Part 1: Deep dive on Axon ($AXON)

In order to read this entire deep dive on Axon ($AXON) you’ll need to become a paid subscriber by clicking the button below. If you’re already a paid subscriber than I thank you for your support. Paid subscribers receive 2-3 deep dives per month plus access to my current investment portfolio (+104.7% YTD), my investment models and my daily webcasts.

I also run a Stocktwits rooms where I post about my investment portfolio and trading portfolio (fwiw, my trading portfolio is up +71% YTD with a much different strategy than my investment portfolio)

Here are my other newsletters…

Company: AXON, formerly known as Taser

Ticker: (AXON)

Website: Axon.com

IPO date: June 2001 (traditional IPO)

IPO price: $13.00 ($0.52 stock split adjusted)

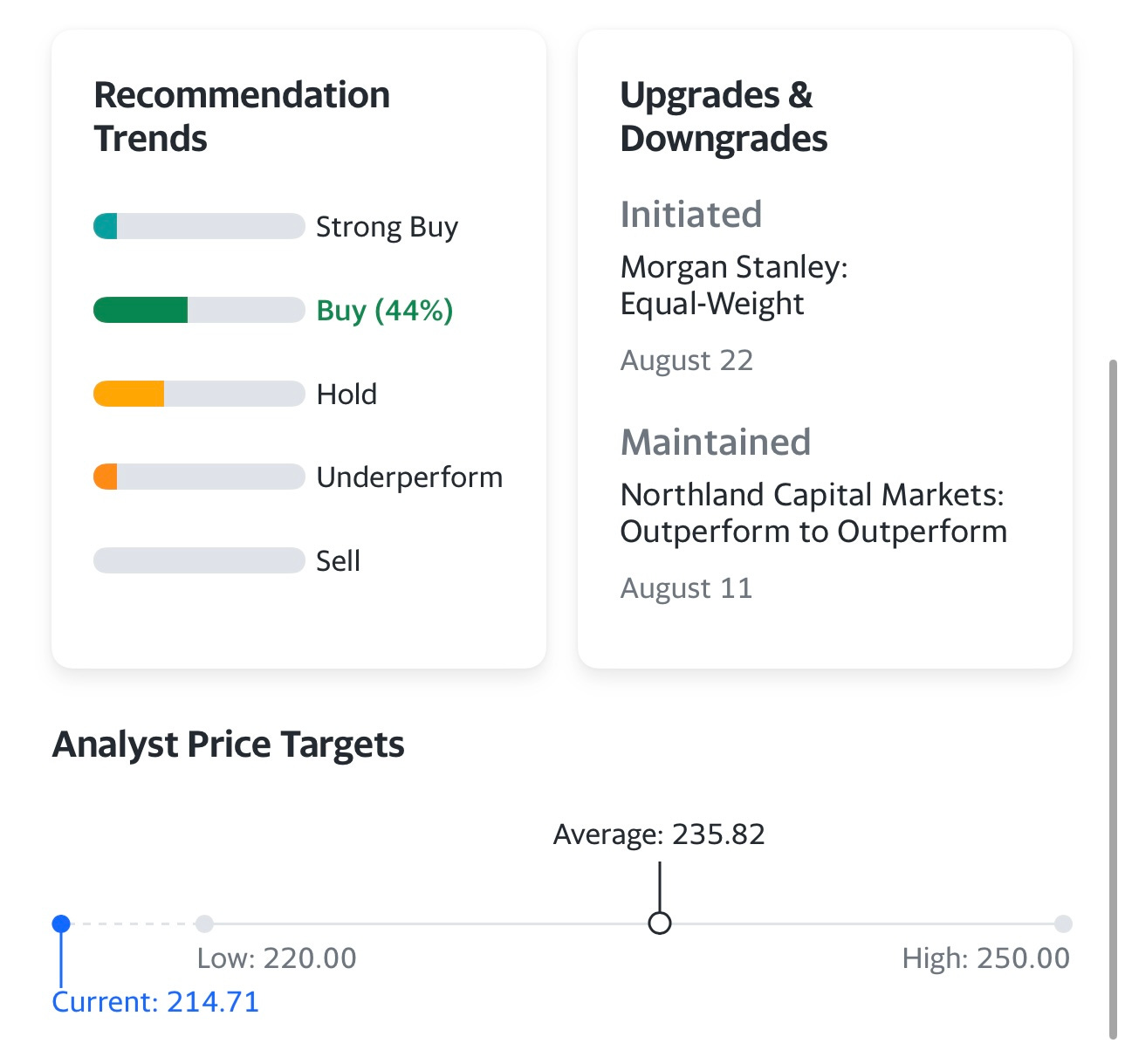

Current stock price: $214.71

Outstanding shares: 74.76 million

52 week high: $229.95 on May 03, 2023

52 week low: $109.31 on September 23, 2022

ATH: $229.95 on May 03, 2023

Market cap: $16.052 billion

Net cash/debt: +$417 million

Enterprise value: $15.635 billion

Headquarters: Scottsdale, Arizona, United States

Number of employees: 2,800+

Average price target from analysts: $235.82

Investor Relations: https://investor.axon.com/home

Q2 2023 Earnings Report [click here]

Q2 2023 Webcast [click here]

Q2 2023 Shareholder Letter [click here]

August 2023 Presentation [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Business Model [part 1]

Competitive Advantages [part 1]

Risks [part 1]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Additional Sources [part 1 and 2]

Below the paywall is the Axon ($AXON) deep dive along with links to my investment portfolio (up +104% YTD), investment models and daily webcasts.

As a paid subscriber you have access to the following:

My investment portfolio [click here]

My investment models [click here]

My daily webcasts [click here]

Introduction

I have a very small position in AXON but it hardly counts given the size. If I made a list of 5-10 stocks that I wish I had been more bullish on the past 3-5 years, AXON would probably be on the list. As you can see, AXON is a 10-bagger since 2017 (~6 years).

Not only does it haunt me that I didn’t own AXON the past 6 years while it went from ~$20 to ~$200 but I actually did own the stock 20 years ago when it was called Taser International and traded under the ticker symbol TASR.

In 2017, TASR changed the company name and ticker to AXON, if I still had those shares from 2003 I’m probably holding a 100-bagger or more.

AXON in 2023 and TASR is 2003 are very different companies. TASR was basically just selling their namesake non-lethal taser guns to law enforcement but AXON is a comprehensive hardware and software company that sells all kinds of products to law enforcement, military, other government agency, security teams and many other types of customers.

One of the reasons I didn’t give AXON enough attention the past couple years is because I thought they were getting an artificial bump in sales from the BLM riots after the death of George Floyd which started forcing law enforcement to begin looking at more non-lethal alternatives when dealing with conflicts. Perhaps that was a turning point for the company and really pushed them into the mainstream while creating a significant tailwind that they’ve done a great job capitalizing off.

I’m not one of these “defund the police” guys, in fact I’m probably the opposite. I think we need to give the police better training (before & during their career), better access to mental health experts and better equipment. The better equipment starts with non-lethal AXON guns as well as body cameras and more advanced communication hardware.

I’m very impressed with AXON’s growth strategy over the past 5 years, considering that 95% of law enforcement departments now use AXON products. What’s exciting for shareholders is that AXON is now putting a bigger focus on international growth which will be important if the company wants to reach $4 billion in sales by 2028 which I think is possible but a chunk of those revenues will need to come from outside the US.

The problem for AXON shareholders or anyone looking to buy the stock is that the current P/E multiple is already quite high (60x 2023 non-GAAP EPS) so 20-30% revenue growth plus some slight margin expansion won’t be enough to take the stock much higher over the next 3-5 years.

In order for AXON to double over the next 4-5 years they will need to crush the current estimates…

One of the reasons I’m not willing to start a position at current prices is because the stock is already trading with a 60x P/E and I think they’ll need to spend some time growing into that multiple. There are simply too many other stocks that I believe have a much better chance of doubling over the next 3-4 years so that’s where I’m putting my capital. With that said, there’s still a chance I’d own AXON in my investment portfolio but I’d have to use stop losses because I don’t want to own the stock if the multiple needs to contract by 40-50% to bring it more inline with the fundamentals. I’m also willing to own AXON in my trading portfolio as long as the technicals remain strong and right now they look good.

Over the past few years we’ve seen the estimates trending higher which is a good thing but 25% revenue growth and 30% EBITDA growth won’t be good enough to justify a 60 P/E multiple.

If we look at EV/SALES and EV/EBITDA multiples over the past 3 years, it looks like AXON is currently trading in the middle. If we get a big market pullback and AXON is trading at 5x sales like it was a year ago and the fundamentals haven’t changed then I’d definitely be looking to start a position, just doubtful that happens. If AXON pulled back 50% it’s probably because they missed on earnings and lowered guidance in which case the multiple is going to get hammered.

For now I’ll keep AXON on my watchlist, along with stocks like ELF that I’d like to own but I have concerns about valuation so I need a pullback or more conviction about what the financials might look like over the next 3-5 years. In order for me to own AXON, I’d need to believe they can get to $4.5+ billion in 2028 with net income margins closer to 25%, if those two things happen then I think shareholders might be happy owning the stock but in all honesty I just think there’s better opportunities out there with more upside potential.

Company Background

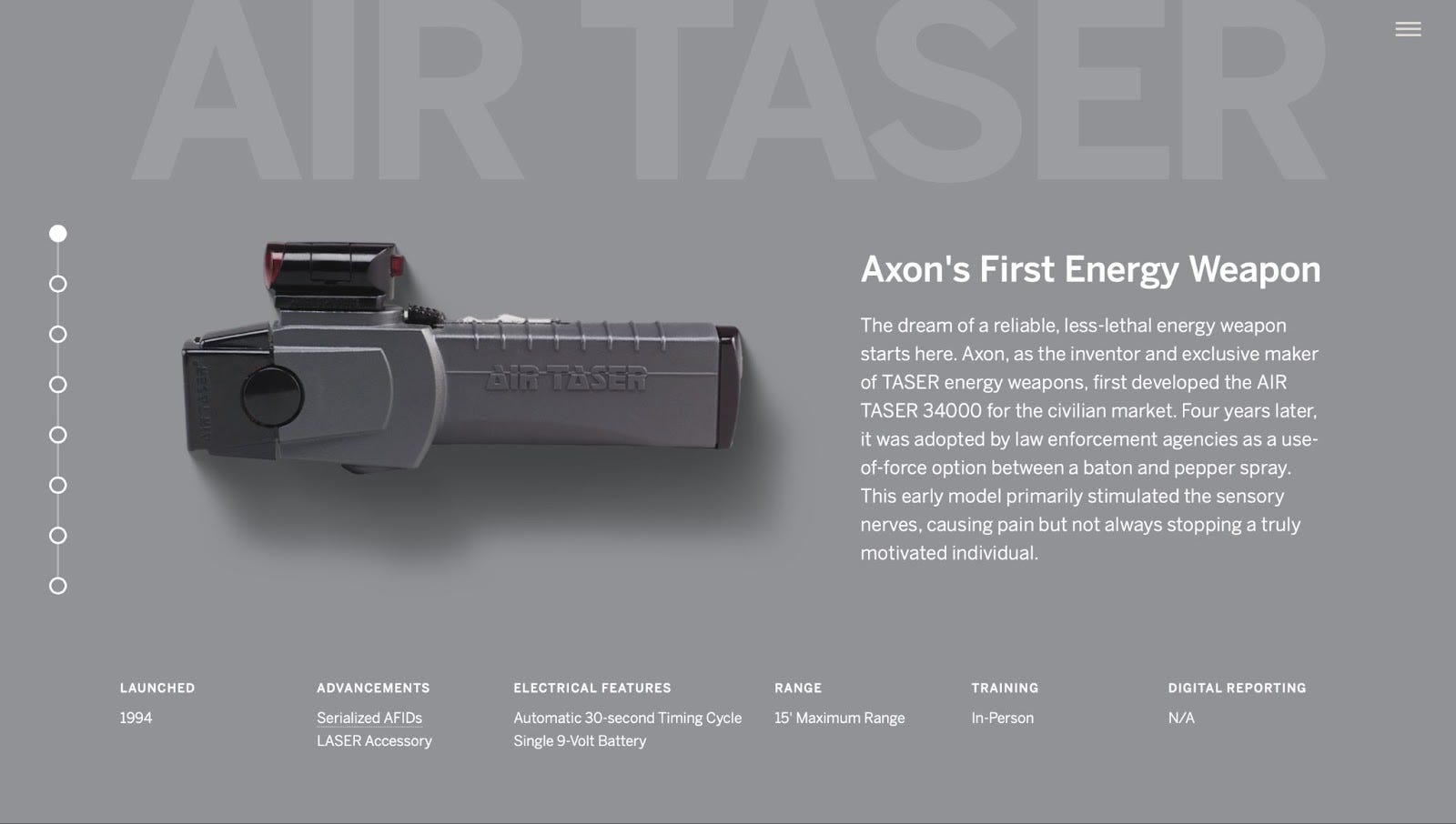

Axon was founded back in 1993 as Air Taser by Rick Smith (who still serves as the CEO and holds 4% of the company, currently worth $612 million) after two of his close friends were shot and killed in a road rage incident.

Because of this tragic event, Smith became passionately interested in the gun violence problem and public safety in general. He believed the solution to this growing problem lies not within large reforms driven by Congress and politicians but rather in technology.

So, Smith began by tackling the traditional firearm first. He wanted to develop a less-lethal alternative, which eventually became TASER, the iconic and most popular energy weapon today.

The original AIR TASER 34000 was launched in 1994 and was initially intended for civilian use. This early model delivered the shock through projectiles directly upon contact with the body within 15 feet, stimulating the sensory nerves. While it certainly caused pain, it did not always stop the assaulting person.

Yet, the device had a growing popularity and, surprisingly, resonated more with law enforcement agencies as they started to increasingly adopt it as a less-lethal device in their toolkit. The demand was actually so high that in the first year of operations, the company sold devices worth several millions of dollars.

As soon as AIR TASER 34000 hit the field, it became clear that just relying solely on pain compliance was ineffective. The company worked for five years to introduce the next model, ADVANCED TASER M26, which caused involuntary muscle contractions by stimulating both the sensory nerves and the motor nerves. This device also allowed users to log and track their usage, including time, date, and duration of each use. These core features became the foundation for all future TASER models.

Despite the growing sales of TASER both in the US and across the ocean, TASER International (the company changed its name from Air Taser to TASER International in 1998) struggled financially. It was costly to produce the device, and the company kept losing money. Smith desperately needed the infusion of capital to keep the company afloat.

In June 2001, TASER International went public, raising approximately $11 million. The stock began trading on NASDAQ at $13 per share ($0.52 stock split adjusted). In three months, the September 11 attacks happened, propelling the company many years ahead of its IPO projections. Orders started to pour in from all over the place, and the company finished 2001 making a profit for the first time in its history.

As TASER became more and more adopted, the need to understand how it is being used in the field was growing. Capturing evidence of events was highly valuable to customers, so the company came up with a solution to implement the camera on the new model of the TASER device, which was launched in 2003. Essentially, it was the predecessor of body cameras, the standard in the industry today.

The TASER CAM was a great innovation at that time, but it had a significant drawback: it could only capture footage during the use of TASER, missing the events before and after the usage. To address this problem, the company developed its very first standalone body-worn camera (mounted on the head and consisting of a camera, a controller, and a monitor to review video recordings) in 2008. That marked the beginning of the camera business for the company.

That same year, the company launched Evidence.com, the software designed to work with a massive amount of digital content that body cameras began collecting. This software enabled users to store and review video evidence at any time. Since then, redaction, transcription, sharing, and other features, which ingest, organize, unify, and share all types of digital evidence, have been added to the Evidence.com platform.

TASER devices, body-worn cameras, and video evidence software were just the start of building an entire ecosystem of products and solutions designed to solve society's most challenging problems, from protecting life to capturing truth to accelerating justice.

In the past decade, the company made meaningful expansion beyond three key products to now include additional products and partner technology such as drones, in-car cameras, Automatic License/Number Plate Recognition (ALPR/ANPR), auto-transcription software, real-time crime centers (RTCC), and even virtual reality de-escalation training.

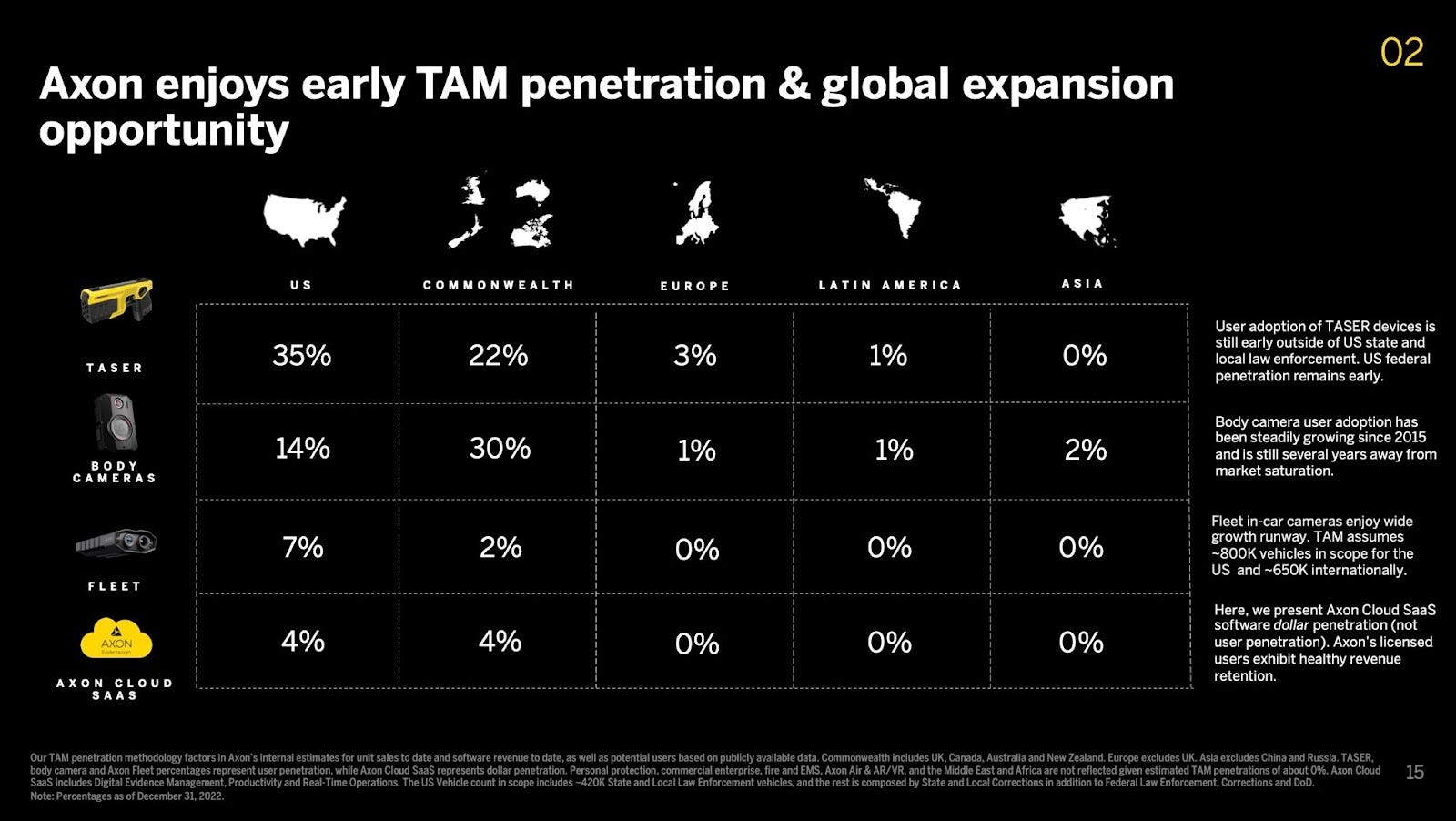

Axon (the company changed its name from TASER International to Axon in 2017) is now a market leader across all categories of products and solutions for public safety in the US. The company serves thousands of public safety agencies across the country on federal, state, and local levels. Over 95% of US state and local law enforcement agencies use Axon's products.

In recent years, the user base has been rapidly expanding beyond law enforcement. Attorneys, fire and EMS personnel, correction facilities, the US military, and other groups and organizations are increasingly adopting Axon's body cameras and software.

And this is just in the US — Axon has been present outside of North America for decades, but the focus was really on the US market all of these years. Only now, the company is making significant steps into European markets and some emerging markets like Brazil, where it wants to replicate the same success as in the US, where its products reached mainstream status.

Smith has played a critical role in Axon's rise. He is an incredibly aspiring founder who has been delivering year in and year out for more than three decades. The results are truly astonishing: through all the ups and downs, the company grew from just a couple of tens of millions of capitalization to $15+ billion today, delivering a mind-blowing 40,000%+ stock appreciation from its IPO price.

And Smith is not planning to slow down. He has an even more ambitious goal, which he calls a moonshot goal: to cut gun-related deaths between police and the public in the United States by 50 percent before 2033 by supplying officers with equipment and technology that makes their jobs safer, easier, and more efficient while maximizing the public tax dollars spent.

At the same time, Axon is on its way to being the first to bring cloud software at scale to public safety, enabling growth for decades ahead.

Opportunity

Axon operates in the defense industry as a technology company, building the public safety operating system of the future by integrating a suite of hardware devices and cloud software.

Public safety today is one of society's top priorities, and it contains a wide range of issues, from preventing criminal activities and responding quickly and effectively to emergencies to managing natural and human-made disasters and promoting the health and well-being of the community.

Trends

There are several trends that drive this augmented focus, from rising crime rates and terrorism to public awareness (the demand by citizens for more safety) and political will (politicians use public safety for election purposes).

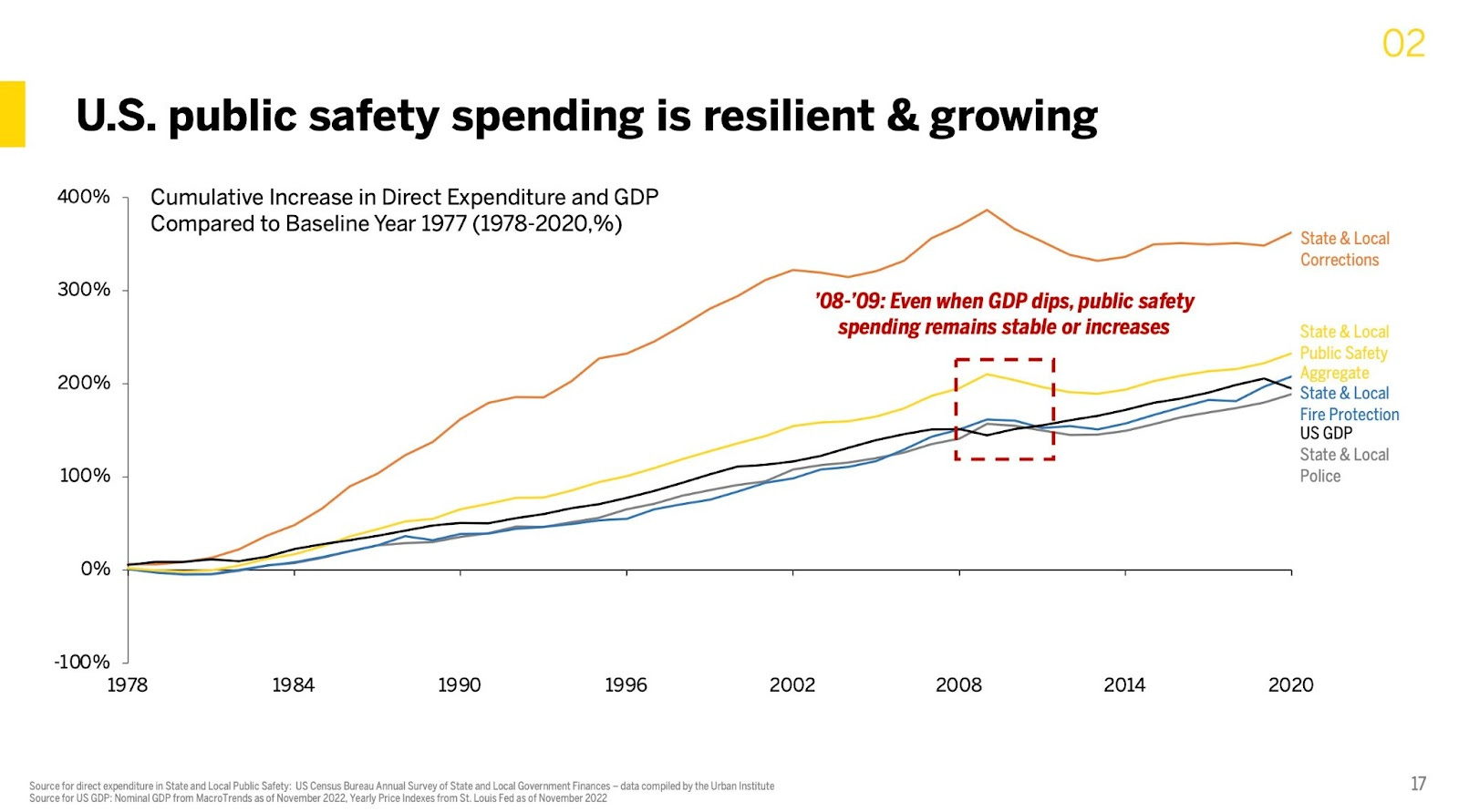

Billions of dollars are invested in this sector by governments all around the world. In the US, public safety spending is a critical component of the overall public expenditure. Over the recent decades, public safety spending has seen consistent growth, regardless of the economic cycle, proving over and over again its resiliency.

More importantly, investments in this sector will only continue to increase going forward, and there are several reasons for this fundamental long-term trend that benefits Axon considerably and provides multi-year growth opportunities.

To begin with, the scope of public safety has been widening in the past several decades. Traditionally, it was primarily police and fire services. After 9/11, it expanded to terrorism and homeland security. With the significant growth of the internet, smartphones, and overall digitalization, cybersecurity has been added to the list. And most recently, the COVID-19 pandemic has shown that public health and public safety are inherently linked. This broadening scope requires increased spending to fully and effectively address all safety challenges of today's society.

Second, technological advancements propelled public safety to the next level. With the advent of advanced CCTV systems, facial and license plate recognition software, and the rising usage of drones, public safety costs have increased considerably and require even more investment.

Furthermore, because of the growing number of communication systems used by different agencies, communication between them is getting more complex, fragmented, and, as a result, more expensive. And not to mention data – a lot of data that is being generated on a daily basis, which requires AI/ML technologies to process and analyze it. AI/ML comes with powerful servers, which are expensive to buy and manage. Perhaps this is the area that will require the most investment in the future.

When all factors are combined, rising public safety spending is inevitable and will only increase in size every year as we advance.

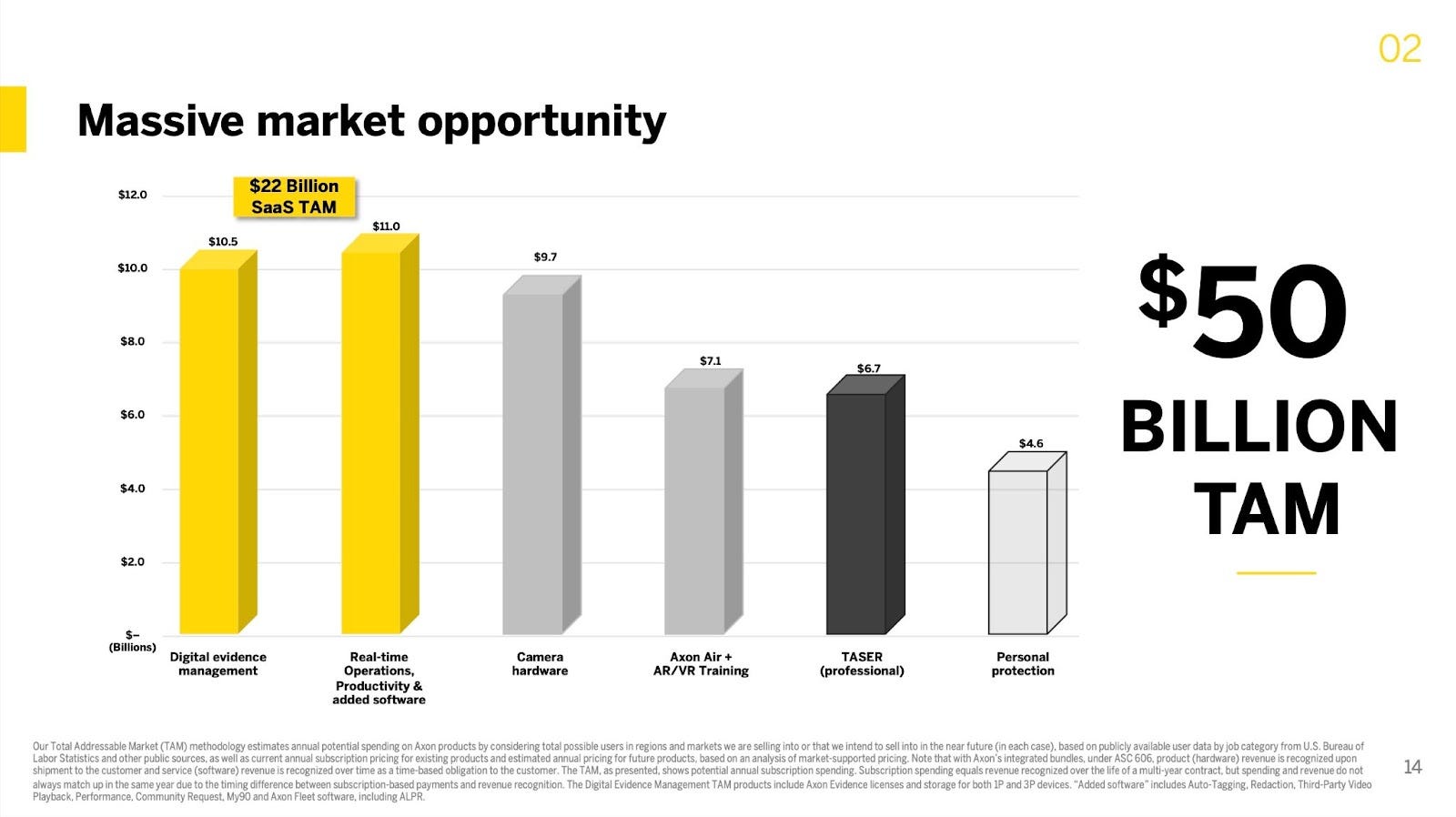

Total Addressable Market (TAM)

Just three years ago, the company estimated that its total addressable market was $27 billion.

By 2023, the total addressable market has almost doubled ($50+ billion), which confirms the growth of public safety spending and also the ability of Axon to introduce new products and solutions that lead to TAM evolving and expanding.

As of Q2 2023, Axon accounted for less than 1% of overall spending on policing in the US. And the company's current contracts with customers represent a tiny percentage (on average, no more than 2%) of their overall budgets. There is so much room for increasing current customers' wallet share.

Growth Drivers

Axon has diversified growth opportunities in several vectors, which can be classified into four large groups:

Selling existing products to new customers

Selling new products to existing customers

Opening new markets and targeting new user profiles

Expanding internationally

TASER

Numerous research studies have shown that the TASER device is the most effective less-lethal weapon, with the lowest likelihood of injury to officers and assaulters.

These results are excellent marketing for TASER, helping Axon continuously grow its adoption among more and more customers. As a result, sales are growing, and the company's market share of a somewhat $11+ billion market segment (which includes both professional use of energy weapons and for self-defense) is increasing.

The company does not stand still and keeps innovating, constantly advancing TASER's main capabilities: shots, range, and accuracy. More shots is vital because suspects are always on the move, and having just two shots (with two probes) decreases the chances of catching them.

More range makes it safer for both the officer and the suspect, while better accuracy makes the usage of the device more efficient.

The result of these innovations recently has been the introduction of the brand-new, next-generation TASER 10. This model began shipping in the first quarter of 2023, and it is a generational advancement in TASER technology.

TASER 10 device features a range of 45 feet (compared to 25 feet in the previous model, TASER 7) to allow more time and space for decision-making and 10 individually targeted probes (compared to just 4 probes in TASER 7) to provide more opportunities to effectively stop a threat and decrease the escalation to lethal force.

"Recently, I met with police chiefs who said, once their officers take TASER 10 out in the field, they will not go out again without it." – Rick Smith.

When paired with Axon Signal, a TASER becomes an even more powerful device for de-escalation, making it a best-in-class less-lethal tool. With wireless alerts sent to nearby Axon cameras when the TASER is unholstered, officers can confidently capture the scene without needing to press a button. This transforms the TASER into a connected device that enhances officer safety and effectiveness.

TASER 10 sets up a multi-year growth opportunity for Axon as many legacy customers are not only looking to upgrade but do it early, a great sign of product-market fit. The company actually has such an overwhelming demand for the new device that its main problem now is how to fulfill this demand in a situation when the supply chain is still recovering.

Currently, the company is building the new TASER by hand, testing the designs in the field with real customers before the company plans to invest in automation manufacturing. This lowers the gross margin in the near term, but the sales of the new TASER 10 are currently a tiny percentage of the mix of all TASER products. At the time when TASER 10 will become a considerable part, the device will be already produced using automated tools on the scale.

Axon VR

A large part of the TASER adoption is training. Providing ongoing training for public safety officers is essential to ensure they can perform their duties to the best of their abilities. But not all training is equal. Traditional police training can be time-consuming, unrealistic, and costly.

Axon was the first to introduce VR training, which takes training to the next level. It allows officers to prepare for real-life situations in the field, simulating "live" scenarios, prompting similar stress responses, and allowing them to build stronger muscle memory during training.

VR training represents a tremendous opportunity for Axon, as it could become the industry standard one day, given its vast benefits, from reduced costs to improved outcomes.

Body Cameras

The body camera technology is evolving fast, yet the implementation rates are still meager. The notion of every law enforcement officer in the country wearing a body camera may seem overly ambitious, but it is likely the direction we are heading. Axon will be a net beneficiary of this trend for many years ahead.

The company recently began shipping (in June 2023) the new body camera, Axon 4. This new body camera completely redefines body-worn technology. Axon's innovation in body-worn cameras goes beyond just making them capture evidence. The company creates absolutely new ways of communication between officers in the field and the office.

Axon Body 4 features bi-directional voice communications (a two-way communication feature, enabling field personnel to share body camera live streams with support teams) and, together with Axon Respond+, provides real-time situational awareness through the ability to locate users on live maps, send alerts, and communicate bi-directionally with support teams. It is the first and only body camera with a voice feature.

The company expects increased sales in the second half of 2023 (6-figure sales), driving most of the body camera shipment volumes for the rest of the year, implying that the company will remove the older model pretty soon. This should also trigger lots of upgrades from Axon 3 to Axon 4 among existing customers.

Software

Software business is, perhaps, the best long-term opportunity Axon has. Not only does software have much higher margins, but it also creates high stickiness and wraps everything into an ecosystem – two very significant competitive advantages.

Axon was the first company to bring public safety to the cloud (with Evidence.com). Prior to Axon, software was custom-built, clunky, run on-premise, slow to update and maintain, did not scale, and had little to no integrations. Axon, in turn, does not provide customization but instead offers a high level of configuration.

Within the software segment, Axon offers a number of products grouped into three categories: productivity software, real-time operations, and mobile apps. The company currently has 18 products in total.

Axon Evidence, the digital evidence management system, remains the main growth driver in the software segment. It is the core SaaS offering and the foundation of what Axon is trying to build: the operating system of public safety, which includes evidence management, police reporting, dispatching police officers to calls, in-car video, drone video, and much more. The company wants to build a one-place-to-go for every police and agency officer in the US.

Within software offerings, there are two particular products that have a high potential. The first one is records management (Axon Records), a whole new growth opportunity for the company. With it, Axon is trying to replace the legacy systems, which have historically been fragmented and complex. There are dozens of vendors, but no one has the dominant position.

Axon Records offers one place for records and evidence, allowing customers to create one dynamic report for every incident. It is designed to save a lot of time for officers and make their reporting work more effective.

The best part about Axon Records is that it is directly integrated into Axon Evidence. The company can easily upsell those customers who already use Axon Evidence.

The company had some initial success with a number of mid-sized agencies. As of Q2 2023, 66 agencies with over 21,000 sworn officers have been using the Records solution, including 19 agencies that are already using this product to replace their legacy records management systems. Revenue associated with this product more than tripled year over year. And there is a large backlog of future deployments.

The second product is Axon Justice, an emerging market for the company. Axon Justice empowers prosecutors and criminal defense attorneys to focus on pursuing justice rather than tedious administrative workflows.

Management sees an opportunity in Axon Justice to make the public tax dollars more efficient and improve law enforcement recruiting and retention by automating mundane, time-consuming tasks. With Axon Justice, the company is developing new data applications that will save customers time while helping to ensure accuracy and justice.

The initial results show a strong demand: bookings of the Justice product have increased by triple-digits in the latest quarter.

New markets

The introduction of products like Axon Justice is an excellent example of how Axon is entering into new markets.

The company is actively diversifying into new markets by adding new types of customer profiles and by adding to its core customer base. In recent years, the company has heavily invested in sales personnel to capture these new markets.

The new markets go beyond law enforcement and now include attorneys, fire and EMS personnel, corrections, the US military, and campus security. There is a further potential to expand to the enterprise for non-police use cases (retail workers that get assaulted and theft detection) and hospital and sports venue surveillance.

New markets have momentum: 4 of the 10 largest deals in Q2 2023 came from new and emerging markets, a sign of continued diversification.

Partnerships will play a critical role in expanding to new markets. Axon actively partners with other innovative technology companies to solve new challenges. For example, connected cameras can be viewed and searched on the Fusus Real Time Crime Center, providing live looks from across town. Or the ALPR technology inside Flock Safety cameras can provide real-time information on the stolen vehicle's location. These solutions can connect to Axon's Body Cameras, Fleet Cameras, and Axon Air Drones to greatly increase the speed at which suspects are found and arrested.

Entering new markets and expanding to new cases is still in the early stage, providing a long runway for growth.

International expansion

The global adoption of Axon products and solutions is another massive opportunity at the early stage. Just 17% of total sales in 2022 came from countries outside of the US, with the UK, Canada, and Australia being the primary contributors.

Axon is only beginning its trials in the European market and taking a first step in emerging markets like Brazil.

Over the past two years, Axon has hosted one of the largest roadshows for public safety in the US and Canada. Its customer-focused roadshow began in 2021 with Axon visiting the 48 states in the United States and several cities in Canada to demonstrate its latest public safety technology.

In 2023, the roadshow expanded to England, Wales, France, Spain, Portugal, Italy, Germany, and Belgium, with the goal of showcasing the global adoption potential of Axon's technology. Each stop

is designed to recognize and celebrate Axon's global customers with localized content, hands-on product demonstrations, networking, and public safety appreciation.

Robotic security

Robotic security is a growing category for law enforcement. Axon has recently made a critical acquisition that will also allow the company to enter this market.

In June 2023, the company acquired a Belgium-based Sky-Hero, which builds a leading indoor tactical drone solution that complements the existing Axon Air strategy. While the acquisition will not be a meaningful revenue contributor in 2023, it fits into the company's long-term vision.

Sky-Hero is already selling to US federal government customers and SWAT teams. The company also sells all across Europe, unlocking many new customer relationships in that region for Axon.

Cybercrime

Cybercrime is a rapidly growing public safety problem, and while it is not yet on Axon's roadmap (at least the company has not announced it yet), entering this market makes perfect sense, given so many established relationships with law enforcement agencies and one ecosystem that Axon offers.

The "predictive policing" technology is the next big thing, and Axon may already be working on it.

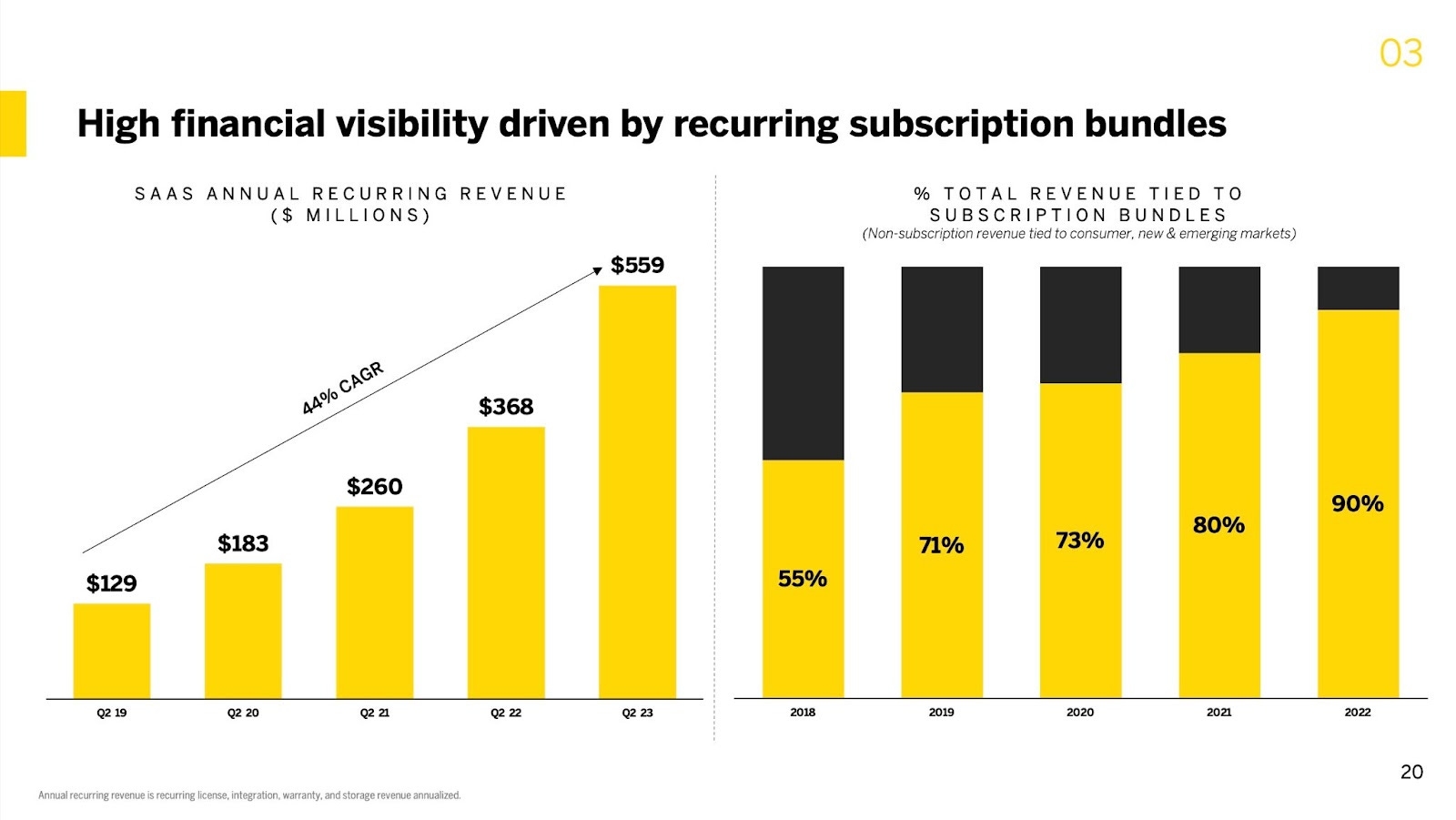

Business Model

Axon's business model is characterized by a high level of recurring revenue (90%+ of total revenue), which comes from selling various products and solutions to a 17,000+ global customer base.

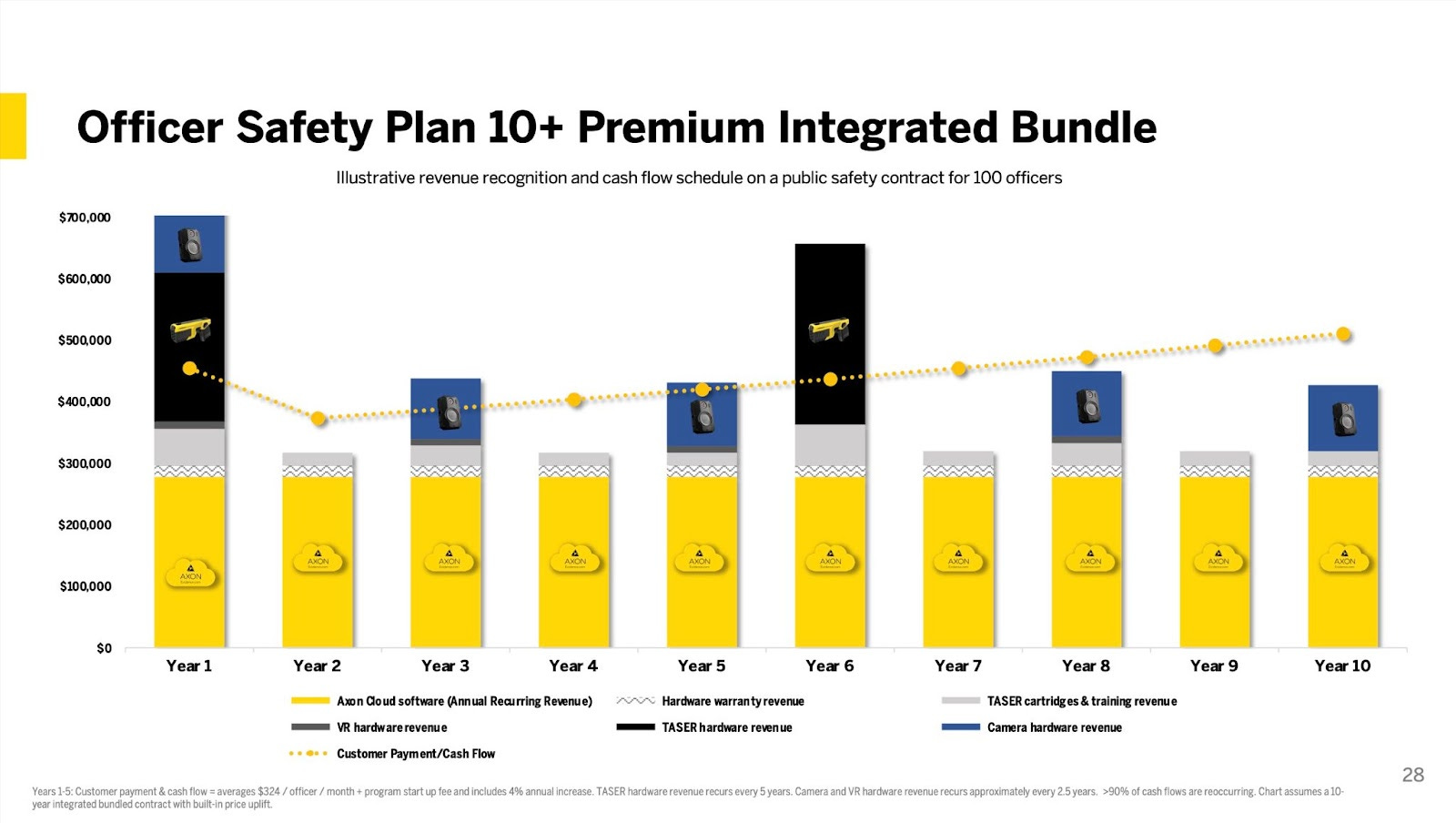

The average contract signed with each customer is 5+ years, providing even more visibility into long-term revenue growth. Each contract has clauses with upgrades to new devices, meaning that each customer, at some point, will migrate from old versions of hardware products to newer ones, and this cycle will repeat all over again with the introduction of new models.

The company is also successfully using a land-to-expand strategy, continuously upselling or cross-selling its existing customers with new products, which is illustrated in a 122% Net Revenue Retention rate.

Revenue Streams

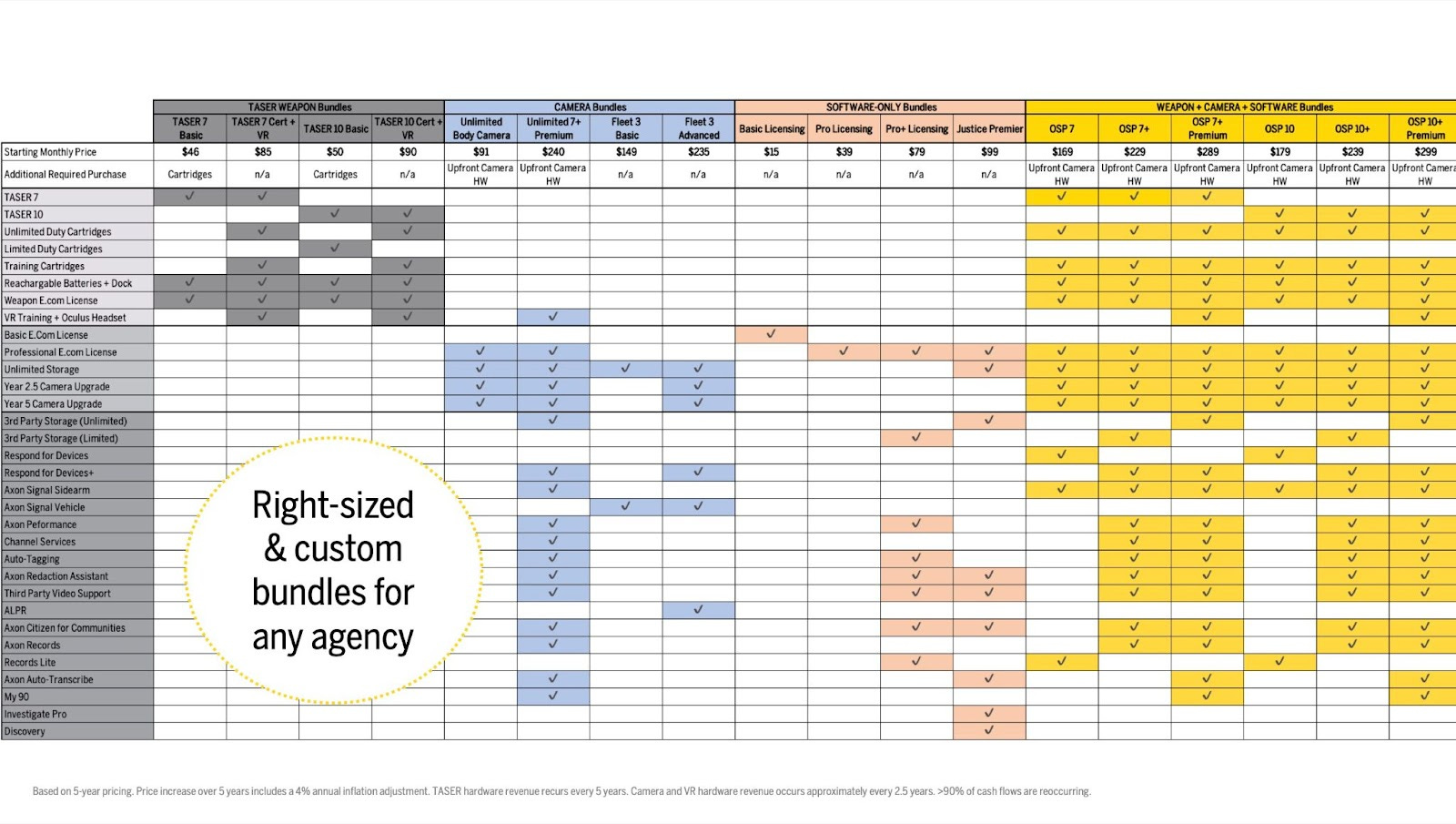

All Axon products are cloud-connected and sold either on a la carte basis or via mutually reinforcing integrated bundles. Customers can pick one of the bundles from three broad product categories:

TASER (TASER 10 or TASER 7 plus Axon VR Training);

Cameras (one of Axon's body cameras, Axon Fleet in-car systems, and other devices that work with Axon software);

Software (many SaaS solutions in three categories: digital evidence management, productivity, and real-time operations).

There is also an option that includes all three product categories in one bundle, called Officer Safety Plan (OSP), which has shown a growing demand in the past several quarters. Every bundle category has several variations.

In the past several years, Axon has been highly successful in pivoting and implementing a strategy to sell all of its hardware products alongside the subscription to its digital evidence management platform (Axon Evidence).

This is reflected in a phenomenal SaaS annual revenue growth since 2016. Total revenue tied to subscription bundles skyrocketed from 34% of total revenue in 2016 to 90% in 2022.

Gross Margin

The total company gross margin has been stable in the past several years at a healthy level of 61% on average. Breaking down the gross margin per product category, the software and services category has the highest gross margin of all (~73%), followed by TASER (~63%) and cameras (~42%).

Software-only gross margin, most of which is annually recurring and includes cloud storage and compute costs, exceeded 80% for the first time in Q2 2023.

The company continues to ramp up Axon Body 4 and TASER 10, limiting the growth of the total company gross margin in the near term.

Financials

As of Q2 2023

Operating Expenses

Operating expenses have improved significantly after a spike in 2020 (63% of total revenue) and 2021 (82% of total revenue) due to the stock-based compensation expense related to the CEO Performance Award and eXponential Stock Performance Plan (XSPP), helping the company return to posting operating income for the first time since 2018.

Operating expenses have been stable since Q1 2022 at 51%-54% of the total revenue level, though stock-based compensation (SBC) remains slightly elevated, primarily due to the recent acquisition and the vesting of the final two tranches of the XSPP program. In the first half of 2023, SBC was almost 10% of total revenue ($66 million) and 0.41% of the company's market cap.

In the past three years, the company increased shares outstanding by 17.6%, while the stock price has appreciated by more than 135%.

Profitability

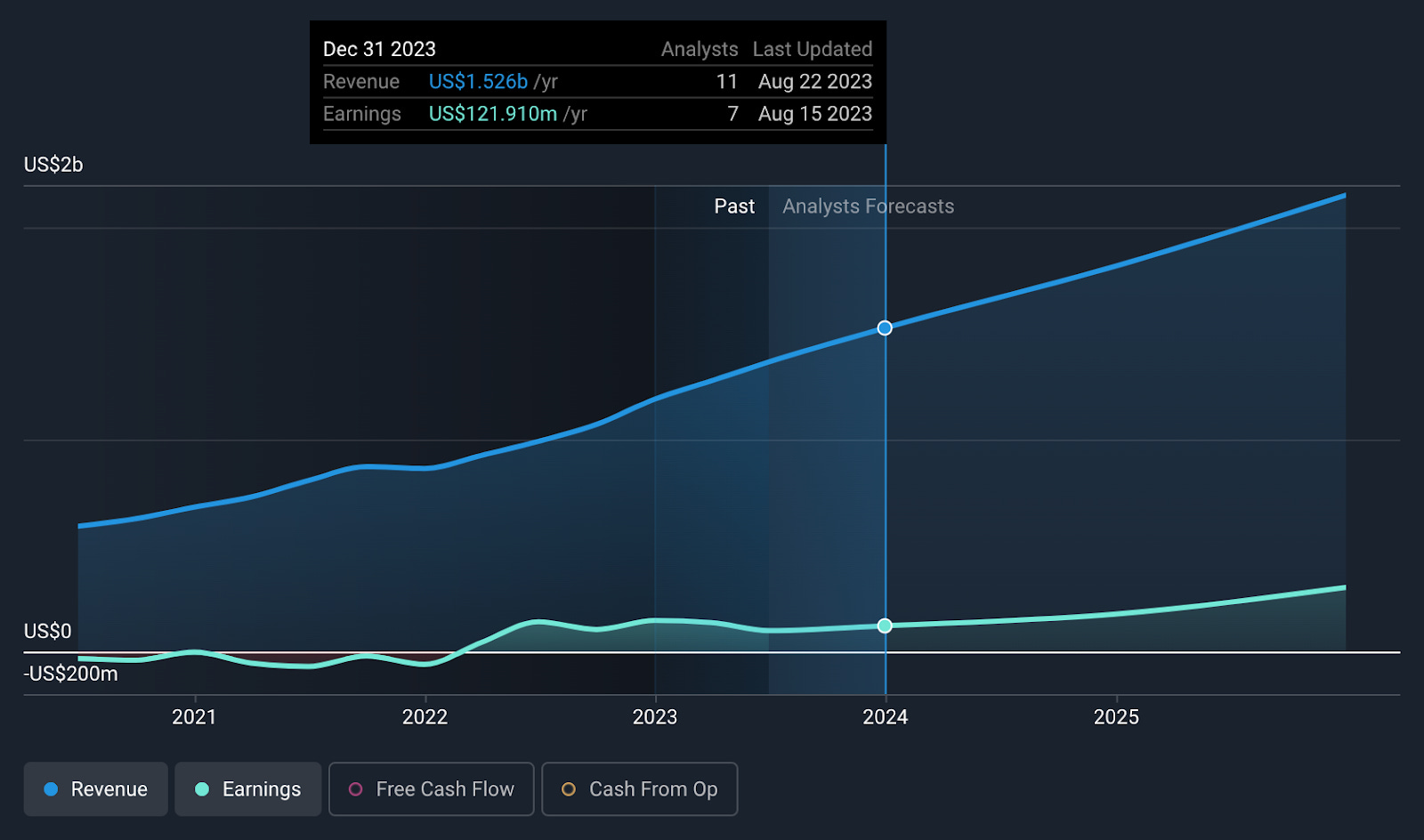

Axon returned to profitability in 2022, posting $147 million in net income after two years of negative earnings.

The analysts' consensus is that Axon will deliver another profitable year in 2023, though earnings will be lower (approximately $122 million) than in 2022 before the company reaccelerates its growth in 2024.

Axon should become a highly profitable company at scale and maturity.

Balance Sheet

Axon had $1.08 billion in cash, equivalents, and investments at the end of Q2 2023 and outstanding 0.50% convertible notes (due 2027) in the principal amount of $690 million.

Cash Flow

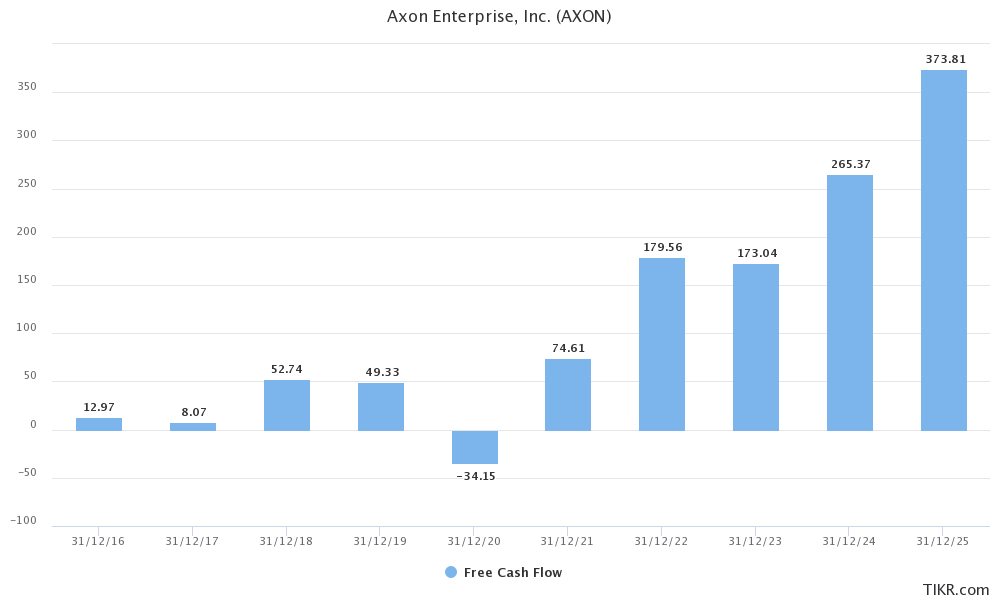

Axon has been robust in generating free cash flow in the past few years. Furthermore, after a slight dip in 2023, the company is projected to reaccelerate FCF generation in the coming years.

Manufacturing

Axon performs light manufacturing, final assembly, and final test operations at its headquarters in Scottsdale, Arizona, US. The company owns all the equipment required to develop, prototype, manufacture, and assemble the finished products, including critical injection molded component tooling.

The company is still recovering from the supply chain challenges of the past several years and continues to take necessary steps to diversify its supply chain and global manufacturing footprint to avoid any challenges in the future.

Distribution

Axon primarily sells its products and solutions to four types of customers:

US state and local governments

The US federal government

International government customers

Commercial enterprises

The company primarily sells to customers through its direct sales force and online store. Building the best sales team in the industry is one of the top priorities of Axon.

No customer represents more than 10% of the company's total revenue.

Competitive Advantages

Competition

Axon faces severe competition in all segments of its business, including the less-lethal alternative weapon segment, where TASER is a clear market leader.

In the body-worn camera and in-car video/automatic license plate readers markets, the company faces competition from a number of companies, among which are Motorola Solutions (offers unified public safety and enterprise security ecosystem), Utility (offers Digital Evidence Management, In-Car Video, and Advanced Body Cameras), Getac Technology (offers solutions to police, fire & rescue, and ambulance), Panasonic (offers various government technologies), Reveal Media (manufacturer of high-performance body cameras and digital evidence management system), Safe Fleet (offers various fleet safety solutions), Digital Ally (offers a complete front and back end solution for body cams, in-car video systems, data solutions, and support for Law Enforcement, EMS, Commercial Fleets), Visual Labs (produces Smartphone Body and Dash Cameras), Intrensic (offers body cameras and digital evidence software), Safety Vision (offers advanced AI mobile video surveillance, cloud-based management and storage solution), Rekor Systems (revolutionary roadway intelligence), and Genetec (provides unified security solutions that combine IP-based video surveillance, access control, automatic license plate recognition, and other solutions).

Axon's cloud-based digital evidence management system, Axon Evidence, competes with other cloud-based platforms of similar functionality (from companies like Motorola Solutions, Panasonic, IBM, Oracle, FotoWare, Vidizmo, NICE, QueTel, OpenText, and FileOnQ among others) and various on-premises-based systems designed by third parties or developed internally by an agency's technology team.

Axon's Records Management System (RMS) and Computer Aided Dispatch (CAD) compete with over 50 software providers, from large corporations to much smaller vendors. Furthermore, Axon faces competition from an old-school way of report writing – paper, as many law enforcement agencies are not using the software at all.

TASER devices compete with various less-lethal alternatives to firearms, including:

rubber bullets or rubber baton rounds (made by Combined Systems);

pepper spray and pepper spray projectiles (made by Byrna Technologies, SABRE, and Mace Security International);

traditional stun guns (made by UZI and Jolt);

hand-held remote restraint devices involving a tether (made by Wrap Technologies);

laser dazzlers that cause temporary blindness (made by B.E. Meyers & Co);

stun grenades (made by Combined Systems);

long-range acoustic devices (made by Genasys);

police batons and nightsticks (made by Monadnock and Armament Systems and Procedures).

Competitive Advantages

Axon beats most of its competitors by simply offering better products and solutions. For example, TASER devices offer advanced technology, versatility, portability, effectiveness, built-in accountability systems, and low injury rates, making them the best less-lethal alternatives. TASER devices can also connect to the cloud network, enabling law enforcement agencies and other professionals to better manage their non-lethal programs and automate use-of-force reporting.

Technology

TASER is an excellent example of the best-in-class technology. But there is so much more innovation going on across all segments.

Axon has been one of the first companies in the industry to start integrating AI capabilities into its products, building a substantial first-mover advantage in implementing this critical technology.

For example, videos collected from Axon body cameras can already be automatically transcribed in less than 5 minutes when uploaded to Axon Evidence, allowing agencies to quickly search and review video evidence for the specific moment when a suspect said something. Eventually, AI would write an entire police report for the officer.

AI now also powers other products like automated license plate recognition (ALPR) products, with many more to come.

Axon is best positioned to adopt generative AI for law enforcement use since all of its products and solutions are cloud-connected. This will allow the company to expand its market leadership position further.

Ecosystem

The ecosystem, perhaps, is Axon's main competitive advantage, something that the company has been building for several decades and that no other competitor can match.

Axon invested hundreds of millions of dollars into building out its ecosystem, which consists of TASER devices, wearable cameras and sensors, and the world's leading cloud platform that securely hosts the enormous data generated by this expansive ecosystem.

Every new product or solution is immediately connected to Axon's ecosystem, enhancing its capabilities and making it more and more powerful. This, in turn, creates high stickiness because law enforcement agencies and other customers are getting locked into using Axon's products only, similar to what Apple does.

The ecosystem advantage has been the key driver of Axon's success in recent years and will only help drive more business in the future.

Brand

The brand also plays a critical role in this industry. Axon has possibly built one of the most recognizable brands. The TASER brand is known to millions of people thanks to its popularization in video games and TV shows.

You will also find the Axon logo in hundreds of police chasing videos on YouTube, including in viral channels like Code Blue Cam and Police Activity, which have millions of subscribers. You won't find products from other companies in more than 90% of such videos.

Risks

Law enforcement customers

Axon substantially depends on the acceptance of its products by law enforcement customers, especially internationally, where it has little adoption yet. The company needs to continuously drive the adoption and usage of its products among as many law enforcement customers as possible.

Brand reputation

Any negative coverage and publicity surrounding Axon's products and services and their use severely impact their sales. There is still a lot of debate on the Internet on whether law enforcement agencies should use TASER devices.

Competition

The public safety industry is receiving significant attention today, with billions of dollars pouring into it. It attracts many companies to develop technology for the law enforcement market. In some areas of the industry, the competition is already so intense that over 50 companies offer their products and solutions.

In addition, while Axon offers the best body-worn camera on the market today, its market share in the US is still 14%, indicating how competitive this market is.

Supply chain

Supply chain challenges remain a risk for Axon, especially when the company sources the majority of components from just one third-party supplier.

In 2022, the revenue generated by TASER 7 was affected by approximately $35 million due to delayed shipment of orders that were scheduled to be fulfilled before December 31, 2022. This delay was caused by a manufacturing component issue for the TASER 7 devices. Similarly, the revenue from Axon Body also suffered a setback of about $15.5 million as orders scheduled for shipment before December 31, 2022, could not be fulfilled because of supply chain constraints for the Axon Body 3 devices.

Development of new products

Axon's future success significantly depends on the company's ability to develop and introduce new products and solutions on time for the next cycle of upgrades. Any delays will affect the company's revenue growth.

International expansion

Axon's products and solutions are slow to get adopted outside of the US and Commonwealth countries. Expansion to Europe, Latin America, and Asia sounds like an exciting opportunity on paper, but it may prove to be much harder and require more resources and time. Countries in these markets may also have different regulations regarding energy weapons, classifying them as illegal.

Additional Sources

Management – https://investor.axon.com/management-team

Board of Directors – https://investor.axon.com/board-of-directors

Ownership – https://www.sec.gov/Archives/edgar/data/1069183/000106918323000019/axon-20230531xdef14a.htm#SHAREOWNERSHIP_845224 (page 21)

Have a great week!!!

~Jonah

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.