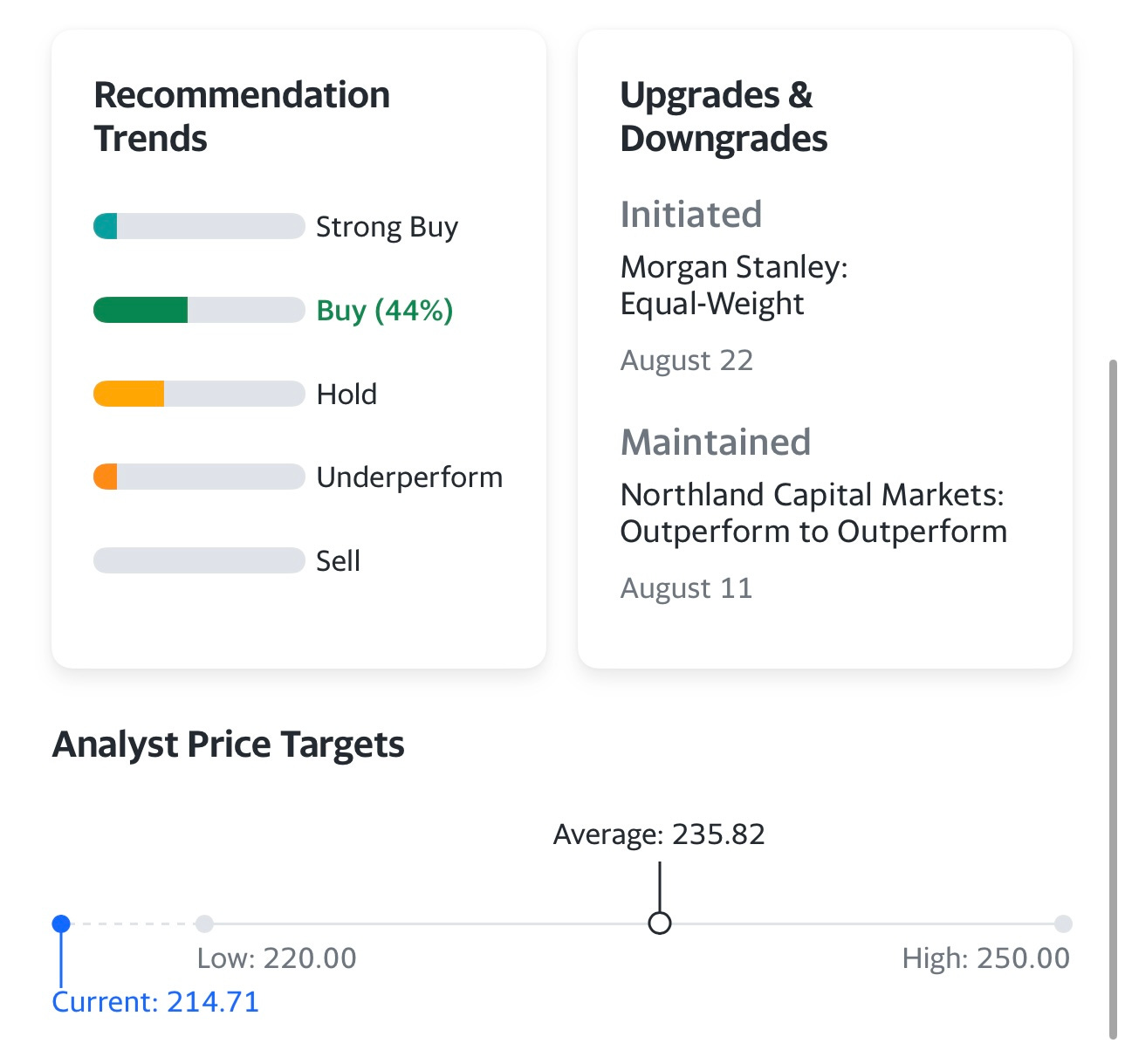

Analysts

Looks like there are 8-10 analysts that actively cover AXON, most of them have buy/overweight ratings with price targets ranging from $230 to $309 with an average price target of $235 to $253 depending on which data source you look at. If you take the midpoint, analysts are looking for approx 16% upside from here which isn’t great but once again AXON has proven an ability to exceed expectations/estimates over the long term so I would not be shocked if they keep doing it.

Here’s what the analysts have been saying:

August 22nd: Axon initiated with an Equal Weight at Morgan Stanley 08/22 AXON Morgan Stanley initiated coverage of Axon Enterprise with an Equal Weight rating and $230 price target. The analyst believes Axon has multiple growth drivers to maintain 20%-25% annual revenue growth over the coming years. However, this is largely reflected in the stock's valuation, the analyst tells investors in a research note. The firm says that if Axon more aggressively went after its international opportunity or meaningfully improved its profitability profile, it could turn more positive on the shares.

August 11th: Northland analyst Michael Latimore raised the firm's price target on Axon to $235 from $227 and keeps an Outperform rating on the shares. Axon posted 62% cloud revenue growth, "ranking it as one of the fastest growing SaaS businesses," while Q2 demand was "broad based beyond that," says the firm. Axon continues to advance its products and the new TASER 10 and Body 4 "hold great potential," the analyst tells investors.

August 9th: Needham keeps a Buy rating and $240 price target on Axon (AXON) but adds the name to the firm's Conviction List in place of Hubspot (HUBS) following the company's Q1 earnings beat. The analyst sees greater visibility around demand and manufacturing for T10 and AB4 that will result in ongoing revenue trends above expectations. Needham further notes that Axon also remains simultaneously focused on profitable growth and margin expansion.

May 11th: Baird analyst William Power raised the firm's price target on Axon to $240 from $237 and keeps an Outperform rating on the shares. The analyst said while we acknowledge what remains a high valuation, we remain positive on the near- and long-term fundamentals and would be buyers on the weakness.

May 11th: JPMorgan analyst Paul Chung upgraded Axon to Overweight from Neutral with an unchanged price target of $236. The analyst tells investors to take advantage of the 15% decline in the stock price yesterday post the earnings print. The pullback the firm was waiting for came sooner than expected, driven by temporary headwinds ahead of a strong upgrade cycle across body cams and Taser 10, the analyst tells investors in a research note. The firm says Axon's gross margins are taking a hit on product mix shift o Fleet and ramp in second half of 2023 product releases, which will ultimately drive higher bundle revenue and buoy overall annual recurring revenue longer term.

May 10th: Credit Suisse raised the firm's price target on Axon to $309 from $300 and keeps an Outperform rating on the shares. The firm cites a strong start to 2023, with revenue/adjusted EBITDA well above Credit Suisse estimates, driven by beat in all segments, especially Software and Sensors. Gross margin was softer than expected, primarily due to higher-than-expected Fleet 3 shipments. The firm also points out that management raised full year 2023 top-line and adjusted EBITDA guidance, another positive.

May 10th: Barclays analyst Tim Long raised the firm's price target on Axon Enterprise to $256 from $222 and keeps an Overweight rating on the shares. The company delivered strong Q1 revenue, Adjusted EBITDA and earnings, all materially ahead of estimates with growth in both reporting segments, the analyst tells investors in a research note.

Technicals

As you can see here, AXON is up 10x from just 6 years ago when the stock was around $20. Kudos to anyone that bought the stock in 2017 or earlier and held on because it dropped 60% from the 2021 highs to the 2022 lows. This is why patience through pullbacks is so hard but so important for long-term tax-efficient capital appreciation.

As an investor I’d wait for the stock to pullback 25-30% to the 200w moving average at ~$140 (chart above)

As a trader I’d consider a position if it bounces off the 21/23d ema or I’d wait for a breakout through 217.56 — other spots to buy off a bounce would be the 200d sma at ~$200 or the 200d ema at ~$192

Conclusion

Here’s some fun math… looking back at AXON in September 2017 when the stock was around $20, if we assume the same share count back then (it might have been higher or lower), the market cap (not including cash/debt) would have been around $1.5 billion. They did $43 million in 2017 so ~6 years ago, the stock was trading at 35x next year’s net income. Right now AXON is trading at 51.7x next year’s net income except the difference is AXON grew net income by 63% per year from 2017 through 2023 but nobody is expecting them to replicate that over the next ~6 years. For a stock to 10x in 6 years is a 47% CAGR, in this case it was driven mostly by net income (or earnings) growth. AXON shareholders should not expect anymore multiple expansion from here because net income growth over the next 3-5 years is going to be lower than the current P/E or EV/NI multiple. AXON is one of those stocks that I definitely missed the past few years, I regret not digging into the company last year after it pulled back 60% from the 2021 highs. As I mentioned in the intro, I thought their sales were benefiting from the BLM riots and I didn’t appreciate the tailwinds being created but now AXON is quite the impressive company so the question I have to ask myself is… do I chase at these prices but use a stop loss? do I wait/hope for a pullback? do I start a small 1-2% position with the intention of averaging down? As of this moment, I’m inclined to not add AXON to my investment portfolio because I don’t see 100% upside in the next ~3 years but I’m very willing to put AXON into my trading portfolio once the technicals look a little better.

Even if I started a position in my investment portfolio, I’d be scared to hold those shares into Q3 earnings because any signs for a slowdown in growth or disappointing guidance could easily send the stock down 15-20% in a couple days and I wouldn’t want to put myself in that position.

Additional Sources

Management – https://investor.axon.com/management-team

Board of Directors – https://investor.axon.com/board-of-directors

Ownership – https://www.sec.gov/Archives/edgar/data/1069183/000106918323000019/axon-20230531xdef14a.htm#SHAREOWNERSHIP_845224 (page 21)

If you have any thoughts or questions on AXON or you’re a current shareholder and I missed something important, please feel free to let me know.

Enjoy the rest of your week!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.